US stock futures inch higher with Q3 earnings on tap

Introduction & Market Context

Permian Resources Corp (NASDAQ:PR) reported strong first-quarter 2025 results on May 7, showcasing operational efficiency improvements and strategic capital allocation. The pure-play Delaware Basin exploration and production company demonstrated continued execution across key financial and operational metrics, building on momentum despite missing analyst expectations in the previous quarter.

The company’s stock was up 1.93% in premarket trading at $12.12, suggesting a positive initial market reaction to the results. This follows a pattern seen after Q4 2024 earnings, when the stock rose 4.02% despite missing EPS and revenue forecasts, as investors focused on cash flow generation and growth prospects.

Quarterly Performance Highlights

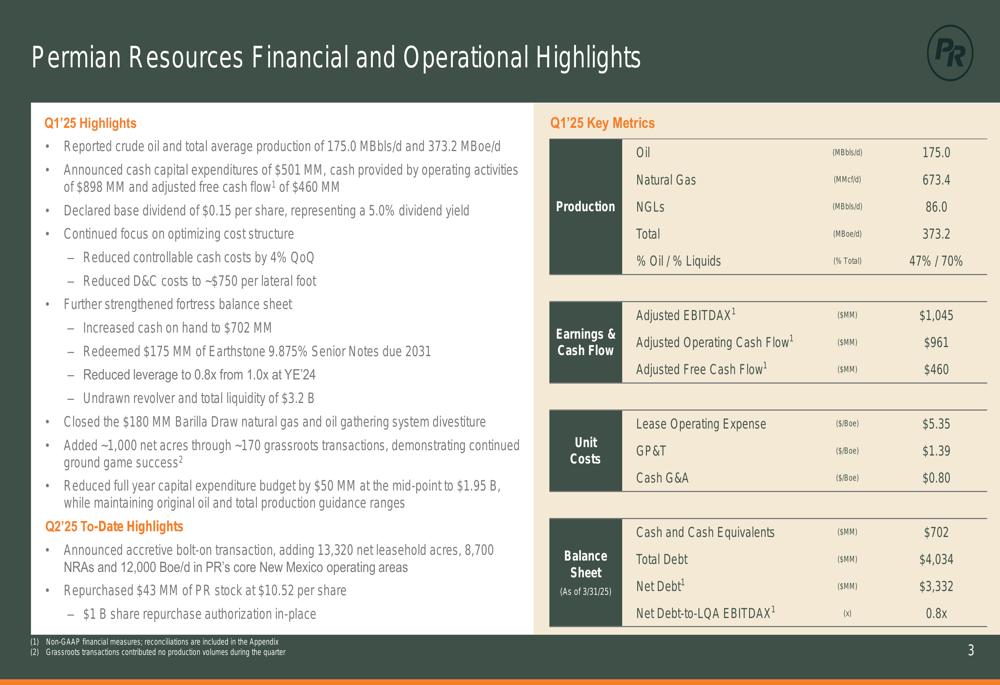

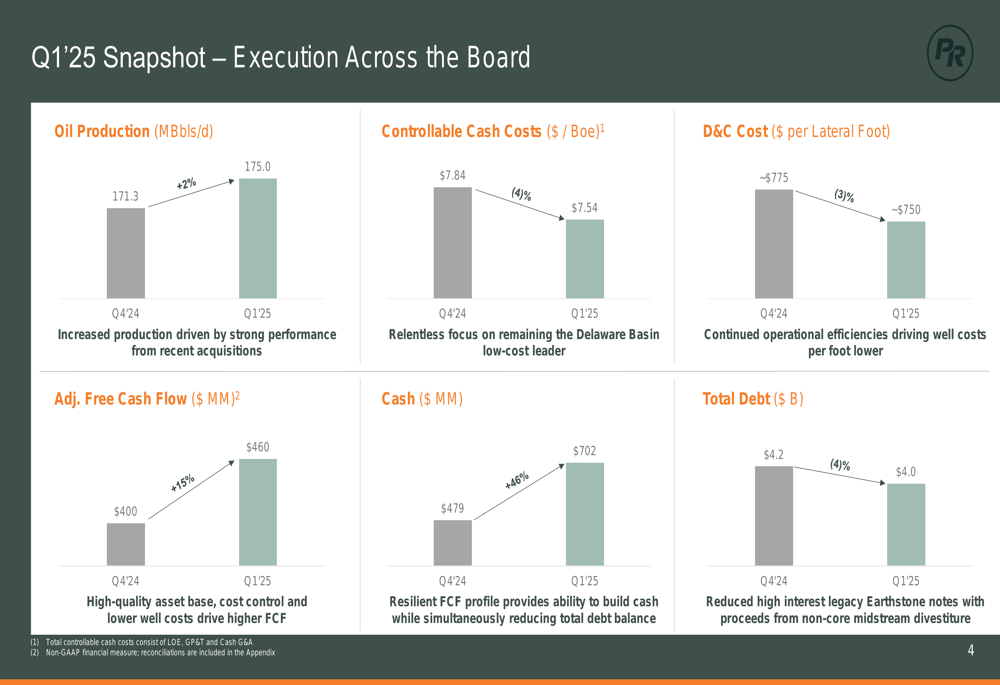

Permian Resources delivered solid operational results in Q1 2025, with crude oil production reaching 175.0 MBbls/d, representing a 2% increase from the previous quarter. Total (EPA:TTEF) production averaged 373.2 MBoe/d, while the company generated $898 million in cash from operating activities and $460 million in adjusted free cash flow, a 15% increase from Q4 2024.

