Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Introduction & Market Context

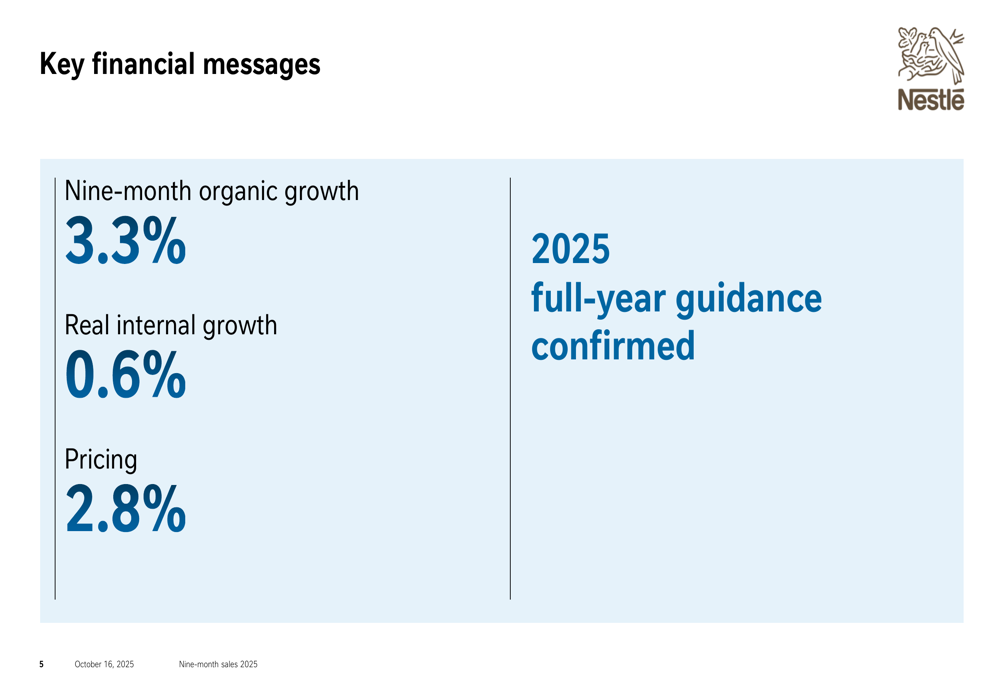

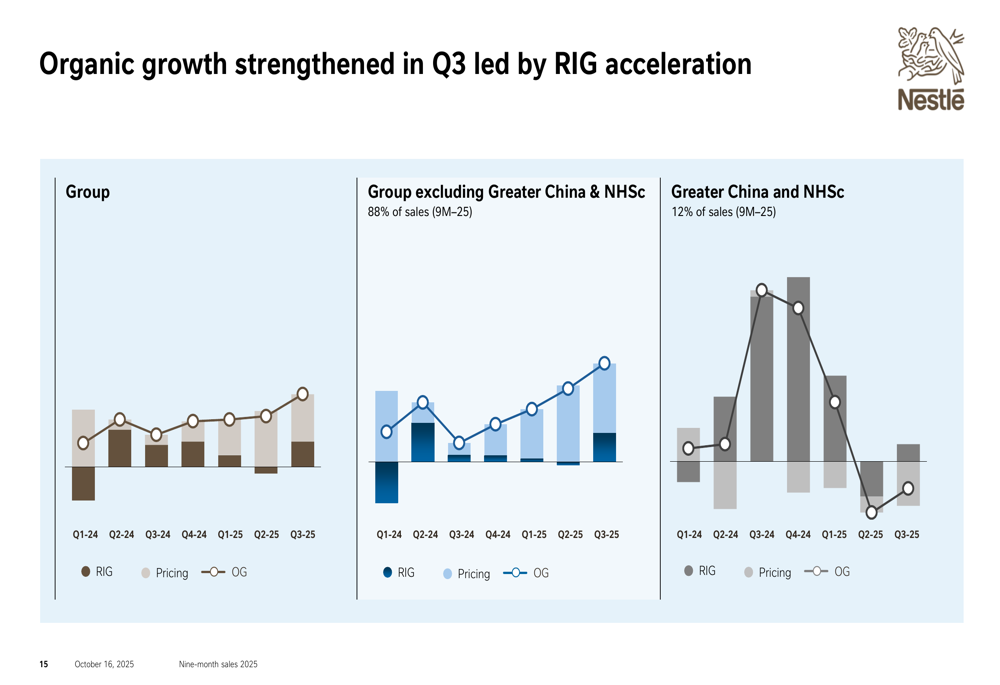

Nestlé SA (SWX:NESN) presented its nine-month sales results for 2025 on October 16, showing accelerating organic growth momentum despite challenging macroeconomic conditions. The Swiss food and beverage giant reported organic growth of 3.3% for the first nine months of 2025, with a notable acceleration to 4.3% in the third quarter, suggesting that strategic initiatives are beginning to yield results.

