United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Molson Coors Beverage Company (NYSE:TAP) presented its second quarter 2025 results on August 5, revealing a complex picture of financial performance amid challenging market conditions. The company reported earnings per share growth despite volume declines across its markets, while simultaneously lowering its full-year guidance due to ongoing industry headwinds.

The brewer’s results come as the U.S. beer industry faces significant challenges, with the company noting that macroeconomic and geopolitical factors are impacting consumer behavior in key markets. Despite these headwinds, Molson Coors managed to beat analyst expectations for the quarter, with earnings per share of $2.05 surpassing the forecast of $1.85 by 10.81% according to recent earnings reports.

Quarterly Performance Highlights

Molson Coors reported mixed financial results for Q2 2025, with volume declines offset by favorable pricing and mix, leading to a smaller decline in revenue and relatively stable underlying income.

As shown in the following consolidated results chart:

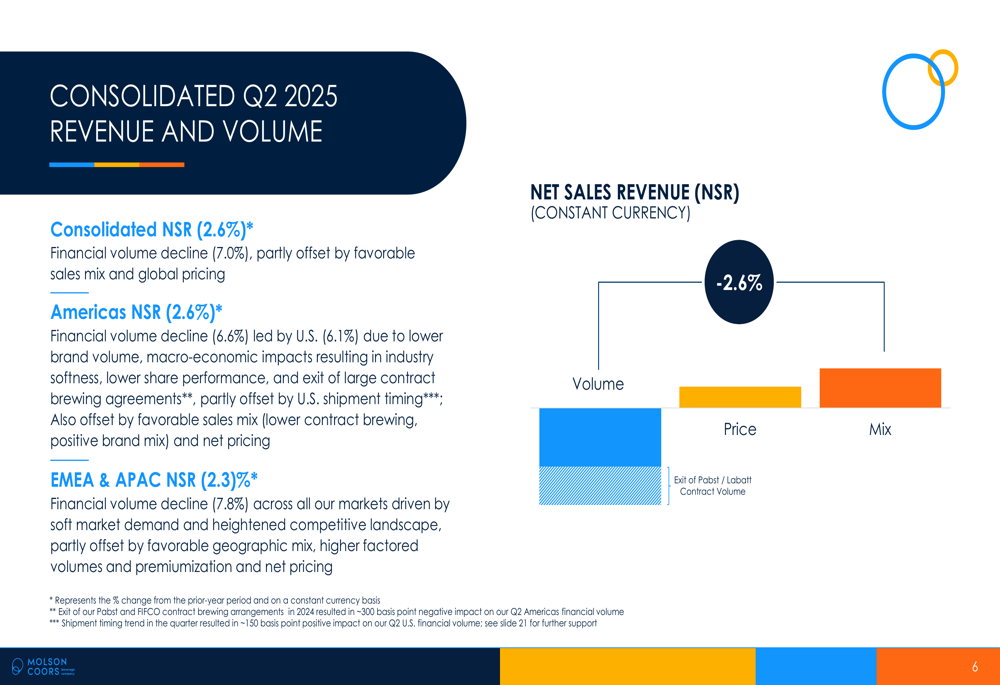

