Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Optiva Inc. (TSX:OPT) presented its second quarter 2025 results on August 12, highlighting strategic wins and technological advancements against a backdrop of financial challenges. The telecom Business Support Systems (BSS) provider continues to focus on cloud transformation and artificial intelligence integration while working to stabilize its financial performance.

The company’s stock closed at $0.61 on September 12, 2025, near its 52-week low of $0.36, reflecting ongoing investor concerns despite management’s emphasis on strategic progress and new customer acquisitions.

Quarterly Performance Highlights

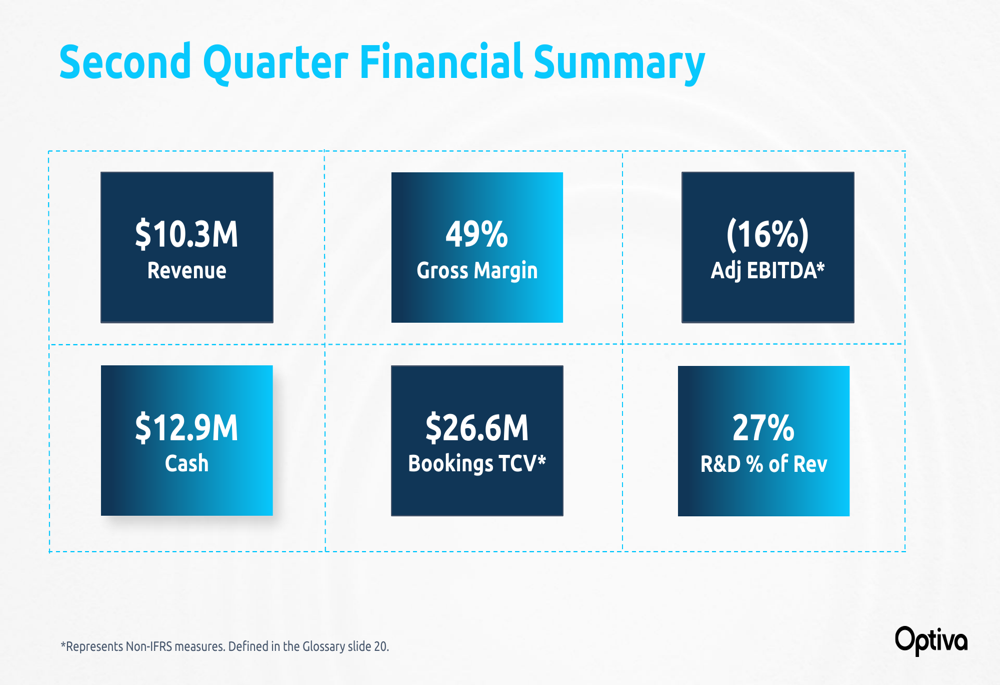

Optiva reported mixed financial results for Q2 2025, with revenue of $10.3 million and a gross margin of 49%, significantly lower than previous quarters. Adjusted EBITDA remained negative at -16%, while R&D expenses represented 27% of revenue, indicating continued investment in product development despite profitability challenges.

As shown in the following financial summary from the presentation:

On a more positive note, the company secured $26.6 million in new bookings (Total Contract Value) during the quarter, including two significant tier-one telecom deals. These included a European Mobile Virtual Network Operator (MVNO) selecting Optiva to modernize its BSS across multiple countries and markets, and a European Mobile Network Operator (MNO) choosing Optiva to power its next-generation MVNE (Mobile Virtual Network Enabler) platform.

