Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

Monro, Inc. (NASDAQ:MNRO) presented its first quarter fiscal 2026 results on July 30, 2025, showing continued sales momentum despite ongoing margin challenges. The automotive service provider’s stock has been recovering from significant declines, with shares currently trading at $16.32, up from the 52-week low of $12.19 but still well below the 52-week high of $31.49.

The company’s presentation comes after a challenging fourth quarter of fiscal 2025, when Monro reported a net loss but saw its stock surge nearly 25% as investors responded positively to strategic operational changes. The first quarter results suggest these initiatives are beginning to gain traction, though profitability pressures persist.

Quarterly Performance Highlights

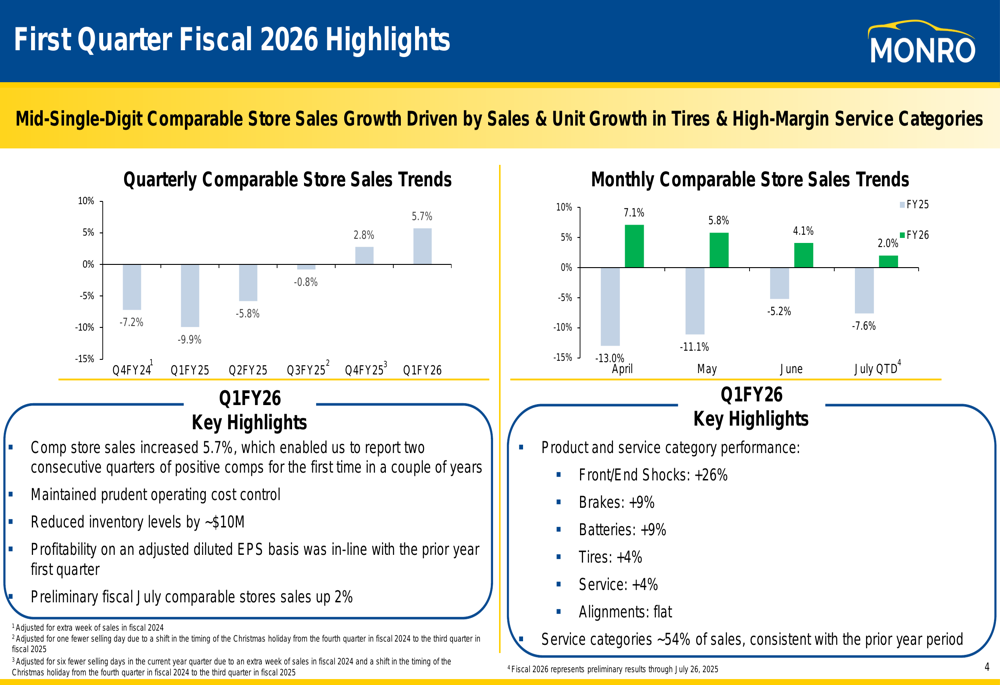

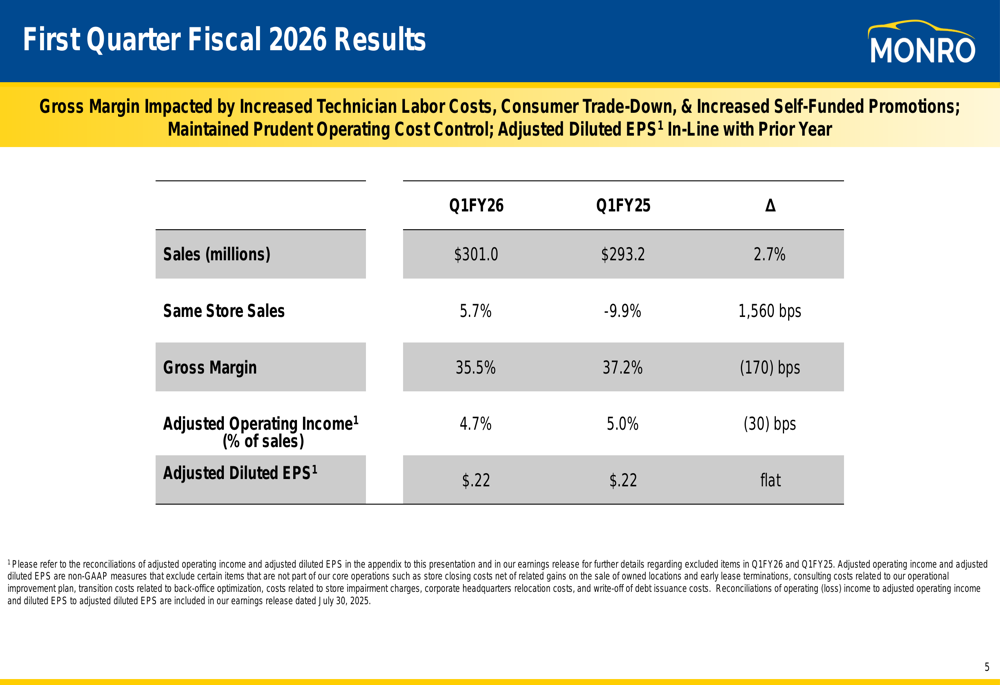

