U.S. stocks edge higher with consumer sentiment data, AI boom in focus

Introduction & Market Context

MRC Global Inc (NYSE:MRC) released its first quarter 2025 earnings presentation on May 7, 2025, revealing sequential revenue growth across all business segments despite missing analyst expectations. The company’s stock fell 8.07% following the announcement, closing at $11.47, as investors reacted to earnings per share of $0.14 against forecasts of $0.22, and revenue of $712 million versus expected $763.93 million.

The global distributor of pipe, valves, and fittings highlighted its financial strength and strategic initiatives, including a newly approved $125 million share repurchase program, while navigating challenges in meeting market expectations.

Quarterly Performance Highlights

MRC Global reported first quarter revenue of $712 million, representing a 7% sequential increase from the fourth quarter of 2024, though down year-over-year. The company achieved adjusted EBITDA of $36 million (5.1% of sales) and adjusted gross profit of $153 million (21.5% of sales).

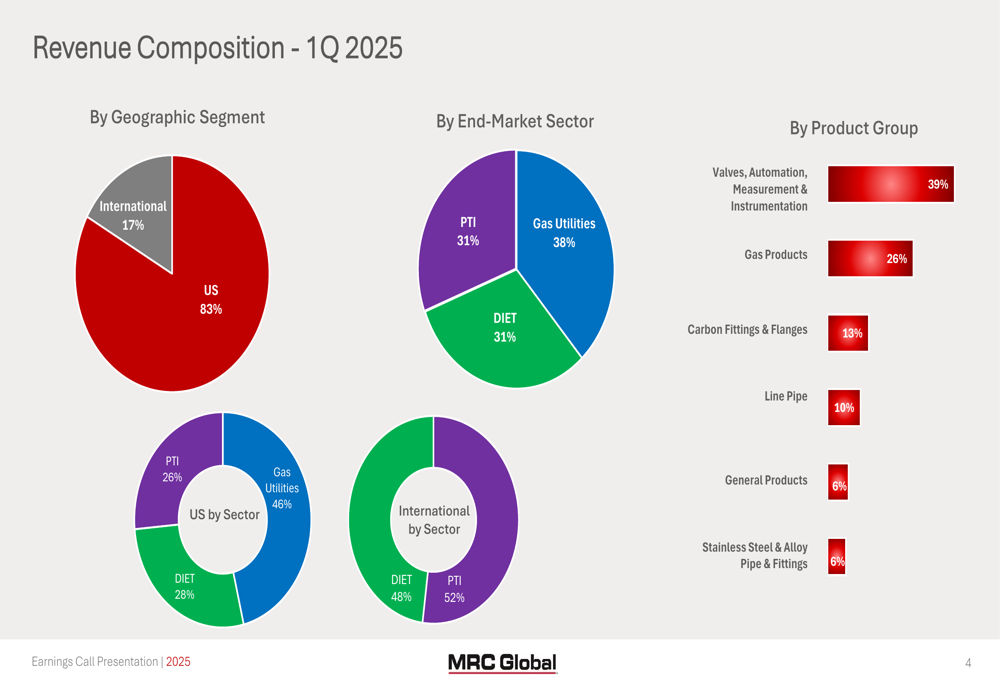

The company’s revenue composition shows the United States accounting for 83% of total revenue, with international operations contributing the remaining 17%. By sector, Gas Utilities represented 38% of revenue, while Process, Transmission & Infrastructure (PTI) and Downstream, Industrial & Energy Transition (DIET) each accounted for 31%.