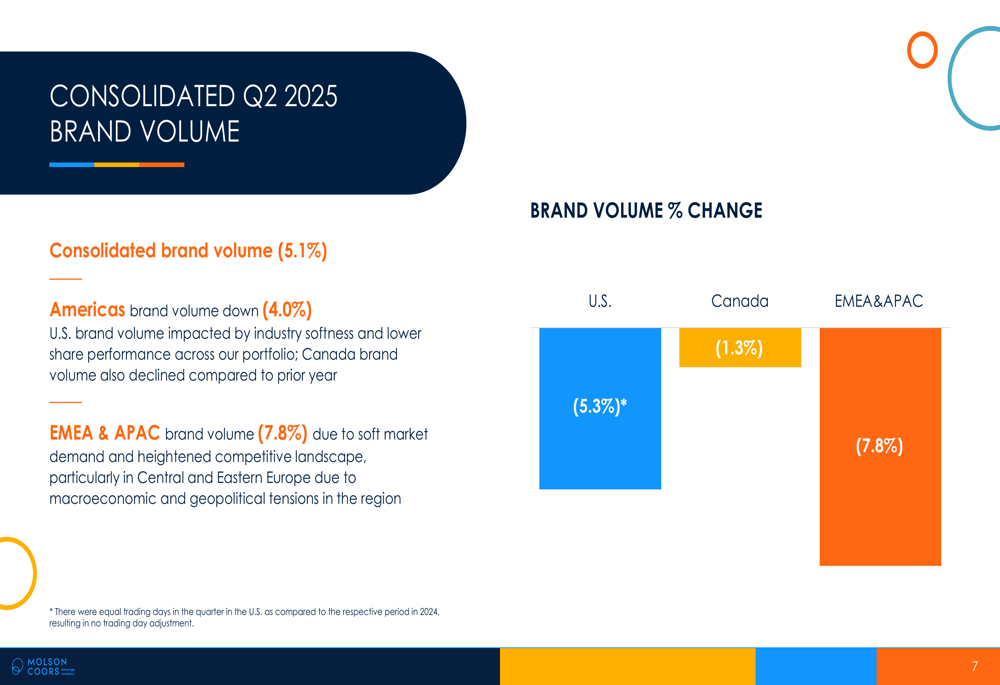

The company’s financial volume decreased by 7.0% year-over-year to 20.870 hectoliters, while brand volume declined by 5.1% to 20.612 hectoliters. Net sales revenue fell by 2.6% to $3.201 billion, though underlying earnings per diluted share increased by 6.8% to $2.05. Underlying free cash flow saw a significant decline of 41.9% to $294 million.

The revenue and volume performance breakdown reveals how pricing and mix partially offset volume declines:

While financial volume declined by 7.0%, favorable sales mix and global pricing helped limit the overall impact on net sales revenue. The company’s brand volume performance varied by region, with Americas down 4.0% and EMEA & APAC down 7.8%, as illustrated in the following chart:

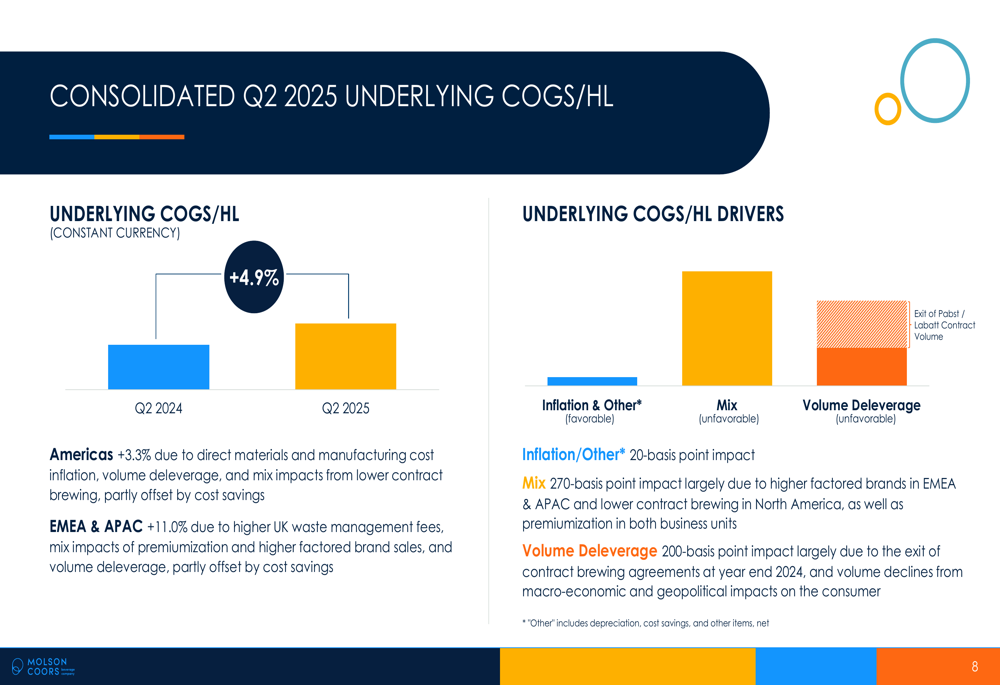

Cost pressures continued to impact the business, with underlying COGS per hectoliter increasing by 4.9% in constant currency:

This increase was primarily driven by mix effects (270 basis points) and volume deleverage (200 basis points), with inflation and other factors contributing just 20 basis points to the increase.

