Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

Norwegian hydrogen technology company Nel ASA (OSE:NEL) reported a significant revenue decline in its second quarter 2025 results presentation on July 16, 2025. The company is navigating a challenging market environment where final investment decisions (FIDs) on hydrogen projects continue to be delayed, despite a growing project pipeline.

Nel maintains that the quality of projects in its pipeline has improved due to stricter FID criteria, with several target projects in the 20-200 MW range expected to move forward in the coming quarters. The company highlighted improved clarity around US regulations, particularly the extension of the 45V hydrogen tax credit through January 1, 2028, as a potential catalyst for market growth.

Quarterly Performance Highlights

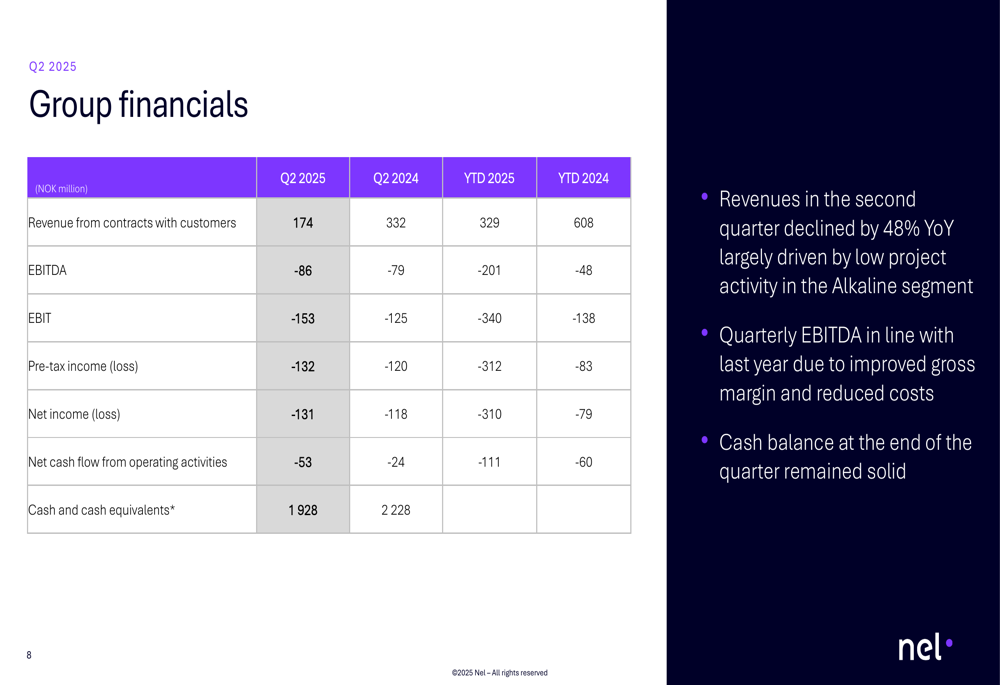

Nel reported revenue of NOK 174 million in Q2 2025, representing a 48% decrease compared to NOK 332 million in the same quarter last year. The company posted an EBITDA loss of NOK 86 million, slightly worse than the NOK 79 million loss in Q2 2024.

As shown in the following comprehensive financial table:

Order intake fell dramatically to NOK 71 million, down 74% year-over-year, while the order backlog decreased by 40% to NOK 1,249 million. The company’s cash position remained substantial at NOK 1,928 million, though down from NOK 2,228 million a year earlier.

The quarterly order intake and backlog trends are illustrated in this chart:

Detailed Financial Analysis

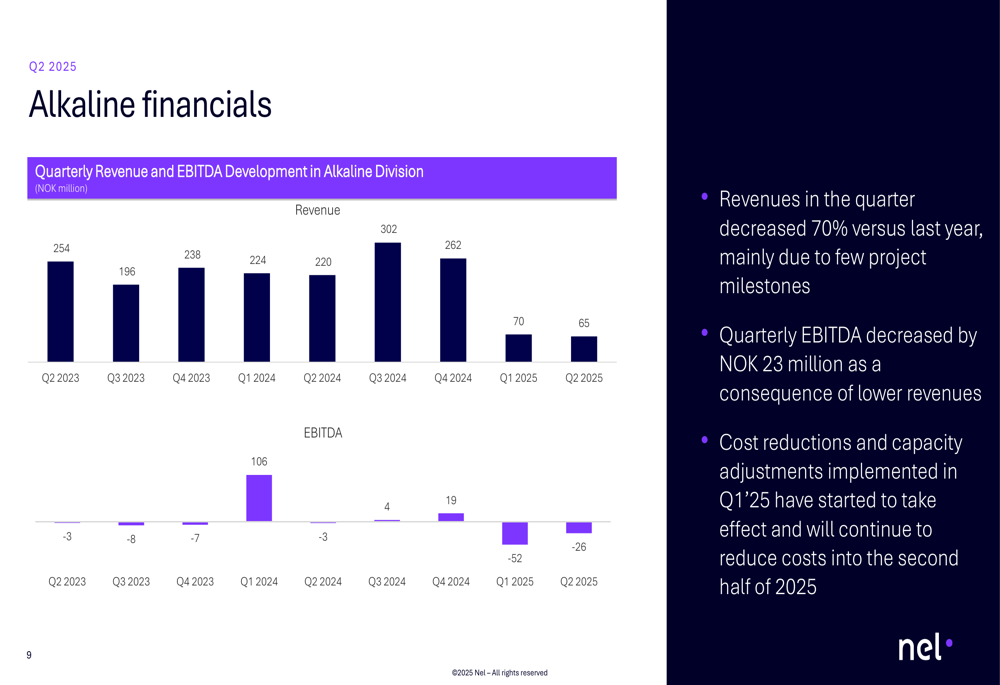

The revenue decline was particularly pronounced in Nel’s Alkaline division, which saw a 70% year-over-year decrease to NOK 70 million from NOK 262 million in Q2 2024. This significant drop was attributed to low project activity and few project milestones being reached during the quarter. The division’s EBITDA worsened to NOK -26 million from NOK -3 million a year earlier.

The Alkaline division’s performance is visualized in these charts:

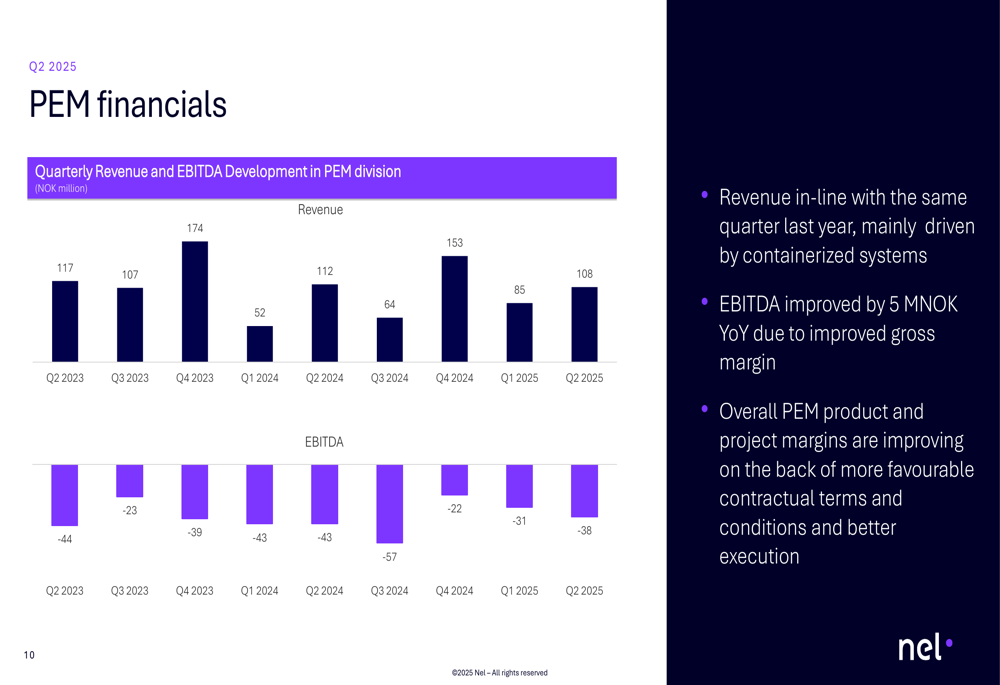

In contrast, Nel’s PEM division showed more stability, with revenue of NOK 108 million, only slightly below the NOK 112 million reported in Q2 2024. The PEM division’s EBITDA improved by NOK 5 million year-over-year to NOK -38 million, which the company attributed to improved gross margins. Nel noted that overall PEM product and project margins are improving.