Monro reported a 5.7% increase in comparable store sales for Q1 fiscal 2026, a significant improvement compared to the 9.9% decline in the same period last year. This represents a 1,560 basis point swing in performance. Total (EPA:TTEF) sales reached $301 million, up 2.7% from $293.2 million in Q1 fiscal 2025.

As shown in the following chart of quarterly and monthly comparable store sales trends:

Product category performance varied significantly, with front-end shocks leading the way at 26% growth, followed by brakes and batteries (both up 9%), while tires and service categories each grew by 4%. Alignments remained flat. Service categories continued to represent approximately 54% of total sales, consistent with the prior year period.

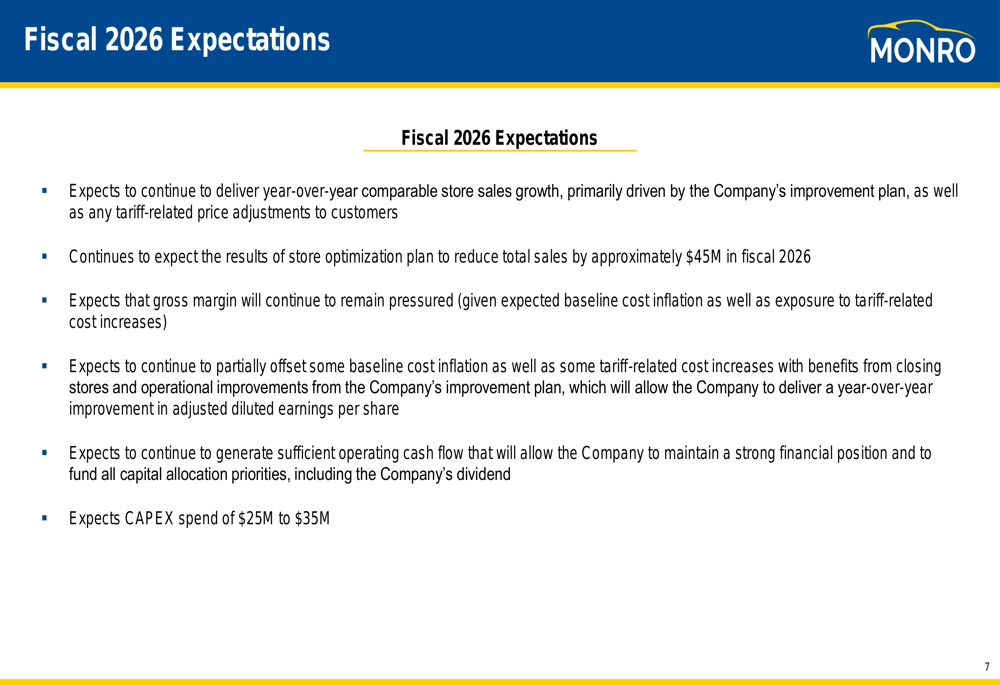

Despite the sales growth, Monro’s gross margin declined to 35.5% from 37.2% in the prior year period, a decrease of 170 basis points. The company attributed this decline to increased technician labor costs, consumer trade-down, and increased self-funded promotions.

