Street Calls of the Week

Introduction & Market Context

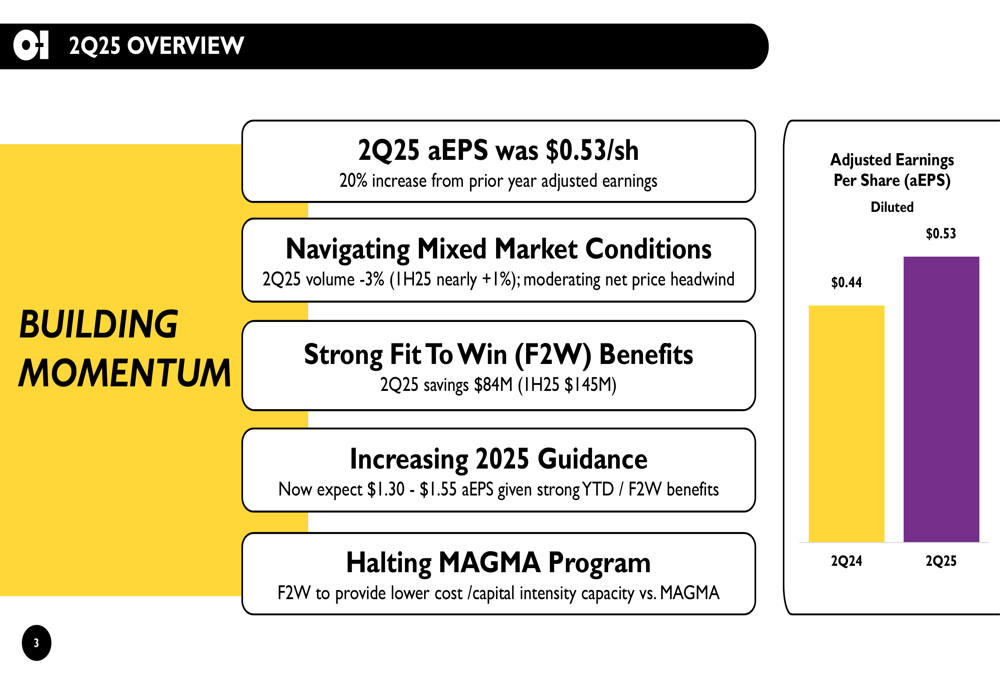

O-I Glass Inc. (NYSE:OI) released its second quarter 2025 earnings presentation on July 30, 2025, revealing a 20% increase in adjusted earnings per share despite facing mixed market conditions. The glass packaging manufacturer continues to navigate regional disparities while making significant progress on its cost-saving initiatives.

The company’s stock has shown positive momentum in recent months, with fundamentals data showing a 52-week range of $9.23 to $16.04. Following the earnings release, the stock showed minimal movement in aftermarket trading, with a slight 0.07% increase to $14.41.

Quarterly Performance Highlights

O-I Glass reported second quarter 2025 adjusted earnings per share of $0.53, representing a 20% increase from $0.44 in the prior year period. This performance continues the positive momentum seen in Q1 2025, when the company reported $0.40 per share, exceeding analyst expectations at that time.

As shown in the following chart comparing Q2 2024 and Q2 2025 adjusted earnings per share:

