Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

Olin Corporation (NYSE:OLN) presented its first quarter 2025 earnings results on May 2, 2025, reporting an Adjusted EBITDA of $186 million, slightly down from $193 million in the previous quarter but showing a more significant decline from $242 million in the same quarter last year. The chemical and ammunition manufacturer highlighted its strategic progress, including a recent acquisition and debt refinancing, while navigating mixed performance across its business segments.

The company’s stock responded positively in after-hours trading, rising 6% to $22.95, suggesting investors were encouraged by the results and outlook despite some ongoing challenges in key business areas.

Quarterly Performance Highlights

Olin’s presentation emphasized "controlling the controllable" amid varying market conditions across its three business segments. The company reported total sales of $1.65 billion for Q1 2025, with its Chlor Alkali Products & Vinyls (CAPV) segment showing resilience, while Epoxy continued to operate at a loss and Winchester faced significant headwinds in its commercial business.

As shown in the following quarterly highlights slide, Olin accommodated additional demand related to chlorine industry supply disruptions, maintained ECU value stability, and completed a strategic bond refinancing:

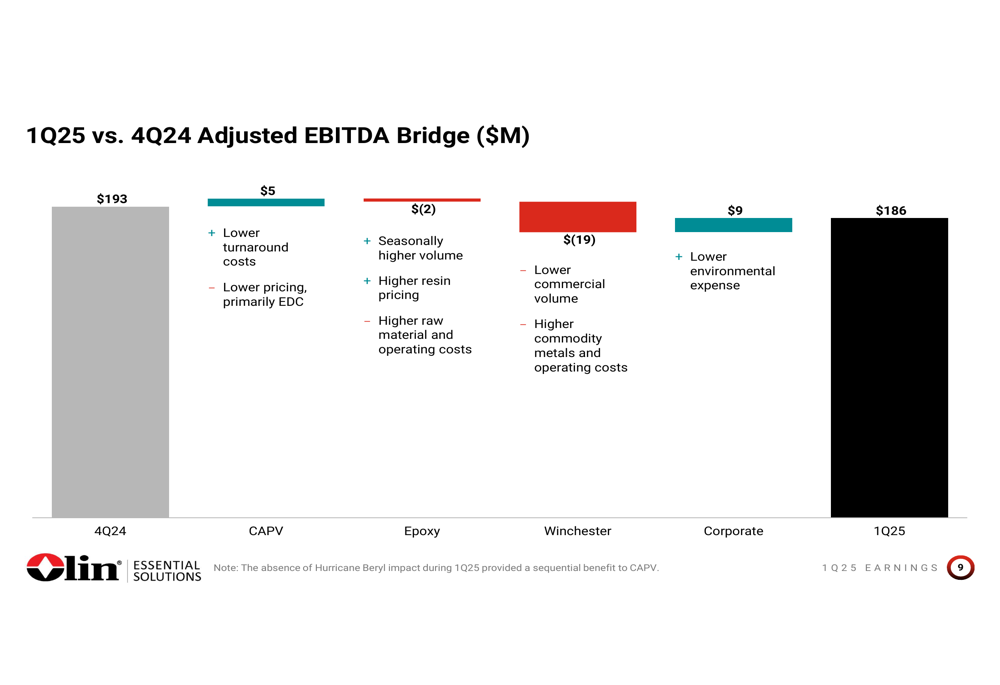

The company’s Adjusted EBITDA bridge from Q4 2024 to Q1 2025 illustrates the varying performance across segments, with CAPV improving by $5 million, Epoxy declining by $2 million, and Winchester dropping by $19 million. Corporate expenses decreased by $9 million, primarily due to lower environmental costs:

Segment Analysis

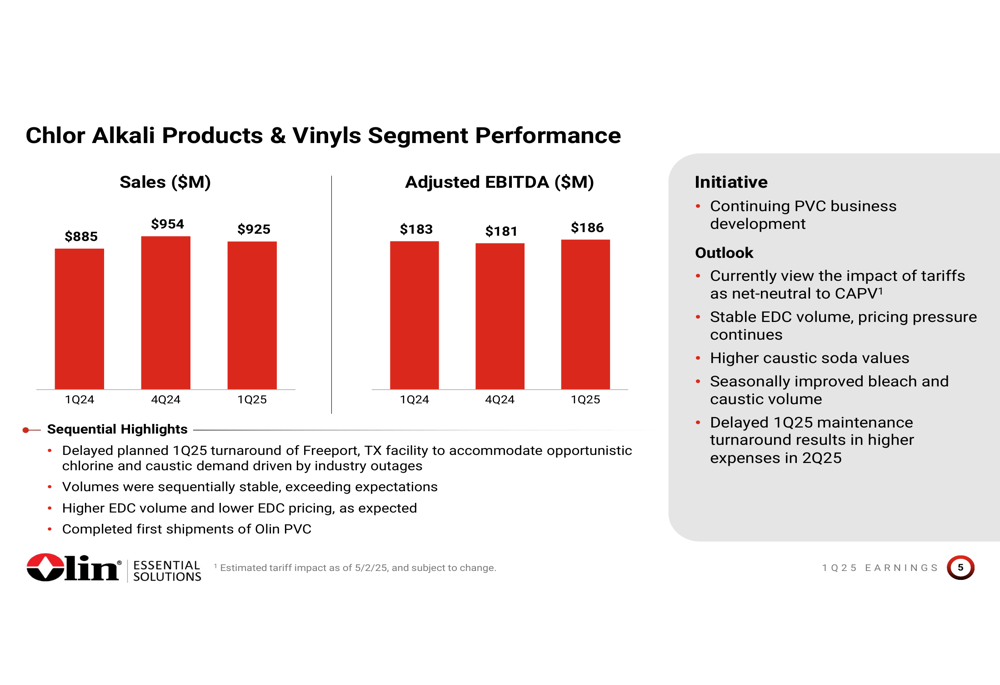

Chlor Alkali Products & Vinyls (CAPV)

The CAPV segment, Olin’s largest business unit, delivered sales of $925 million and Adjusted EBITDA of $186 million in Q1 2025, showing modest improvement from the previous quarter’s $181 million. The company delayed a planned maintenance outage at its Freeport, TX facility to accommodate additional demand related to industry supply disruptions, while experiencing stable volumes and higher EDC (ethylene dichloride) volume, albeit with lower EDC pricing.

The segment’s performance data and outlook are detailed in the following slide:

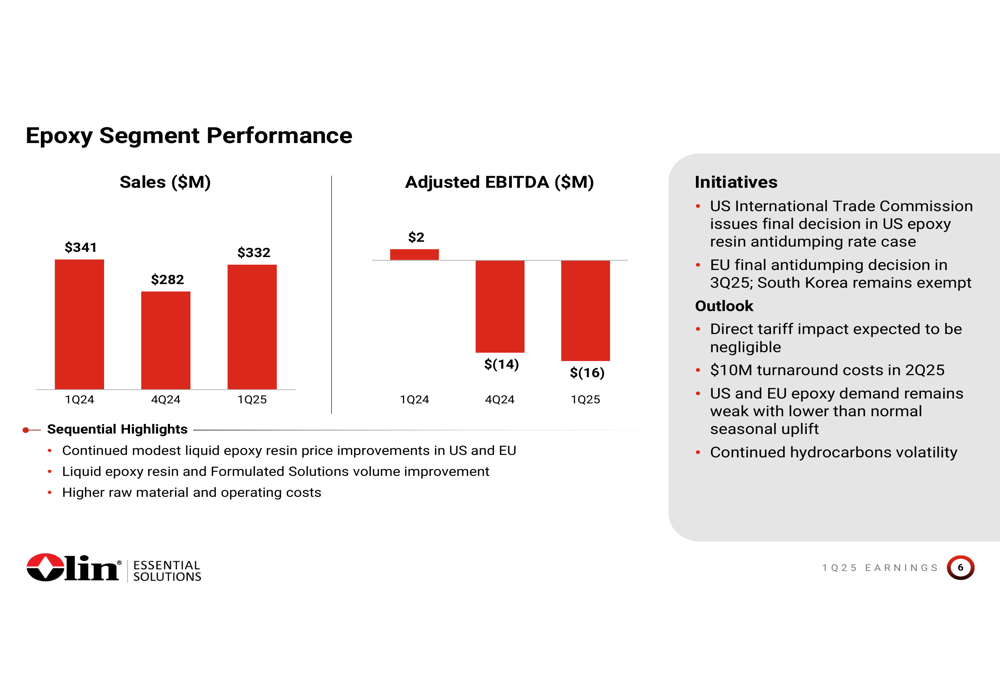

Epoxy

Olin’s Epoxy segment continued to face challenges, reporting sales of $332 million but an Adjusted EBITDA loss of $16 million in Q1 2025, slightly worse than the $14 million loss in Q4 2024. Despite modest liquid epoxy resin price improvements in the US and EU and volume improvements in both liquid epoxy resin and formulated solutions, higher raw material and operating costs offset these gains.

The segment is awaiting final decisions on antidumping cases in both the US and EU, with the EU final decision expected in Q3 2025. Management noted that US and EU epoxy demand remains weak with lower than normal seasonal uplift.

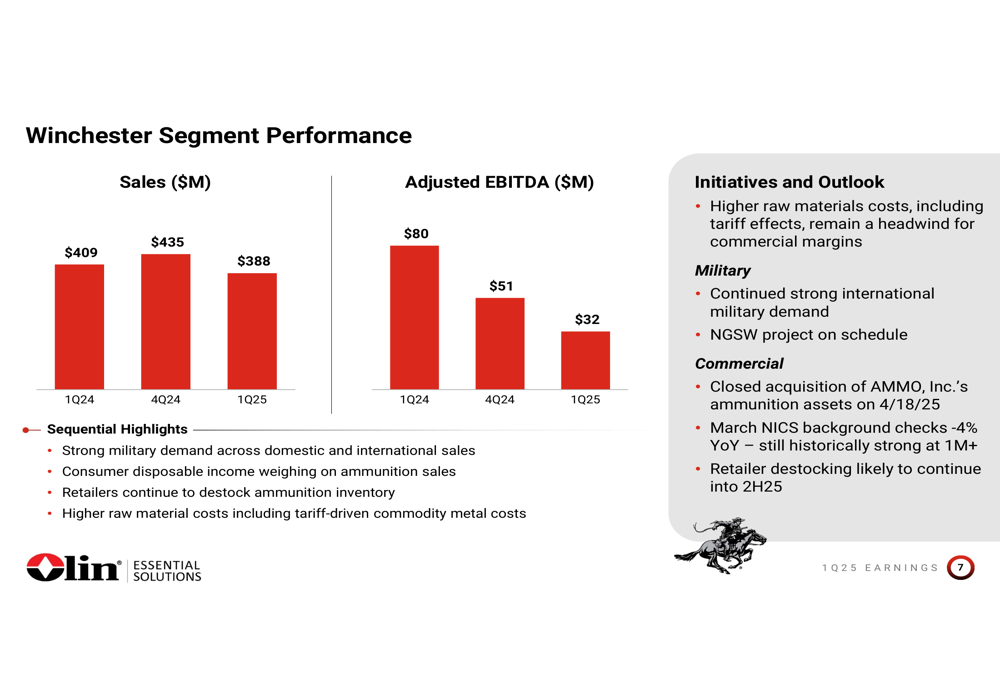

Winchester

The Winchester ammunition segment experienced the most significant decline among Olin’s businesses, with Adjusted EBITDA falling to $32 million in Q1 2025 from $51 million in Q4 2024 and $80 million in Q1 2024. While military demand remained strong, consumer disposable income pressures weighed on ammunition sales, and retailers continued to destock inventory. Higher raw material costs, including tariff effects, further compressed margins.

