Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

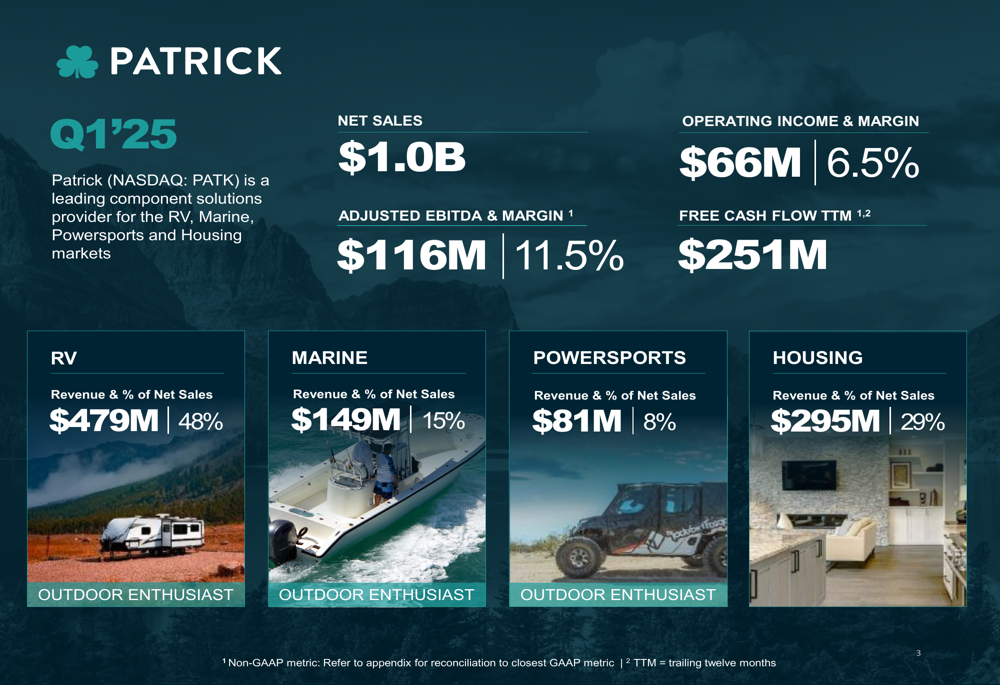

Patrick Industries , Inc. (NASDAQ:PATK) reported continued revenue growth and strategic diversification progress in its Q1 2025 earnings presentation delivered on May 1, 2025. The company achieved 7% year-over-year revenue growth to $1.0 billion, driven primarily by strength in its RV and Housing segments, while maintaining solid profitability despite challenges in its Marine and Powersports divisions.

Quarterly Performance Highlights

Patrick Industries reported net sales of $1.0 billion for Q1 2025, representing a 7% increase compared to $933 million in Q1 2024. Adjusted EBITDA reached $116 million with an 11.5% margin, while operating income came in at $66 million with a 6.5% margin. The company’s gross margin improved to 22.8% from 21.9% in the prior-year period.

"Our strategic diversification journey continues to yield positive results, with strong performance in our RV and Housing segments offsetting challenges in Marine and Powersports," the company noted in its presentation.

As shown in the following financial highlights chart, Patrick’s revenue is well-diversified across four key segments, with RV representing 48%, Housing 29%, Marine 15%, and Powersports 8% of Q1 net sales:

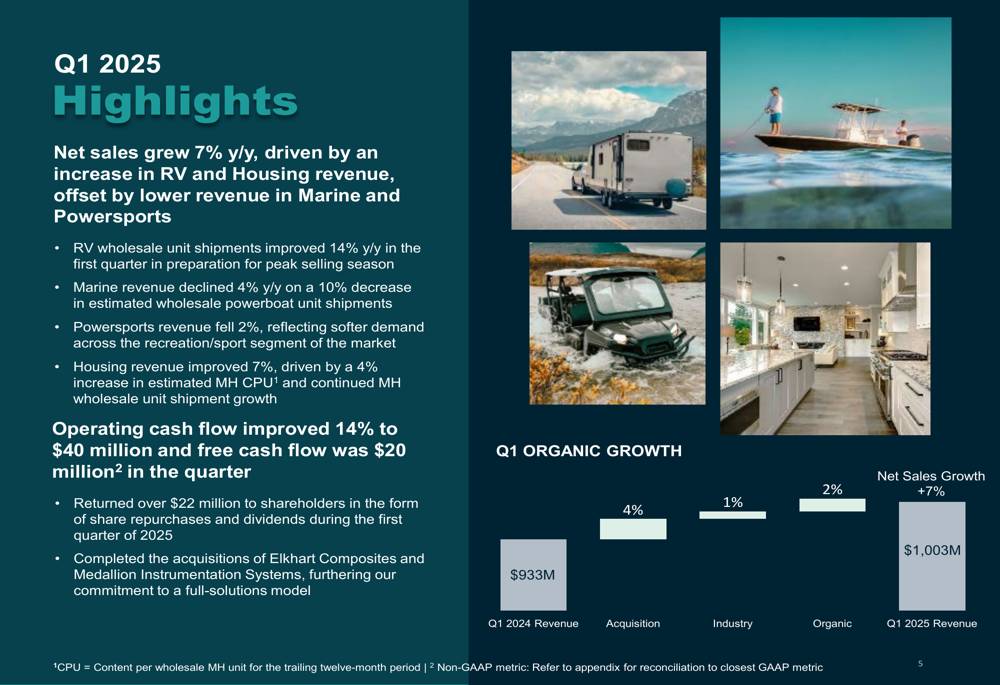

The company’s Q1 2025 organic growth analysis reveals that acquisitions contributed 4% to the overall 7% revenue growth, while industry growth added 1% and organic initiatives contributed 2%:

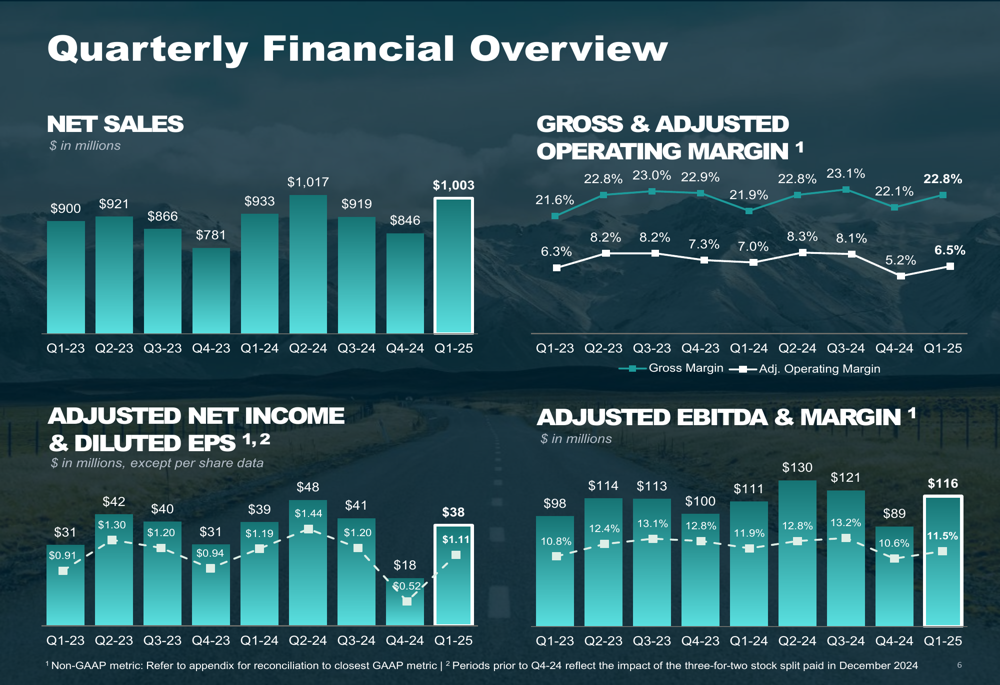

Patrick’s quarterly financial trends show steady improvement in net sales and adjusted EBITDA over recent quarters:

Segment Analysis

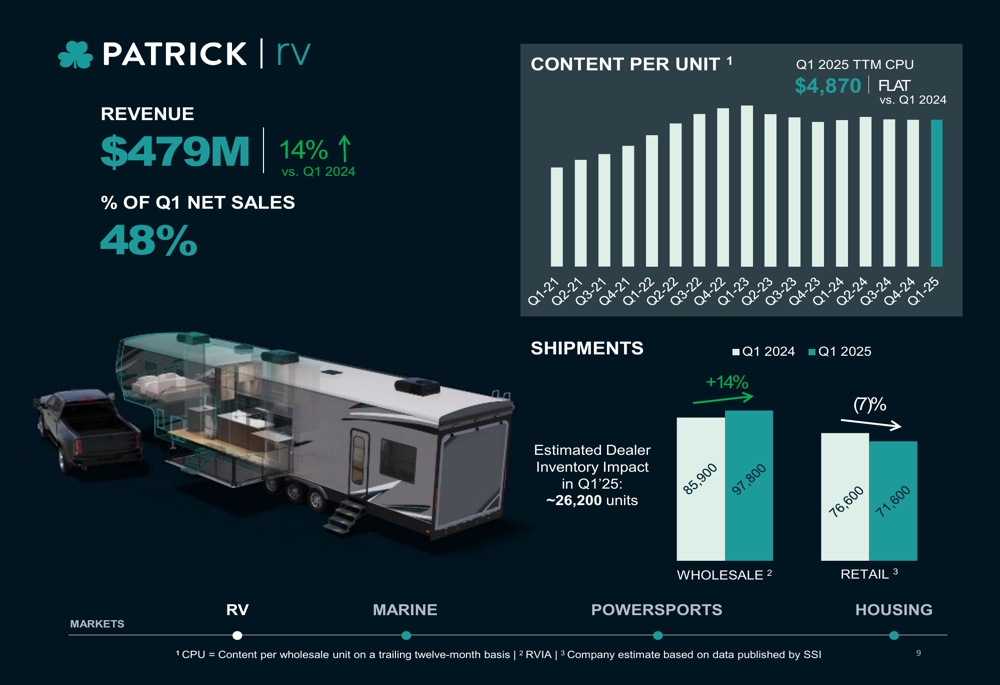

The RV segment was a standout performer in Q1 2025, with revenue increasing 14% year-over-year to $479 million. This growth was driven by a 14% increase in wholesale shipments to 97,800 units, though retail shipments decreased 7% to 71,600 units. Content per unit remained flat at $4,870.

The following chart illustrates the RV segment’s performance metrics:

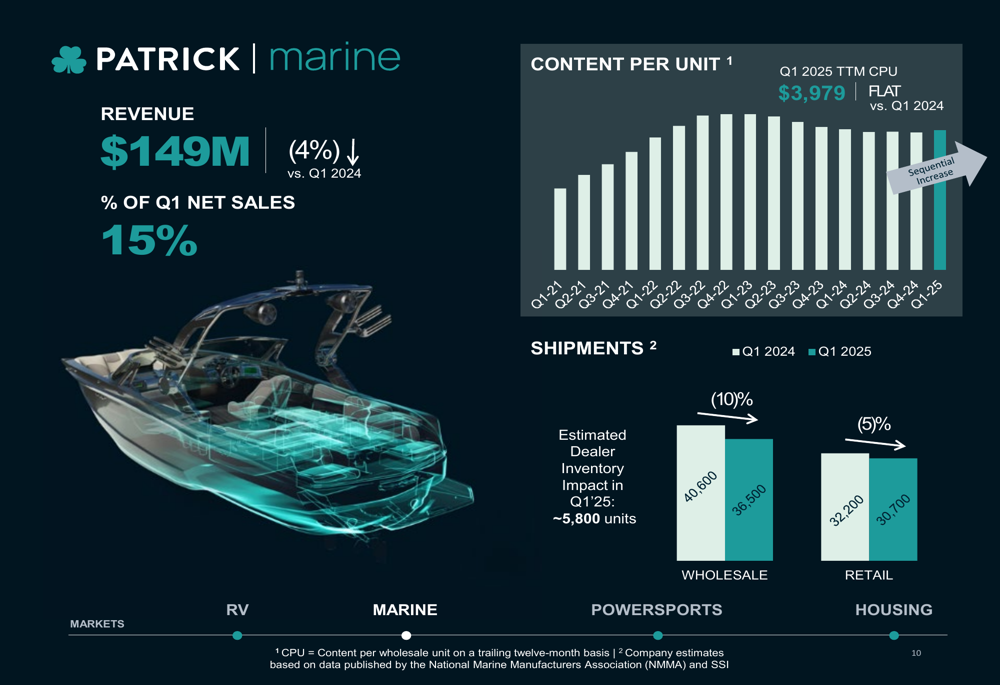

In contrast, the Marine segment experienced a 4% revenue decline to $149 million, as wholesale shipments fell 10% to 36,500 units and retail shipments decreased 5% to 30,700 units. Content per unit remained stable at $3,979.

The Marine segment’s performance is detailed in this chart:

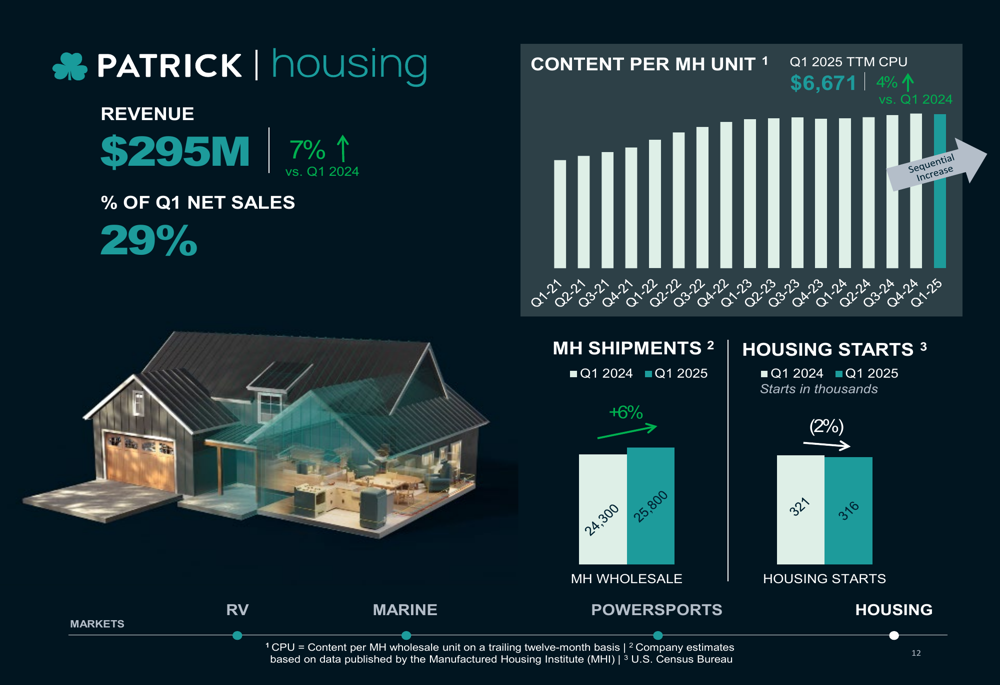

The Housing segment showed strong performance with revenue increasing 7% to $295 million. Manufactured housing shipments rose 6% to 25,800 units, while housing starts decreased slightly by 2% to 316,000. Content per manufactured housing unit increased 4% to $6,671.