As shown in the following revenue composition breakdown:

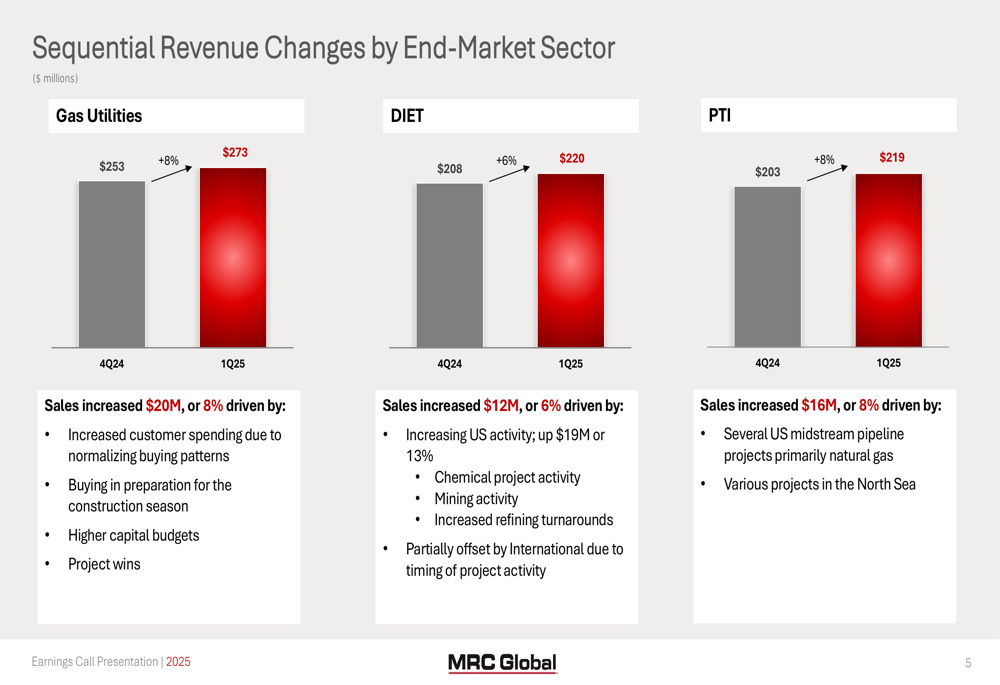

Sequential revenue growth was evident across all sectors, with Gas Utilities and PTI each increasing by 8% ($20 million and $16 million respectively), while DIET grew by 6% ($12 million). The Gas Utilities growth was driven by increased customer spending and higher capital budgets, while PTI benefited from several US midstream pipeline projects and North Sea activities.

The following chart illustrates these sequential revenue changes by sector:

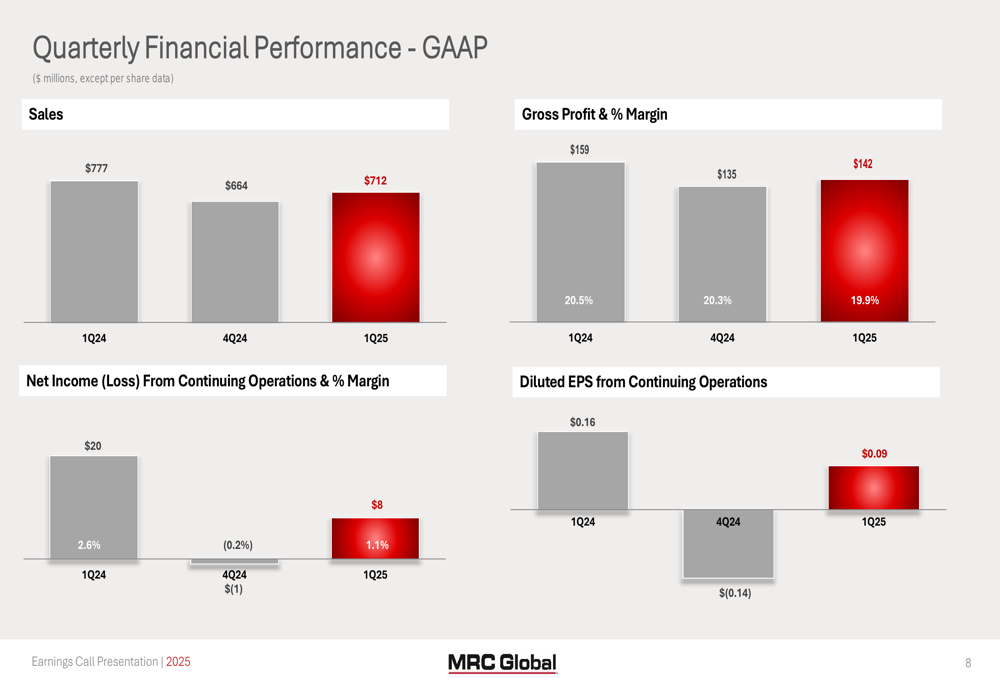

From a profitability perspective, MRC Global reported net income from continuing operations of $8 million (1.1% of sales), or $0.09 per diluted share. This represents a decline from the $20 million (2.6% of sales) reported in Q1 2024, but an improvement from the $1 million loss in Q4 2024.