The PEM division’s quarterly performance is shown here:

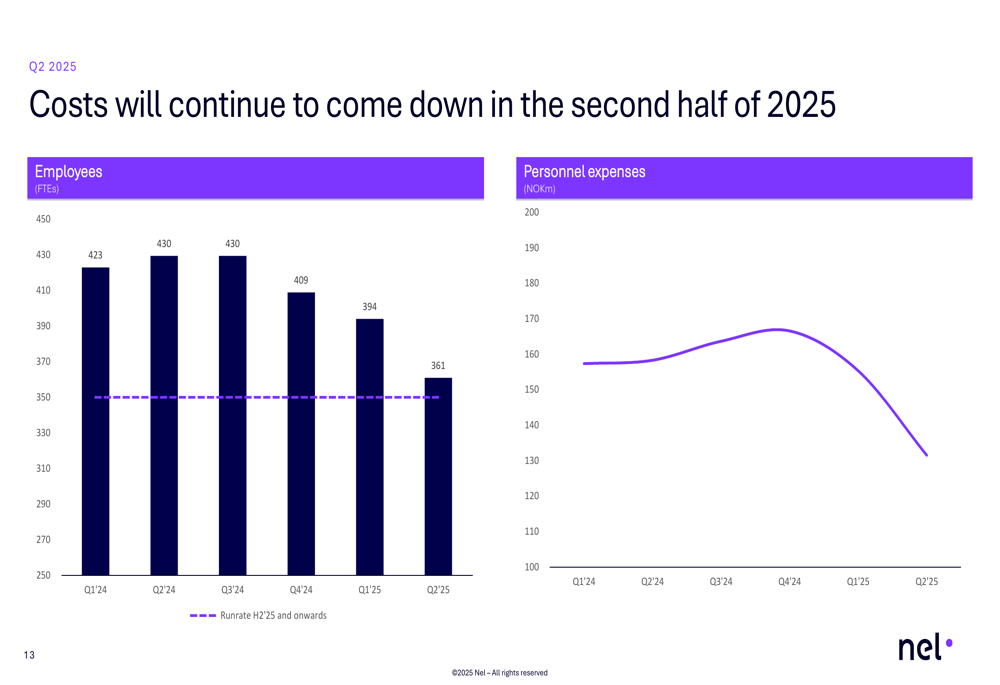

Nel has implemented significant cost reduction measures, reducing its workforce from 430 full-time equivalents in Q1 2024 to 361 in Q2 2025. This headcount reduction, along with other efficiency measures, is part of the company’s strategy to improve its financial position amid challenging market conditions.

The company’s cost reduction efforts are illustrated in this chart:

Strategic Initiatives & Technology Development

Despite financial challenges, Nel continues to invest heavily in next-generation technologies that it believes will dramatically improve its competitive position. The company is developing advanced alkaline and PEM electrolyzer technologies that promise significant reductions in both capital expenditure (CAPEX) and operating expenses (OPEX).