The Housing segment’s metrics are illustrated here:

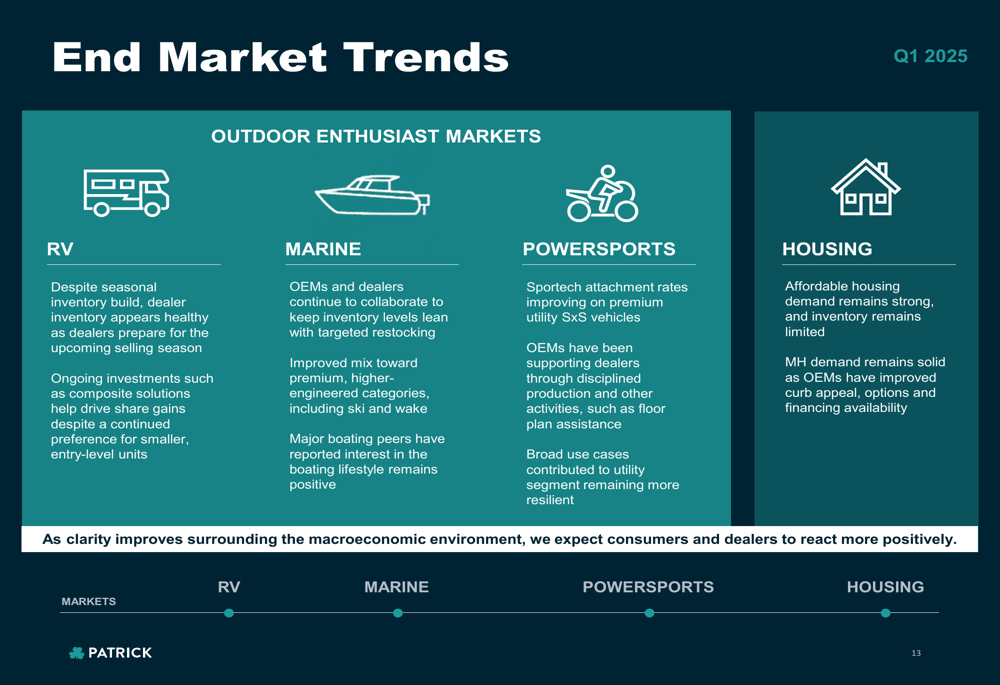

Patrick provided insights into current market trends across its segments, noting that RV dealer inventory appears healthy despite seasonal build, while Marine OEMs and dealers are maintaining lean inventory with targeted restocking. The company also highlighted that affordable housing demand remains strong with limited inventory.

The company’s assessment of end market trends is shown in the following slide:

Strategic Initiatives & Acquisitions

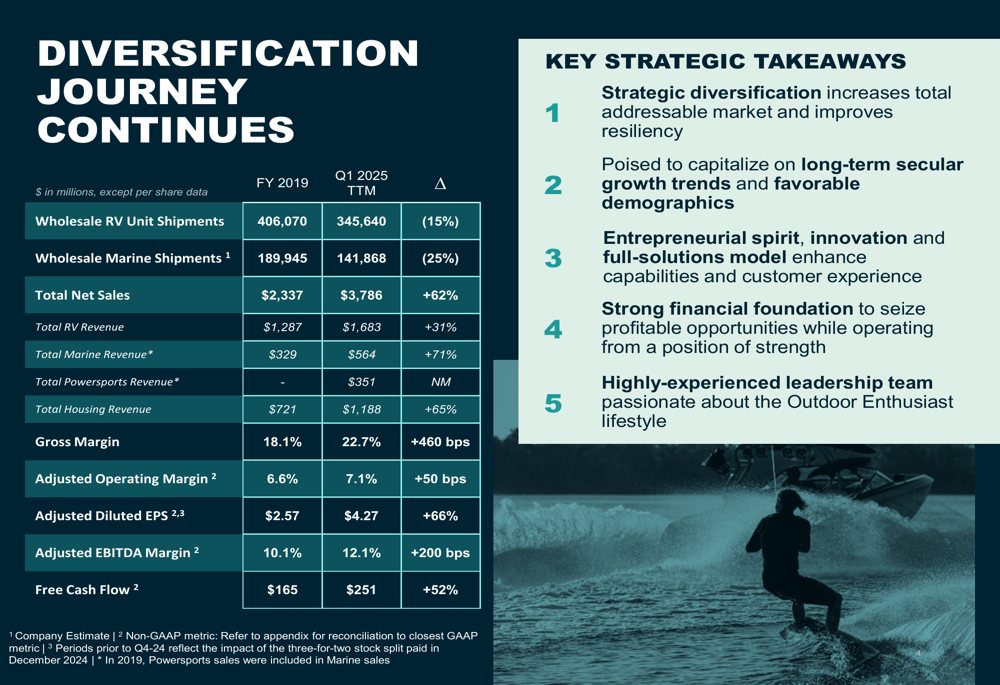

Patrick continues to execute on its strategic diversification plan, which has shown significant progress since 2019. Despite industry challenges, including a 15% decrease in wholesale RV unit shipments and a 25% decrease in wholesale Marine shipments since 2019, the company has grown its total net sales by 62% to $3.8 billion.

The company’s diversification journey is illustrated in this comprehensive overview:

During Q1 2025, Patrick completed two strategic acquisitions: Elkhart Composites and Medallion Instrumentation Systems, further expanding its product offerings and market reach. The company returned over $22 million to shareholders during the quarter while maintaining its acquisition strategy.

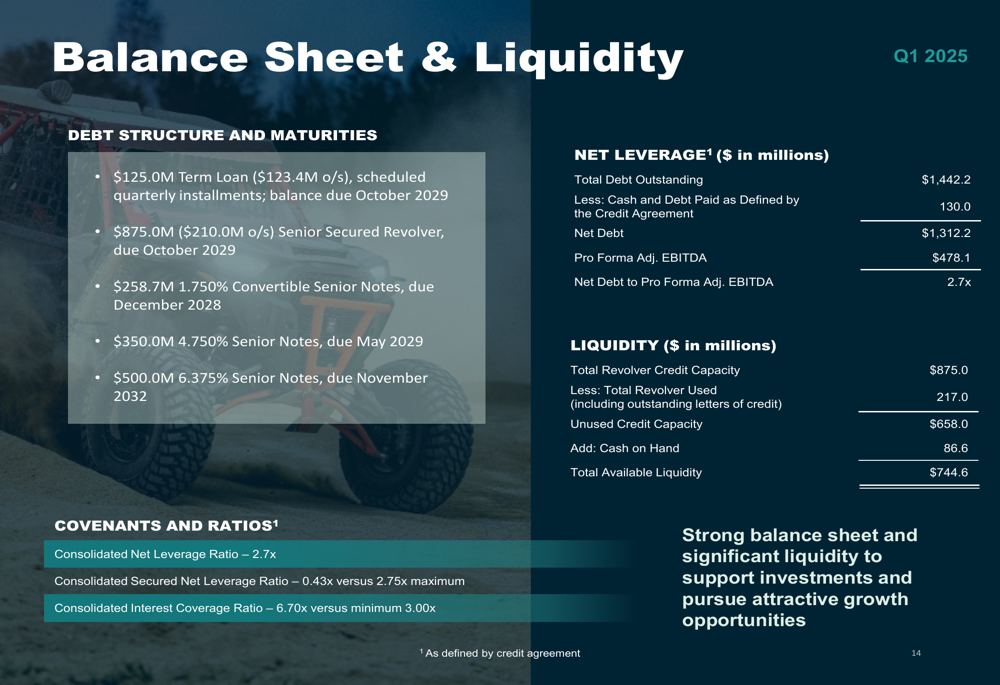

Balance Sheet & Liquidity

Patrick Industries maintains a strong financial position with total available liquidity of $744.6 million as of Q1 2025, including $86.6 million in cash and $658.0 million in unused credit capacity. The company’s net debt stands at $1.3 billion, resulting in a net debt to Pro Forma Adjusted EBITDA ratio of 2.7x.