As shown in the following performance metrics chart:

The company demonstrated execution across multiple fronts, with controllable cash costs decreasing 4% to $7.54/Boe and drilling and completion costs reduced by 3% to approximately $750 per lateral foot. These efficiency gains contributed to the improved free cash flow generation, enabling a quarterly base dividend of $0.15 per share, which represents a 5.0% yield.

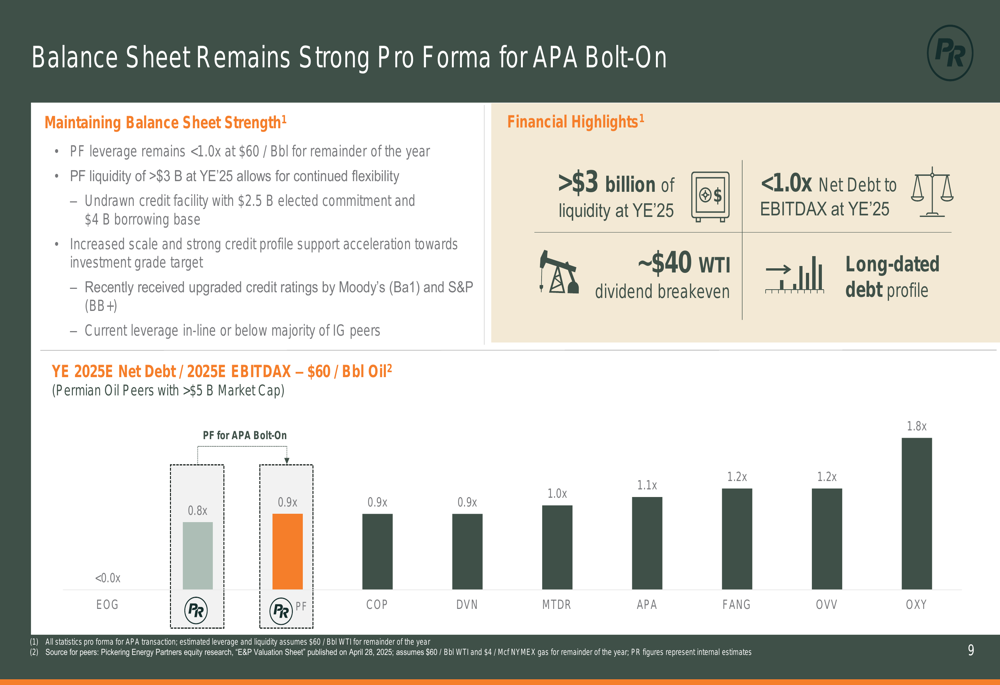

Balance Sheet Strengthening

A key highlight of the quarter was Permian Resources’ significant balance sheet improvement. Cash increased 46% to $702 million, while total debt decreased 4% to $4.0 billion. This resulted in a reduction of the net debt-to-LQA EBITDAX ratio from 1.1x at year-end 2023 to 0.8x in Q1 2025.

The company’s financial position is illustrated in the following chart:

Total liquidity reached $3.2 billion, up from $2.1 billion at year-end 2023, providing substantial financial flexibility. Projected free cash flow is expected to grow from $0.7 billion in FY 2023 to $1.4 billion in FY 2025, with FCF per share increasing from $1.13 to $1.64. The company also maintains a strong hedge position, with 24% of 2025 oil production hedged, comparing favorably to several peers.