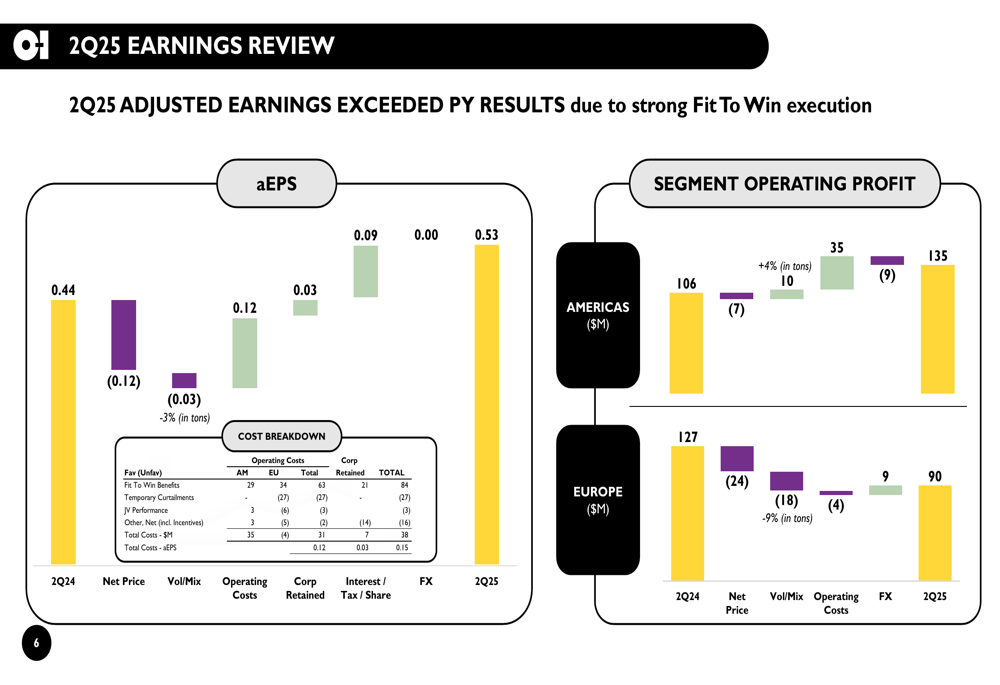

The company achieved this earnings growth despite a 3% decline in sales volume during the quarter. Net sales for Q2 2025 were $1,706 million, slightly down from $1,729 million in Q2 2024. Segment operating profit totaled $225 million compared to $233 million in the prior year period.

A detailed breakdown of the factors affecting earnings performance reveals that operating costs improvements and net price contributed positively, while volume/mix had a negative impact:

Regional Performance Analysis

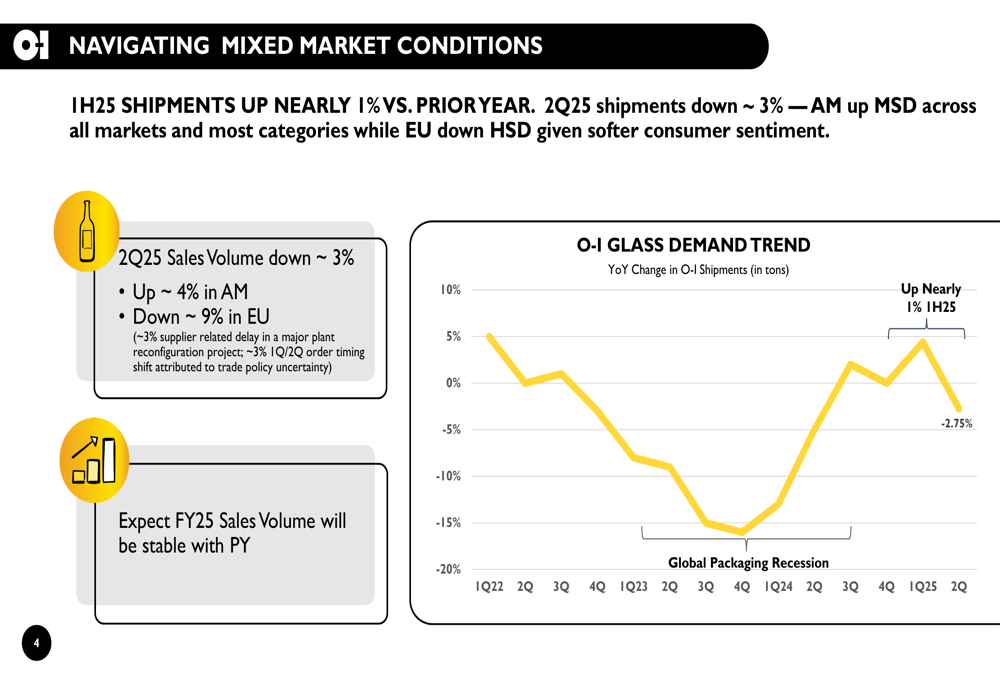

O-I Glass experienced significant regional disparities in performance during Q2 2025. The Americas segment showed resilience with shipments up approximately 4%, while Europe faced challenges with shipments down about 9%. The European decline was attributed to softer consumer sentiment (3%), supplier-related delays (3%), and order timing shifts between quarters (3%).

