Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Owens Corning (NYSE:OC) presented its first quarter 2025 financial results on May 7, revealing a substantial 25% year-over-year revenue increase but facing margin compression compared to the same period last year. Despite highlighting "strong revenue and margin performance" in its presentation, the building materials manufacturer’s stock fell 4.04% to $142.63 during the trading session, continuing a pattern of market skepticism similar to what followed its Q4 2024 results.

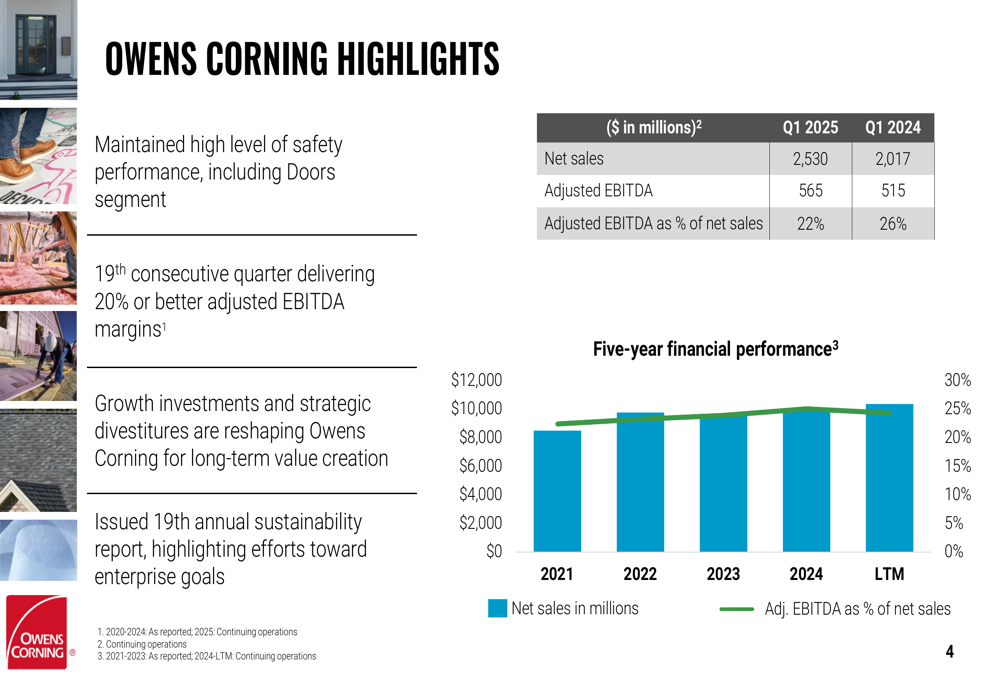

The company’s presentation emphasized its 19th consecutive quarter of delivering adjusted EBITDA margins of 20% or better, though the actual margin of 22% represented a decline from 26% in Q1 2024. This performance comes as Owens Corning continues to reshape its portfolio through strategic acquisitions and divestitures, including the integration of its relatively new Doors segment.