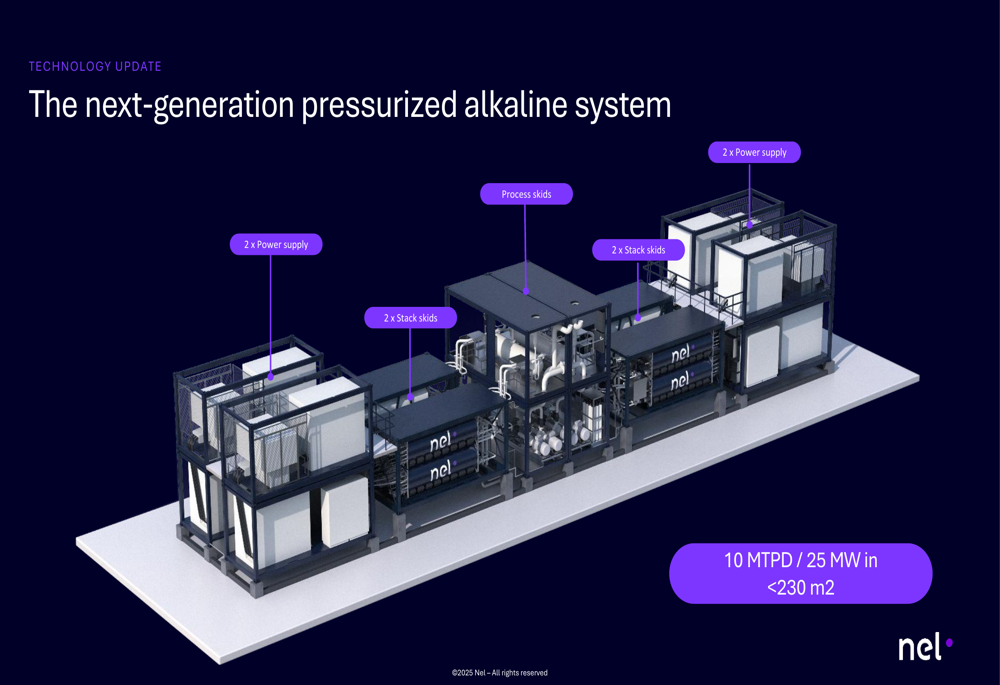

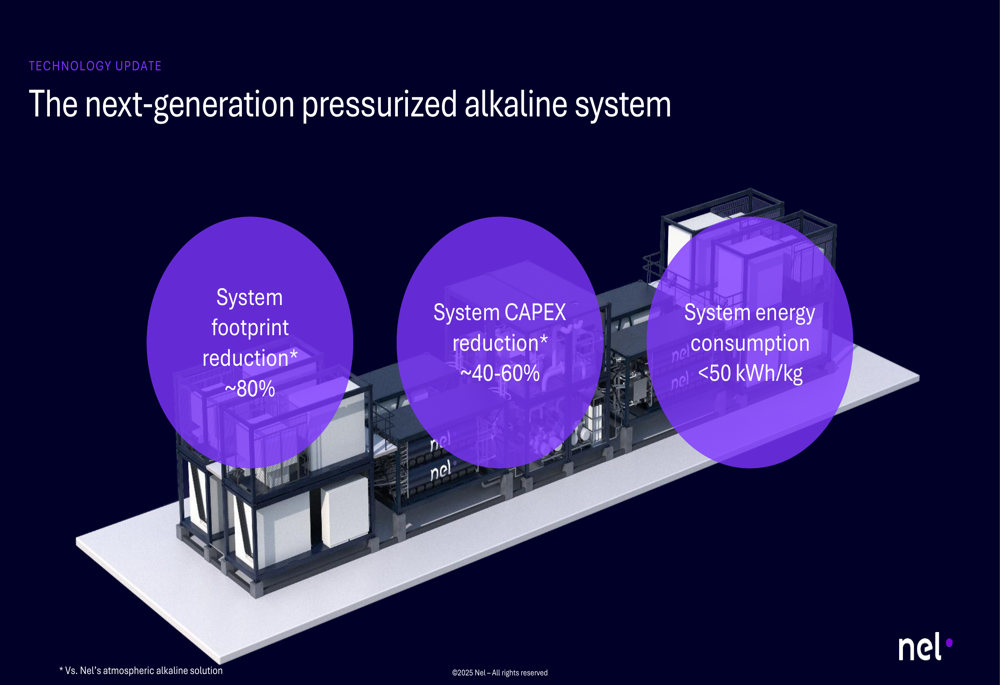

Nel’s next-generation pressurized alkaline system, currently in development, is expected to deliver approximately 80% reduction in system footprint and 40-60% reduction in system CAPEX compared to Nel’s current atmospheric alkaline solution. The system will also achieve energy consumption below 50 kWh/kg.

The company’s next-generation alkaline system is visualized here:

The benefits of this new system are substantial, as shown in this slide:

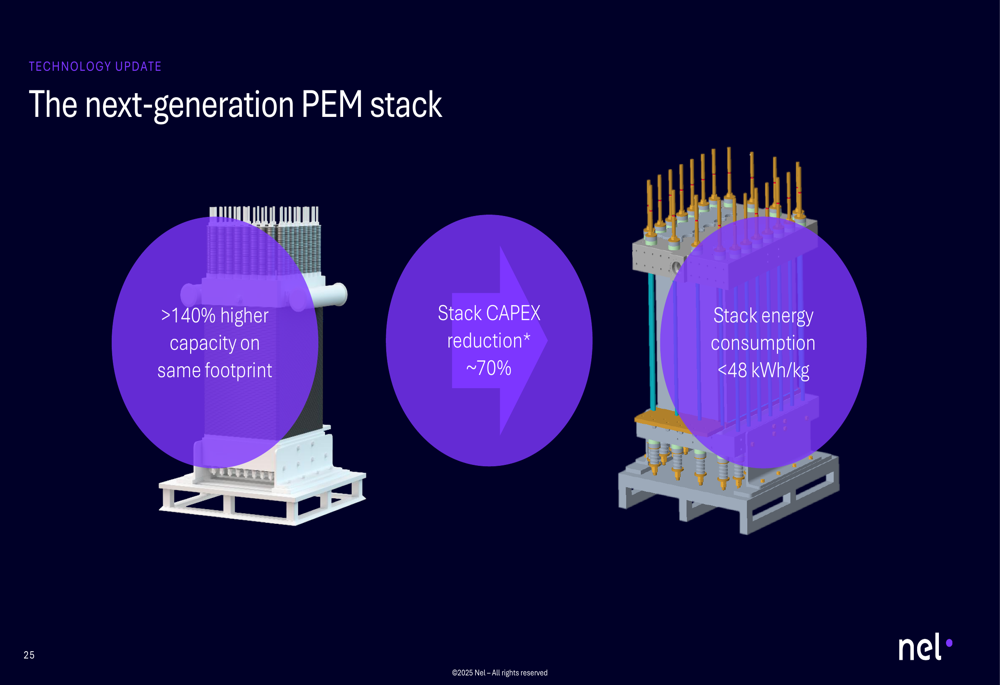

Similarly, Nel’s next-generation PEM stack is designed to deliver 140% higher capacity on the same footprint, approximately 70% reduction in stack CAPEX, and energy consumption below 48 kWh/kg.