The company’s quarterly financial performance is summarized in this chart:

Balance Sheet & Capital Allocation Strategy

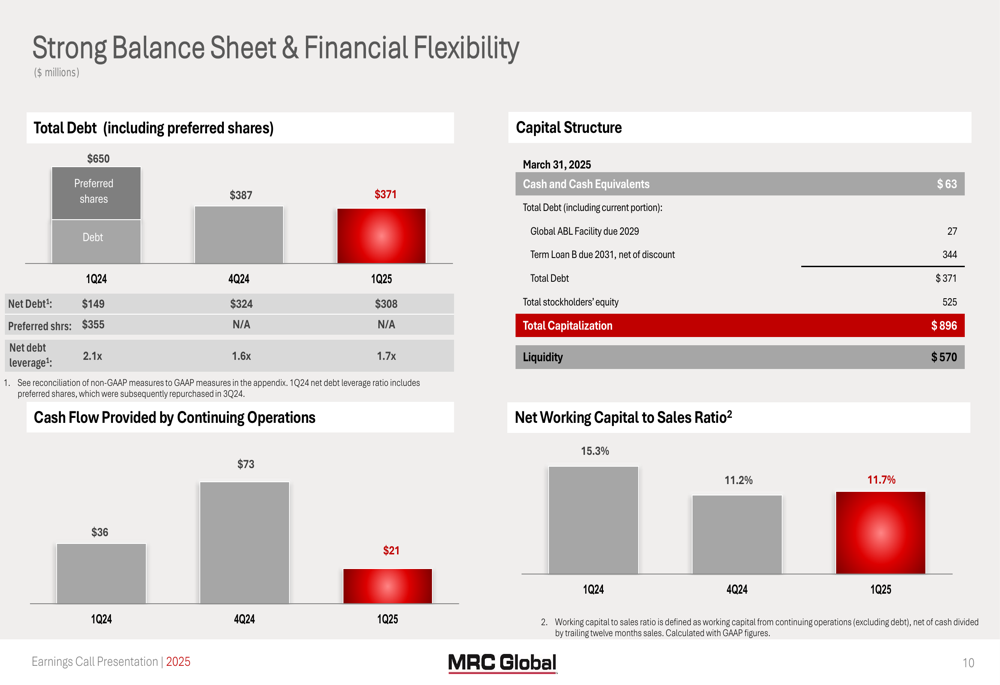

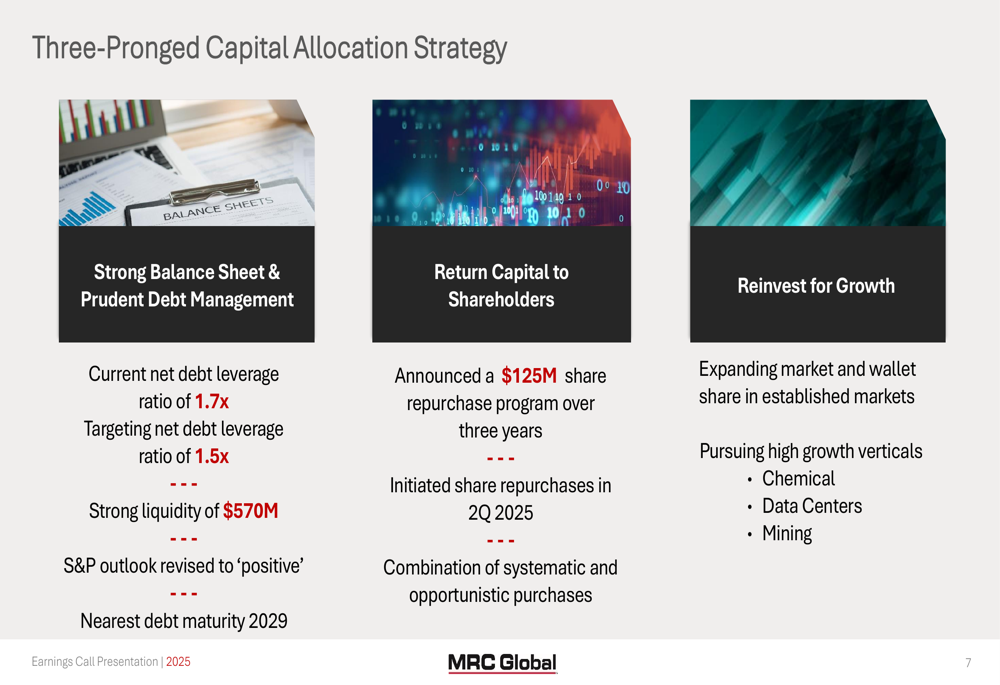

MRC Global emphasized its strong balance sheet, reporting $63 million in cash, total debt of $371 million, and liquidity of $570 million. The company’s net debt leverage ratio stands at 1.7x, slightly up from 1.6x in Q4 2024, but still within management’s target range.

The company’s financial position is illustrated in the following slide:

A key announcement was the approval of a $125 million share repurchase program to be executed over three years, beginning in Q2 2025. This forms part of MRC Global’s three-pronged capital allocation strategy, which also includes maintaining a strong balance sheet and reinvesting for growth.

