Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Newmark Group Inc (NASDAQ:NMRK) presented its second quarter 2025 financial results on July 30, showcasing robust growth across all business segments and an improved outlook for the full year. The commercial real estate services provider reported significant year-over-year improvements in revenue, earnings, and EBITDA, continuing the positive momentum seen in the first quarter.

In premarket trading following the presentation, Newmark shares rose 2.29% to $14.77, building on the previous day’s 6.57% gain, as investors responded positively to the strong quarterly performance and upward revision of full-year guidance.

Quarterly Performance Highlights

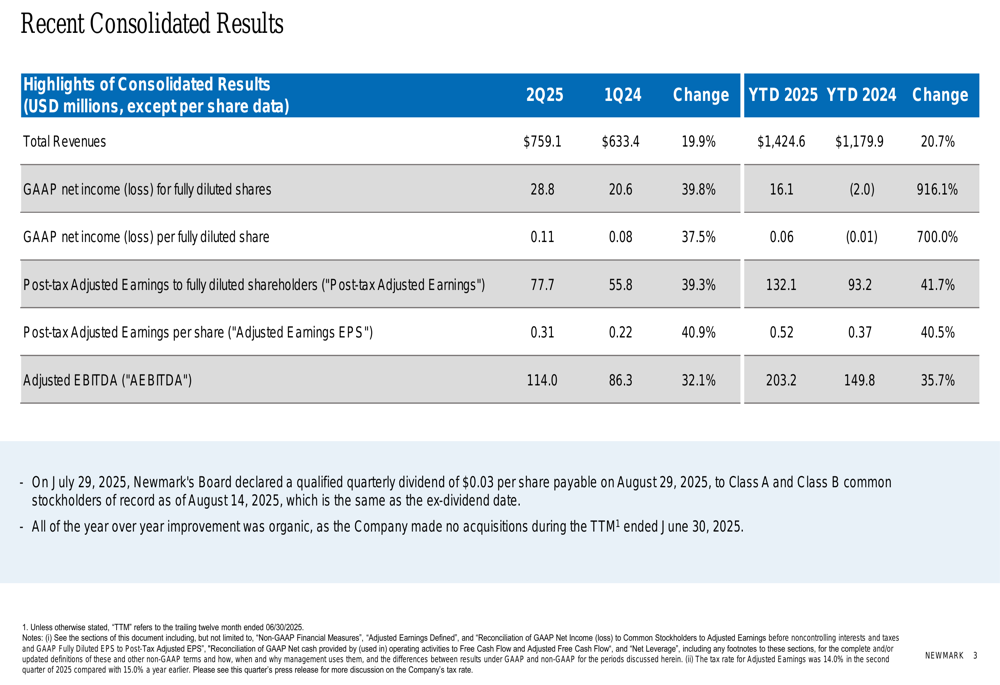

Newmark reported total revenues of $759.1 million for Q2 2025, representing a 19.9% increase compared to the same period last year. This strong top-line performance was accompanied by even more impressive growth in profitability metrics.

As shown in the following comprehensive financial table from the presentation:

The company’s GAAP net income for fully diluted shares reached $28.8 million, up 39.8% year-over-year, while GAAP earnings per share rose 37.5% to $0.11. On an adjusted basis, which excludes certain non-recurring items, Newmark’s performance was even stronger, with post-tax adjusted earnings increasing 39.3% to $77.7 million and adjusted earnings per share jumping 40.9% to $0.31.

Adjusted EBITDA grew 32.1% to $114.0 million, with the AEBITDA margin expanding 139 basis points to 15.0%, demonstrating the company’s improved operational efficiency and strong operating leverage.

The second quarter results continue the positive trajectory seen in Q1 2025, when the company reported a 21.8% revenue increase and 40% growth in adjusted EPS. Notably, management emphasized that all year-over-year improvement was organic.