The following table summarizes the key financial metrics for the quarter:

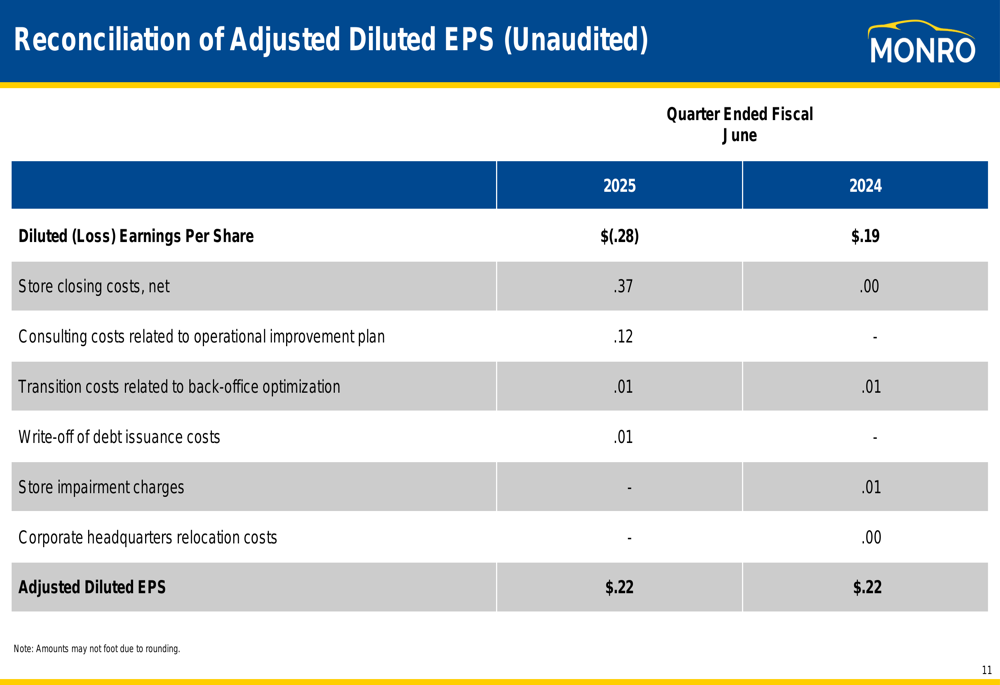

Adjusted operating income as a percentage of sales declined slightly to 4.7% from 5.0% in the prior year period. Adjusted diluted earnings per share remained flat at $0.22 compared to the same quarter last year, despite the challenging margin environment.

Strategic Initiatives

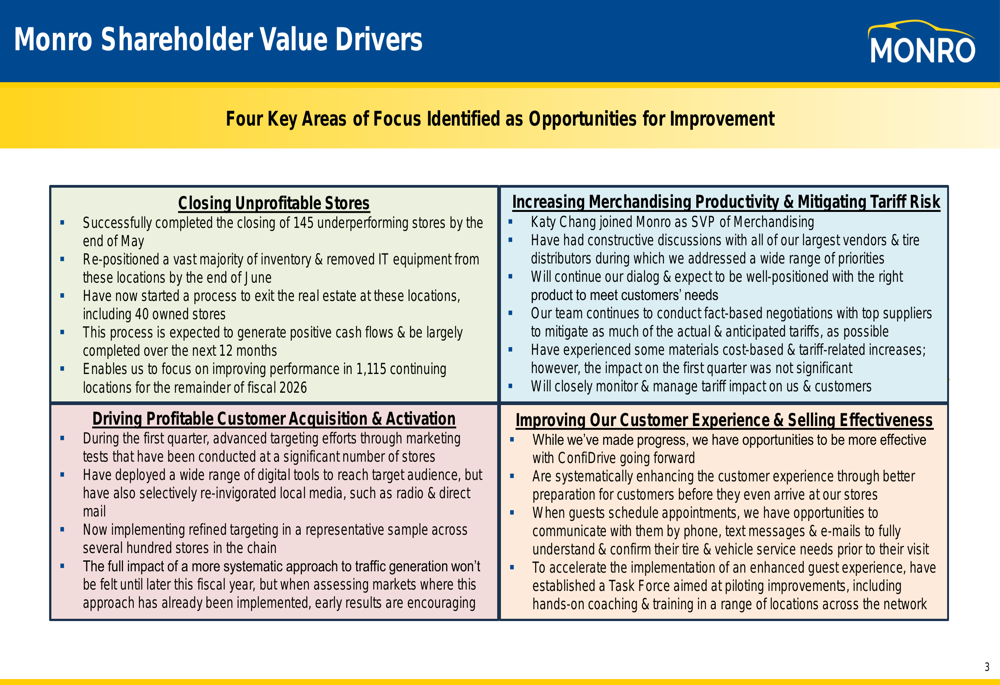

Monro outlined four key areas of focus designed to drive shareholder value, as illustrated in this strategic framework:

The company has made significant progress on its store optimization plan, successfully closing 145 unprofitable locations. This initiative is expected to reduce total sales by approximately $45 million in fiscal 2026 but should improve overall profitability.