The company’s shares have been trading around CHF 90, as investors assess Nestlé’s ability to navigate inflation, supply chain pressures, and changing consumer preferences while implementing significant cost-cutting measures.

Quarterly Performance Highlights

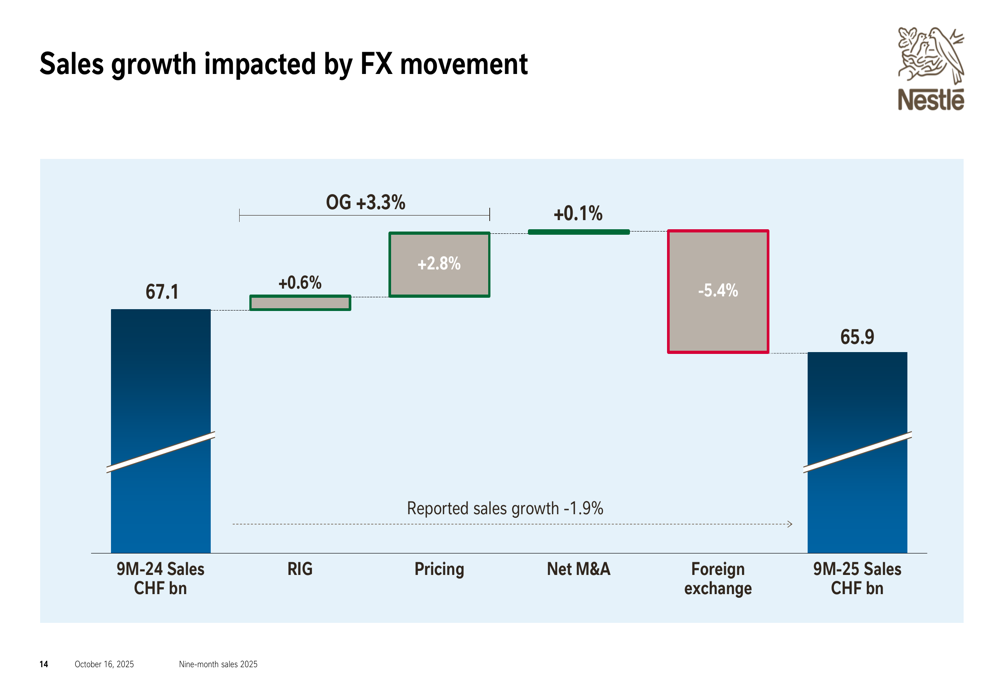

Nestlé reported nine-month sales of CHF 65.9 billion, representing a 1.9% decrease in reported terms compared to the previous year, primarily due to significant foreign exchange headwinds of -5.4%. However, the underlying organic growth of 3.3% was driven by pricing contributions of 2.8% and real internal growth (RIG) of 0.6%.

As shown in the following key financial metrics slide, the company has maintained its full-year guidance:

The most encouraging sign came from the third quarter, where organic growth accelerated to 4.3%, suggesting momentum is building as the year progresses. This improvement was reflected in the quarterly trend analysis:

The waterfall chart below illustrates how various factors affected Nestlé’s sales performance, with foreign exchange having the most significant negative impact:

Strategic Initiatives

Nestlé outlined four strategic pillars driving its transformation: RIG-led growth through bolder investment and innovation, ensuring a winning portfolio, fostering a performance culture, and accelerating business transformation with cost savings.

