Xia Yu, director at Summit Therapeutics, buys $9.9 million in shares

Introduction & Market Context

Orrön Energy (STO:ORRON) presented its Q2 2025 results on August 6, 2025, revealing continued challenges in the renewable energy market. The company’s stock fell 6.1% following the presentation, closing at 4.62 SEK, as investors reacted to the negative EBITDA figures and ongoing market pressures. The stock is currently trading significantly below its 52-week high of 10.7 SEK, reflecting persistent headwinds in the renewable energy sector.

The presentation, delivered by CEO Daniel Fitzgerald and CFO Espen Hennie, highlighted Orrön’s efforts to navigate a complex market environment characterized by price volatility and increasing balancing costs, while advancing its strategic initiatives in project development.

As shown in the following overview of the company’s positioning and assets:

Quarterly Performance Highlights

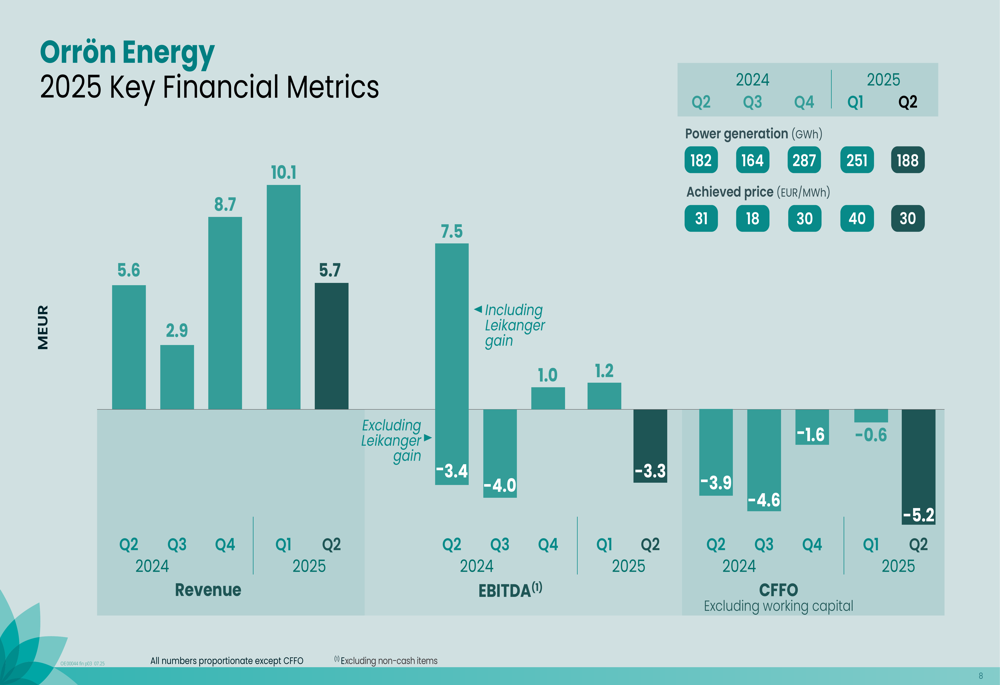

Orrön Energy reported power generation of 188 GWh for Q2 2025, slightly higher than the 182 GWh recorded in Q2 2024. However, financial results were less encouraging, with revenue of 6 MEUR and an EBITDA of -3 MEUR for the quarter. The achieved power price was 30 EUR/MWh, matching Q4 2024 levels but down from the 40 EUR/MWh achieved in Q1 2025.