Business Segment Analysis

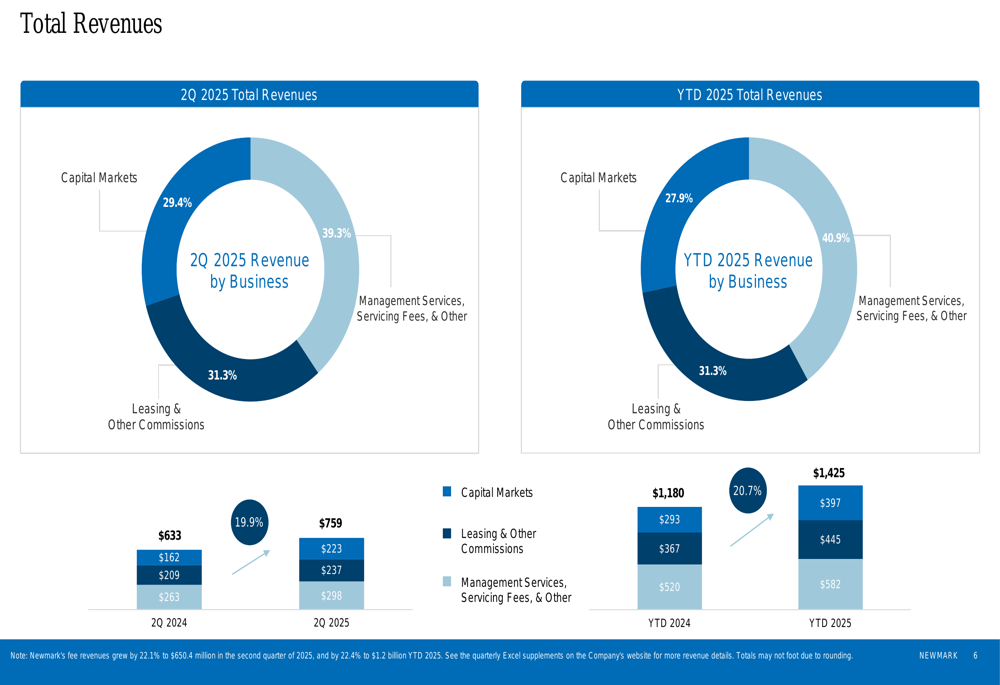

Newmark’s revenue growth was broad-based across all business segments. The following chart illustrates the distribution of total revenues by business line:

Management Services, Servicing Fees & Other represented the largest revenue segment at 39.3% of total revenues, followed by Leasing & Other Commissions at 31.3% and Capital Markets at 29.4%. All segments showed strong year-over-year growth, with Capital Markets experiencing the most significant increase.

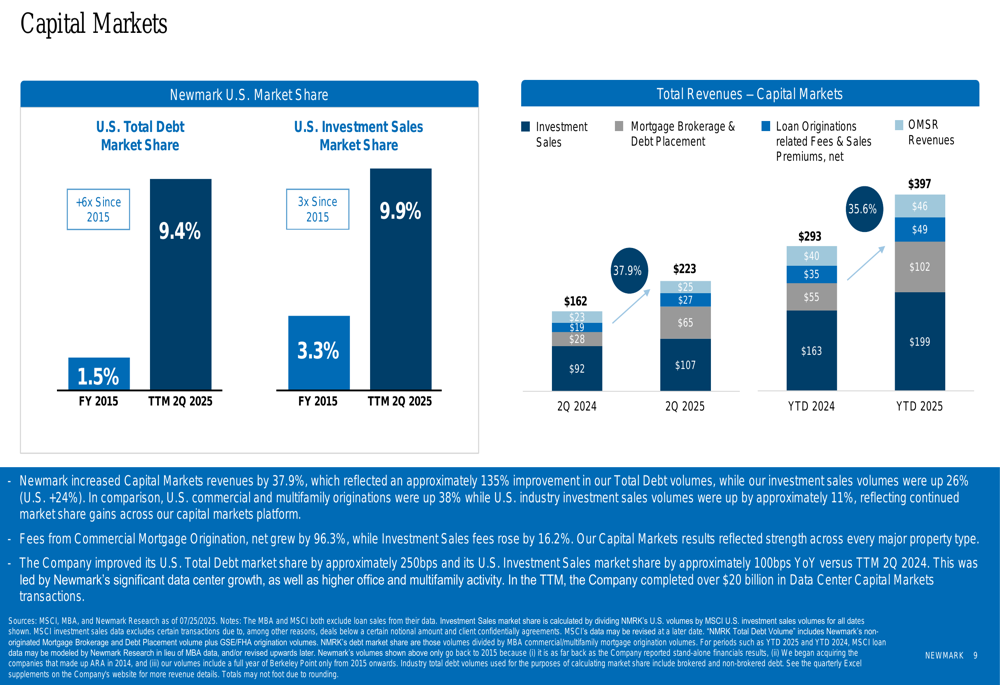

The Capital Markets segment, which includes investment sales, mortgage brokerage, and debt placement, has been a particular area of strength for Newmark, as shown in the following breakdown:

The company has significantly increased its U.S. market share in both total debt and investment sales since 2015, positioning it well to capitalize on the approximately $542 billion of potentially troubled commercial real estate debt maturing between 2025 and 2027.

