Street Calls of the Week

Introduction & Market Context

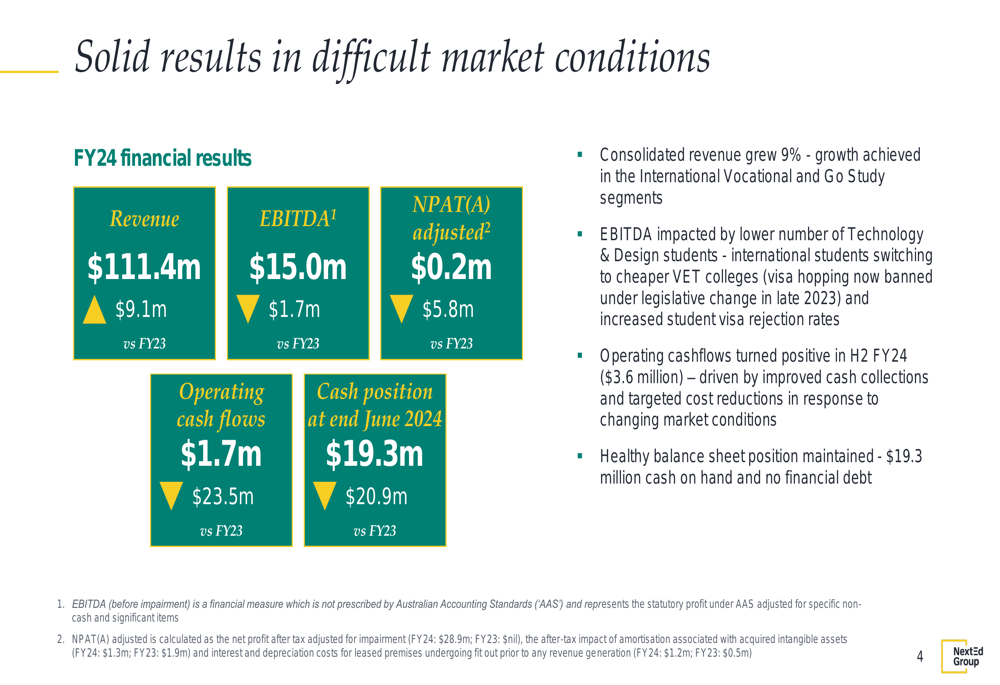

NextEd Group Ltd (ASX:NXD) presented its FY24 results on August 29, 2024, highlighting a 9% revenue growth to $111.4 million despite facing significant headwinds from government migration policy changes affecting international student visas. The education provider has strategically shifted its focus toward higher-margin vocational courses while implementing cost-saving measures to navigate the challenging regulatory environment.

As shown in the following comprehensive financial overview, NextEd achieved revenue growth while experiencing pressure on profitability metrics:

Financial Performance Highlights

NextEd’s consolidated revenue grew by 9% to $111.4 million, primarily driven by strong performance in the International Vocational and Go Study segments. However, EBITDA declined by 10% to $15.0 million, while adjusted NPAT(A) fell significantly by 97% to $0.2 million compared to the previous year.

The company’s cash position at the end of June 2024 stood at $19.3 million, down from $40.2 million a year earlier, reflecting investments in campus expansions and the impact of challenging market conditions. Notably, operating cash flows turned positive in H2 FY24 at $3.6 million, demonstrating improved cash collections and the early benefits of cost reduction initiatives.

