Keysight partners with NVIDIA on quantum-AI computing architecture

Introduction & Market Context

Netel Holding AB (STO:NETEL) presented its third-quarter 2025 results on October 24, revealing significant profitability challenges and a comprehensive recovery strategy. The infrastructure service provider, operating in the telecom, power, and infrastructure sectors, saw its stock decline 7.87% to SEK 4.15 following the presentation, approaching its 52-week low of SEK 3.89.

Despite operating in markets driven by megatrends like electrification and digitalization, Netel faced substantial headwinds during the quarter, primarily due to project write-downs and lower volumes. The company’s order backlog remains strong at SEK 3.84 billion, suggesting potential for future recovery if execution improves.

Quarterly Performance Highlights

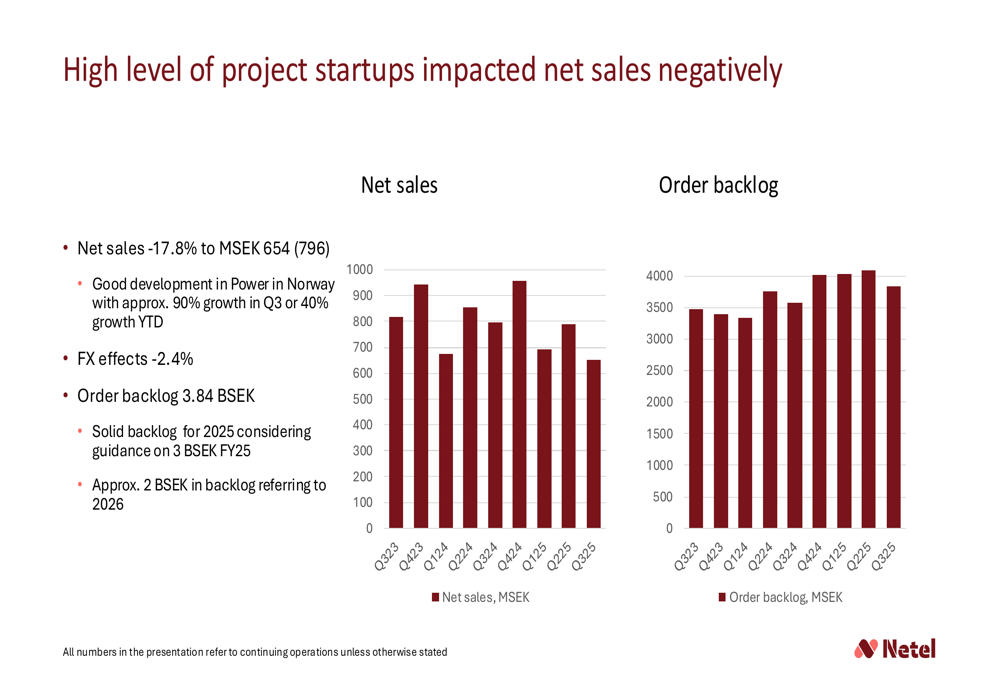

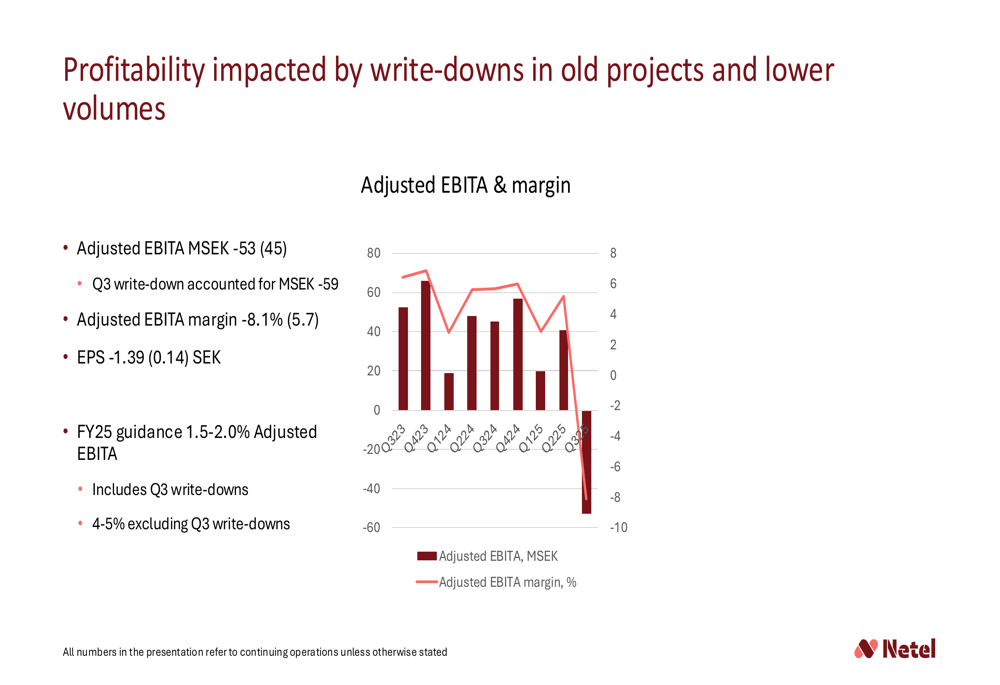

