U.S. stocks rise on Fed cut bets; earnings continue to flow

Introduction & Market Context

PayPal Holdings Inc (NASDAQ:PYPL) presented its second quarter 2025 results on July 29, showcasing accelerating growth and improved financial performance. The digital payments giant reported 5% revenue growth year-over-year, an improvement from the previous quarter, leading management to raise full-year guidance for both transaction margin dollars and earnings per share. Despite the positive results, PayPal’s stock traded down 1.56% in premarket trading at $77.00, following a 0.31% gain the previous day.

The company’s Q2 performance demonstrates continued momentum from its Q1 results, when it beat earnings expectations but slightly missed revenue forecasts. The latest presentation highlights PayPal’s strategic shift from a pure payments company to a comprehensive commerce platform with multiple growth drivers.

Quarterly Performance Highlights

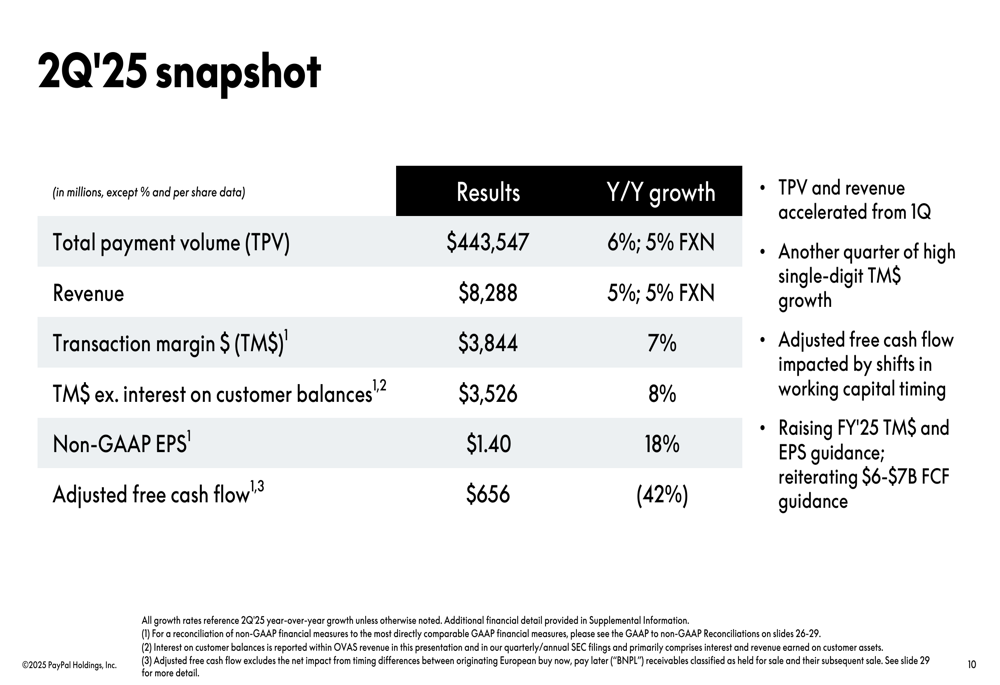

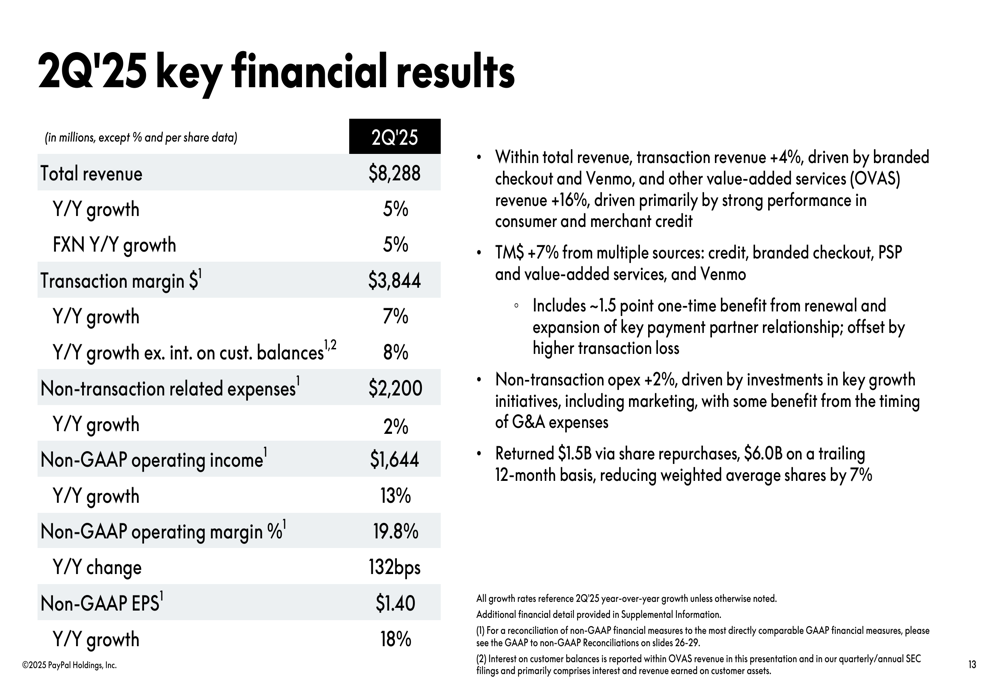

PayPal reported total payment volume (TPV) of $443.5 billion, representing 6% year-over-year growth (5% on an FX-neutral basis). Revenue reached $8.29 billion, up 5% compared to the same period last year, while non-GAAP earnings per share climbed 18% to $1.40.