Strategic Initiatives and Acquisitions

A key highlight of Olin’s presentation was the completed acquisition of AMMO, Inc.’s production assets for $56 million. The acquisition brings world-class shell case manufacturing capabilities and a skilled workforce of over 200 employees. Management expects first-year Adjusted EBITDA contribution of $10-15 million, growing to approximately $40 million by the third year including synergies.

The following slide details the strategic rationale and financial expectations for the acquisition:

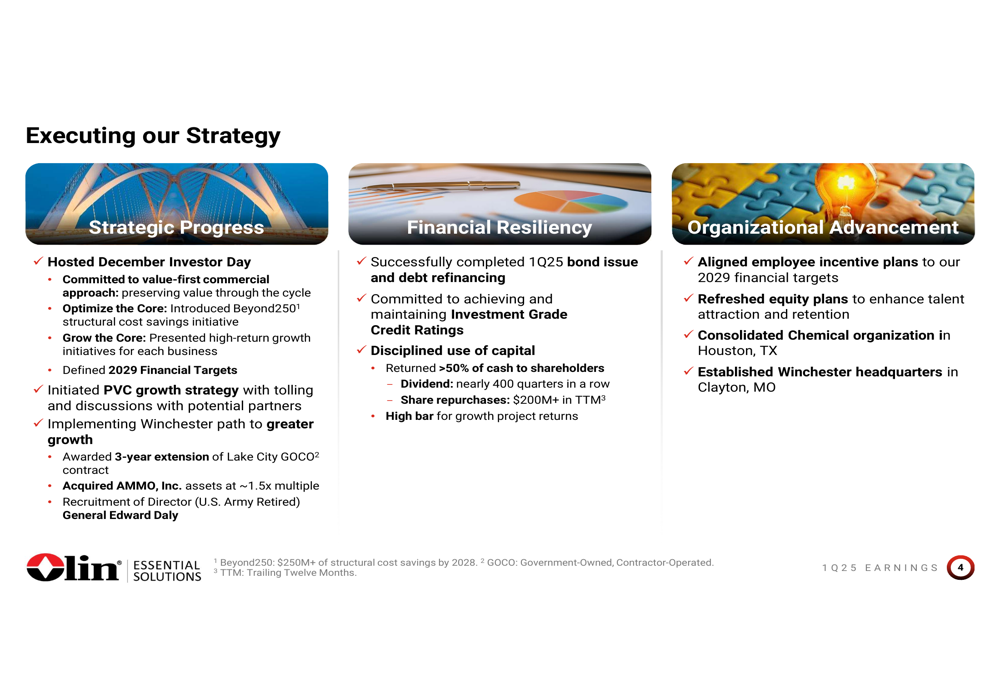

Olin also outlined its broader strategic execution across three key areas: Strategic Progress, Financial Resiliency, and Organizational Advancement. Notable achievements include the introduction of the "Beyond250" structural cost savings initiative, a 3-year extension of Winchester’s Lake City GOCO contract, and the consolidation of the Chemical organization in Houston, TX.

