European shares fall: Trump threatens ’massive’ tariff increase on China

Introduction & Market Context

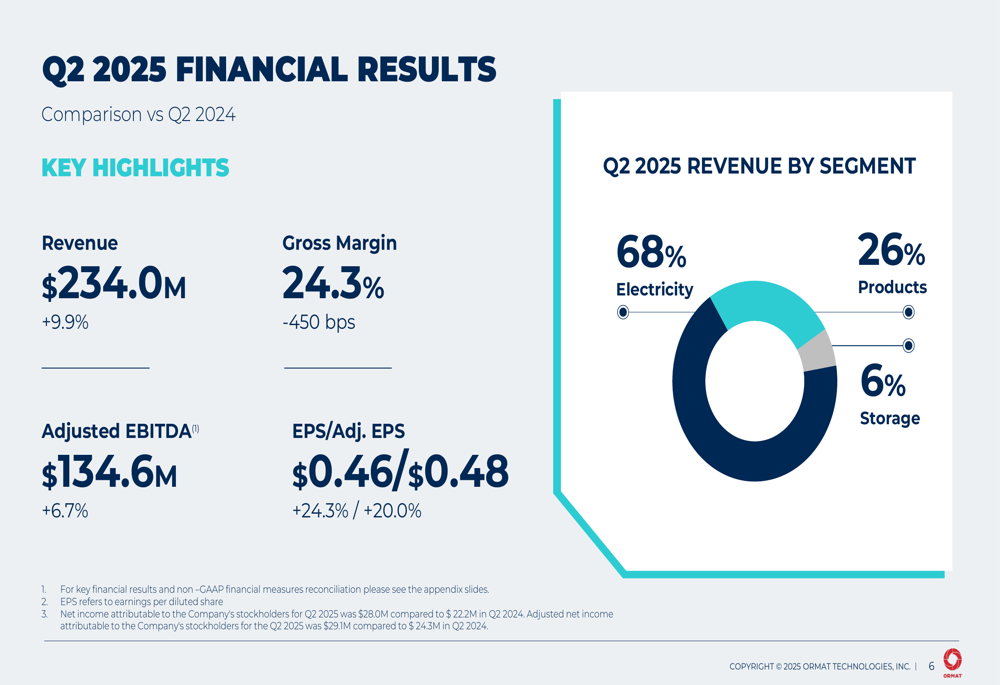

Ormat Technologies Inc (NYSE:ORA) reported strong second-quarter 2025 results on August 7, with revenue increasing by 9.9% year-over-year to $234.0 million, driven primarily by significant growth in its Products and Energy Storage segments. The renewable energy company’s stock closed at $85.20, up 1.83% following the earnings release, continuing its recovery from the 52-week low of $61.58.

The company’s performance builds on its Q1 momentum, when it exceeded analyst expectations with an EPS of $0.66. For Q2 2025, Ormat reported earnings per share of $0.46, representing a 24.3% increase compared to the same period last year, as the company continues to benefit from favorable regulatory conditions and growing demand for renewable energy solutions.

Quarterly Performance Highlights

Ormat’s Q2 2025 financial results showed strong overall performance with revenue reaching $234.0 million, a 9.9% increase year-over-year. Adjusted EBITDA grew by 6.7% to $134.6 million, while earnings per share jumped 24.3% to $0.46. However, gross margin declined by 450 basis points to 24.3%.

As shown in the following financial results summary:

The company’s revenue mix for Q2 2025 shows the Electricity segment accounting for 68% of total revenue, followed by Products at 26% and Storage at 6%. This represents a shift from previous quarters as the Products and Storage segments continue to grow their contribution to overall revenue.

