Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

OR Royalties Inc. (NYSE:OR) released its second quarter 2025 results on August 6, showing substantial revenue and earnings growth despite relatively flat gold equivalent ounce (GEO) production. The company’s shares responded positively, trading up 2.24% to $30.15 in premarket trading, building on recent momentum that has seen the stock approach its 52-week high of $29.50.

The royalty and streaming company benefited significantly from higher gold prices during the quarter, which helped drive financial outperformance even as production volumes remained stable year-over-year. This dynamic highlights the leverage that royalty companies provide to precious metals prices without the operational costs and risks faced by miners.

Quarterly Performance Highlights

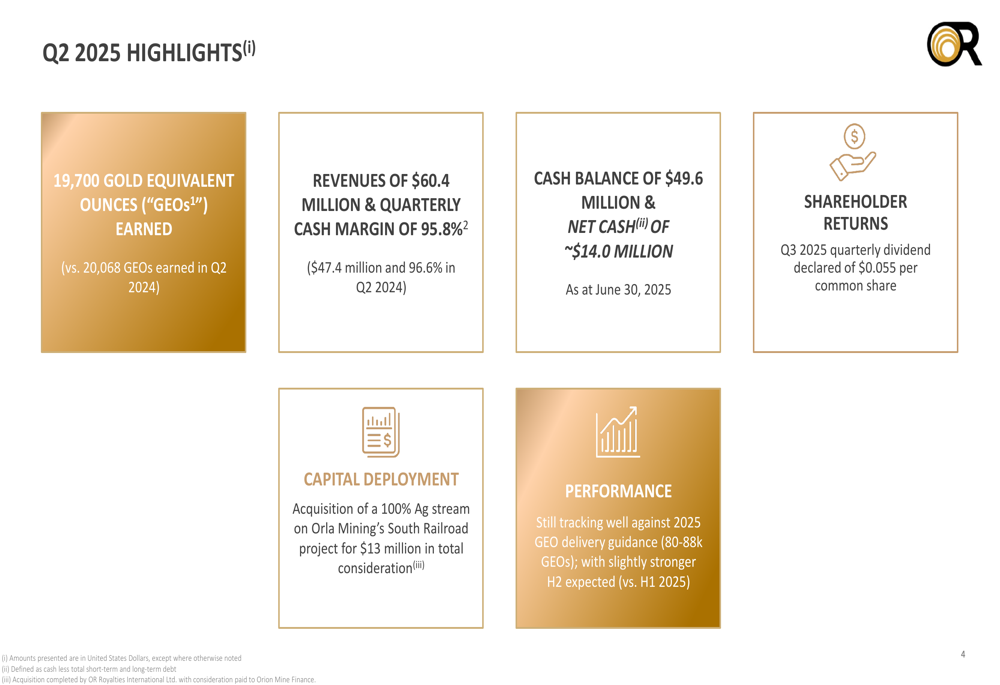

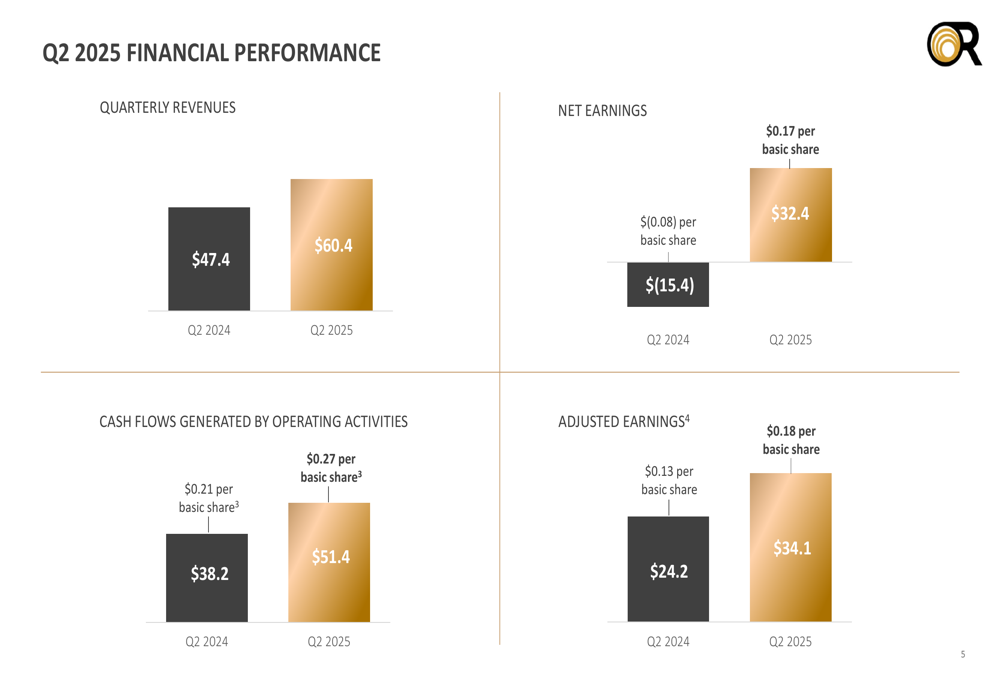

OR Royalties reported earning 19,700 gold equivalent ounces in Q2 2025, a slight decrease from 20,068 GEOs in the same period last year. However, revenues jumped 27.4% to $60.4 million, compared to $47.4 million in Q2 2024, primarily driven by higher realized gold prices.

As shown in the following quarterly highlights:

The company maintained an impressive cash margin of 95.8% during the quarter, only slightly below the 96.6% achieved in Q2 2024. Net earnings showed a dramatic improvement, reaching $32.4 million ($0.17 per share) compared to a net loss of $15.4 million (-$0.08 per share) in the prior-year period.

Cash flows from operations also showed strong growth, increasing to $51.4 million ($0.27 per share) from $38.2 million ($0.21 per share) in Q2 2024, representing a 34.6% increase. Adjusted earnings rose 41% to $34.1 million ($0.18 per share) from $24.2 million ($0.13 per share).

Detailed Financial Analysis

The company’s financial performance benefited substantially from higher realized gold prices, which averaged $3,284 per ounce in Q2 2025 compared to $2,346 in Q2 2024 – a 40% increase. This price appreciation more than offset the slight decline in production volumes.

The breakdown of Q2 2025 financial results compared to Q2 2024 shows the significant improvement across all key metrics:

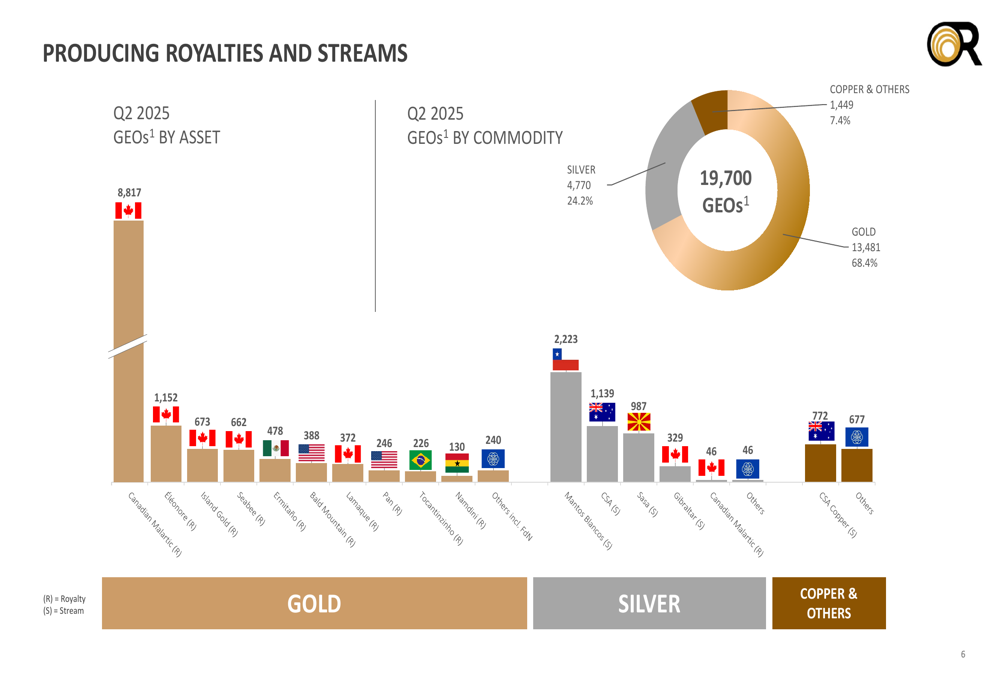

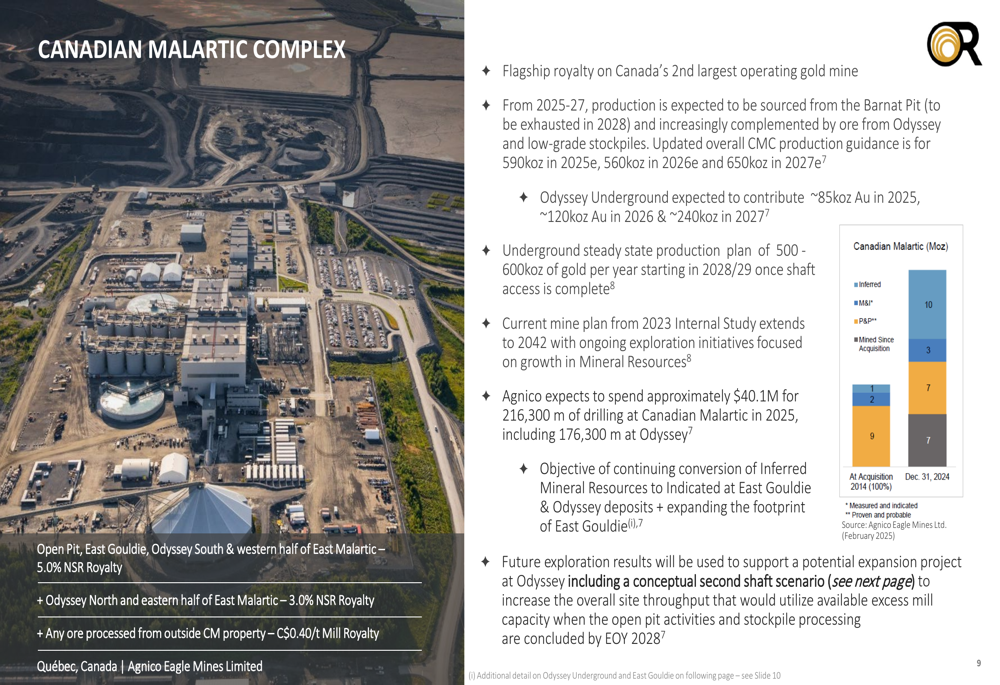

OR Royalties’ portfolio continues to be dominated by its Canadian Malartic royalty, which contributed 8,817 GEOs (44.8% of total) during the quarter. Other significant contributors included Gibraltar (2,223 GEOs), CSA (1,139 GEOs), and Mantos Blancos (987 GEOs).