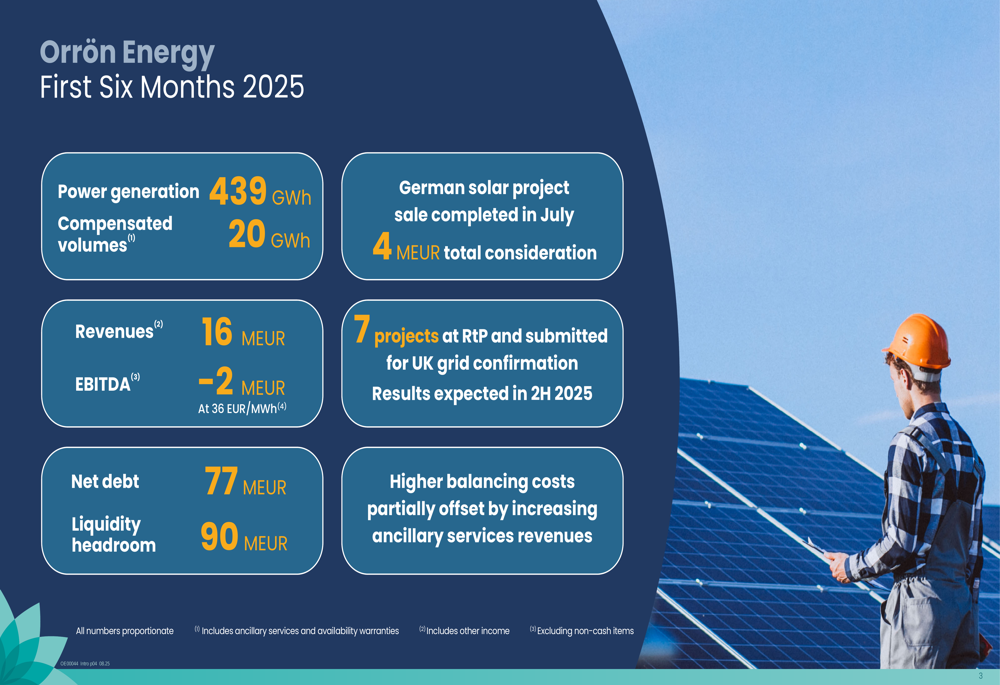

For the first half of 2025, the company generated 439 GWh of power (including 20 GWh of compensated volumes), resulting in revenues of 16 MEUR and an EBITDA of -2 MEUR at an average achieved price of 36 EUR/MWh.

The following slide summarizes the company’s first six months performance for 2025:

The company’s power generation has remained relatively stable over recent periods, though slightly down from the 460 GWh recorded in H1 2024. Management projects total 2025 production to range between 900-1,050 GWh, which represents a slight downward adjustment from previous guidance.

The quarterly financial metrics reveal the challenges the company is facing:

Detailed Financial Analysis

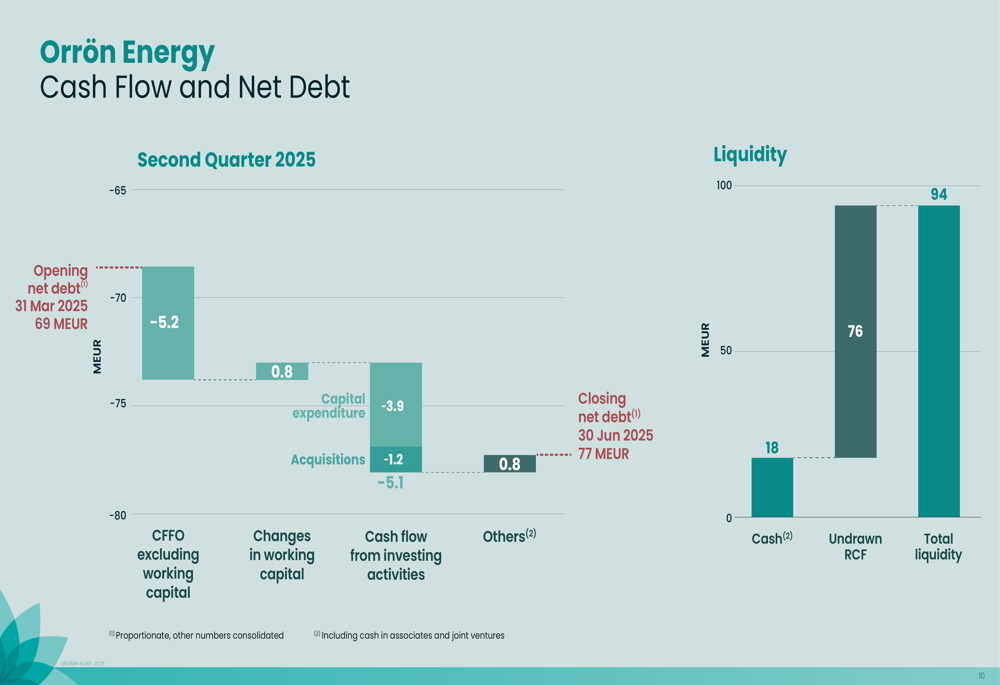

Orrön Energy’s financial position shows increasing pressure, with net debt rising to 77 MEUR by the end of Q2 2025, up from 69 MEUR at the beginning of the quarter. This increase was primarily driven by negative cash flow from operations (-5.2 MEUR excluding working capital) and continued capital expenditures (-3.9 MEUR).

Despite these challenges, the company maintains significant liquidity headroom of 94 MEUR, consisting of 18 MEUR in cash and 76 MEUR in undrawn revolving credit facilities.

The following cash flow and net debt analysis provides further insight into the company’s financial movements during Q2:

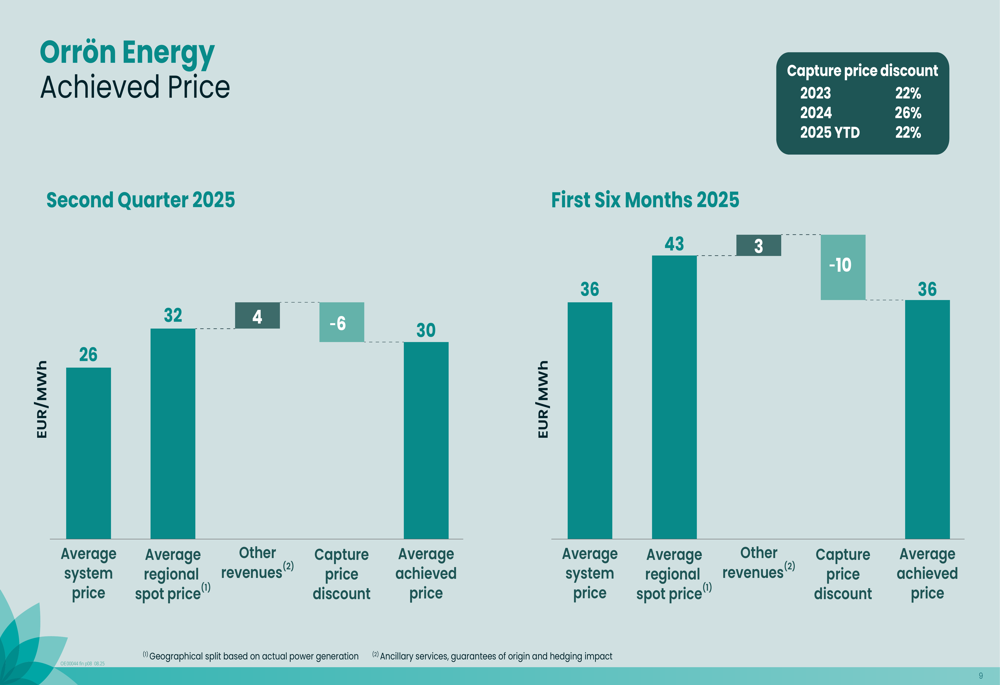

A key factor affecting Orrön’s financial performance is the achieved power price, which continues to be impacted by the capture price discount - a common challenge for renewable energy producers. For H1 2025, the capture price discount was 22%, an improvement from the 26% recorded in 2024.

The breakdown of the achieved price components shows:

The company is also experiencing higher balancing costs, which reached 3.1 MEUR in the first half of 2025, compared to 1.3 MEUR in the same period of 2024. However, this is partially offset by the emergence of ancillary services revenues, which contributed 0.8 MEUR in H1 2025 compared to zero in the previous year.

