One & One Green Technologies stock soars 100% after IPO debut

Introduction & Market Context

Pfisterer Holding SE (PFSE) released its half-year 2025 financial results on August 22, highlighting substantial growth in order intake and improved profitability across its electrical connection and insulation solutions business. The company’s stock closed at €60.70 on August 21, up 0.83% ahead of the results announcement, and remains near its 52-week high of €62.30.

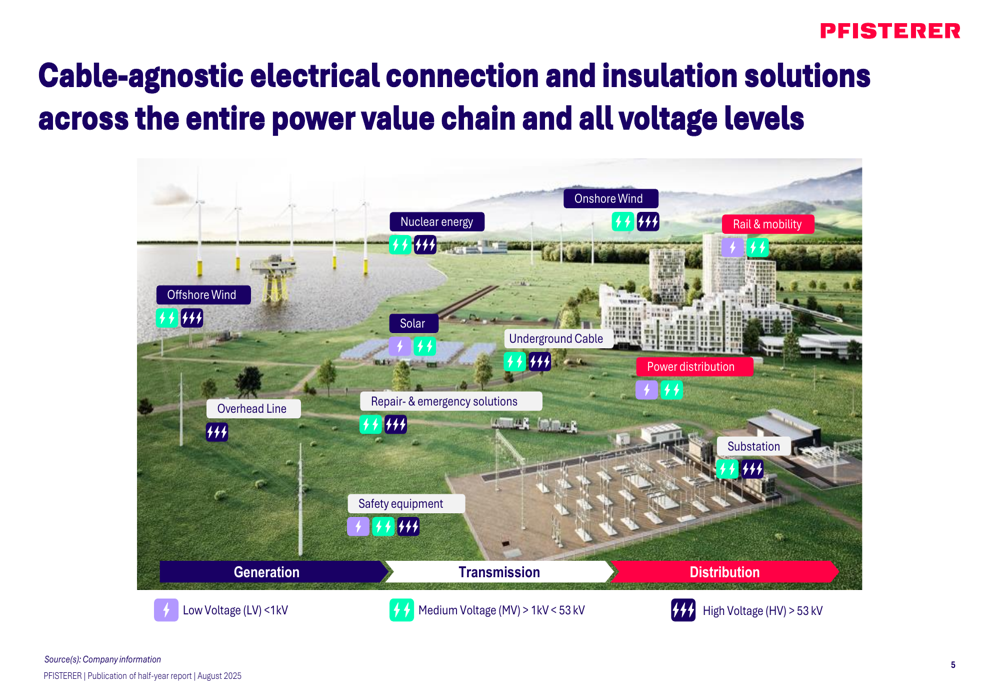

Pfisterer, a global provider of cable-agnostic electrical connection and insulation solutions, operates across the entire power value chain and all voltage levels in over 90 countries. The company is positioned to benefit from several major market trends, including increased electricity demand driven by digitalization and AI, grid modernization in Europe, and substantial infrastructure investments in the United States.

As shown in the following image of Pfisterer’s power value chain positioning:

Financial Highlights

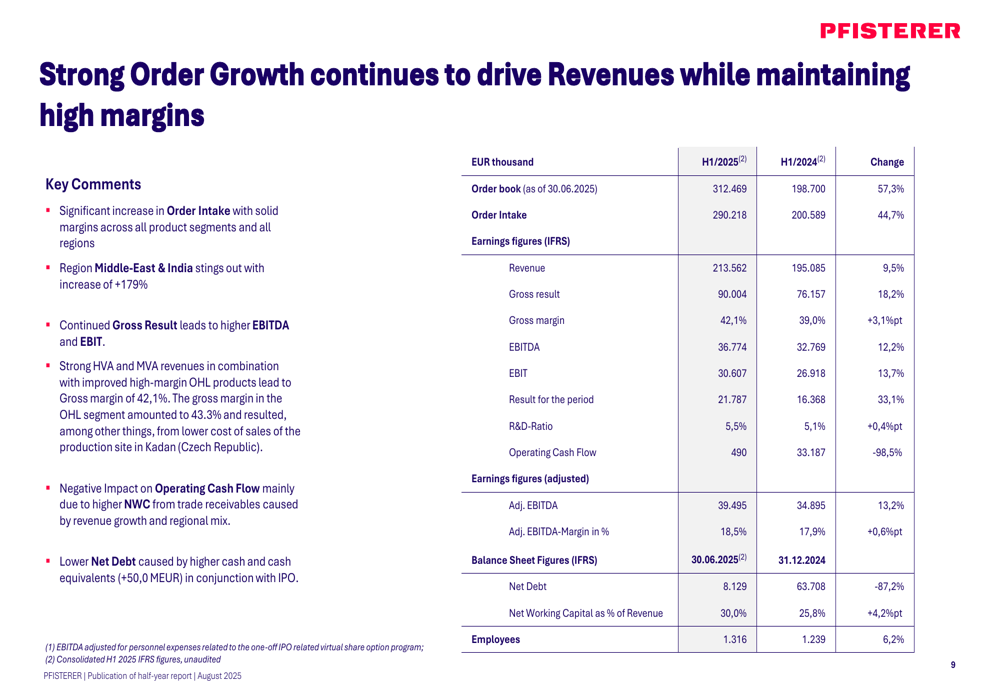

Pfisterer reported impressive financial results for the first half of 2025, with particularly strong performance in the second quarter. The company’s order book reached €312.47 million, representing a 57.3% increase compared to H1 2024, while order intake grew 44.7% to €290.22 million.