Transaction (JO:NTUJ) margin dollars (TM$), a key metric for PayPal’s profitability, grew 7% year-over-year to $3.84 billion. Excluding interest on customer balances, TM$ increased by 8%, demonstrating the company’s ability to drive profitable growth across its core business.

As shown in the following snapshot of Q2 2025 key financial results:

The company’s active account base grew to 438 million, a 2% increase year-over-year, while monthly active accounts also rose 2% to 226 million. These modest user growth figures reflect PayPal’s focus on driving engagement and value from existing users rather than pursuing aggressive user acquisition.

Strategic Initiatives

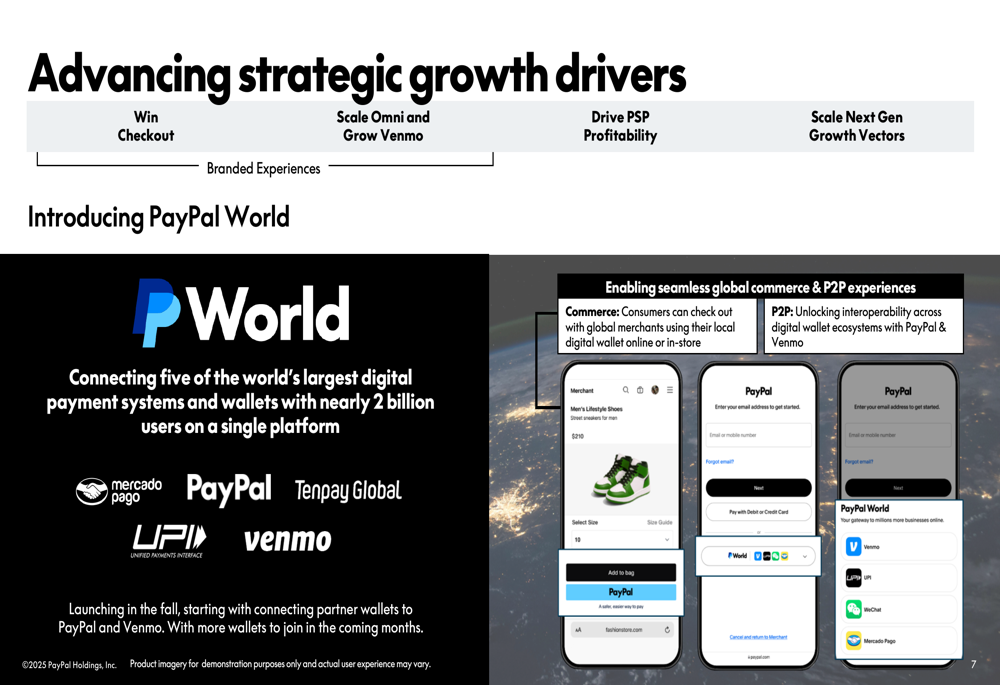

PayPal introduced several strategic initiatives aimed at expanding its ecosystem and driving future growth. Most notably, the company unveiled "PayPal World," a platform connecting five of the world’s largest digital payment systems and wallets with nearly 2 billion users. Set to launch in fall 2025, PayPal World will connect partner wallets including Mercado Pago, Tenpay Global, UPI, and Venmo.