To counter margin pressures and tariff risks, Monro has brought in new merchandising leadership with the appointment of Katy Chang as SVP of Merchandising. The company is engaged in constructive discussions with vendors and implementing fact-based negotiations to mitigate potential tariff impacts.

Customer acquisition efforts have advanced through targeted marketing tests and deployment of digital tools, with early results described as promising. Additionally, Monro has formed a dedicated Task Force to pilot improvements in customer experience and selling effectiveness.

Financial Position and Outlook

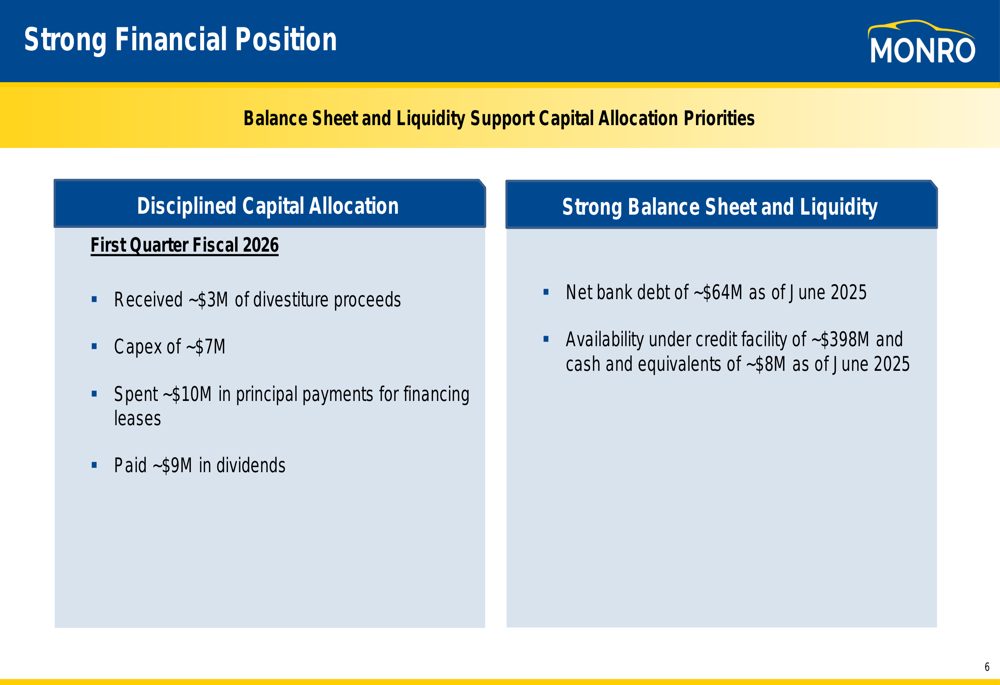

Monro maintained a disciplined approach to capital allocation during the quarter, as shown in the following financial position summary:

The company received approximately $3 million in divestiture proceeds while spending approximately $7 million on capital expenditures and $10 million in principal payments for financing leases. Monro also paid approximately $9 million in dividends, continuing its commitment to shareholder returns.

As of June 2025, Monro reported net bank debt of approximately $64 million, with availability under its credit facility of approximately $398 million and cash and equivalents of approximately $8 million, providing substantial liquidity for operations and strategic initiatives.

Forward-Looking Statements

Looking ahead to the remainder of fiscal 2026, Monro provided the following outlook:

The company expects to continue delivering year-over-year comparable store sales growth, with preliminary July comparable store sales already up 2%. However, management anticipates that gross margin will remain under pressure due to ongoing challenges.

Monro expects to partially offset some baseline cost inflation through operational improvements and projects capital expenditures of $25 million to $35 million for the fiscal year. The company believes it will continue to generate sufficient operating cash flow to fund its business needs and strategic initiatives.

To provide a clearer picture of its underlying performance, Monro shared detailed reconciliations of its adjusted financial metrics, which exclude one-time costs related to store closings, consulting for operational improvements, and back-office optimization:

These adjustments highlight the significant impact of the store closing initiative, which resulted in $14.8 million in costs during the quarter, as well as $4.7 million in consulting costs related to the operational improvement plan.

While Monro faces continued challenges from margin pressures and potential tariff impacts, the positive comparable sales growth and progress on strategic initiatives suggest the company is making headway in its efforts to improve long-term performance and shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.