Strategic Initiatives

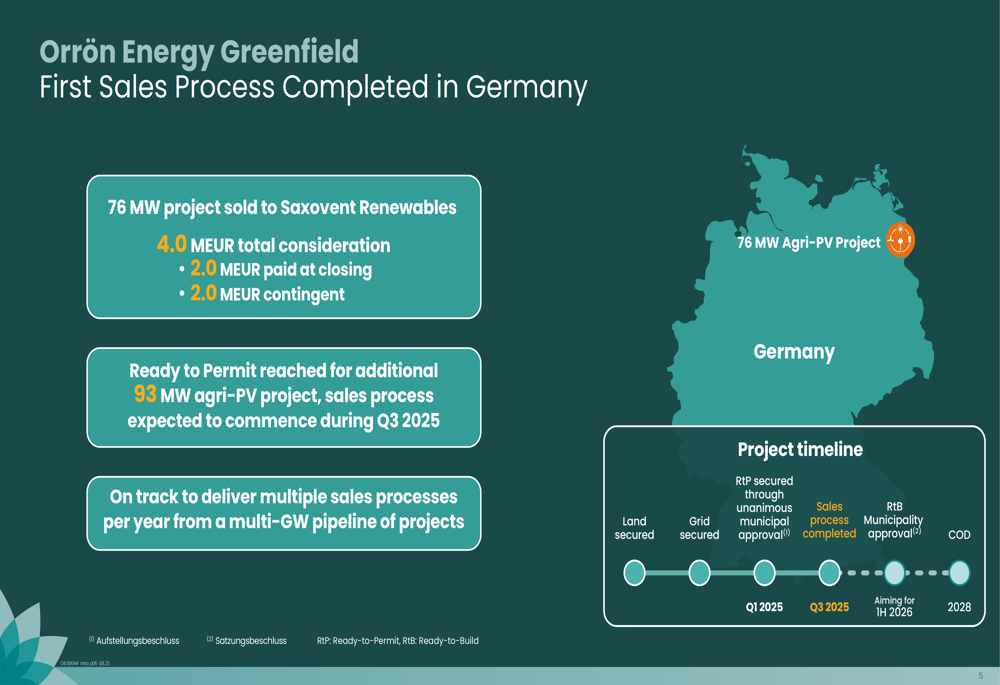

Despite financial headwinds, Orrön Energy continues to advance its strategic initiatives, particularly in project development and sales. In July, the company completed the sale of a 76 MW German solar project to Saxovent Renewables for a total consideration of 4.0 MEUR, with 2.0 MEUR paid at closing and the remainder contingent on future milestones.

The company has also reached the Ready-to-Permit stage for an additional 93 MW agri-PV project in Germany, with the sales process expected to commence in Q3 2025.

The following slide details the German project sales process:

Additionally, Orrön Energy has 7 projects at the Ready-to-Permit stage that have been submitted for UK grid confirmation, with results expected in the second half of 2025. These project development activities represent a key part of the company’s strategy to create value beyond its operating assets.