As illustrated in this preview of the PayPal World platform:

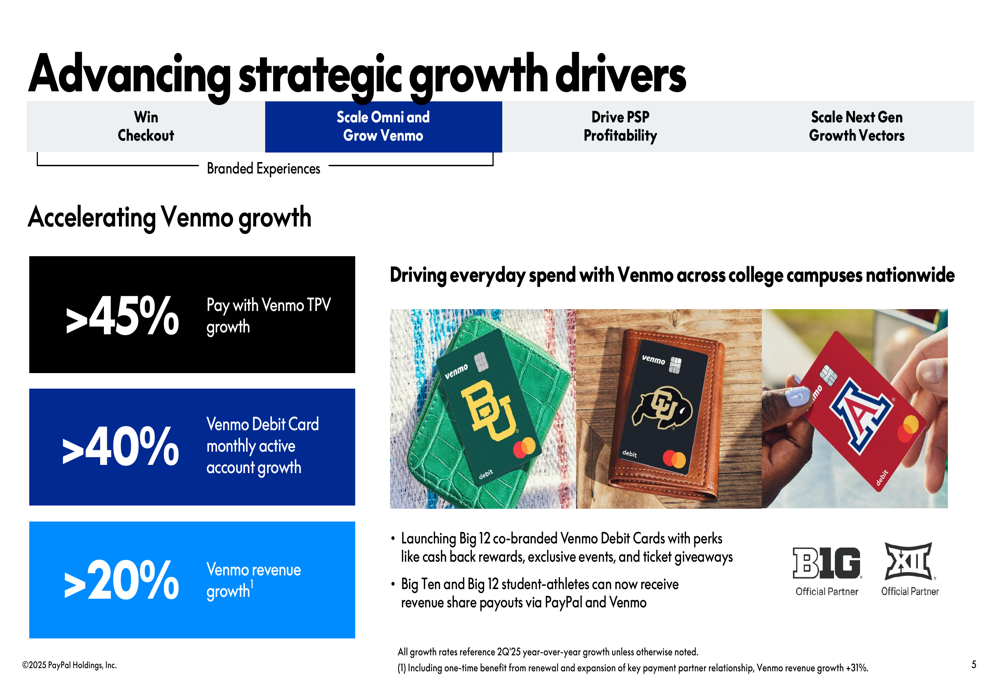

Venmo, PayPal’s peer-to-peer payment service, showed particularly strong performance with revenue growth exceeding 20% (31% including a one-time benefit from a key payment partner relationship). Venmo’s total payment volume grew 12%, its highest rate in three years, while its debit card saw monthly active account growth of over 40%.

The company highlighted its Venmo growth initiatives, including the launch of Big 12 co-branded debit cards:

PayPal is also expanding beyond e-commerce with initiatives like its first contactless mobile wallet, now available nationwide in Germany on both iOS and Android. The company reported over 3 million contactless mobile wallet enrollments in Germany since launch, with more than 50% of enrolled NFC users setting PayPal as their default NFC wallet.