Regional Performance Analysis

Molson Coors’ performance varied significantly by region, with the Americas segment showing more resilience than the EMEA & APAC markets.

In the Americas, net sales revenue decreased by 2.6% to $2.505 billion, while underlying income before income tax increased by 5.4% to $514 million despite a 6.6% decline in financial volume. The company attributed this performance to favorable mix, increased net pricing, lower MG&A expense, and cost savings initiatives, partially offset by lower financial volume and cost inflation.

The EMEA & APAC region faced greater challenges, with net sales revenue declining by 2.3% to $704 million and underlying income before income tax falling by 17.9% to $72 million. Financial and brand volumes both decreased by 7.8%, with performance drivers including lower financial volume and higher UK waste management fees, partially offset by lower MG&A expense, favorable net pricing, and favorable mix.

Despite these challenges, the company highlighted that its core U.S. power brands maintained their collective volume share at 15.2% in the first half of 2025, with Coors Banquet achieving its 16th consecutive quarter of industry volume share growth.

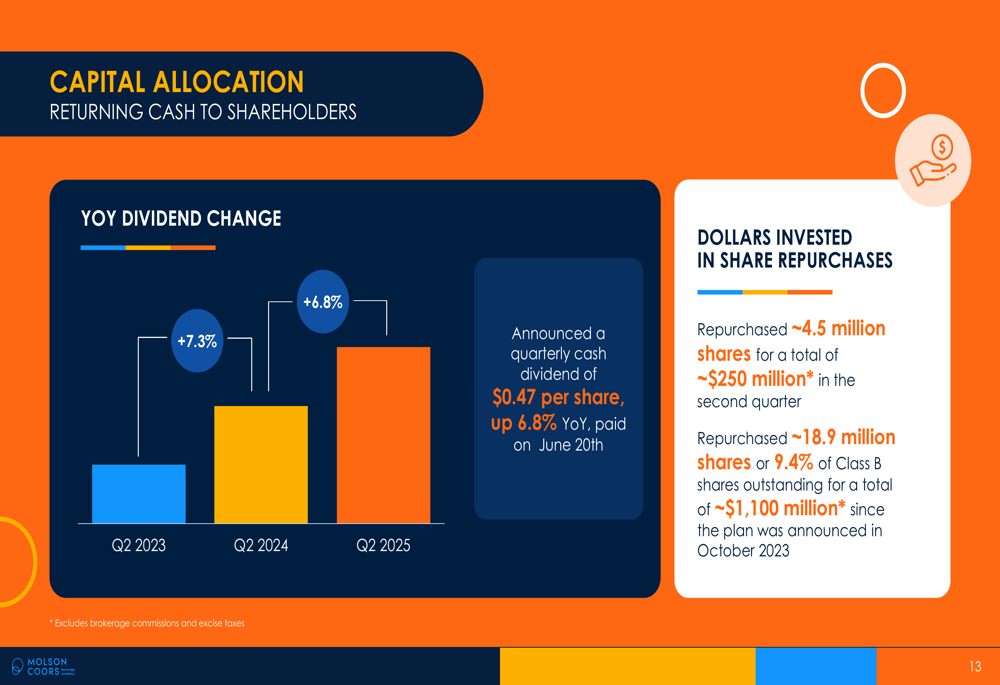

Capital Allocation

Molson Coors maintained its disciplined approach to capital allocation, balancing investments in the business, debt management, and shareholder returns.