Quarterly Performance Highlights

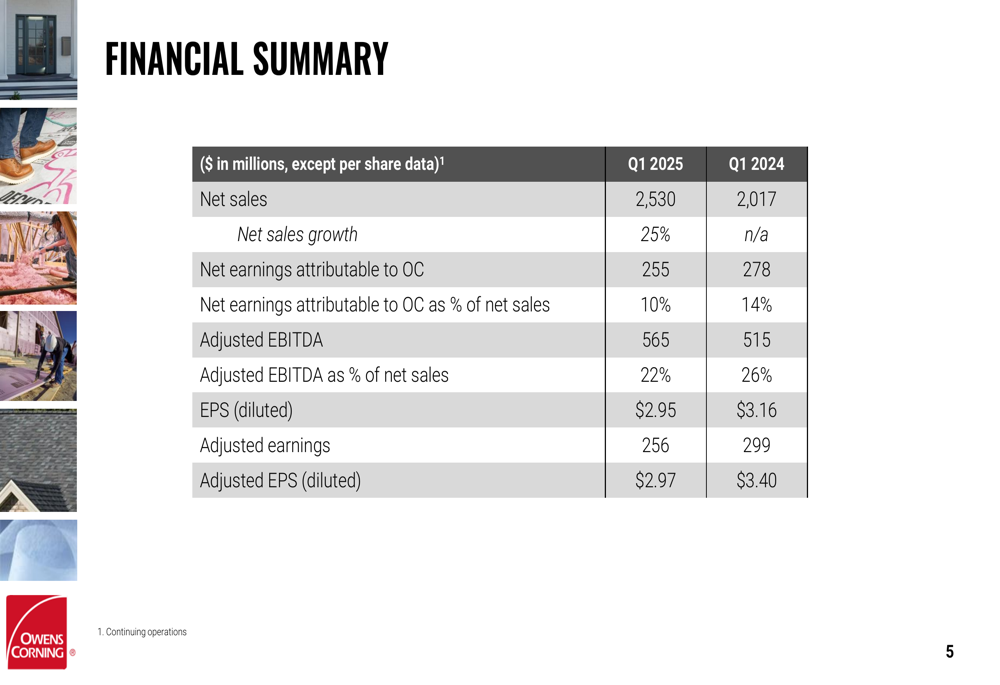

Owens Corning reported Q1 2025 net sales of $2.53 billion, a significant increase from $2.02 billion in the first quarter of 2024. However, despite the revenue growth, several profitability metrics declined year-over-year.

As shown in the company’s financial summary:

Net earnings attributable to Owens Corning fell to $255 million (10% of net sales) compared to $278 million (14% of net sales) in Q1 2024. Adjusted EBITDA increased in absolute terms to $565 million from $515 million, but as a percentage of sales declined to 22% from 26%.

Diluted earnings per share decreased to $2.95 from $3.16 in the prior year, while adjusted EPS fell more substantially to $2.97 from $3.40. The company noted that all values represent continuing operations, reflecting its ongoing portfolio transformation.

The company’s overall performance highlights were presented as follows:

From a cash flow perspective, Owens Corning reported a free cash outflow of $252 million for the quarter, though it still returned $159 million to shareholders through share repurchases and dividends. The company maintained a strong liquidity position of $1.9 billion, consisting of approximately $400 million in cash and $1.5 billion available on its bank debt facility. Capital additions for the quarter totaled $203 million, and the company reported a 16% return on capital for the trailing twelve months.

Segment Analysis

Owens Corning’s performance varied significantly across its three business segments, with Roofing continuing to deliver the strongest margins.

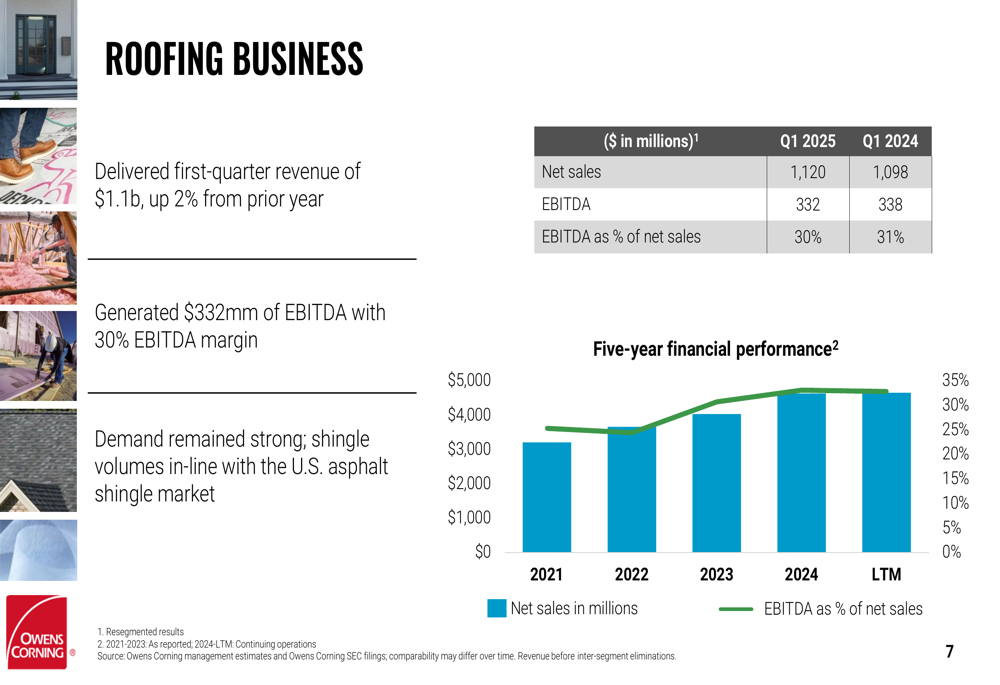

The Roofing business posted first-quarter revenue of $1.1 billion, up 2% from the prior year, with an impressive EBITDA of $332 million and a 30% EBITDA margin. The company noted that demand remained strong, with shingle volumes in line with the broader U.S. asphalt shingle market.