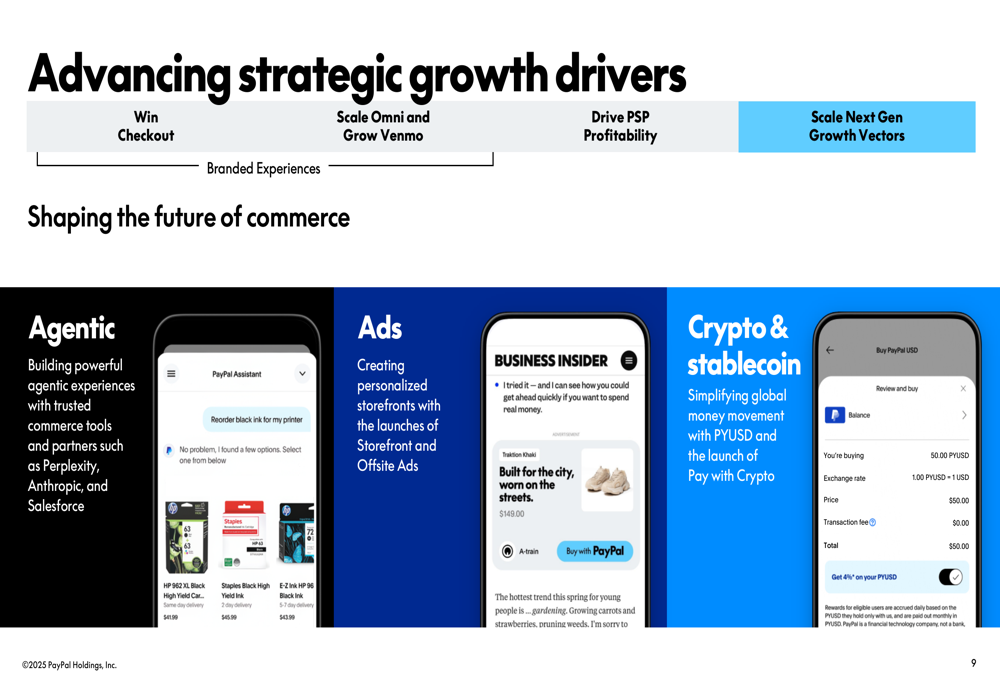

The company’s innovation strategy focuses on three key areas: agentic experiences (AI-powered commerce tools), personalized storefronts with ads, and crypto & stablecoin payment options. These initiatives aim to shape the future of commerce by creating more intelligent, personalized, and flexible payment experiences.

As shown in this overview of PayPal’s innovation focus areas:

Detailed Financial Analysis

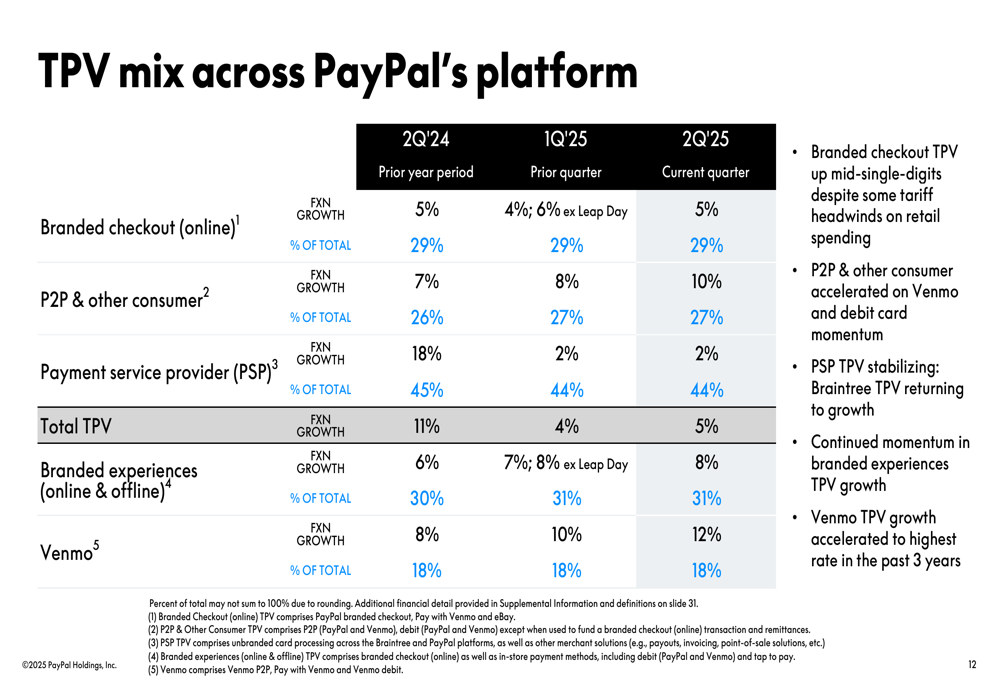

PayPal’s TPV mix shows varying growth rates across different segments of its business. Branded checkout (online) grew 5% on an FX-neutral basis and represents 29% of total TPV. Peer-to-peer and other consumer payments grew 8% and account for 27% of TPV, while payment service provider (PSP) volumes grew 2% and make up 44% of total TPV.

