WATCH LIVE: Investing.com reveals the top 10 stock picks for 2026

Introduction & Market Context

Mycronic AB (STO:MYCR) reported strong second-quarter 2025 results, with substantial sales growth despite facing headwinds in new orders. The Swedish electronics equipment manufacturer saw its stock close at SEK 200.8, down 0.93% following the announcement, as investors weighed impressive current performance against potential future challenges.

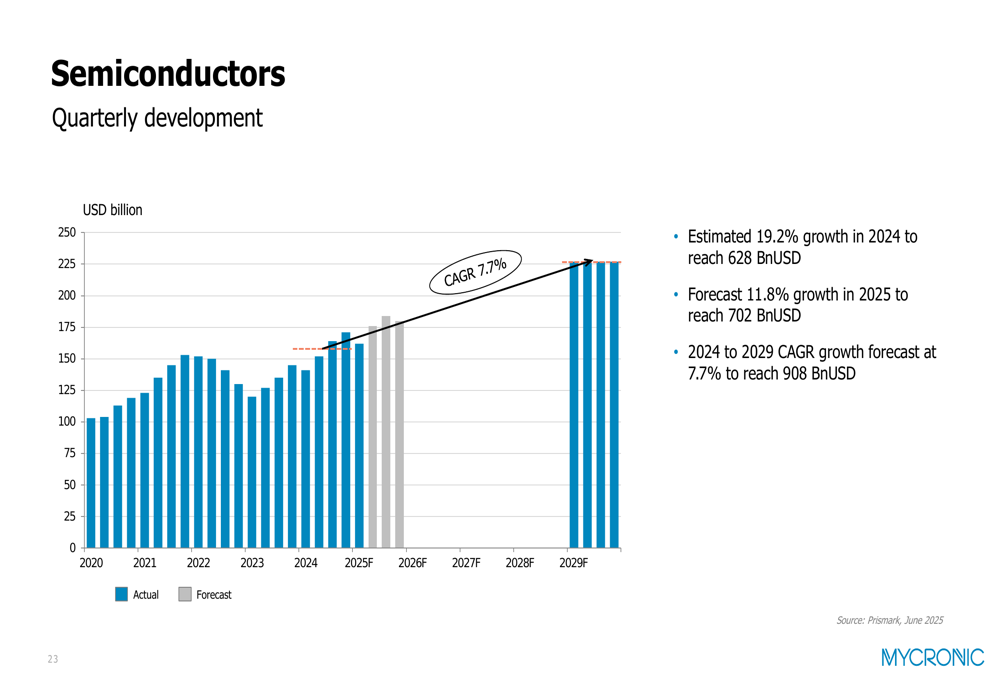

The company operates in a mixed global electronics market environment, with the semiconductor industry showing robust 19.2% growth in 2024 while SMT assembly equipment markets declined 7.7%. This context frames Mycronic's performance as the company navigates varying conditions across its diverse divisions.