Financial Position and Outlook

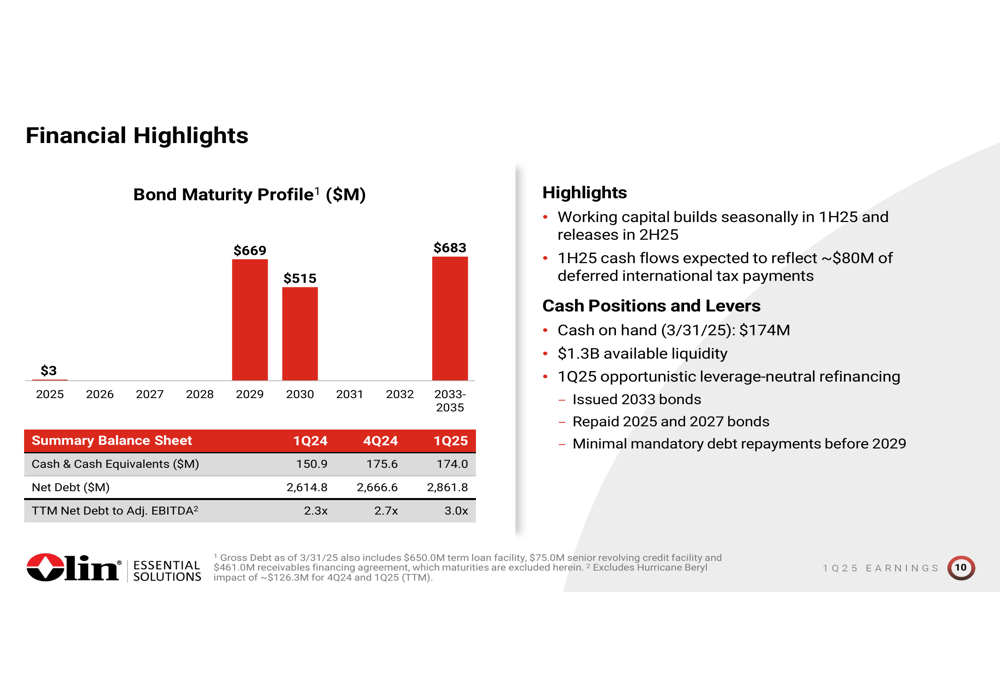

Olin successfully completed a bond issue and debt refinancing in Q1 2025, pushing its nearest significant debt maturity out to 2029. However, the company’s leverage increased, with the trailing twelve months Net Debt to Adjusted EBITDA ratio rising to 3.0x from 2.7x in the previous quarter.