The following chart illustrates the company’s global demand trends, showing the mixed market conditions across regions:

This regional divergence is further reflected in segment operating profit, with the Americas increasing to $135 million from $106 million in Q2 2024, while Europe declined to $90 million from $127 million. Management noted that despite these challenges, they expect full-year 2025 sales volume to remain stable compared to the prior year.

Fit To Win Progress

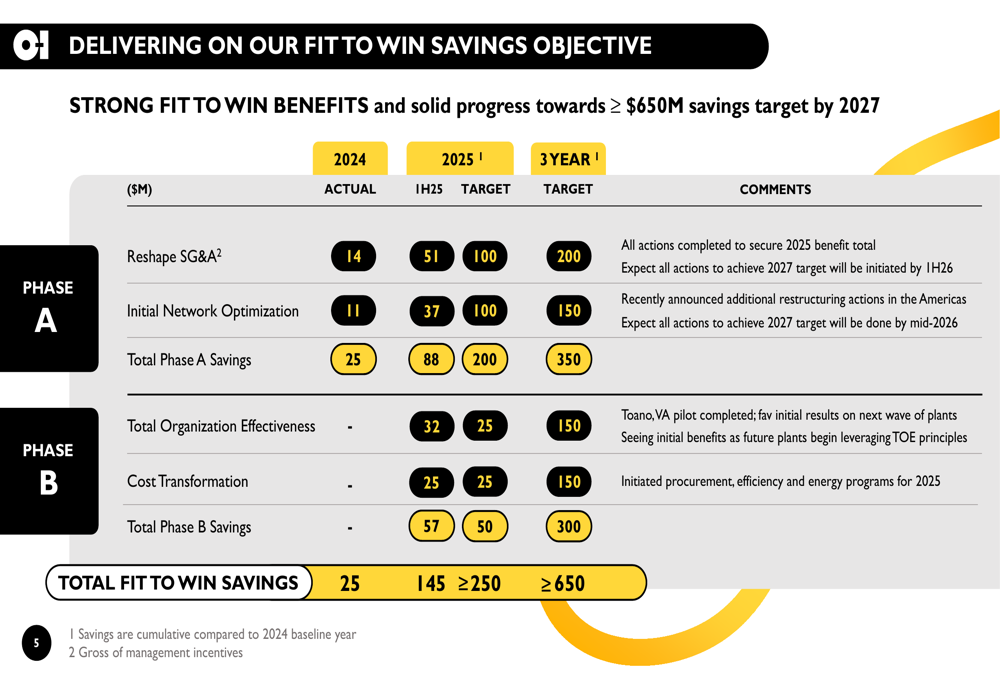

A key driver of O-I Glass’s improved profitability is the company’s "Fit To Win" (F2W) cost-saving program, which generated $84 million in savings during Q2 2025 and $145 million in the first half of the year. The program targets at least $650 million in cumulative savings by 2027.

The following table details the progress and targets of the Fit To Win program across various initiatives:

The program consists of two phases. Phase A includes reshaping SG&A and initial network optimization, which contributed $88 million in savings during the first half of 2025. Phase B focuses on total organization effectiveness and cost transformation, adding another $57 million in savings. This strong execution has positioned the company to exceed its 2025 target of at least $250 million in savings.