Forward-Looking Statements

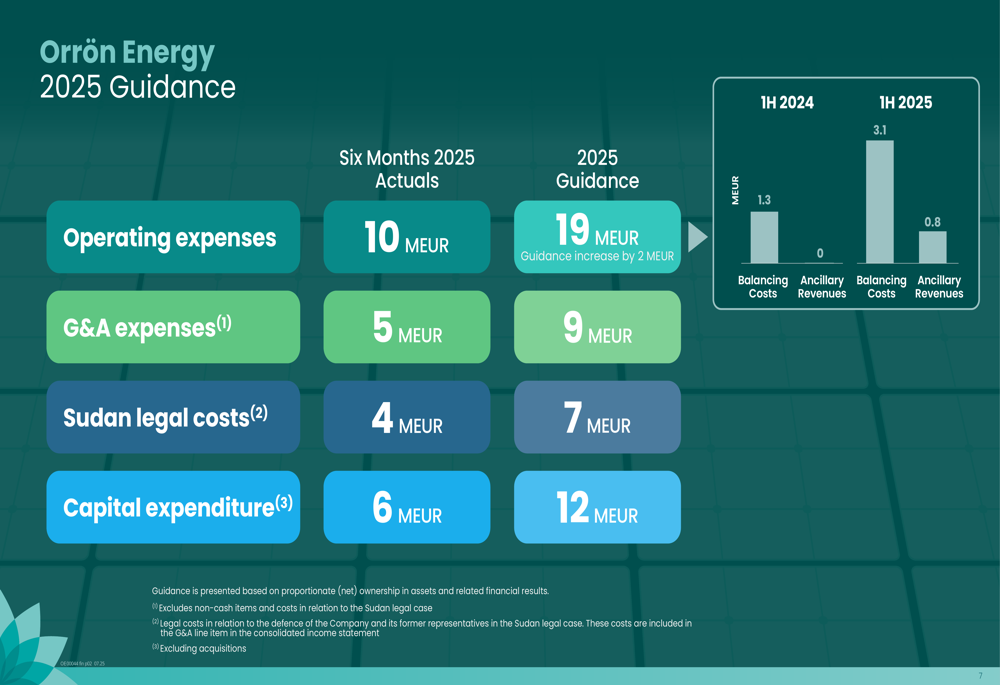

Looking ahead, Orrön Energy has updated its 2025 guidance, increasing operating expenses to 19 MEUR (up by 2 MEUR from previous guidance) while maintaining G&A expenses at 9 MEUR. The company expects Sudan legal costs to reach 7 MEUR and has set capital expenditure guidance at 12 MEUR for the year.

The updated guidance and first-half actuals are presented here:

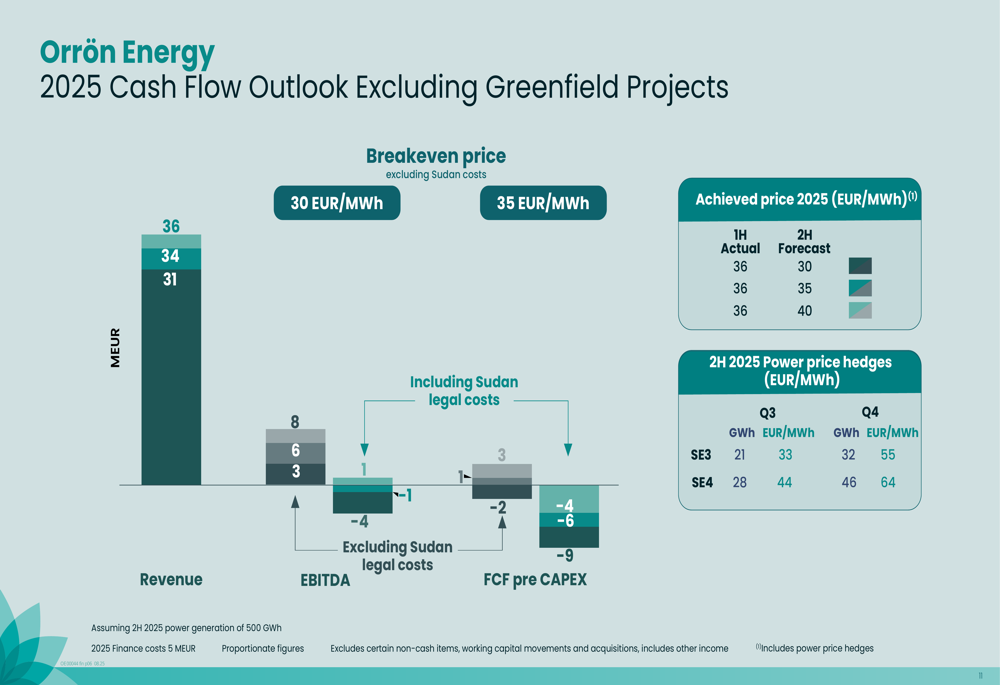

For the second half of 2025, Orrön has secured power price hedges for a portion of its production, including 21 GWh in SE3 at 33 EUR/MWh and 28 GWh in SE4 at 44 EUR/MWh. For Q3 and Q4, the company has hedged 32 GWh at 55 EUR/MWh and 46 GWh at 64 EUR/MWh respectively.

The company’s cash flow outlook indicates a breakeven price between 30-35 EUR/MWh, suggesting that current market prices are hovering around the company’s breakeven level:

With achieved prices in the first half of 2025 averaging 36 EUR/MWh and forecasts for the second half at 30 EUR/MWh, Orrön Energy faces continued margin pressure. The company will need to successfully execute its project sales and operational improvements to offset these challenges and return to positive EBITDA territory in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.