By commodity, gold remained the primary driver, accounting for 13,481 GEOs (68.4%), followed by silver at 4,770 GEOs (24.2%) and copper and other metals at 1,449 GEOs (7.4%):

Competitive Industry Position

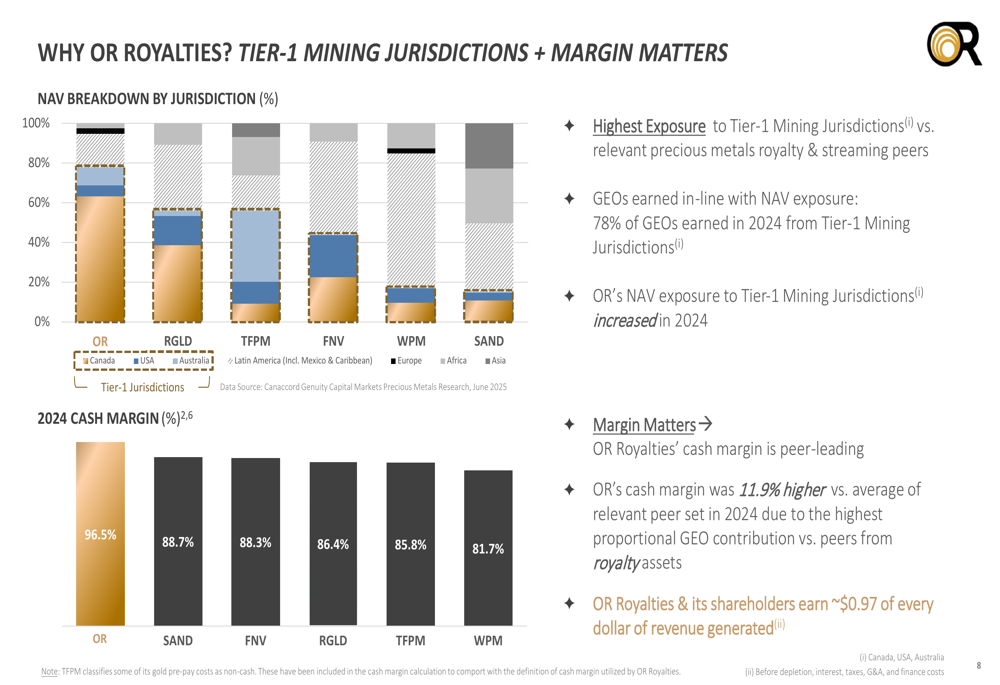

OR Royalties continues to differentiate itself within the royalty and streaming sector through its focus on Tier-1 mining jurisdictions and industry-leading cash margins. The company highlighted that 78% of GEOs earned in 2024 came from Tier-1 mining jurisdictions, providing lower geopolitical risk compared to some peers.

The company’s cash margin of 96.5% in 2024 was significantly higher than its closest competitors, with the next highest being SAND at 88.7%, followed by FNV at 88.3%. This means OR Royalties and its shareholders earn approximately $0.97 of every dollar of revenue generated:

The company’s portfolio remains heavily weighted toward precious metals, with 94.3% of H1 2025 GEOs coming from gold and silver. This focus, combined with exposure to low-cost mines (84% of NPV from first cash cost quartile), positions OR Royalties as a high-quality precious metals investment vehicle.