Quarterly Performance Highlights

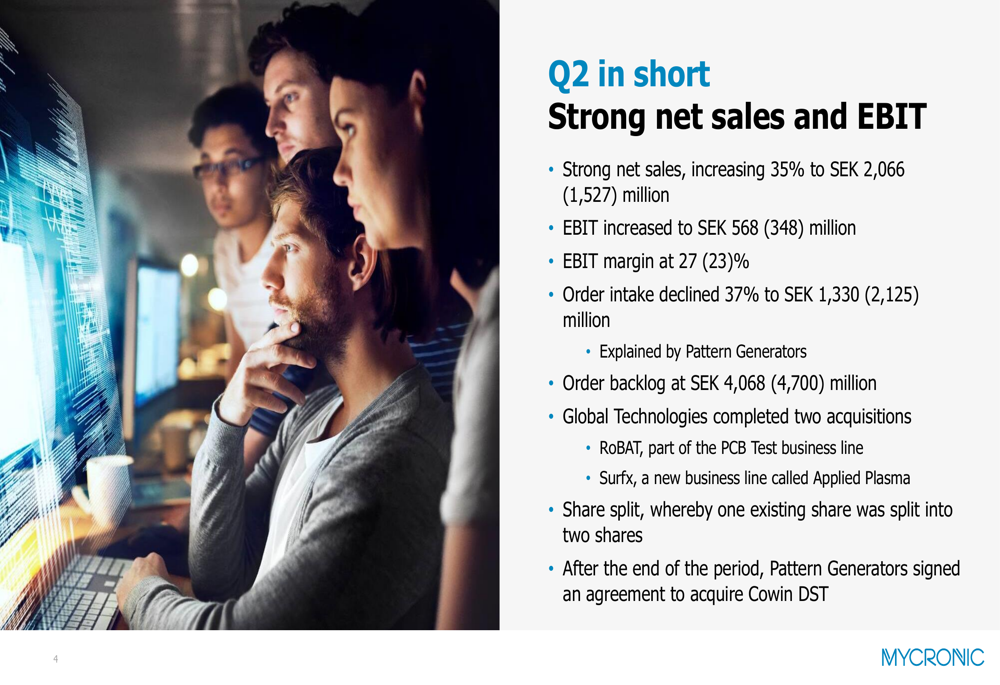

Mycronic delivered exceptional sales growth in Q2 2025, with net sales increasing 35% year-over-year to SEK 2,066 million. The company's EBIT jumped to SEK 568 million, representing a 27% margin compared to 23% in the same period last year. However, order intake declined 37% to SEK 1,330 million, primarily due to lower activity in the Pattern Generators division.

As shown in the following chart highlighting key Q2 metrics:

The company's order backlog stood at SEK 4,068 million, down from SEK 4,700 million in the comparable period. Aftermarket revenue remained strong at SEK 465 million, continuing to provide stable recurring income.

Detailed Financial Analysis

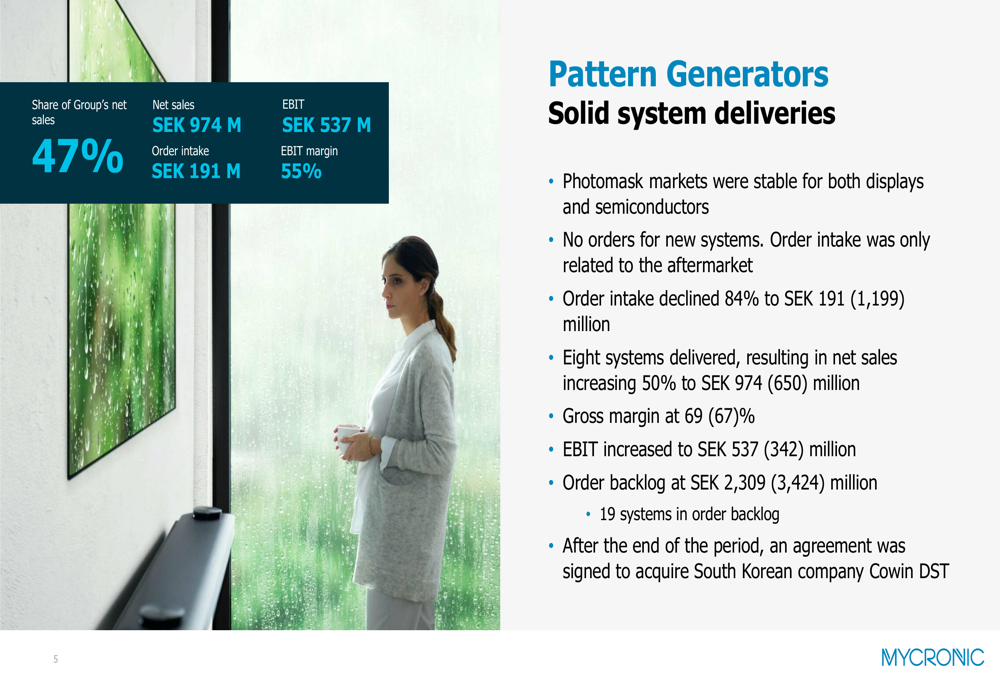

The Pattern Generators division was the standout performer, contributing 47% of group net sales with SEK 974 million and delivering an impressive 55% EBIT margin. The division benefited from the delivery of eight systems during the quarter, resulting in a 50% increase in net sales compared to Q2 2024.