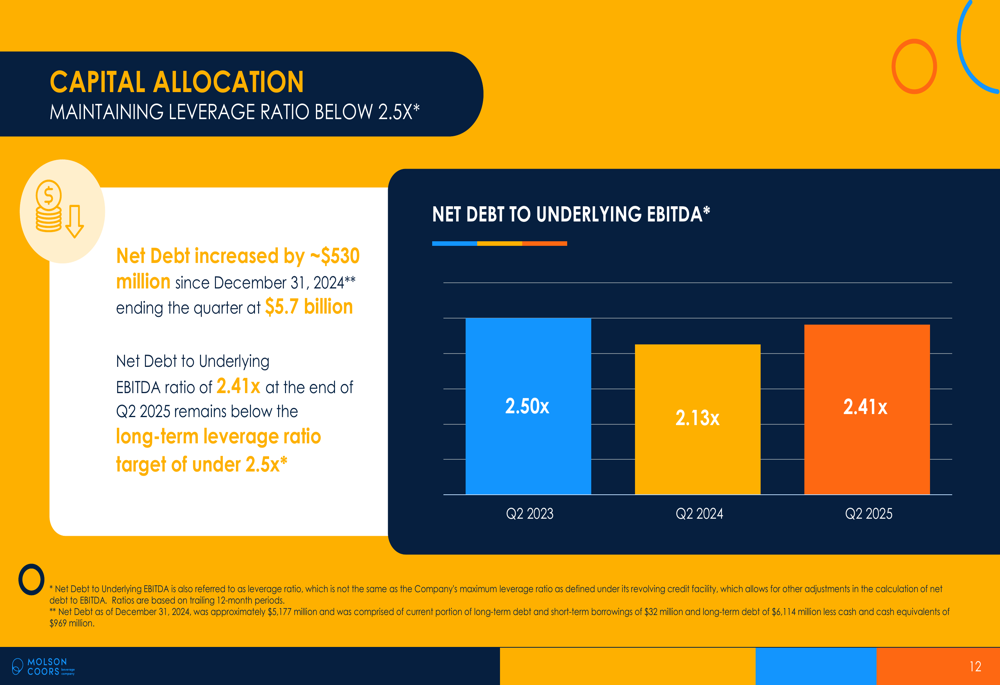

The company’s leverage ratio remained below its long-term target of 2.5x, ending Q2 2025 with a Net Debt to Underlying EBITDA ratio of 2.41x:

While net debt increased by approximately $530 million since December 31, 2024, ending the quarter at $5.7 billion, the company continues to maintain a strong balance sheet.

Molson Coors also continued its commitment to returning cash to shareholders, increasing its quarterly dividend by 6.8% year-over-year to $0.47 per share. The company repurchased approximately 4.5 million shares for a total of around $250 million in the second quarter, bringing the total to approximately 18.9 million shares (9.4% of Class B shares outstanding) for about $1.1 billion since the repurchase plan was announced in October 2023.

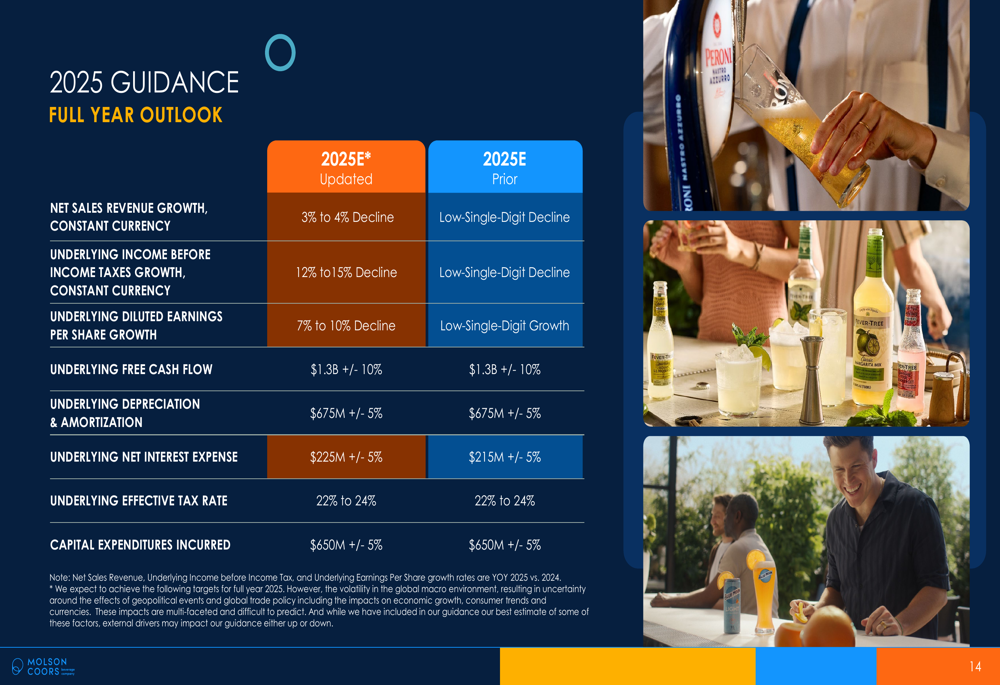

Revised Guidance & Outlook

In light of the challenging market conditions, Molson Coors revised its full-year 2025 guidance downward:

The company now expects a 3% to 4% decline in net sales revenue (constant currency), a 12% to 15% decline in underlying income before income taxes (constant currency), and a 7% to 10% decline in underlying diluted earnings per share. However, Molson Coors reaffirmed its underlying free cash flow guidance of $1.3 billion (+/- 10%).

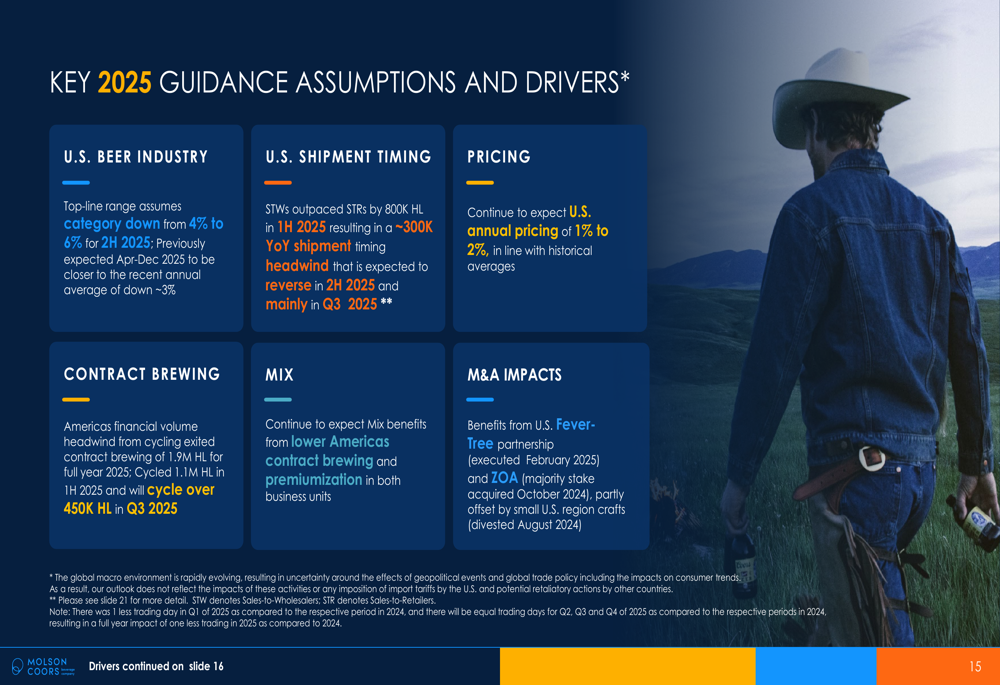

These revisions are based on several key assumptions, including:

The U.S. beer industry is expected to decline by 4% to 6% in the second half of 2025, with U.S. annual pricing projected at 1% to 2%. The company also anticipates mix benefits from lower Americas contract brewing and premiumization, as well as impacts from the U.S. Fever-Tree partnership and ZOA, partly offset by small U.S. region crafts.

Despite the near-term challenges, Molson Coors emphasized its continued focus on its long-term growth strategy, centered around its four-pillar acceleration plan: growing core power brand net revenue, aggressively premiumizing its portfolio, scaling and expanding in beyond beer, and supporting its people, communities, and planet.

CEO Gavin Hattersley, according to recent earnings reports, characterized the current market challenges as "cyclical," suggesting confidence in the company’s ability to navigate the current environment while maintaining its strategic direction.

As of September 15, 2025, Molson Coors’ stock was trading at $48.42, up 0.13% for the day, but near its 52-week low of $46.94, reflecting ongoing investor concerns about the revised guidance despite the company’s Q2 earnings beat.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.