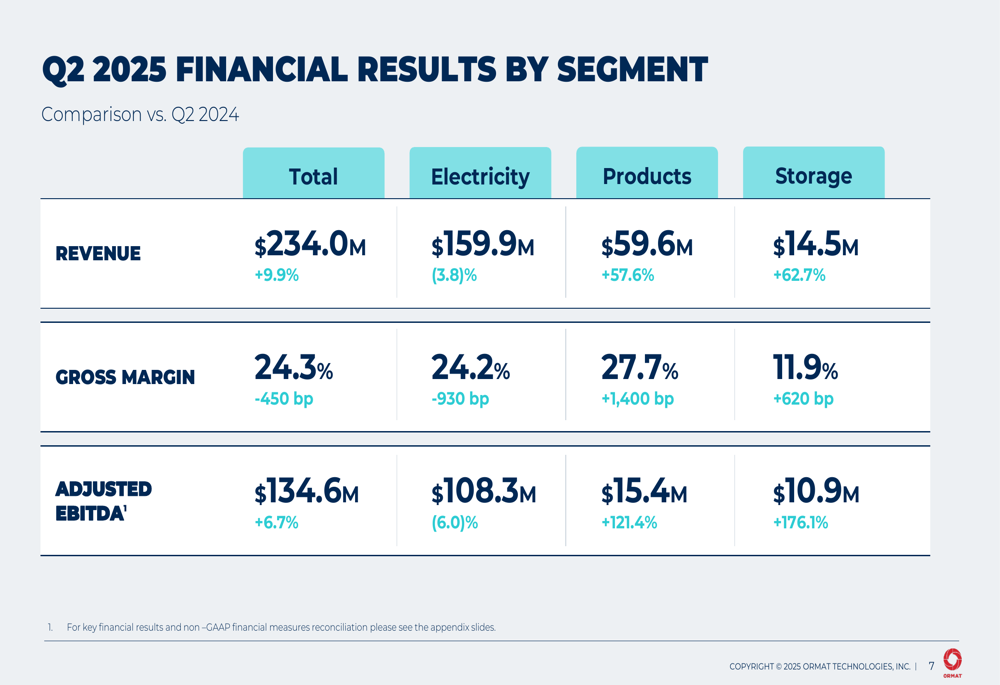

A detailed breakdown of performance by segment reveals contrasting trends:

The Products segment showed exceptional growth with revenue increasing by 57.6% to $59.6 million and adjusted EBITDA more than doubling with a 121.4% increase to $15.4 million. Similarly, the Storage segment demonstrated impressive growth with revenue up 62.7% to $14.5 million and adjusted EBITDA surging by 176.1% to $10.9 million. However, the Electricity segment, which remains the company’s largest revenue contributor, experienced a 3.8% decline in revenue to $159.9 million and a 6.0% decrease in adjusted EBITDA to $108.3 million.

Segment Analysis

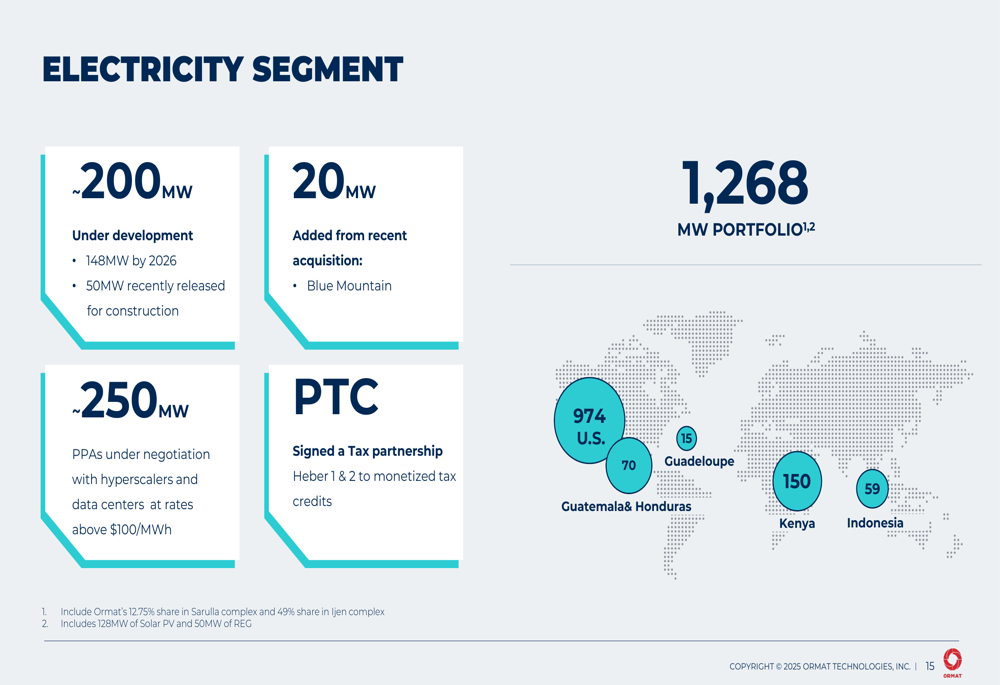

Electricity Segment

Despite the revenue decline in the Electricity segment, Ormat continues to expand its geothermal portfolio, which now totals 1,268 MW across multiple countries. The company completed the acquisition of the 20MW Blue Mountain Geothermal Power Plant for $88 million, with revenue and EBITDA contributions expected to begin in Q3 2025.