The segment’s five-year performance shows consistent margin strength:

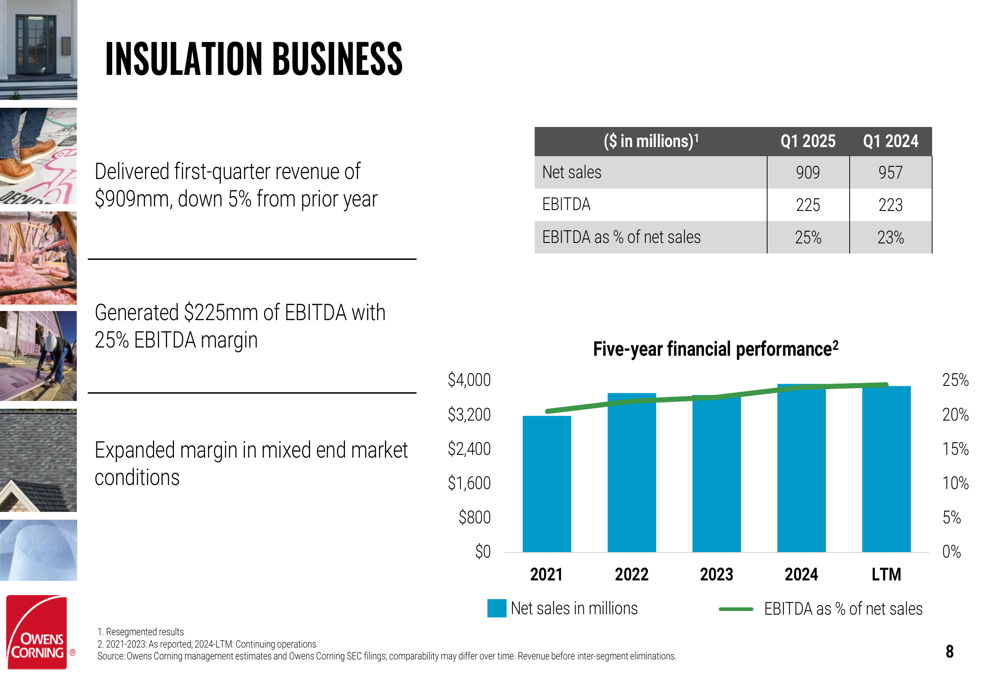

Meanwhile, the Insulation business faced more challenging conditions, with revenue of $909 million, down 5% from the prior year. Despite the revenue decline, the segment delivered EBITDA of $225 million with a 25% margin, demonstrating resilience in what the company described as "mixed end market conditions."

The Insulation segment’s five-year performance shows margin stability despite fluctuating revenues:

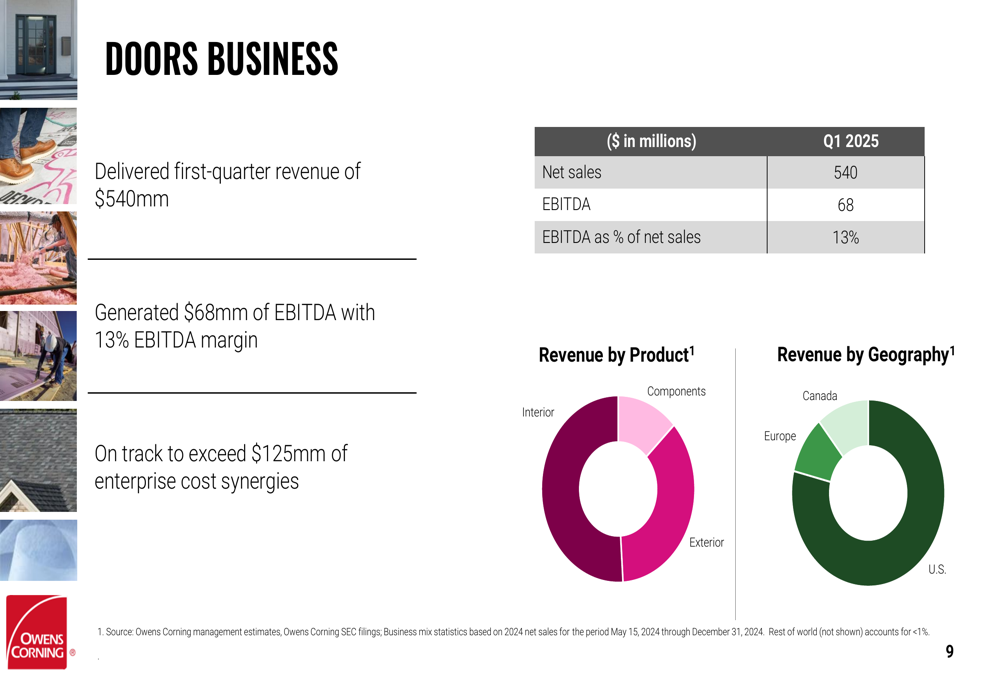

The Doors business, which represents Owens Corning’s newest segment following recent acquisitions, reported first-quarter revenue of $540 million and EBITDA of $68 million, yielding a 13% EBITDA margin. The company indicated that this business is on track to exceed $125 million of enterprise cost synergies, suggesting successful integration progress.