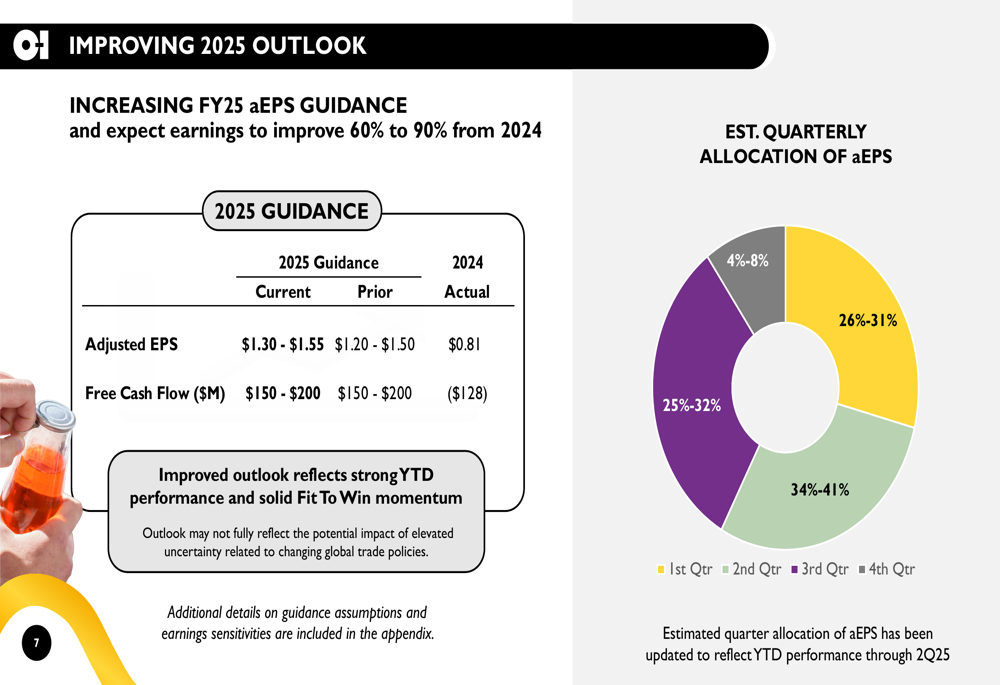

Improved 2025 Outlook

Based on the strong year-to-date performance and momentum from the Fit To Win program, O-I Glass has increased its full-year 2025 guidance. The company now expects adjusted EPS of $1.30-$1.55, up from the previous guidance of $1.20-$1.50 provided during the Q1 earnings report.

The following chart shows the improved outlook and quarterly allocation of expected earnings:

This updated guidance represents a significant improvement of 60-90% compared to 2024 actual results of $0.81 per share. Free cash flow expectations remain unchanged at $150-$200 million, which would be a substantial improvement from the negative $128 million reported in 2024.

Key assumptions underlying the 2025 outlook include adjusted EBITDA of $1.17-$1.21 billion, a net price headwind of $100-$125 million year-over-year, and capital expenditures of $400-$450 million.