The improvements in the next-generation PEM technology are illustrated here:

Nel also announced a partnership with SAMSUNG E&A, which has unveiled its CompassH2 hydrogen plant solution utilizing Nel’s alkaline technology. This 100MW concept is designed to deliver world-class system efficiency, scalability, and cost-competitiveness.

Forward-Looking Statements

Nel outlined a clear roadmap for its next-generation technologies. For the pressurized alkaline solution, the company plans to validate a 6.25 MW prototype in Q3 2025, take a final investment decision on gigawatt-scale production setup in the same quarter, validate a 25 MW customer pilot in 2026, launch the commercial product with first deliveries in 2026, and scale to hundreds of megawatts in 2027.

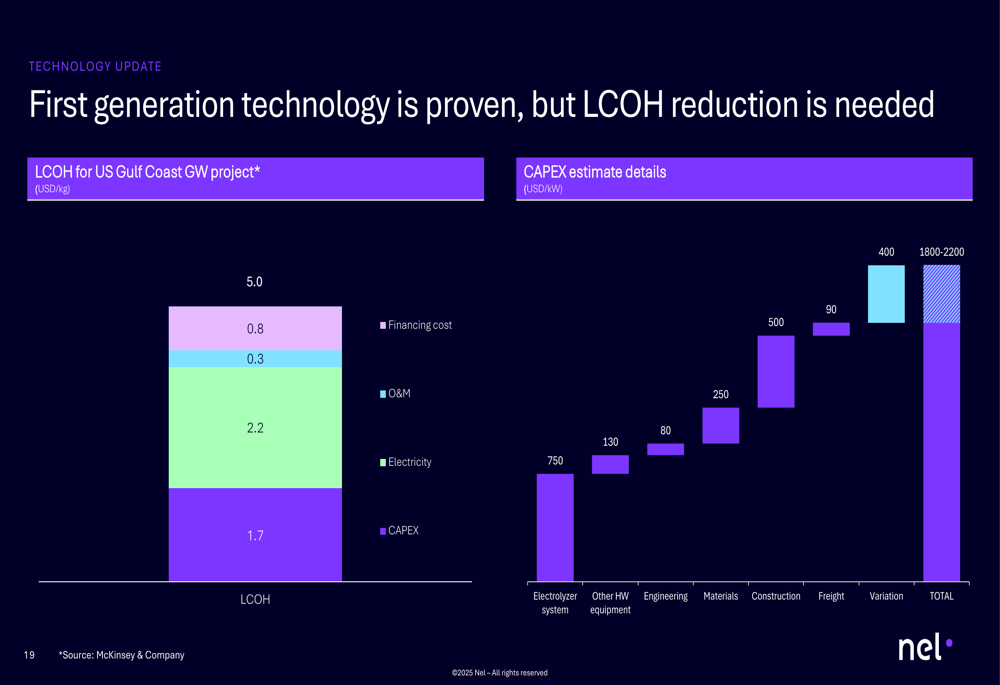

The company’s approach to lowering the levelized cost of hydrogen (LCOH) focuses on both OPEX improvements (through better energy efficiency, wider operating range, and quicker ramp-up/down capabilities) and CAPEX reductions (via cheaper modules, outdoor operation, standardization, and smaller footprint with modularization).

Nel’s breakdown of LCOH components for a US Gulf Coast gigawatt-scale project shows that electricity costs (USD 2.2/kg) remain the largest contributor to hydrogen production costs, followed by CAPEX (USD 1.7/kg), financing costs (USD 0.8/kg), and operations and maintenance (USD 0.3/kg).

This cost breakdown is visualized in the following chart:

While Nel’s Q2 2025 results reflect continued challenges in the hydrogen market, the company is positioning itself for future growth through technological innovation and strategic partnerships. The success of these initiatives will largely depend on market adoption of hydrogen solutions and Nel’s ability to deliver on its ambitious technology roadmap while managing its cash burn in the interim.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.