The TPV mix across PayPal’s platform reveals important trends:

A notable development is the return to growth for Braintree, PayPal’s payment processing solution for merchants. After several quarters of challenges, the stabilization of the PSP business segment represents an important milestone for the company.

Transaction revenue grew 4%, driven by positive contributions from branded checkout, Venmo, and consumer and merchant credit. Non-transaction expenses increased by just 2% year-over-year to $2.2 billion, demonstrating the company’s focus on operational efficiency. This led to non-GAAP operating income of $1.64 billion, up 13% year-over-year.

The key financial results demonstrate PayPal’s improving profitability metrics:

One area of concern was adjusted free cash flow, which declined 42% year-over-year to $656 million. Despite this quarterly drop, PayPal maintained its full-year free cash flow guidance of $6-7 billion, suggesting management expects stronger cash generation in the second half of the year.

Forward-Looking Statements

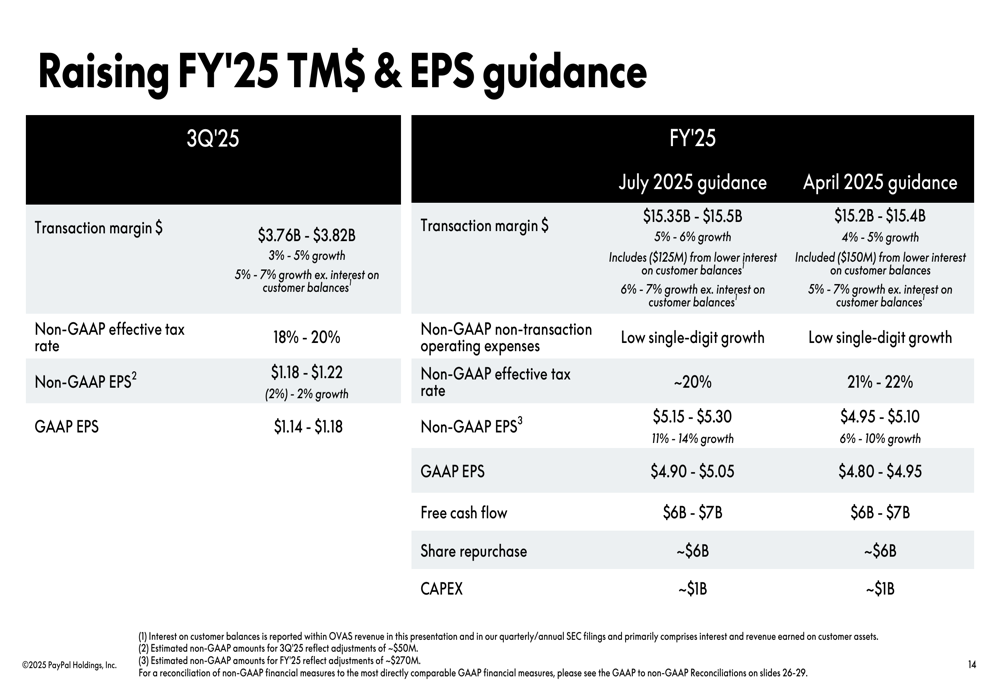

Based on its strong first-half performance, PayPal raised its full-year 2025 guidance for both transaction margin dollars and earnings per share. The company now expects transaction margin dollars of $15.35-15.5 billion, up from its previous guidance of $15.2-15.4 billion. Non-GAAP EPS guidance was raised to $5.15-5.30, compared to the previous range of $4.95-5.10.

The updated guidance reflects management’s confidence in continued execution across multiple growth drivers:

PayPal maintained its free cash flow guidance of $6-7 billion for the full year, despite the weaker Q2 performance in this metric. The company highlighted that it continues to return capital to shareholders, with $1.5 billion in share repurchases reducing weighted average shares by 7%.

Looking ahead, PayPal emphasized its focus on strengthening its value proposition through branded experiences, expanding Venmo, driving PSP profitability, and investing in future commerce innovations. The company’s multi-pronged strategy aims to balance near-term financial performance with long-term growth initiatives in an increasingly competitive digital payments landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.