Growth Outlook & Strategic Initiatives

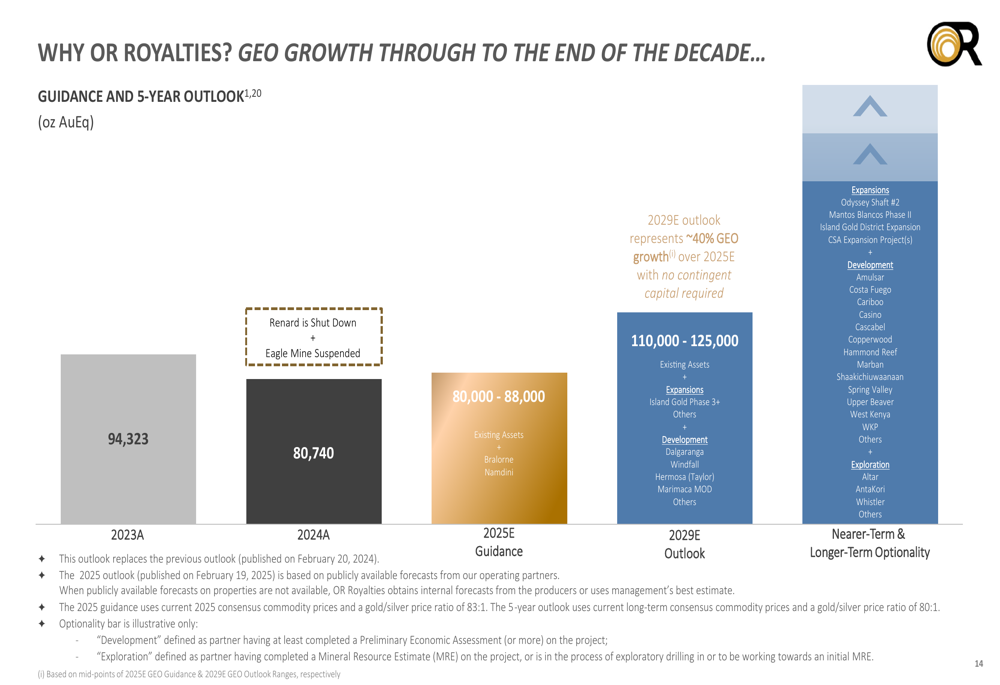

OR Royalties reaffirmed its 2025 guidance of 80,000-88,000 GEOs, noting that performance is tracking well with a slightly stronger second half expected. More significantly, the company outlined its 5-year outlook, projecting GEO production to reach 110,000-125,000 by 2029, representing approximately 40% growth from current levels:

This growth is expected to come from existing assets, expansions (particularly at Island Gold Phase 3+), and development projects including Dalgaranga, Windfall, Hermosa (Taylor), and Marimaca MOD. Additionally, the company highlighted several high-quality development assets not included in the 5-year outlook that could provide further upside, including Spring Valley, Cariboo, Upper Beaver, and others.

During the quarter, OR Royalties acquired a 100% silver stream on Orla Mining’s South Railroad project for $13 million, adding to its growth pipeline. The company also noted that its flagship Canadian Malartic Complex continues to advance, with the Odyssey Underground expected to contribute approximately 85,000 ounces of gold in 2025, growing to 240,000 ounces by 2027:

Balance Sheet & Investment Potential

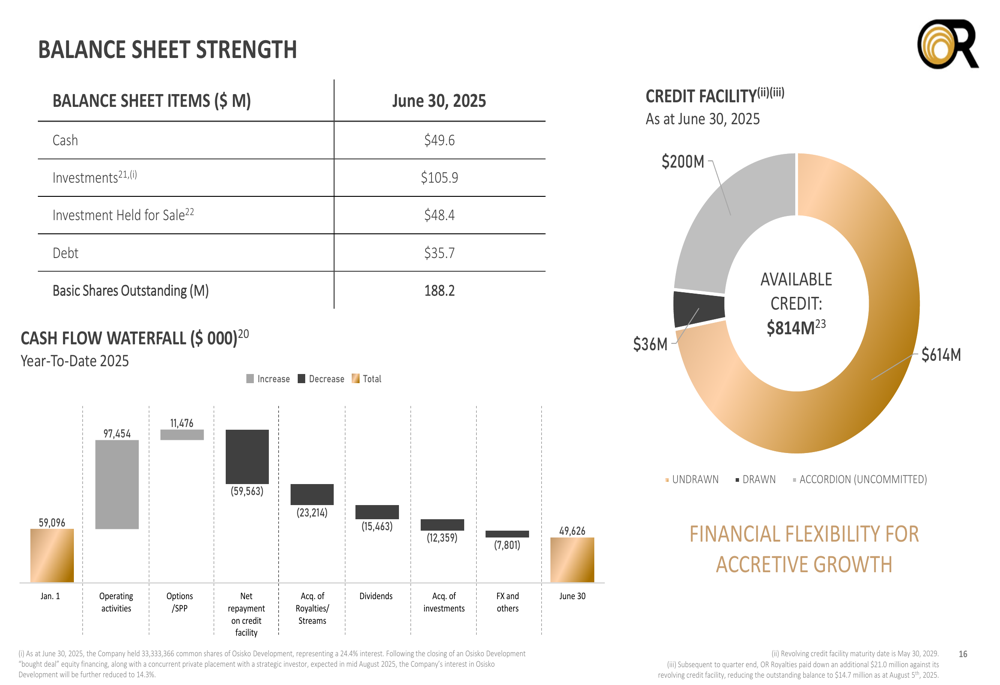

OR Royalties maintains a strong financial position with $49.6 million in cash, $105.9 million in investments, and $48.4 million in investments held for sale as of June 30, 2025. With debt of only $35.7 million and $814 million in available credit, the company has substantial financial flexibility for future acquisitions and investments:

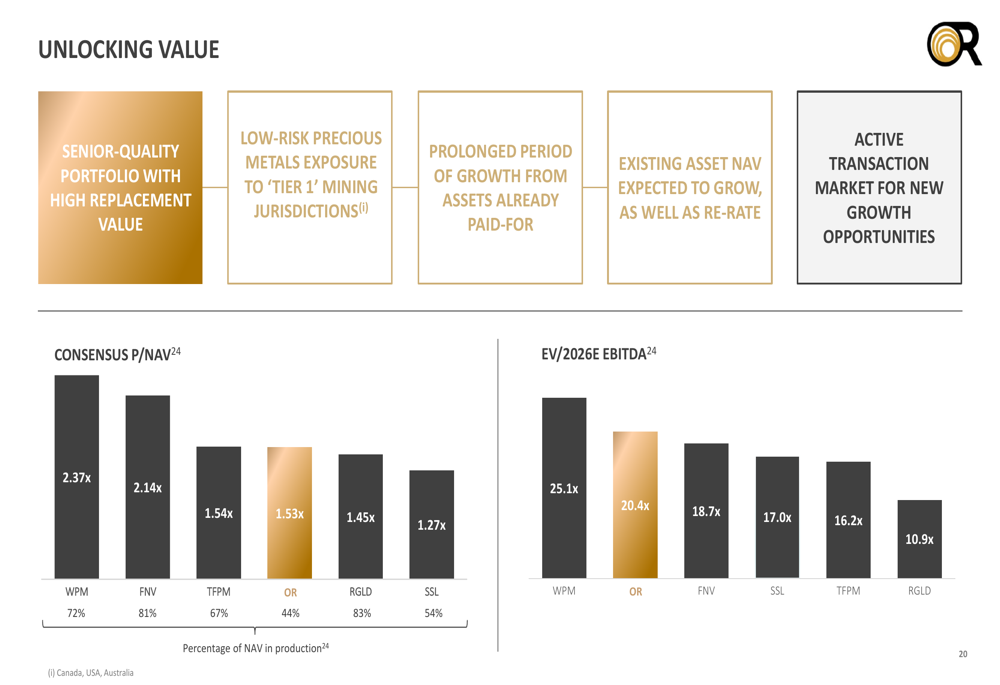

The company declared a Q3 2025 quarterly dividend of $0.055 per common share, continuing its commitment to shareholder returns. Management highlighted that OR Royalties trades at a discount to some of its peers on both P/NAV and EV/EBITDA metrics, suggesting potential for valuation expansion:

Looking ahead, OR Royalties identified several near-term catalysts across its portfolio, including the Island Gold District Expansion Study (late 2025), Windfall Updated Feasibility Study (H2 2025), and Marimaca MOD Definitive Feasibility Study (Q3 2025), which could drive further value creation and growth.

The company’s strong financial performance, industry-leading margins, and clear growth trajectory position it well to continue delivering value to shareholders in the coming years, particularly in an environment of elevated precious metals prices.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.