Netel reported a steep decline in Q3 2025 performance, with net sales decreasing 17.8% year-over-year to SEK 654 million. The most concerning figure was adjusted EBITA, which plummeted to negative SEK 53 million compared to positive SEK 45 million in Q3 2024, resulting in an adjusted EBITA margin of -8.1%.

As shown in the following chart of quarterly net sales and order backlog:

The company’s net sales have been on a downward trend for several quarters, though the order backlog has remained relatively stable around SEK 3.8 billion. This disconnect between current performance and future potential highlights Netel’s execution challenges.

Profitability was severely impacted by write-downs totaling SEK 59 million, primarily from overvalued projects in three companies acquired between 2021-2022. The adjusted EBITA trend illustrates the severity of the situation:

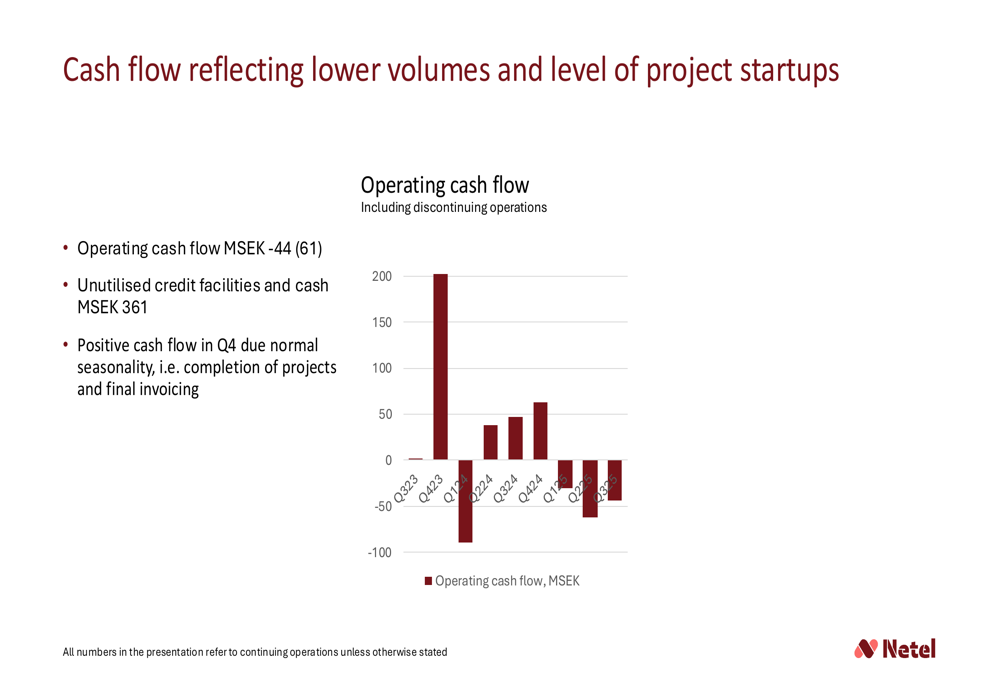

The negative profitability resulted in earnings per share of -SEK 1.39, compared to SEK 0.14 in the same period last year. Operating cash flow was also negative at -SEK 44 million, continuing a concerning trend:

Detailed Financial Analysis

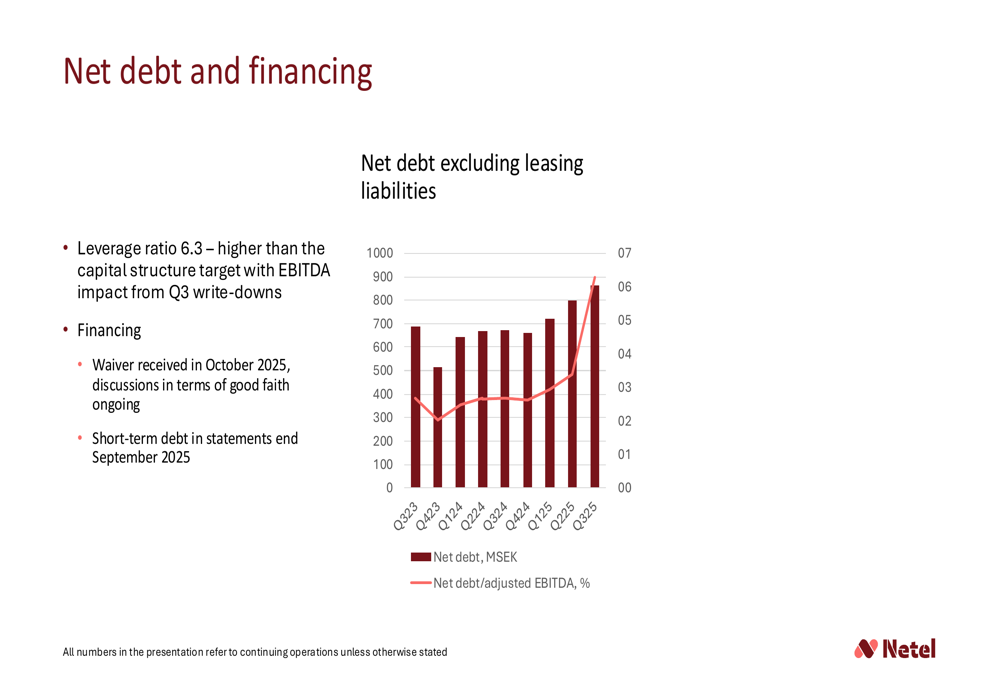

Netel’s financial position has deteriorated, with net debt increasing to SEK 830 million and the leverage ratio reaching 6.3, well above the company’s capital structure target. This prompted the company to seek a waiver from lenders in October 2025, with discussions ongoing regarding longer-term financing solutions.

The debt situation is illustrated in the following chart:

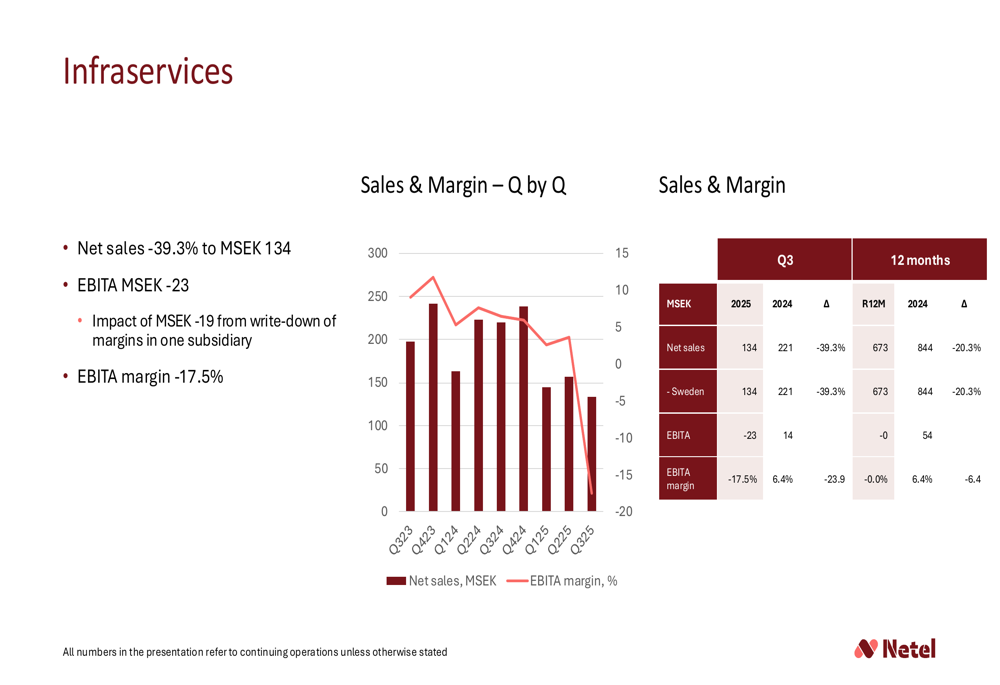

All three business segments reported negative EBITA in Q3. The Infraservices segment saw sales decrease by 39.3% to SEK 134 million, with EBITA falling to -SEK 23 million, impacted by a SEK 19 million write-down in one subsidiary:

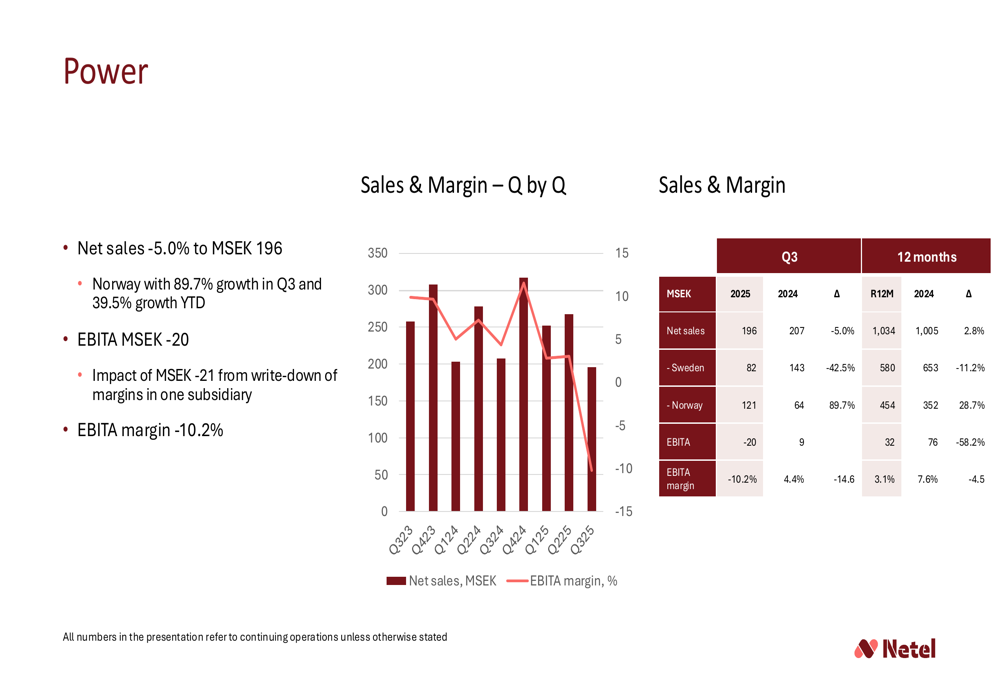

The Power segment experienced a 5.0% sales decline to SEK 196 million, though Norway showed impressive 89.7% growth in Q3. EBITA was -SEK 20 million, affected by a SEK 21 million write-down:

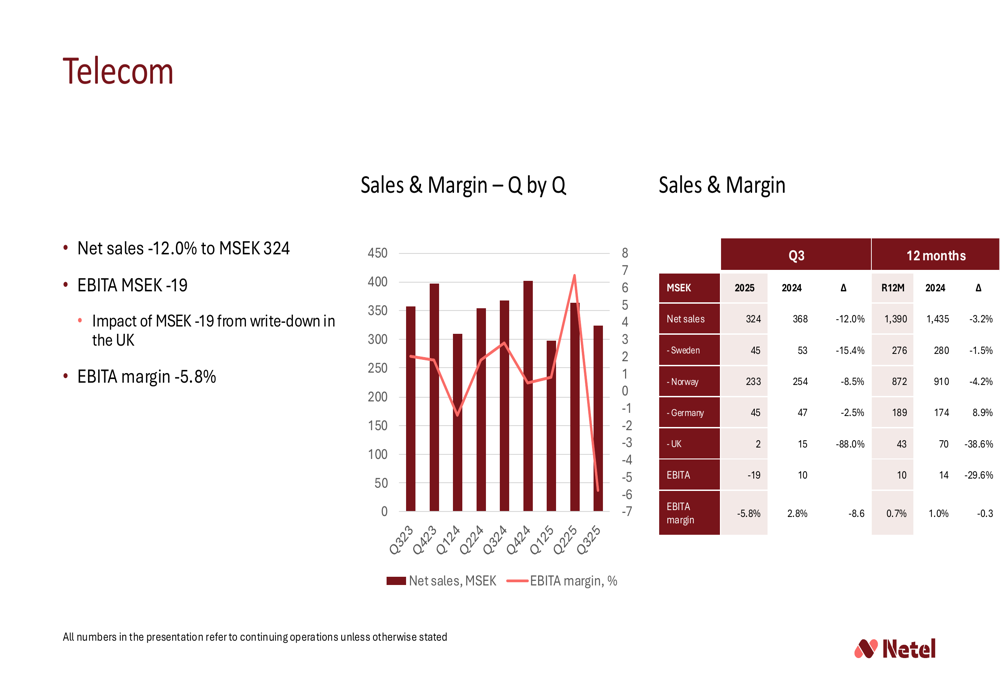

Telecom, Netel’s largest segment, reported a 12.0% sales decrease to SEK 324 million and EBITA of -SEK 19 million, including a SEK 19 million write-down related to UK operations:

Strategic Initiatives & Restructuring

In response to these challenges, Netel outlined a comprehensive action plan focused on restoring profitability. Key initiatives include:

1. Divestment of the underperforming UK operation

2. Restructuring of companies with profitability problems

3. Consolidation of subsidiaries into larger units

4. Reduction of management levels

5. Improvement of internal processes and follow-up

6. Implementation of a cost-saving program targeting SEK 40-50 million

The cost-saving program is structured in two phases: SEK 25 million with full effect by 2026 and an additional SEK 15-25 million with full effect by 2027. Specific measures include new management in the Infraservices division, streamlining the Power division by merging subsidiaries, and implementing efficiency improvements in the Norwegian telecom operations.

CEO Jeanette Reuterskiöld emphasized the company’s commitment to making "tough but necessary decisions" to improve profitability and strengthen Netel’s financial position.

Forward-Looking Statements

Despite current challenges, Netel provided guidance for full-year 2025, projecting net sales of SEK 3 billion with an adjusted EBITA margin of 1.5-2%. For the remaining operations (90% of sales), the company expects an adjusted EBITA margin of 4-5%, suggesting that the problematic areas represent about 10% of the business.

Looking ahead to 2026, Netel anticipates growth and margin improvement, supported by the cost-saving measures and an order backlog for 2026 of approximately SEK 2 billion. The company also expects strong cash flow in Q4 2025, following normal seasonality patterns of project completions and final invoicing.

However, these projections appear optimistic given the current negative trends across most financial metrics and the significant challenges in restoring profitability. The market’s skepticism is reflected in the stock’s performance, which has declined 77% over the past year according to analyst data.

As Netel works to implement its turnaround strategy, investors will be closely watching whether the company can deliver on its cost-saving targets and improve project execution to convert its substantial order backlog into profitable revenue.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.