The company’s electricity generation capacity and development pipeline is illustrated here:

Ormat noted that the revenue decline in the Electricity segment was primarily due to injection limitations at its Puna, Hawaii plant caused by permitting delays and well field maintenance, as well as curtailment issues related to maintenance work on NV Energy’s transmission line. The company expects these issues to lessen in the second half of 2025.

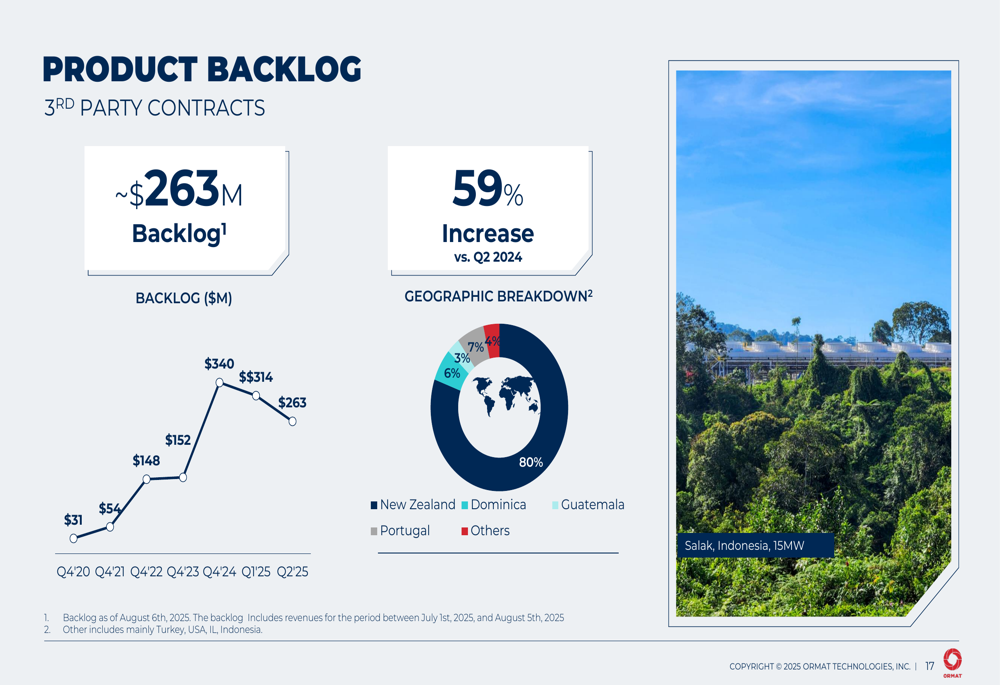

Products Segment

The Products segment showed robust growth, with backlog reaching approximately $263 million as of August 6, 2025, representing a 59% increase compared to Q2 2024. The geographic breakdown of the backlog shows significant concentration in New Zealand (80%), with smaller portions in Dominica, Portugal, Guatemala, and other locations.

As shown in the following product backlog chart:

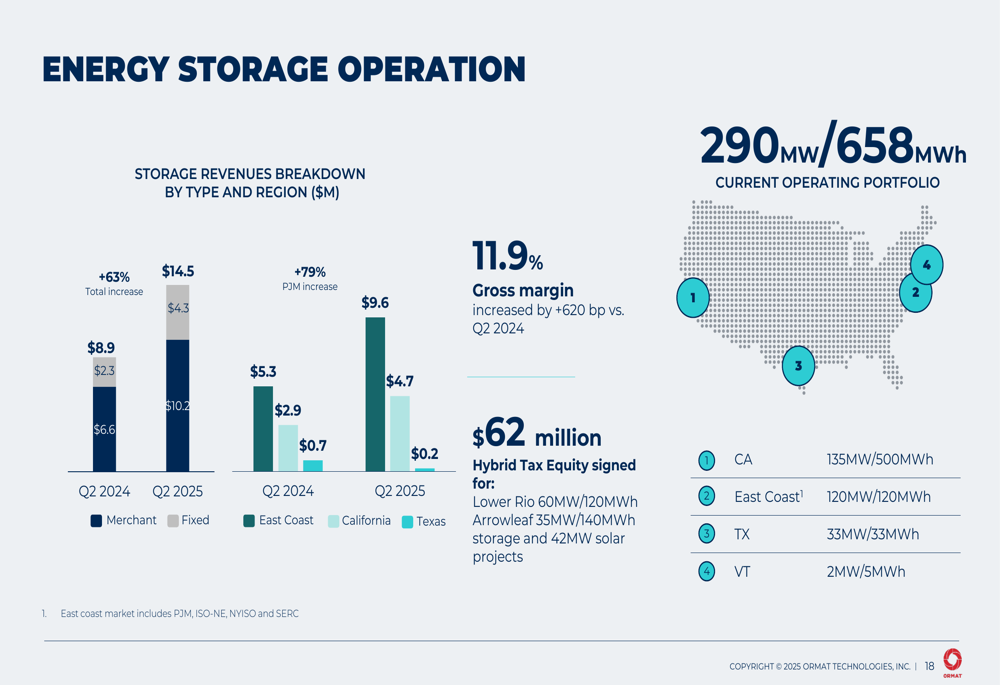

Energy Storage Segment

The Energy Storage segment continues to be Ormat’s fastest-growing business, with revenues increasing by 63% compared to Q2 2024. The company currently operates a portfolio of 290MW/658MWh of energy storage assets, primarily located in California, the East Coast, Texas, and Vermont.

The company’s energy storage operations and revenue growth are illustrated here:

Strategic Growth Initiatives

Ormat outlined an ambitious growth plan targeting 15-17% CAGR for capacity, 8-9% CAGR for revenue, and 9-11% CAGR for adjusted EBITDA from 2024 to 2028. The company aims to increase its capacity from 1.5 GW in 2024 to 2.6-2.8 GW by 2028, while growing revenue from $880 million to $1,200-1,250 million during the same period.

The company’s growth trajectory is illustrated in this chart:

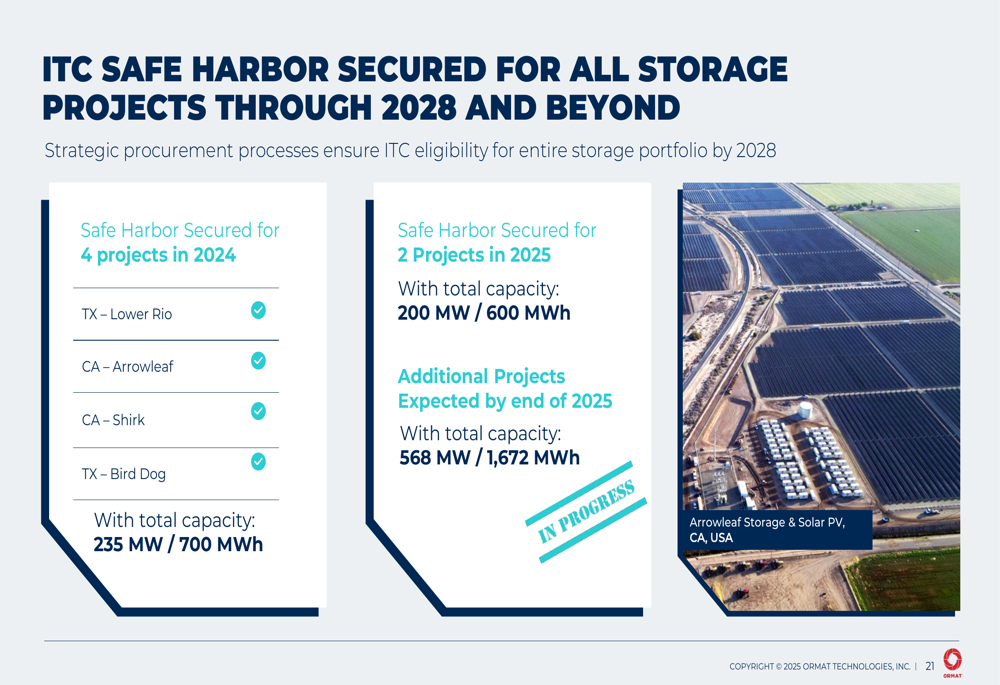

A key component of Ormat’s growth strategy is securing Investment Tax Credit ( ITC (NSE:ITC)) safe harbor for all its storage projects through 2028 and beyond. The company has already secured safe harbor for projects with a total capacity of 235 MW/700 MWh in 2024 and 200 MW/600 MWh in 2025, with additional projects expected by the end of 2025.