Balance Sheet & Cash Flow

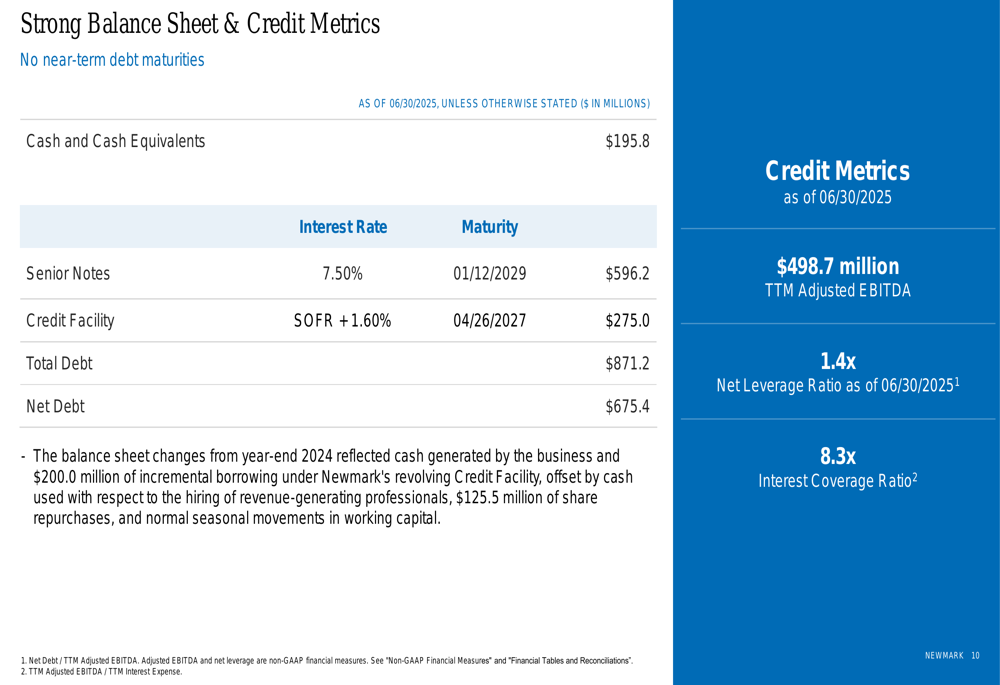

Newmark maintained a strong financial position at the end of Q2 2025, with $195.8 million in cash and cash equivalents. The company’s balance sheet strength is illustrated in the following slide:

The company reported total debt of $871.2 million and net debt of $675.4 million, resulting in a net leverage ratio of 1.4x as of June 30, 2025. This represents a slight increase from the 1.3x reported at the end of Q1 2025 but remains well within management’s target range.

Newmark’s capital-light business model, with approximately two-thirds of expenses being variable, contributes to its strong cash flow generation. The company generated $228.0 million of adjusted free cash flow and maintains a long-term capital deployment strategy of investing 50-60% in growth, returning 30-40% to shareholders, and allocating 10-20% for maintenance investments.

The Board declared a quarterly dividend of $0.03 per share, payable on August 29, 2025, to stockholders of record as of August 14, 2025.