The comprehensive capital allocation approach is outlined here:

Rob Faltiel, CEO of MRC Global, expressed optimism despite the earnings miss, stating, "We are off to an excellent start in 2025." He highlighted the recovery of the gas utility sector and the company’s strong cash flow generation, with $21 million generated from continuing operations in Q1 2025.

Strategic Initiatives & Growth Drivers

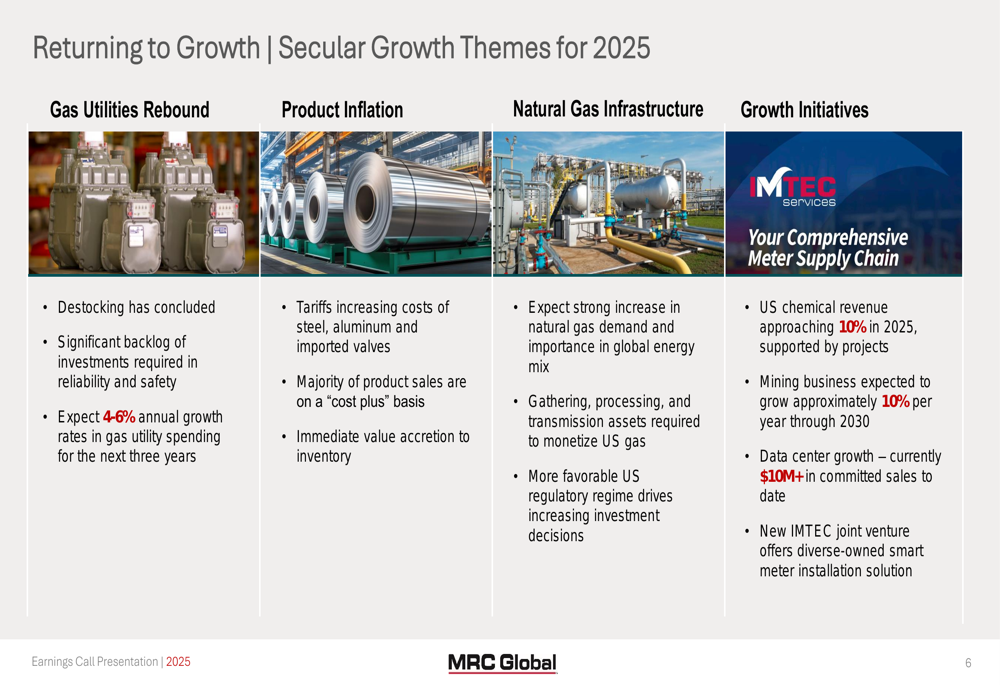

MRC Global outlined several secular growth themes for 2025, including a rebound in Gas Utilities following the conclusion of destocking, and increased demand for natural gas infrastructure. The company also highlighted growth initiatives in chemicals, mining, and data centers, with mining business expected to grow approximately 10% annually through 2030.