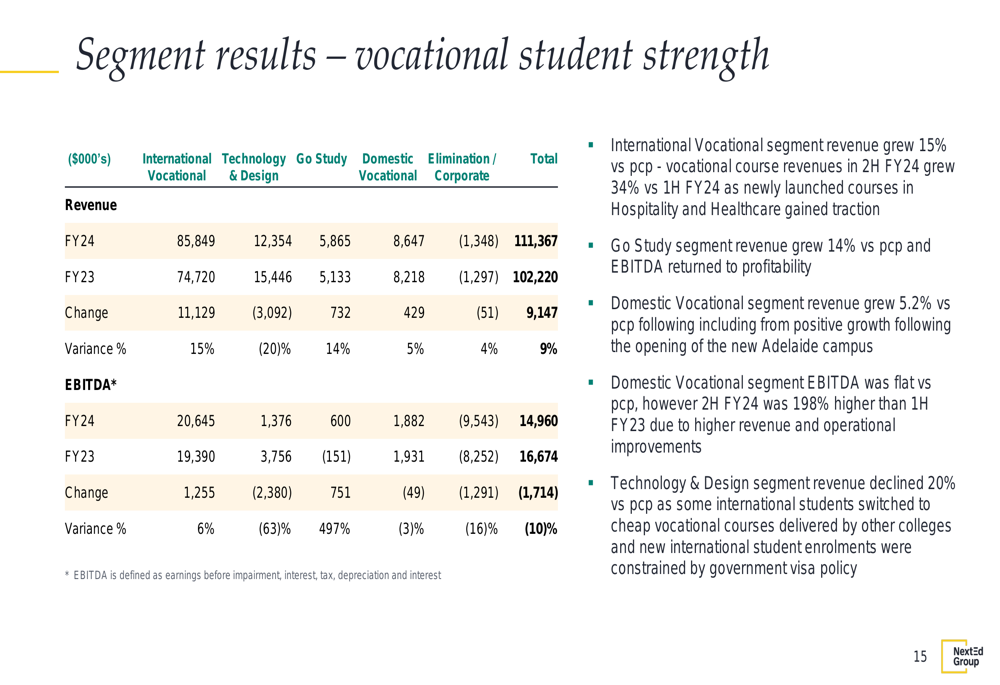

A detailed breakdown of revenue and profitability by segment reveals the varying performance across NextEd’s business units:

The International Vocational segment, which represents NextEd’s largest business unit, delivered 15% revenue growth to $85.8 million and a 6% increase in EBITDA to $20.6 million. This growth was primarily driven by higher-margin vocational courses, with second-half revenue growing 34% compared to the first half of FY24.

In contrast, the Technology & Design segment experienced a 20% decline in revenue to $12.4 million and a 63% drop in EBITDA to $1.4 million, as international students shifted toward more affordable vocational courses amid visa constraints.

Go Study returned to profitability with a 14% revenue increase to $5.9 million and a substantial EBITDA improvement to $0.6 million. The Domestic Vocational segment saw modest revenue growth of 5% to $8.6 million, while EBITDA declined slightly by 3% to $1.9 million.