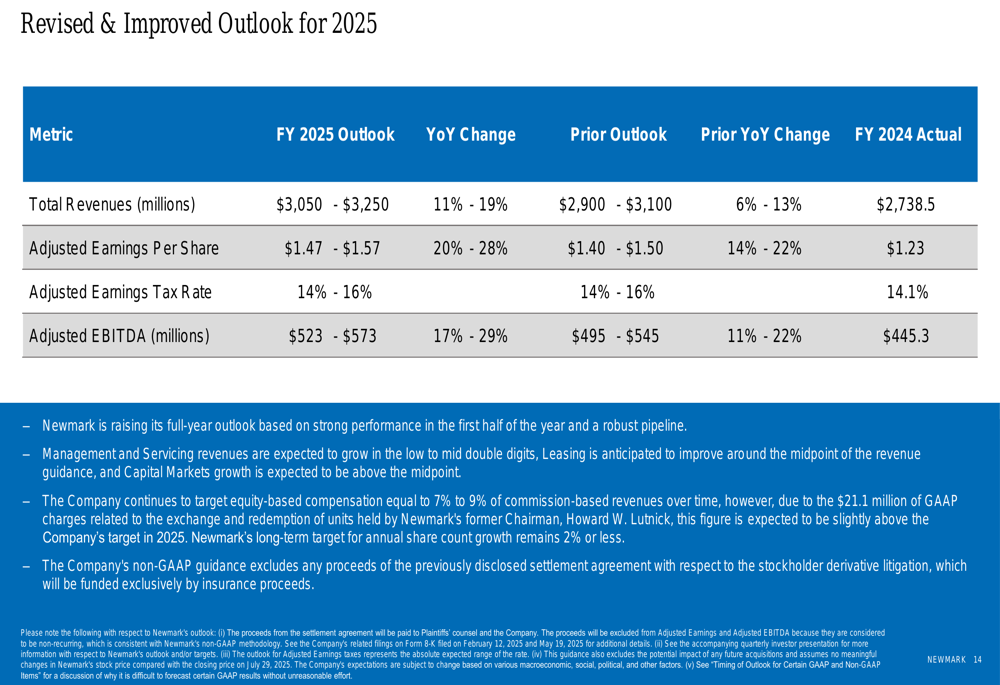

Revised Outlook & Guidance

Based on the strong first-half performance, Newmark has revised its full-year 2025 outlook upward. The updated guidance is presented in the following table:

The company now expects total revenues of $3,050-$3,250 million for fiscal year 2025, representing growth of 11-19% compared to FY 2024. This is an increase from the previous guidance of $2,900-$3,100 million.

Similarly, adjusted earnings per share guidance has been raised to $1.47-$1.57 (20-28% growth) from the previous $1.40-$1.50, and adjusted EBITDA is now expected to reach $523-$573 million (17-29% growth) compared to the earlier projection of $495-$545 million.

Industry Positioning & Strategy

Newmark continues to strengthen its position as a leading commercial real estate advisor and service provider, with over 8,400 professionals across 165 global client service locations. The company’s transaction volume reached approximately $1.1 trillion in 2024, and trailing twelve-month revenues exceeded $2.9 billion.

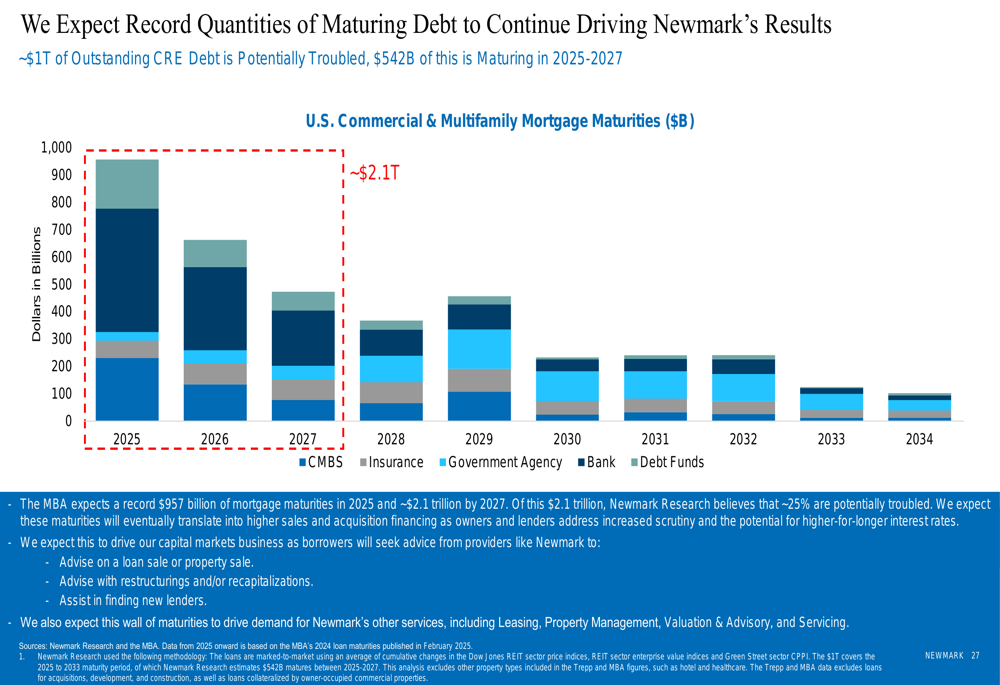

A key driver of Newmark’s future growth is expected to be the significant volume of commercial real estate debt maturing in the coming years, as illustrated in the following chart:

The company is strategically positioned to capitalize on this trend, with approximately $1 trillion of outstanding commercial real estate debt potentially troubled and $542 billion maturing between 2025 and 2027. This presents significant opportunities for Newmark’s capital markets business, particularly in debt restructuring and refinancing services.

During the Q1 2025 earnings call, CEO Barry Gossam had emphasized Newmark’s elevated brand status, noting, "We continue to elevate the brand. People call us for things they might not have called us for two years ago." The Q2 results appear to validate this strategy, with the company continuing to gain market share and expand its service offerings.

With its strong financial position, diversified revenue streams, and strategic positioning in high-growth segments of the commercial real estate market, Newmark appears well-positioned to continue its growth trajectory through the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.