Strategic Acquisitions and Capital Allocation

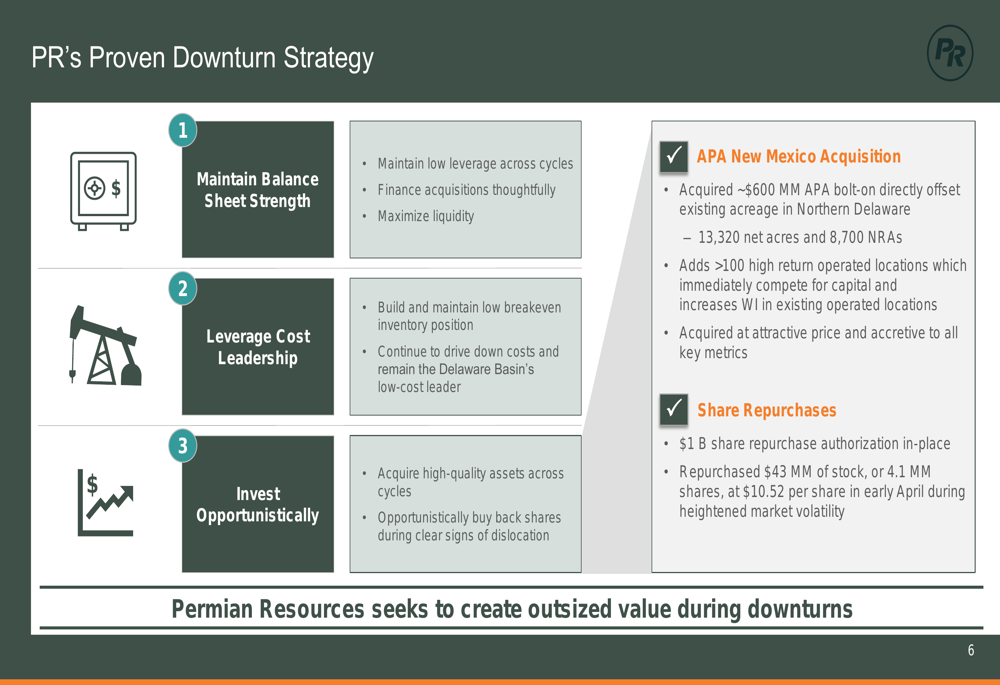

Permian Resources outlined its "proven downturn strategy" focused on maintaining balance sheet strength, leveraging cost leadership, and investing opportunistically. This approach was evident in the company’s recent transactions, including a strategic bolt-on acquisition and share repurchases during market dislocations.

The company’s bolt-on acquisition in New Mexico is detailed in the following slide:

The $608 million acquisition adds approximately 13,320 net acres and 8,700 net royalty acres to Permian Resources’ position in the Delaware Basin. The transaction is expected to be funded with cash on hand while maintaining leverage below 1x and over $3 billion in liquidity at year-end 2025. The acquisition is projected to add approximately 12 MBoe/d of production (45% oil) and over 100 new gross operated locations, with free cash flow per share accretion exceeding 5%.