The company’s growth strategy is detailed in this slide:

Additionally, MRC Global announced the formation of a new joint venture, IMTEC Services, offering Automated Meter Reading (AMR) technology. The company also completed the divestiture of its Canada business in mid-March, generating $17 million in cash proceeds.

Forward-Looking Statements & Outlook

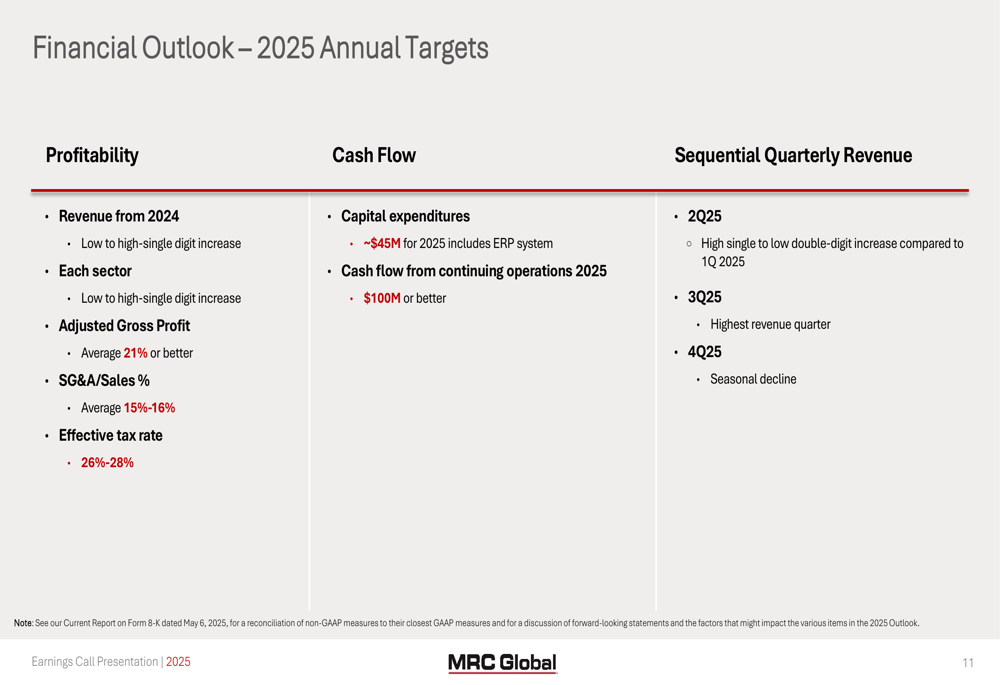

Despite missing analyst expectations for Q1, MRC Global maintained its full-year 2025 guidance, projecting low to high single-digit revenue growth across all sectors. The company expects adjusted gross profit to average 21% or better, with SG&A to sales ratio between 15-16%, and cash flow from continuing operations targeted at $100 million or better.

For quarterly progression, MRC Global anticipates a high single to low double-digit revenue increase in Q2 2025, with Q3 projected to be the highest revenue quarter, followed by a seasonal decline in Q4.

The company’s 2025 financial outlook is summarized here:

Conclusion

MRC Global’s Q1 2025 presentation paints a picture of sequential improvement and strategic positioning for future growth, despite falling short of market expectations. The company’s focus on capital allocation, including the new share repurchase program, alongside targeted growth in high-potential verticals like chemicals, mining, and data centers, demonstrates management’s confidence in the business fundamentals.

However, investors responded negatively to the earnings miss, highlighting the gap between company optimism and market expectations. With the stock trading near its 52-week low of $9.23, MRC Global faces the challenge of rebuilding investor confidence while executing on its growth strategy in an environment complicated by tariff uncertainties and fluctuating commodity prices.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.