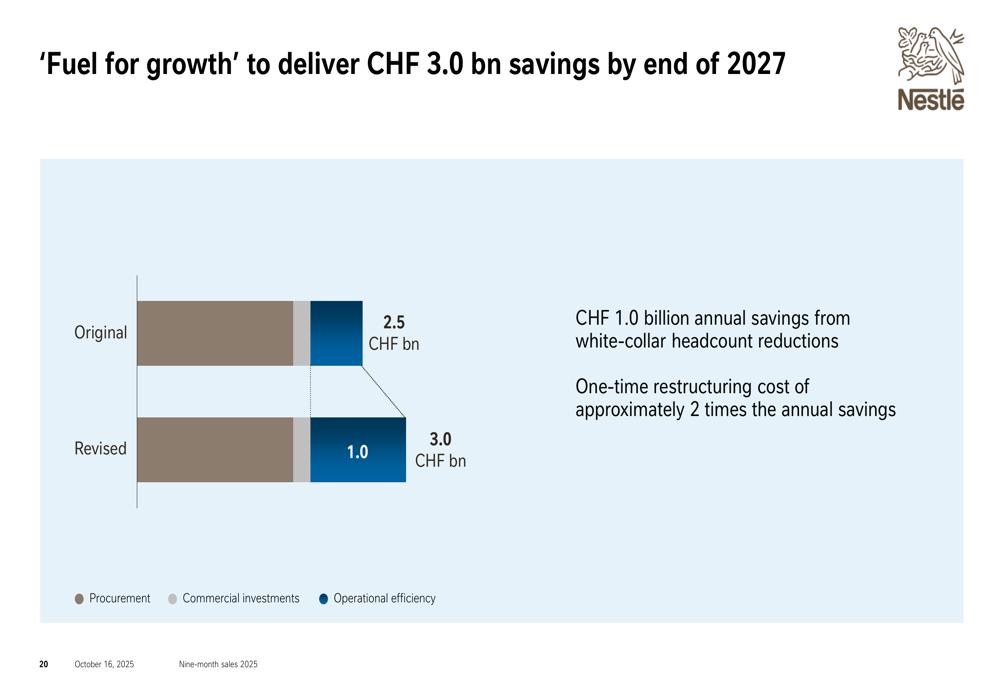

In a significant development, the company announced an expansion of its "Fuel for Growth" cost-saving program, increasing the target from CHF 2.5 billion to CHF 3.0 billion in annual savings by the end of 2027. This expanded initiative includes a planned reduction of approximately 16,000 employees over two years.

The following slide details the expanded cost-saving program:

CEO Philipp Navratil emphasized the urgency of delivering improved shareholder value, stating, "We need to move faster and act with urgency to deliver improved shareholder value." This sentiment reflects the company’s commitment to accelerating its transformation efforts.

Regional and Category Performance

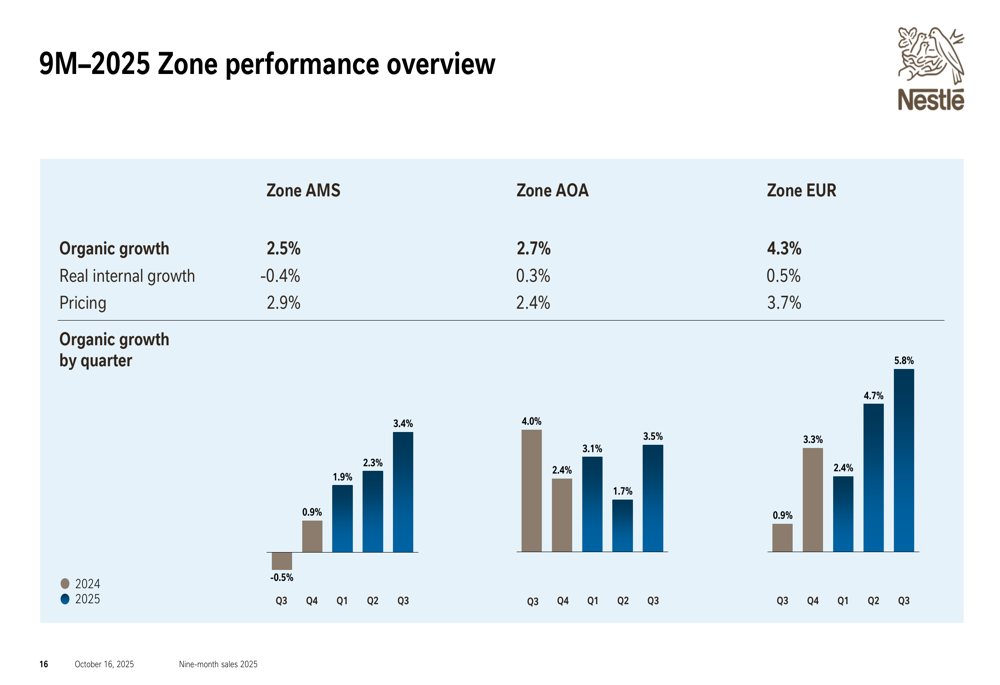

Nestlé’s performance varied significantly across regions and product categories. The European zone showed strong results, driven by coffee, confectionery, and pet care products. Meanwhile, challenges persisted in Greater China and the infant nutrition sector, which continues to face headwinds from declining birth rates.