The Doors segment’s revenue is diversified across product types and geographies as illustrated below:

Forward-Looking Statements

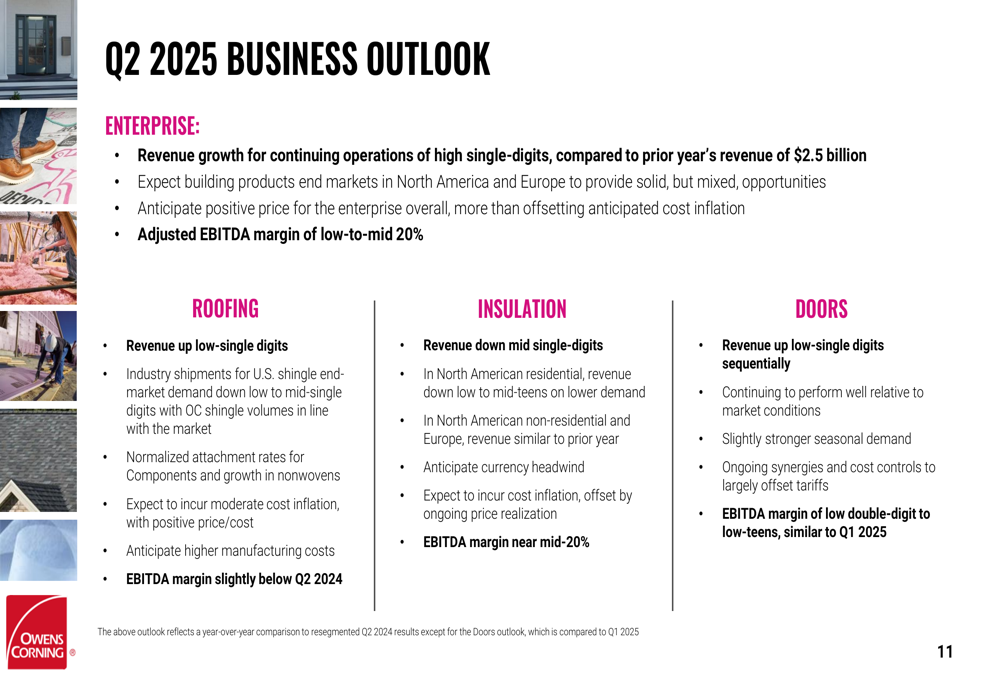

Looking ahead to the second quarter of 2025, Owens Corning provided a cautiously optimistic outlook while acknowledging mixed market conditions. The company expects enterprise revenue growth for continuing operations in the high single-digits compared to the prior year’s revenue of $2.5 billion, with an adjusted EBITDA margin in the low-to-mid 20% range.

The detailed Q2 2025 outlook by segment reveals varying expectations:

For the full year 2025, Owens Corning projects general corporate EBITDA expenses of $240-260 million, interest expense of $250-260 million, and a full-year effective tax rate of 24-26%. Capital additions are expected to be approximately $800 million, with depreciation and amortization of around $650 million.

Strategic Initiatives

Throughout the presentation, Owens Corning emphasized its ongoing strategic transformation. The company highlighted that "growth investments and strategic divestitures are reshaping Owens Corning for long-term value creation," suggesting a deliberate portfolio evolution.

The company also noted the release of its 19th annual sustainability report, underscoring its commitment to environmental and social responsibility as part of its long-term strategy. This focus on sustainability aligns with broader industry trends and increasing investor attention to ESG factors.

The integration of the Doors business appears to be a key strategic priority, with the company reporting progress on achieving synergies. This segment diversifies Owens Corning’s product portfolio and geographic exposure, potentially providing new growth avenues while balancing the more mature Roofing and Insulation businesses.

Despite the positive narrative around strategic initiatives, investors appear to be taking a more cautious view, as reflected in the stock’s decline following the presentation. This reaction may reflect concerns about margin compression, mixed market conditions, or uncertainty about the long-term benefits of the company’s portfolio transformation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.