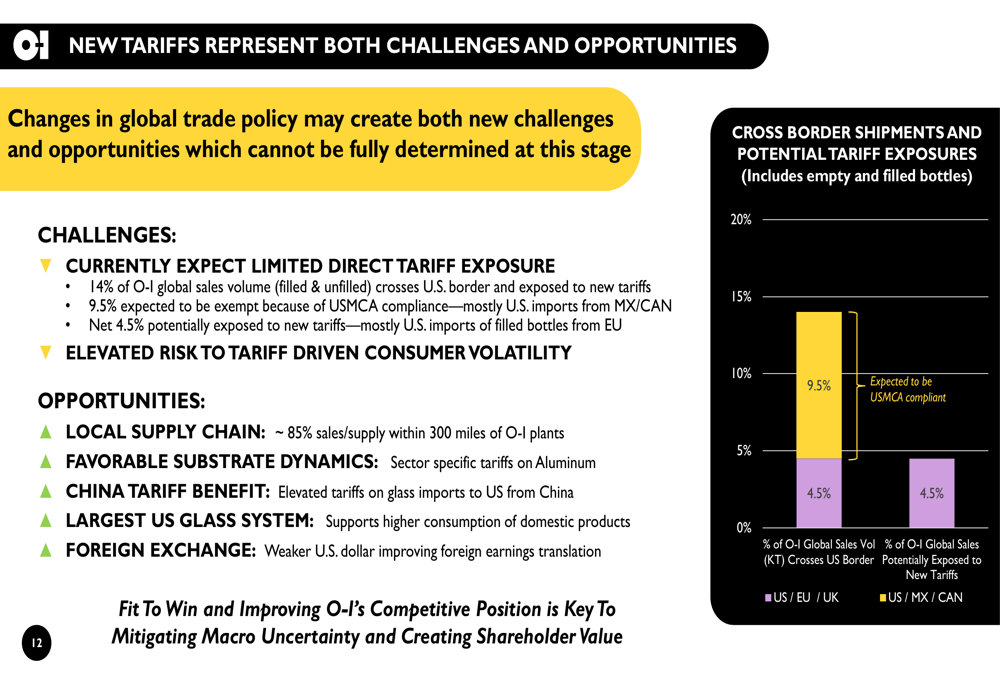

Strategic Initiatives and Tariff Impact

In a significant strategic shift, O-I Glass announced it is halting its MAGMA program, noting that the Fit To Win initiatives will provide lower cost and capital intensity capacity compared to MAGMA. This decision aligns with the company’s focus on improving efficiency and capital allocation.

The company also addressed the potential impact of new tariffs, presenting both challenges and opportunities:

O-I Glass expects limited direct tariff exposure, with only 4.5% of its global sales volume potentially affected by new tariffs, primarily U.S. imports of filled bottles from the EU. The company highlighted several potential advantages from the changing trade landscape, including its local supply chain model (approximately 85% of sales/supply within 300 miles of plants), favorable substrate dynamics from aluminum-specific tariffs, and benefits from increased tariffs on glass imports from China.

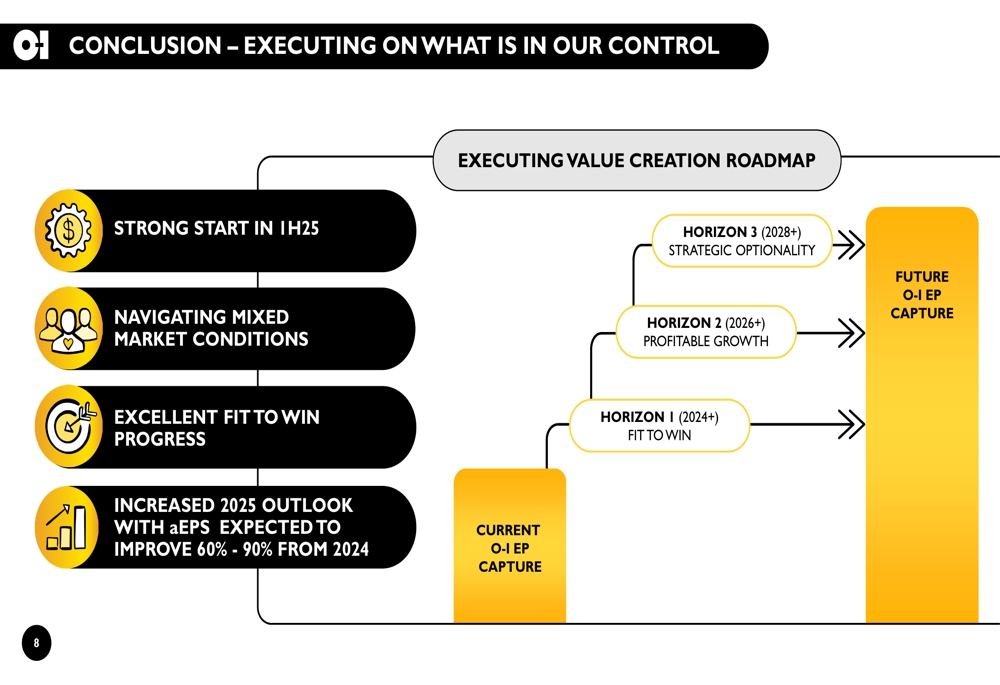

Looking ahead, O-I Glass outlined its value creation roadmap with multiple horizons: Fit To Win (2024+), Profitable Growth (2026+), and Strategic Optionality (2028+). This phased approach demonstrates management’s commitment to delivering sustainable long-term value while addressing near-term challenges.

With the strong first half performance and increased guidance, O-I Glass appears well-positioned to continue its earnings improvement trajectory through 2025, despite the ongoing challenges in certain markets, particularly Europe.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.