The following slide provides an overview of performance by zone:

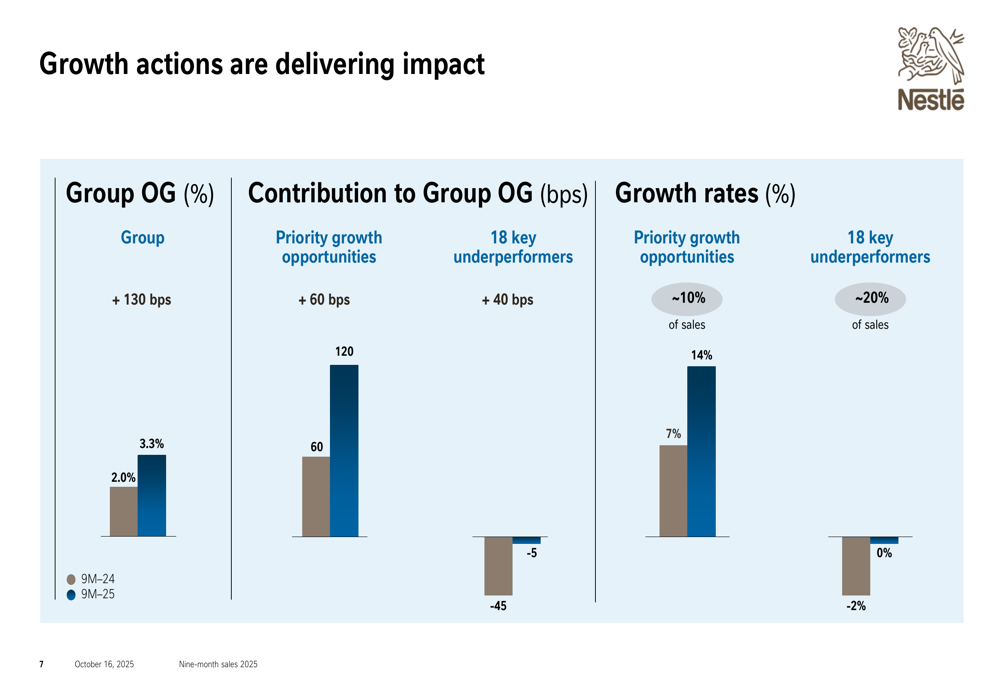

In terms of product categories, PetCare remained a strong performer, while Nestlé Health Science faced more challenging conditions. The company’s strategic focus on high-growth categories appears to be yielding results, as shown in the growth actions impact slide:

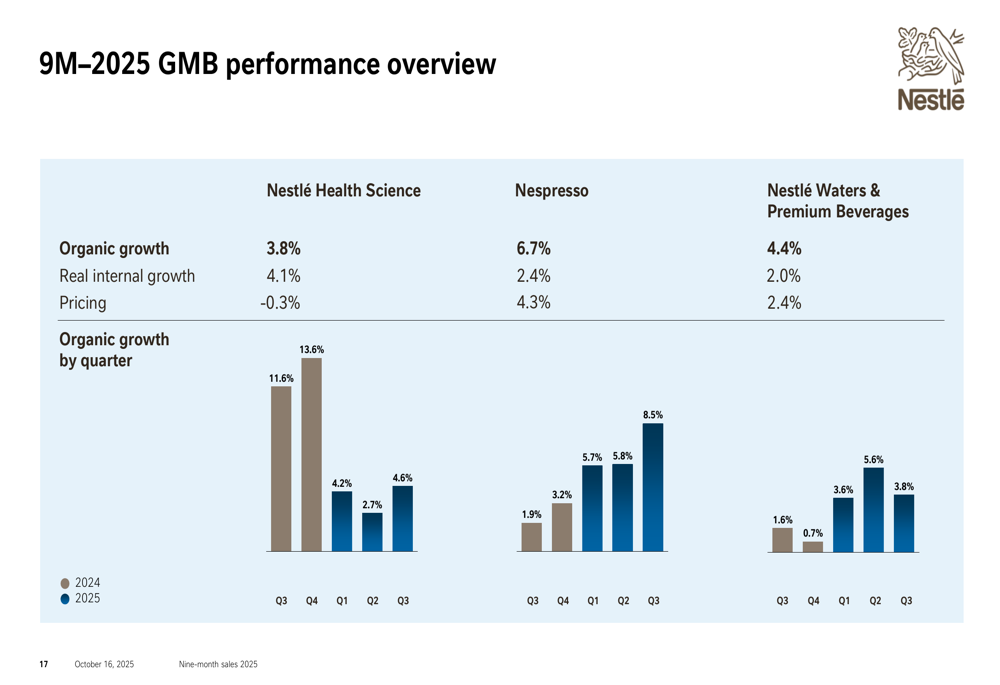

The business segment performance across Global Business Units further illustrates these trends:

Forward-Looking Statements

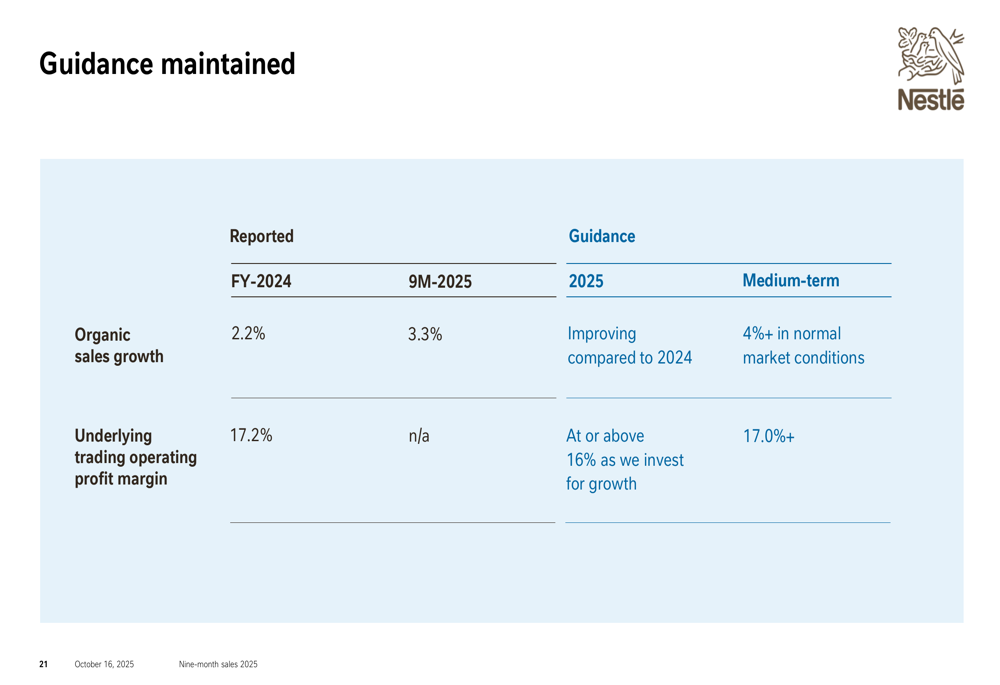

Nestlé maintained its full-year 2025 guidance, projecting organic sales growth improvement compared to 2024’s 2.2%, with an underlying trading operating profit margin at or above 16%. For the medium term, the company aims to achieve organic growth exceeding 4% in normal market conditions, with margins returning to above 17%.

The guidance slide below outlines these targets:

CFO Anna Manz highlighted the company’s focus on growth, saying, "We will drive RIG through investing boldly." This suggests that while cost-cutting measures are being implemented, Nestlé is not sacrificing growth investments.

The company faces several challenges going forward, including supply chain adjustments due to workforce reductions, continued difficulties in Greater China, headwinds in infant nutrition, and potential market saturation in certain categories. Currency fluctuations also remain a significant factor, having reduced reported sales by 5.4% in the first nine months of 2025.

Nevertheless, Nestlé’s accelerating organic growth in Q3 2025, combined with its expanded cost-saving initiatives, positions the company to potentially improve shareholder returns if execution remains strong. Investors will be closely watching whether the company can maintain this growth momentum while successfully implementing its significant transformation plan.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.