The details of the ITC safe harbor strategy are shown here:

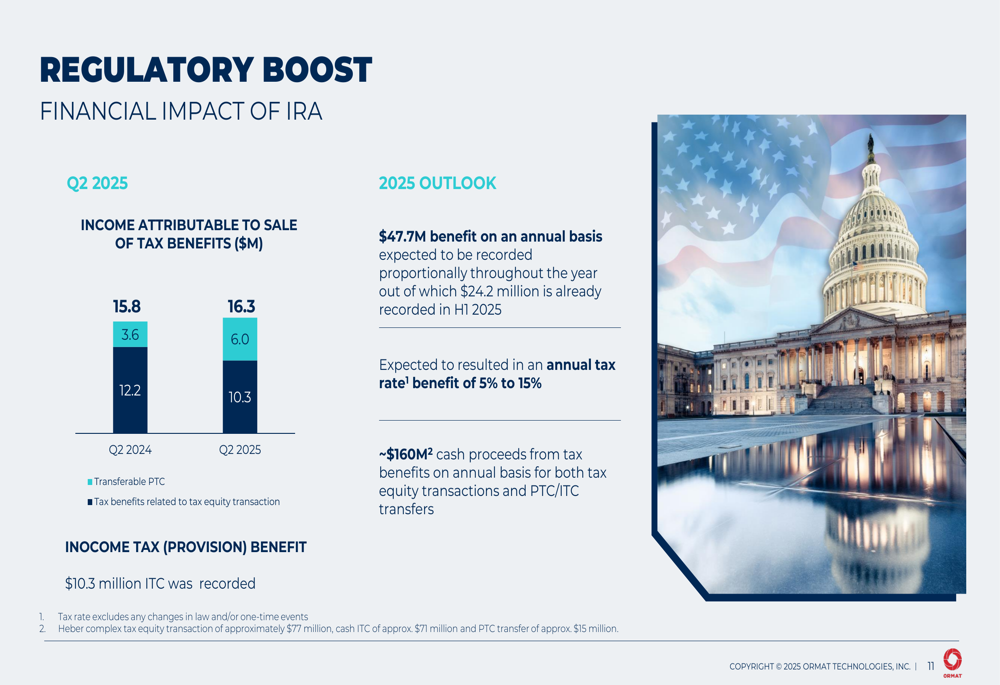

Regulatory Environment and Financial Impact

Ormat continues to benefit significantly from the Inflation Reduction Act (IRA), with expected annual tax benefits of $47.7 million. The company recorded $24.2 million of these benefits in H1 2025 and anticipates an annual tax rate benefit of 5% to 15%. Additionally, Ormat expects approximately $160 million in annual cash proceeds from tax benefits through both tax equity transactions and PTC/ITC transfers.

The financial impact of the IRA is illustrated in this chart:

The recently passed "One Big Beautiful Bill" extends the timeline for renewable energy tax incentives, providing 100% tax credits for geothermal and storage projects that begin construction by December 31, 2033. This represents a significant extension from previous deadlines and provides Ormat with long-term visibility for project development.

Outlook & Guidance

Ormat maintained its 2025 guidance, projecting revenue between $935-975 million (representing approximately 9% year-over-year growth) and adjusted EBITDA between $563-593 million. For the long term, the company targets revenue of $1,200-1,250 million and adjusted EBITDA of $775-825 million by 2028.

The company highlighted several accomplishments in Q2 2025 that position it well for future growth:

Ormat’s strong capital position, with total liquidity of $551 million and H1 2025 cash from operations of $185 million, provides the financial flexibility to execute its growth strategy. However, the company’s net debt of $2.5 billion and net debt to adjusted EBITDA ratio of 4.4x suggest careful management of leverage will be important as it pursues its ambitious expansion plans.

The company is also negotiating approximately 250MW of power purchase agreements (PPAs) with hyperscalers and data centers at rates above $100/MWh, which would represent a significant premium to historical rates and could drive improved profitability in the coming years.

CEO Doron Bouchard, as noted in the Q1 earnings call, remains "committed to achieving our growth trajectory of 2.6 to 2.8 gigawatts of generating capacity by the end of 2028," a target that appears to be supported by the company’s current project pipeline and regulatory environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.