Strategic Initiatives

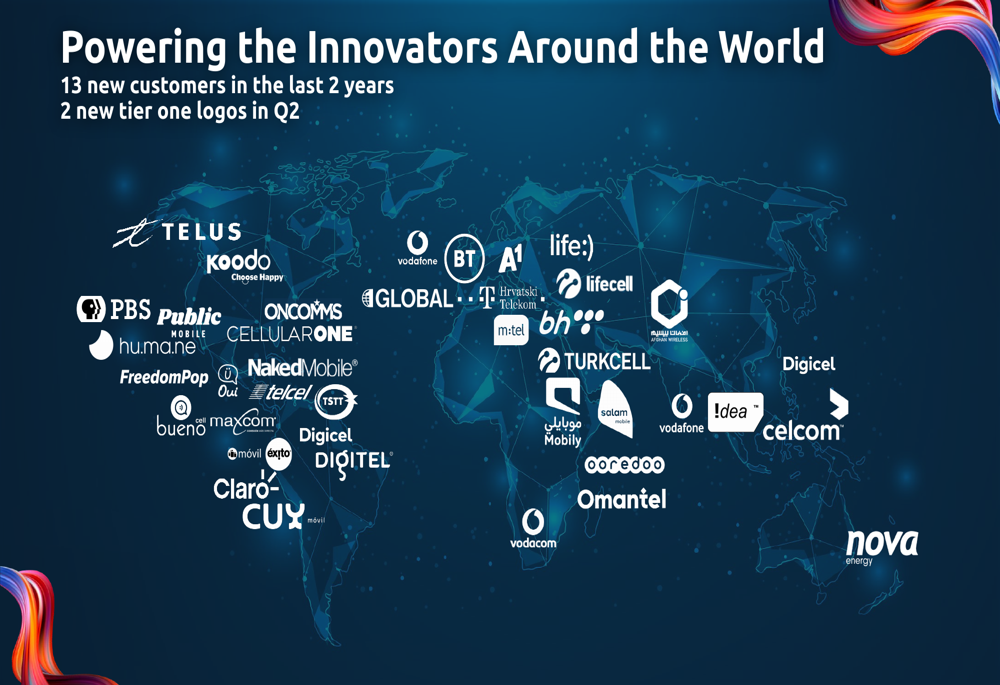

Optiva continues to position itself as a leader in telecom BSS cloudification, highlighting its progress in moving customers to cloud-based solutions. The company’s presentation emphasized its global reach and growing customer base.

The company’s global presence and customer acquisition momentum is illustrated in this world map:

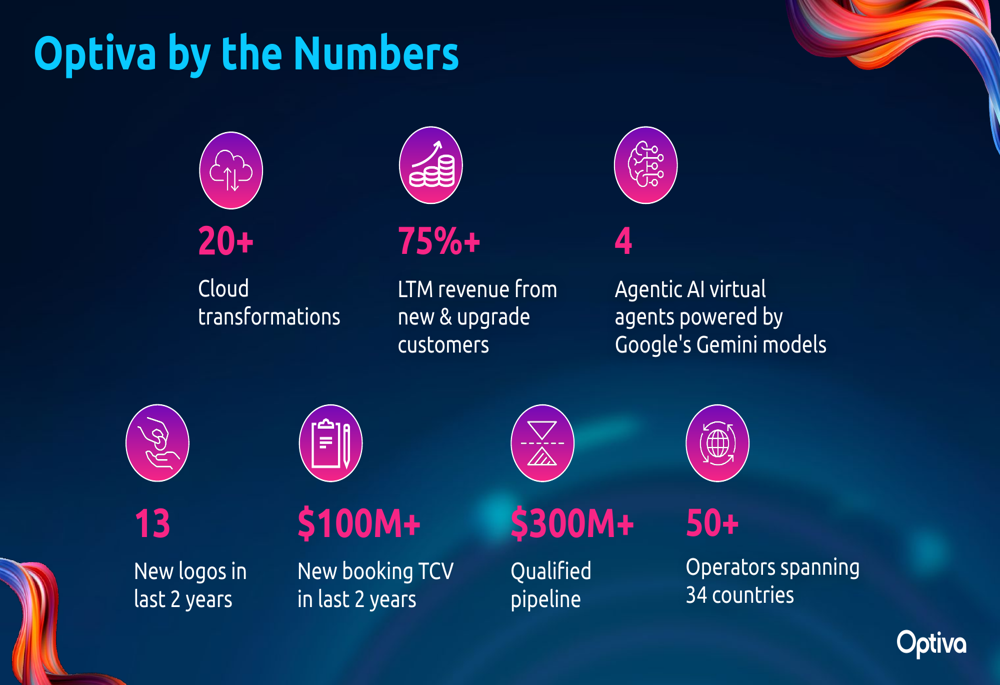

Optiva has made significant strides in its business development efforts over the past two years, as demonstrated by these key metrics:

A major strategic focus for Optiva is its investment in artificial intelligence capabilities. The company introduced Optiva GenAI Agents powered by Google Gemini models, designed to enhance customer experience and operational efficiency for telecom operators.

The following image details Optiva’s AI agents and their capabilities:

Detailed Financial Analysis

A closer examination of Optiva’s financial statements reveals ongoing challenges. While the company highlights new bookings and a qualified pipeline exceeding $300 million, current financial performance shows revenue has declined from $11.09 million in Q2 2023 to $10.3 million in Q2 2025.

The balance sheet indicates $12.9 million in cash as of Q2 2025, but also shows substantial debt in the form of debentures totaling $108.49 million. This debt burden, combined with negative EBITDA, presents significant financial challenges that the company will need to address.

The gross margin percentage has decreased from the 61-65% range in previous periods to 49% in the most recent quarter, suggesting potential pricing pressures or changes in the company’s cost structure.

Forward-Looking Statements

Optiva’s vision for its customers centers around digital transformation, agility, and new monetization models. The company is positioning itself as a partner for telecom operators looking to modernize their BSS infrastructure and capitalize on emerging opportunities.

The company’s strategic vision is outlined in this slide:

Management remains optimistic about Optiva’s pipeline and market position, highlighting its focus on the MVNO market segment and cloud-based solutions. The company has received several industry recognitions, including awards for AI & Analytics Excellence and MVNO solutions, which validate its technological direction.

Despite the current financial challenges, Optiva’s presentation emphasized its technological innovation and customer wins as foundations for future growth. However, investors will likely need to see improvement in core financial metrics before the stock recovers from its current levels near 52-week lows.

The company’s ability to convert its $300+ million qualified pipeline into revenue while improving profitability will be crucial for its long-term success in the competitive telecom BSS market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.