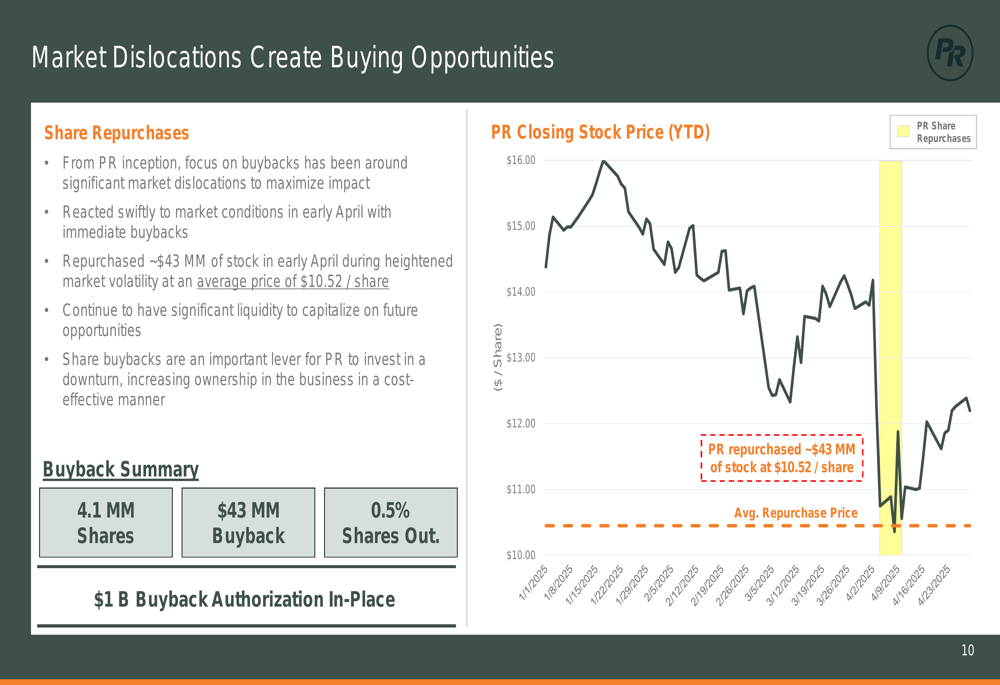

Permian Resources also repurchased $43 million of its stock at an average price of $10.52 per share, representing 4.1 million shares or 0.5% of shares outstanding. The company has a $1 billion share repurchase authorization in place, demonstrating its commitment to returning capital to shareholders during market dislocations.

The timing of these share repurchases is illustrated in the following chart:

Updated Guidance and Outlook

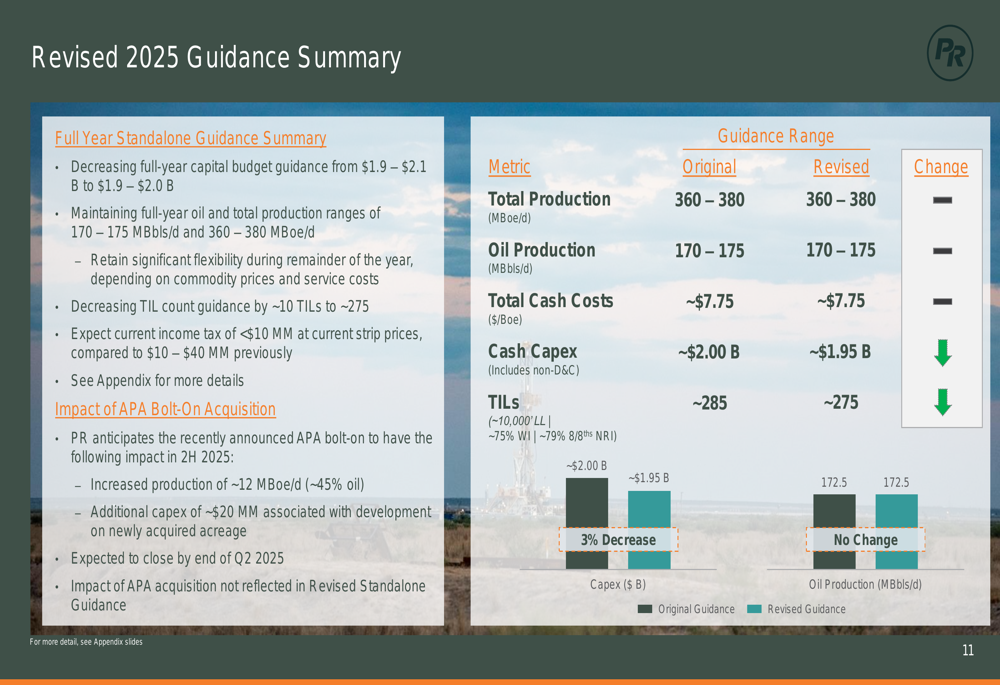

Permian Resources maintained its full-year production guidance while reducing capital expenditure targets, reflecting improved operational efficiency. The company now expects full-year capital spending of $1.9-2.0 billion, down from the previous range of $1.9-2.1 billion, while maintaining oil production guidance of 170-175 MBbls/d and total production of 360-380 MBoe/d.

The updated guidance is summarized in the following table:

The company also reduced its planned well count, decreasing the total TIL (turned-in-line) count by approximately 10 wells to around 275 for the year. This adjustment reflects the company’s focus on capital efficiency and disciplined growth.

Competitive Positioning

Permian Resources highlighted its strong competitive position in the industry, emphasizing its robust free cash flow generation, operational execution track record, and low-cost structure. The company positions itself as offering a leading combination of quality Permian inventory, free cash flow per share generation, balance sheet strength, and cost efficiency.

The following chart illustrates Permian Resources’ valuation relative to peers:

The company’s management team maintains significant ownership, with executives holding more than 6% of shares outstanding, ensuring alignment with shareholder interests. This ownership level exceeds that of many industry peers, where CEO ownership typically averages around 0.5%.

Permian Resources also emphasized its commitment to ESG initiatives, having reduced flaring from 2.0% to 1.0%, increased deployment of continuous emissions monitoring across 60% of oil production, and utilized recycled water in 47% of water used for completion operations.

With its strengthened balance sheet, disciplined capital allocation strategy, and operational efficiency improvements, Permian Resources appears well-positioned to navigate market volatility while continuing to generate value for shareholders through both organic growth and strategic acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.