The following breakdown shows the strong performance of the Pattern Generators division:

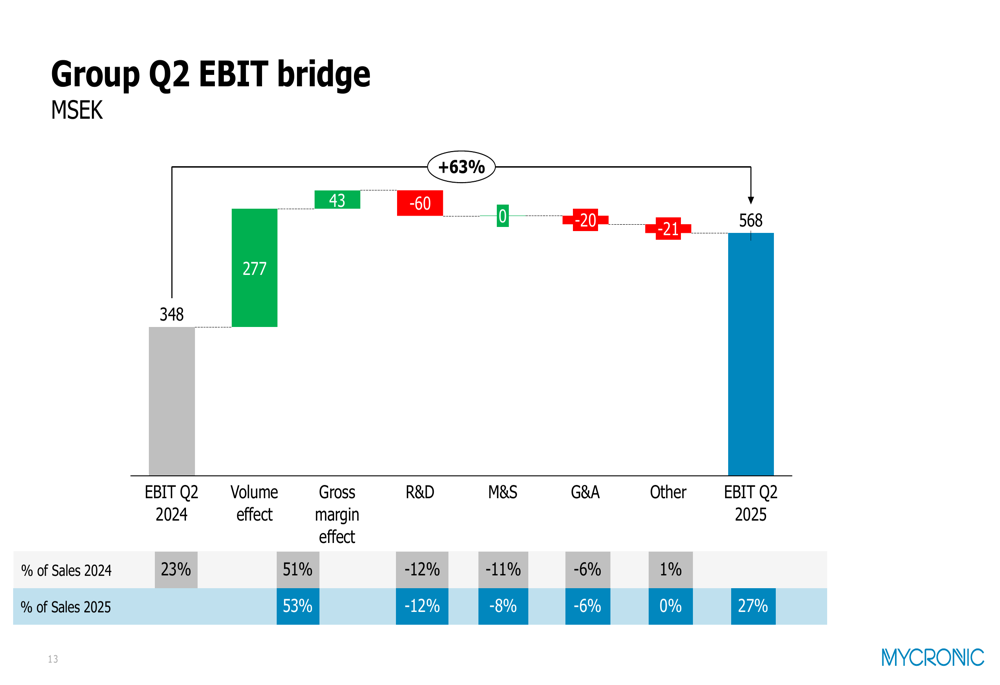

Mycronic's EBIT growth was primarily driven by volume effects and improved gross margins. As illustrated in this EBIT bridge, volume contributed SEK 277 million and gross margin improvements added SEK 43 million, partially offset by increased R&D and G&A expenses:

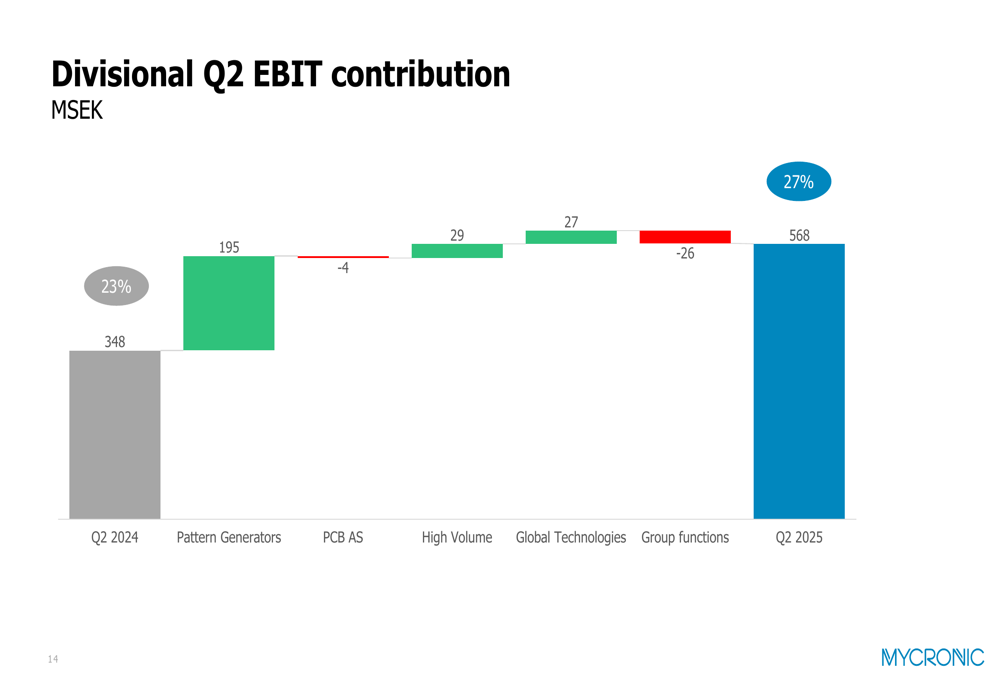

Looking at divisional contributions, Pattern Generators was the main driver of EBIT growth with a SEK 195 million positive impact:

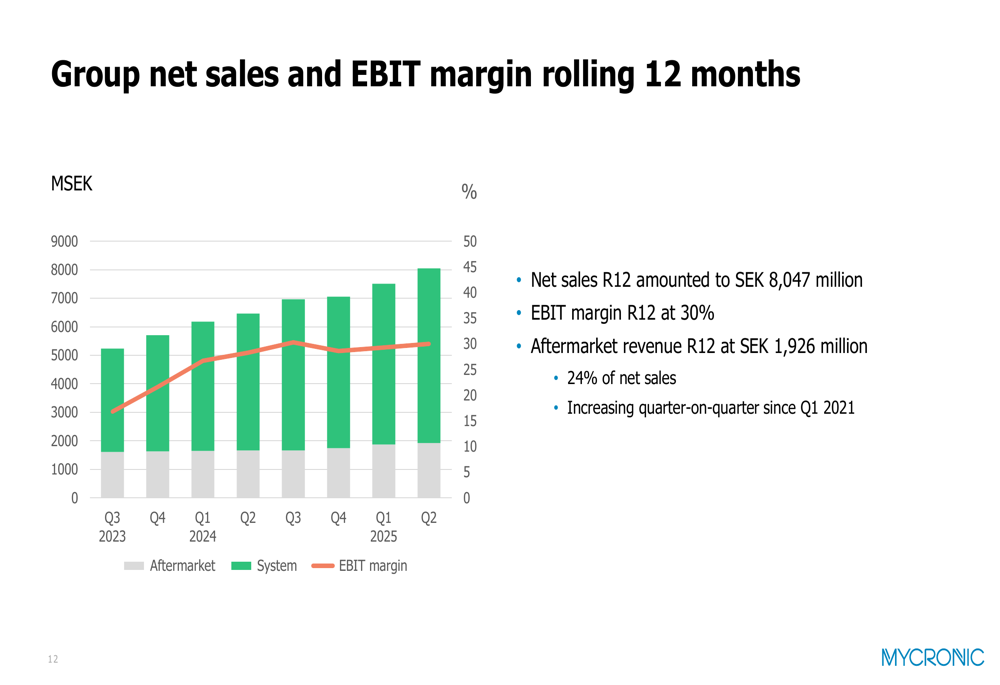

The company's rolling 12-month performance shows continued strength, with net sales reaching SEK 8,047 million and EBIT margin at 30%:

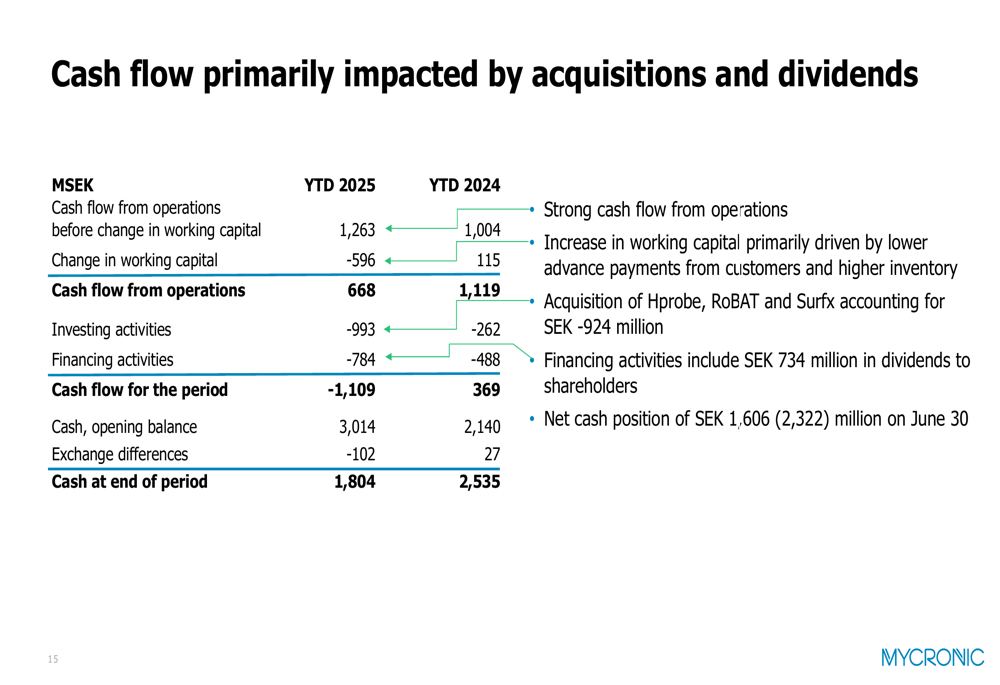

Cash flow from operations remained strong at SEK 668 million for the first half of 2025, though down from SEK 1,119 million in the comparable period. The decline was primarily due to changes in working capital and significant cash outflows for acquisitions totaling SEK 924 million:

Strategic Initiatives

Mycronic completed two strategic acquisitions during the quarter through its Global Technologies division: ROBAT, which has developed technology for fast signal quality tests on PCBs, and Surfx, which provides atmospheric plasma solutions. After the quarter ended, the Pattern Generators division signed an agreement to acquire South Korean company Cowin DST, further strengthening its market position.

The High Volume division performed well with net sales increasing 39% to SEK 443 million, benefiting from strong demand in the Chinese domestic market. Meanwhile, the PCB Assembly Solutions division faced challenges with weak European and US markets, resulting in a 7% decrease in net sales to SEK 328 million.

The Global Technologies division saw significant growth with order intake increasing 95% to SEK 402 million and net sales rising 59% to SEK 323 million, partly due to contributions from newly acquired companies.

Forward-Looking Statements

Based on strong second-quarter performance, completed acquisitions, and reduced uncertainty, Mycronic has revised its 2025 outlook upward with a net sales target of SEK 7.5 billion:

The company operates in markets with varying growth prospects. The semiconductor industry is forecast to grow 11.8% in 2025 to reach USD 702 billion, while the global electronics industry is expected to expand 7.4% to USD 2,743 billion:

Mycronic also highlighted its sustainability initiatives, noting that its existing SEK 1 billion credit facility with Handelsbanken was renewed through 2030 and linked to specific requirements related to the company's science-based climate targets and supply chain due diligence.

While the company faces some challenges with declining order intake and regional market weaknesses, particularly in Europe and the US for PCB assembly solutions, its diversified business model and strong position in growth segments like Pattern Generators provide a solid foundation for continued performance. The strategic acquisitions completed during the quarter further strengthen Mycronic's technological capabilities and market reach as it pursues its revised growth targets for 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.