Bitcoin set for a rebound that could stretch toward $100000, BTIG says

Introduction & Market Context

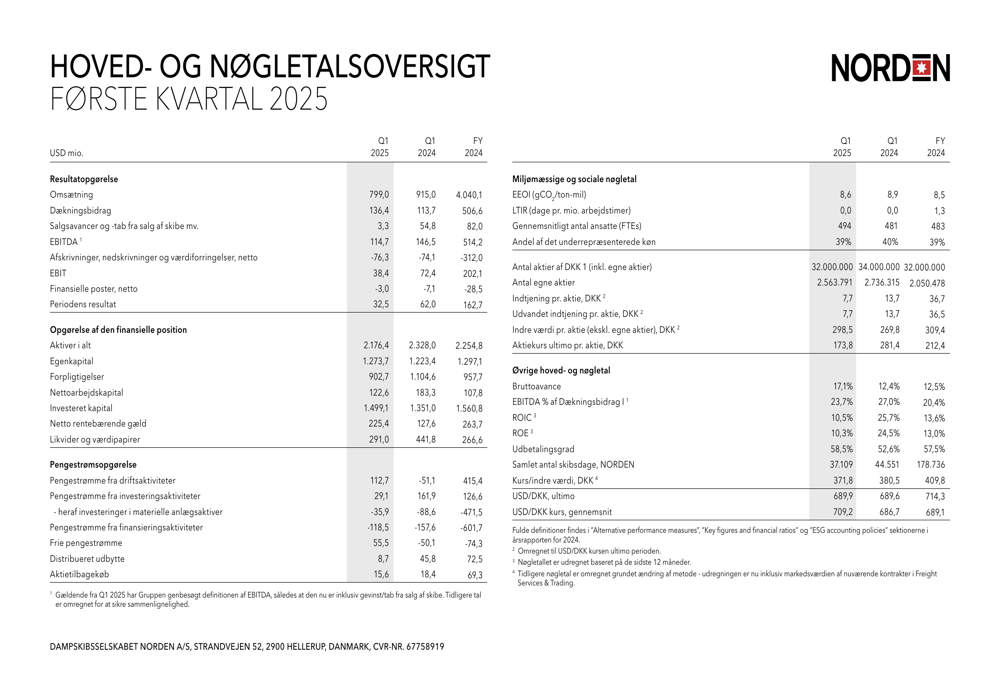

Dampskibsselskabet Norden AS (DNORD) released its first quarter 2025 financial results on May 1, showing a mixed performance characterized by declining revenue and profits but improved margins and operational cash flow. The Danish shipping company’s shares currently trade at 178.8 DKK, significantly below their 52-week high of 347 DKK, reflecting ongoing challenges in the global shipping market.

The Q1 results demonstrate NORDEN’s efforts to enhance operational efficiency amid reduced fleet utilization, with total ship days decreasing by 16.7% compared to the same period last year.

Quarterly Performance Highlights

NORDEN reported Q1 2025 revenue of $799 million, a 12.7% decrease from $915 million in Q1 2024. Net profit fell more substantially, dropping 47.6% to $32.5 million from $62 million in the prior-year quarter. This decline was partly attributed to significantly lower gains from ship sales, which totaled just $3.3 million compared to $54.8 million in Q1 2024.

Despite these challenges, the company achieved notable improvements in gross profit margin, which expanded to 17.1% from 12.4% in Q1 2024. This margin enhancement suggests successful cost management and operational optimization despite the revenue contraction.

The most dramatic improvement came in cash flow generation, with operating cash flow surging to $112.7 million compared to a negative $51.1 million in the same period last year. Free cash flow also turned positive at $55.5 million, a substantial improvement from the negative $50.1 million recorded in Q1 2024.

Detailed Financial Analysis

NORDEN’s EBITDA decreased by 21.7% year-over-year to $114.7 million, while EBIT fell by 47% to $38.4 million. The company’s financial position remains solid, with total assets of $2.18 billion and equity of $1.27 billion as of March 31, 2025.

The company has reduced its net interest-bearing debt to $225.4 million from $263.7 million at the end of 2024, while maintaining a healthy cash and securities position of $291 million. This financial discipline is reflected in the company’s continued share repurchase program, with $15.6 million spent on buybacks during the quarter, though at a reduced rate compared to previous periods.

NORDEN’s return metrics have declined year-over-year, with Return on Invested Capital (ROIC) falling to 10.5% from 25.7% in Q1 2024, and Return on Equity (ROE) decreasing to 10.3% from 24.5%. However, both metrics remain in positive double-digit territory, indicating continued profitability despite the challenging environment.

The company’s capital allocation strategy appears more conservative than in previous periods, with dividend distributions reduced to $8.7 million from $45.8 million in Q1 2024, likely reflecting the more challenging operating environment and reduced profitability.

Strategic Initiatives and Outlook

NORDEN’s operational strategy shows signs of fleet optimization, with total ship days decreasing to 37,109 in Q1 2025 from 44,551 in the same period last year. This 16.7% reduction suggests the company is focusing on efficiency rather than scale, potentially in response to market conditions.

The company continues to make progress on environmental metrics, with its Energy Efficiency Operational Indicator (EEOI) improving to 8.6 gCO2/ton-mile from 8.9 in Q1 2024. This demonstrates NORDEN’s ongoing commitment to sustainability despite financial pressures.

NORDEN has maintained its workforce diversity, with the proportion of the underrepresented gender stable at 39%, nearly unchanged from 40% in Q1 2024. The company’s total workforce has increased slightly to 494 full-time equivalents from 481 a year earlier.

While the presentation materials don’t explicitly outline forward guidance, the company’s focus on margin improvement and cash flow generation suggests a strategic shift toward operational efficiency and financial resilience in what appears to be a challenging market environment for the shipping sector.

Investors will likely focus on whether NORDEN can sustain its margin improvements and strong cash flow generation in future quarters, potentially offsetting the impact of revenue declines as the company navigates through 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.