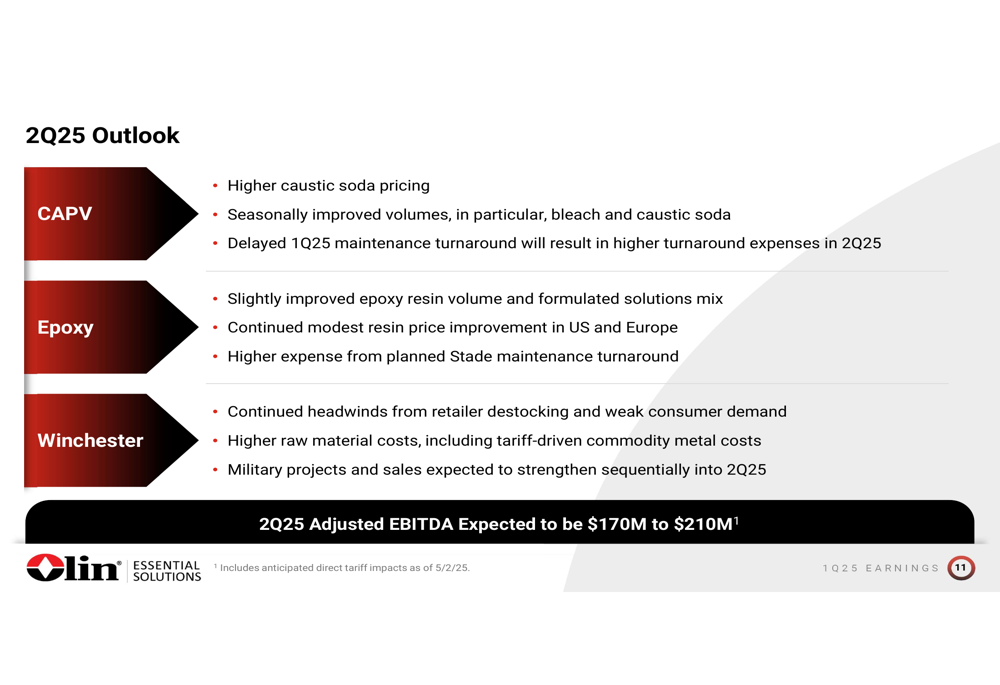

Looking ahead to Q2 2025, Olin expects Adjusted EBITDA in the range of $170-210 million. The outlook varies by segment, with CAPV anticipating higher caustic soda pricing and seasonally improved volumes but increased turnaround expenses. Epoxy expects slightly improved volumes and continued modest price improvements, while Winchester continues to face headwinds from retailer destocking and weak consumer demand.

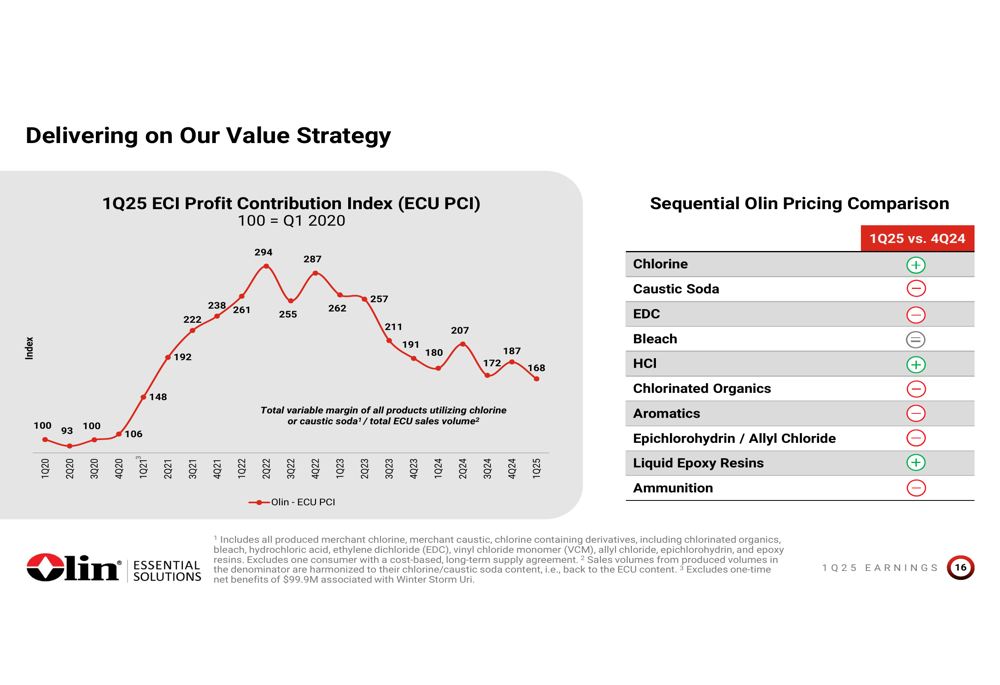

Management also provided insight into pricing trends across its product portfolio, showing positive or stable pricing for chlorine, caustic soda, bleach, HCl, and liquid epoxy resins, while EDC, chlorinated organics, aromatics, epichlorohydrin/allyl chloride, and ammunition experienced price declines:

The company’s maintenance turnaround expenses are expected to increase in Q2 2025, particularly for the CAPV segment due to the delayed Freeport, TX chlor alkali turnaround, and for the Epoxy segment with the planned Stade, Germany turnaround.

As Olin navigates through 2025, management remains focused on executing its value-first commercial approach, maintaining financial resilience through disciplined capital allocation, and advancing organizational initiatives to position the company for long-term success despite current market challenges in some of its key segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.