Strategic Initiatives

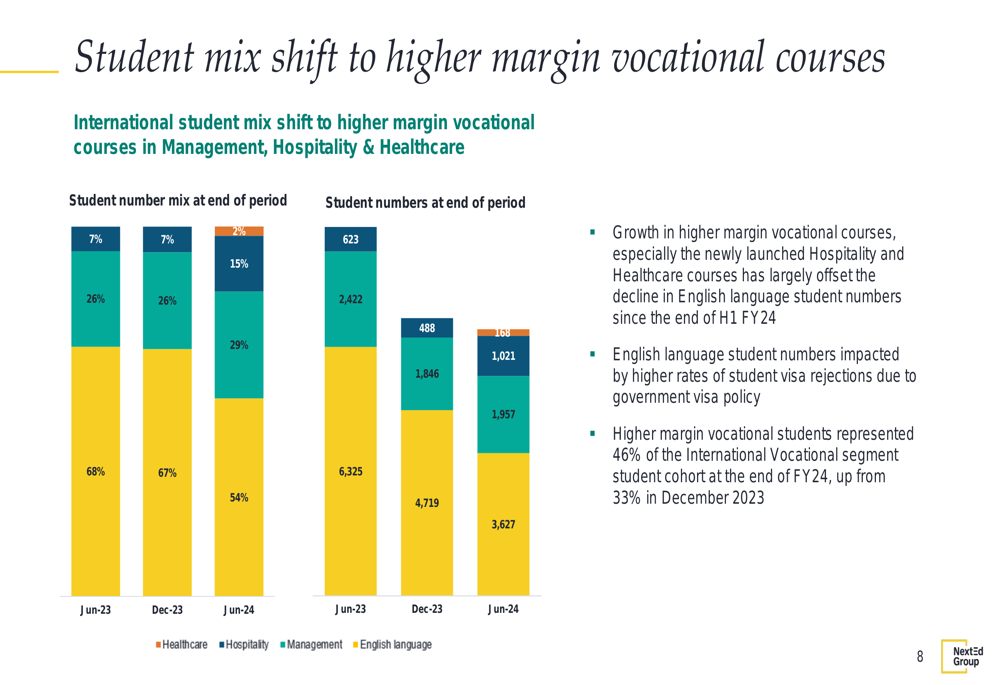

NextEd has successfully executed a strategic shift toward higher-margin vocational courses, particularly in Hospitality and Healthcare. The following chart illustrates this transition in the company’s student mix:

By the end of FY24, higher-margin vocational students represented 46% of the International Vocational segment’s student cohort, up from 33% in December 2023. This shift has helped offset the decline in English language student numbers, which have been impacted by higher rates of student visa rejections.

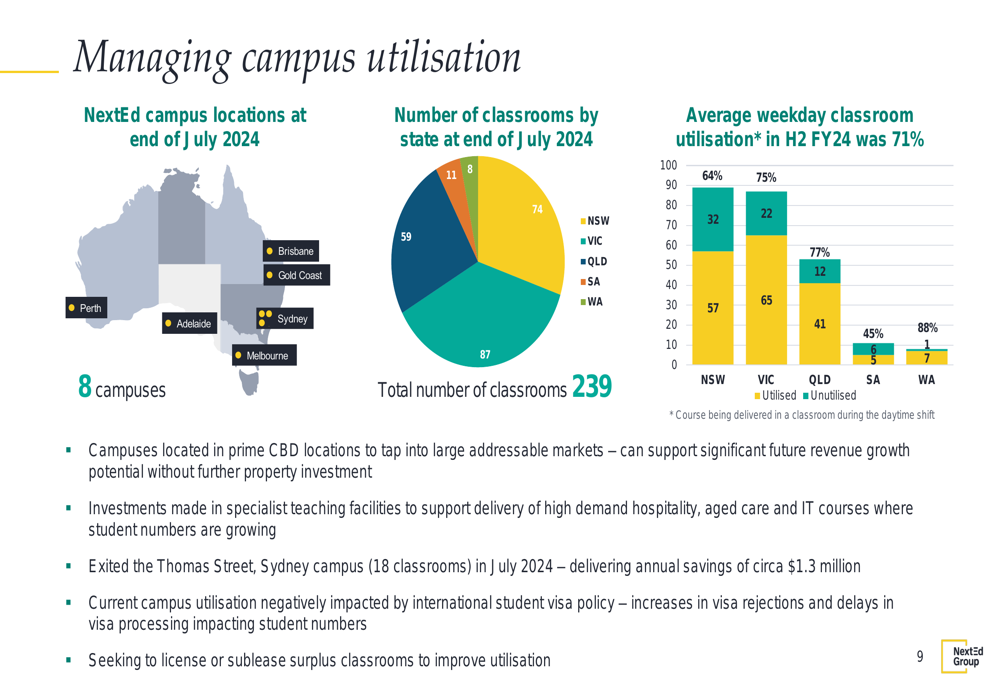

The company has also focused on optimizing its campus utilization across its national footprint. NextEd currently operates 8 campuses with 239 classrooms across five Australian states, achieving an average weekday classroom utilization rate of 71% in H2 FY24:

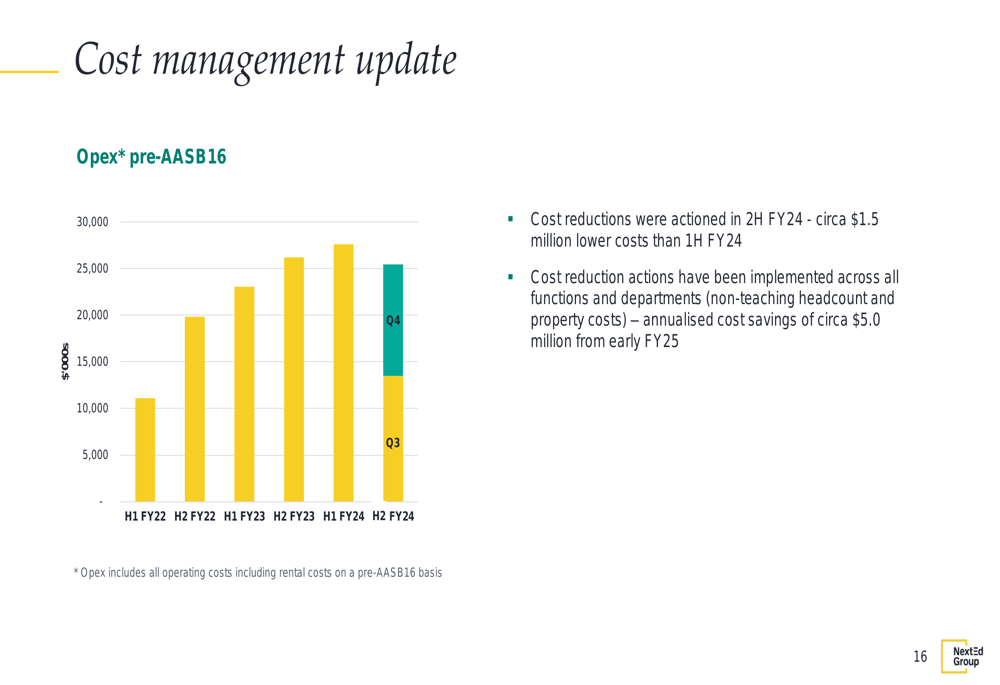

Cost management has been a key priority, with NextEd implementing annualized cost savings of approximately $5.0 million from early FY25. These savings include exiting leases in Sydney and Brisbane, discontinuing the use of short-term licensed classrooms, reducing non-teaching headcount, and optimizing discretionary spending.

The following chart demonstrates the company’s progress in reducing operating expenses:

Regulatory Challenges

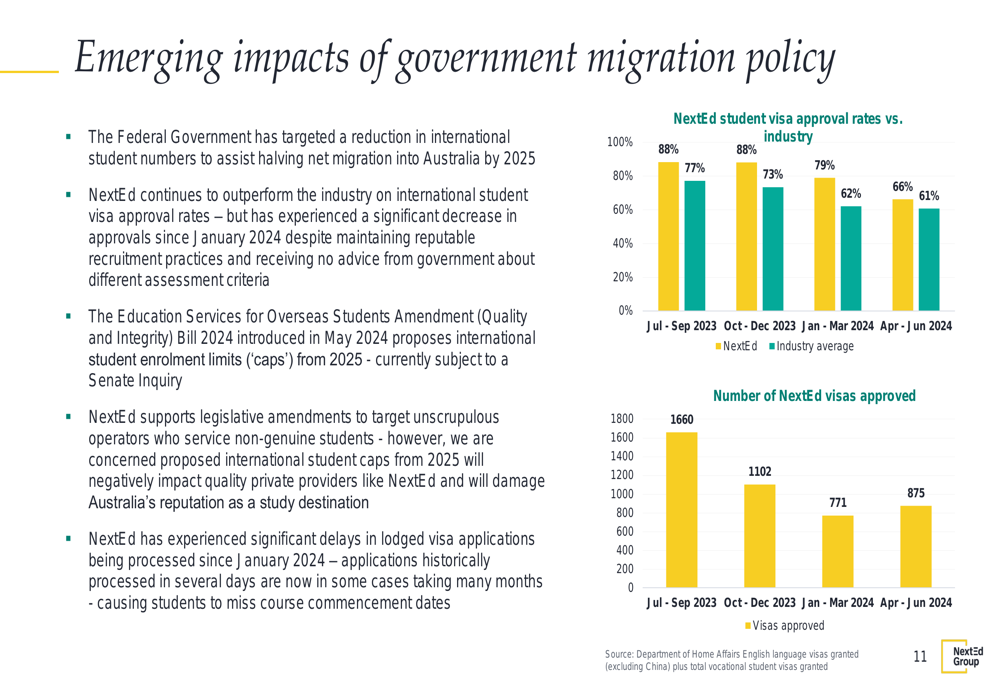

NextEd’s performance has been significantly impacted by changes in government migration policy, which aims to reduce international student numbers to halve net migration by 2025. The company has experienced a notable decrease in student visa approval rates since January 2024, although it continues to outperform industry averages:

The Education Services for Overseas Students Amendment Bill 2024, which proposes international student enrollment limits (’caps’) from 2025, presents an additional regulatory challenge. While NextEd supports legislative amendments targeting unscrupulous operators, the company has expressed concern about the potential impact of student caps on its business.

In response to these regulatory challenges, NextEd has implemented several strategic initiatives, including:

1. Focusing on growing domestic student revenues and profits

2. Prioritizing growth in high-demand, higher-margin vocational courses in Hospitality, Aged Care, and IT

3. Encouraging international students to package English language studies with NextEd’s vocational courses

4. Implementing cost base reductions

5. Ceasing campus footprint expansion and ending the lease over the Thomas Street campus in Sydney

Forward Outlook

NextEd expects that government policy will ultimately protect international education export earnings and support Australia’s workforce requirements. The company is positioning itself to capitalize on government policy changes once clarified and to take advantage of the likely tightened competitive landscape.

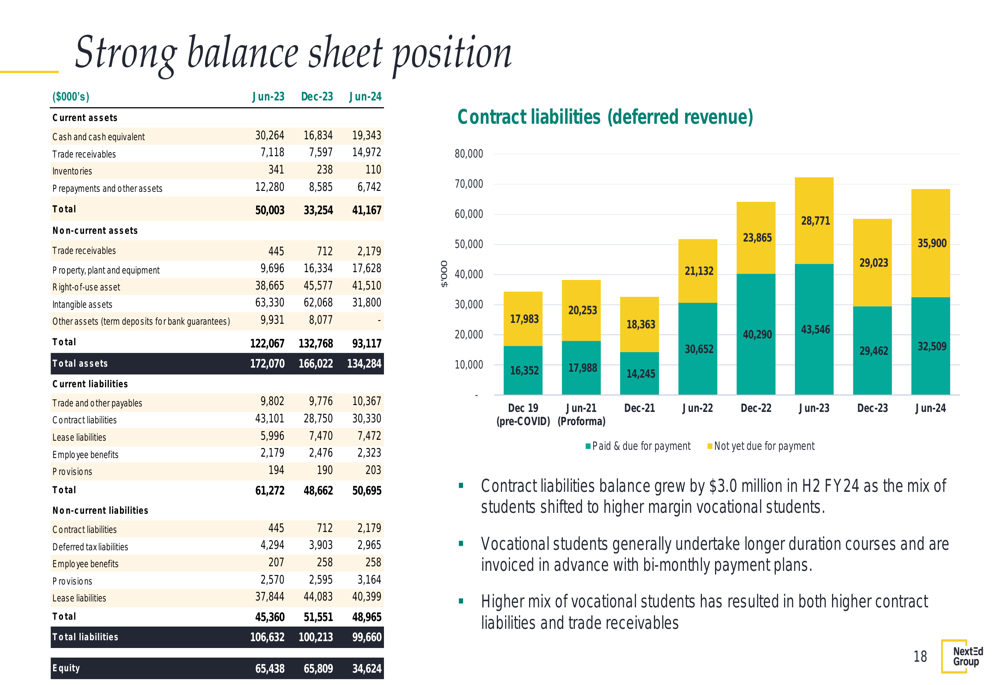

The company’s strategy leverages its differentiated market position, high-demand course range and study pathways, national campus footprint in prime CBD locations, and track record of adapting to market conditions. NextEd maintains a strong balance sheet with $19.3 million in cash and no financial debt, providing financial flexibility to navigate the current market challenges:

With its strategic shift toward higher-margin vocational courses, implementation of cost-saving measures, and focus on domestic student growth, NextEd appears well-positioned to manage the ongoing regulatory challenges in the international education sector while capitalizing on opportunities in the evolving market landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.