The company’s balance sheet and liquidity position is detailed in this slide:

Operating cash flow improved 14% to $40 million in Q1 2025, while free cash flow was $20 million. On a trailing twelve-month basis, free cash flow reached $251 million, representing a 52% increase from 2019.

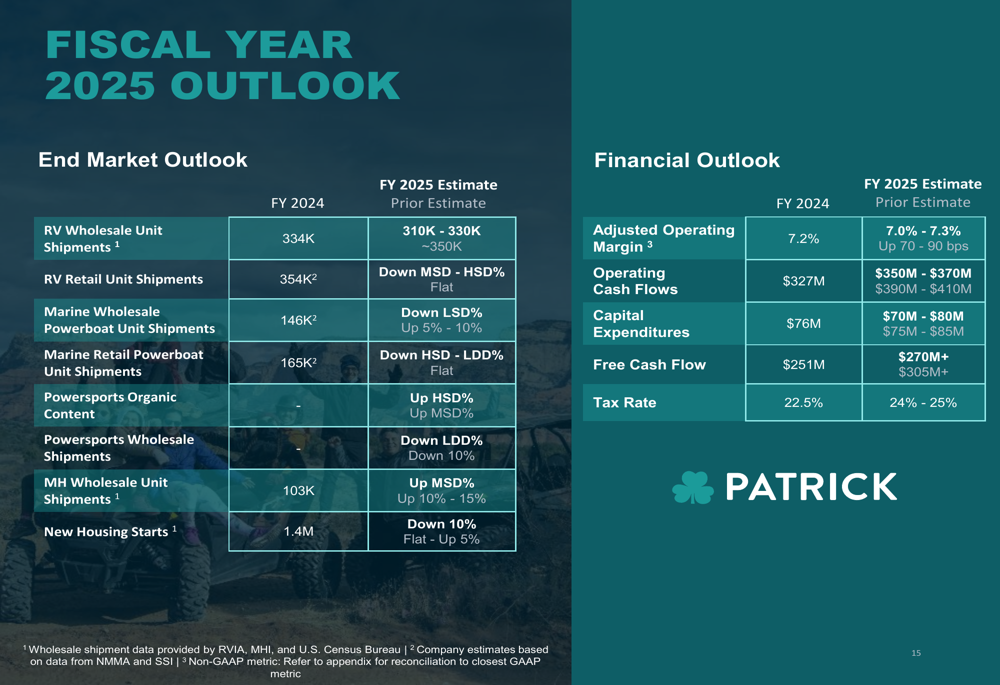

Forward Outlook

Looking ahead to the remainder of fiscal year 2025, Patrick Industries projects RV wholesale unit shipments of 310,000 to 330,000 units, compared to 334,000 units in FY 2024. The company expects adjusted operating margin to be in the range of 7.0% to 7.3%, compared to 7.2% in FY 2024.

The company’s fiscal year 2025 outlook is summarized in this slide:

Patrick Industries expressed cautious optimism about future market conditions, stating, "As clarity improves surrounding the macroeconomic environment, we expect consumers and dealers to react more positively."

This Q1 2025 performance builds on momentum seen in previous quarters. In its Q3 2024 earnings report, Patrick had reported a 6% revenue increase to $919 million and a 7% increase in adjusted EBITDA to $121 million, indicating consistent growth trajectory despite industry fluctuations.

With its diversified business model, strong cash flow generation, and strategic acquisition strategy, Patrick Industries appears well-positioned to navigate market challenges while capitalizing on growth opportunities across its various end markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.