Revenue for H1 2025 increased by 9.5% year-over-year to €213.56 million, with gross profit rising 18.2% to €90.00 million. This resulted in a gross margin of 42.1%, demonstrating the company’s ability to maintain healthy profitability despite global supply chain challenges. EBITDA and EBIT showed strong growth at 12.2% and 13.7% respectively, while net debt decreased dramatically by 87.2% from December 31, 2024, to just €8.13 million.

The comprehensive financial performance is detailed in the following table:

The second quarter of 2025 showed particularly strong momentum, with revenue increasing 21.3% year-over-year to €113.44 million. Gross profit for Q2 jumped 28.7% to €47.95 million, resulting in a gross margin of 42.3%. EBITDA for the quarter grew 23.0% despite one-off costs related to the company’s IPO.

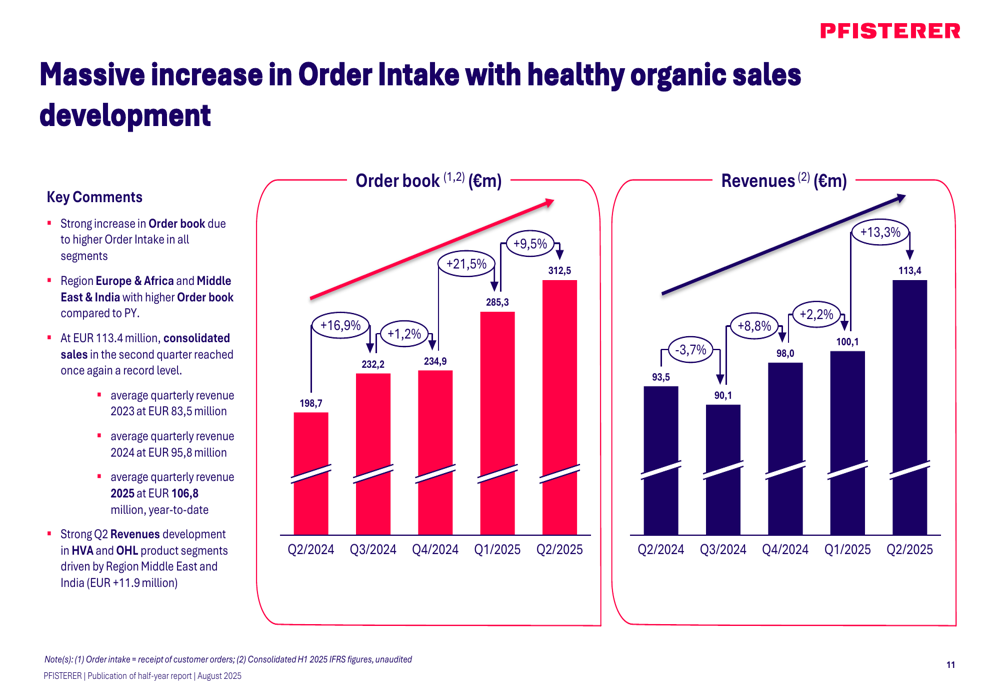

As illustrated in the quarterly revenue and order book progression:

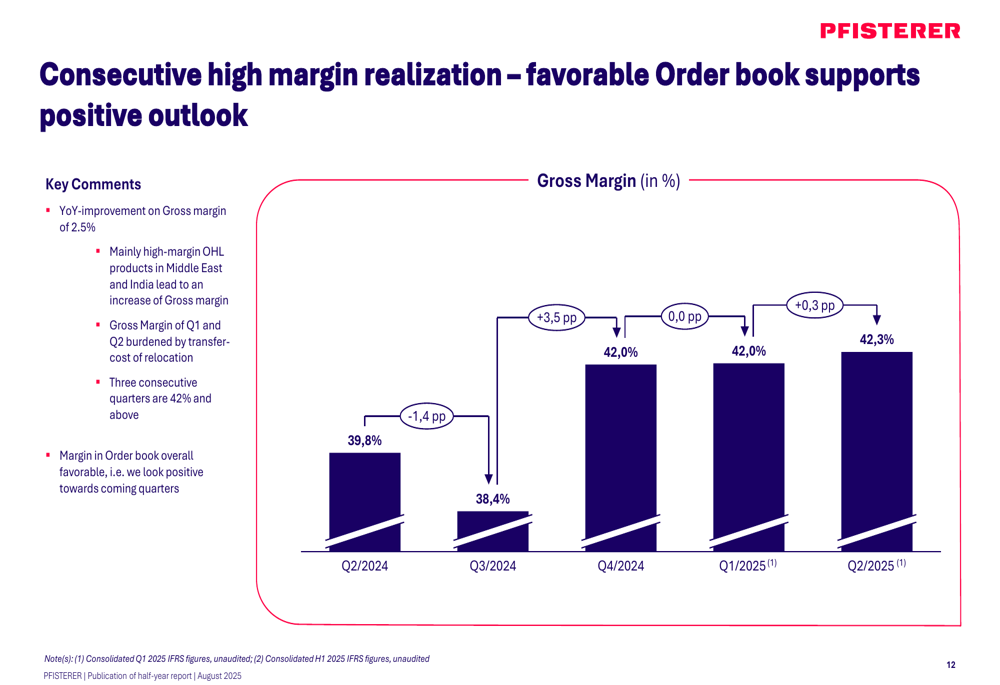

Pfisterer has maintained consistent gross margin improvement over five consecutive quarters, with Q2 2025 reaching 42.3%, representing a 2.5 percentage point improvement year-over-year:

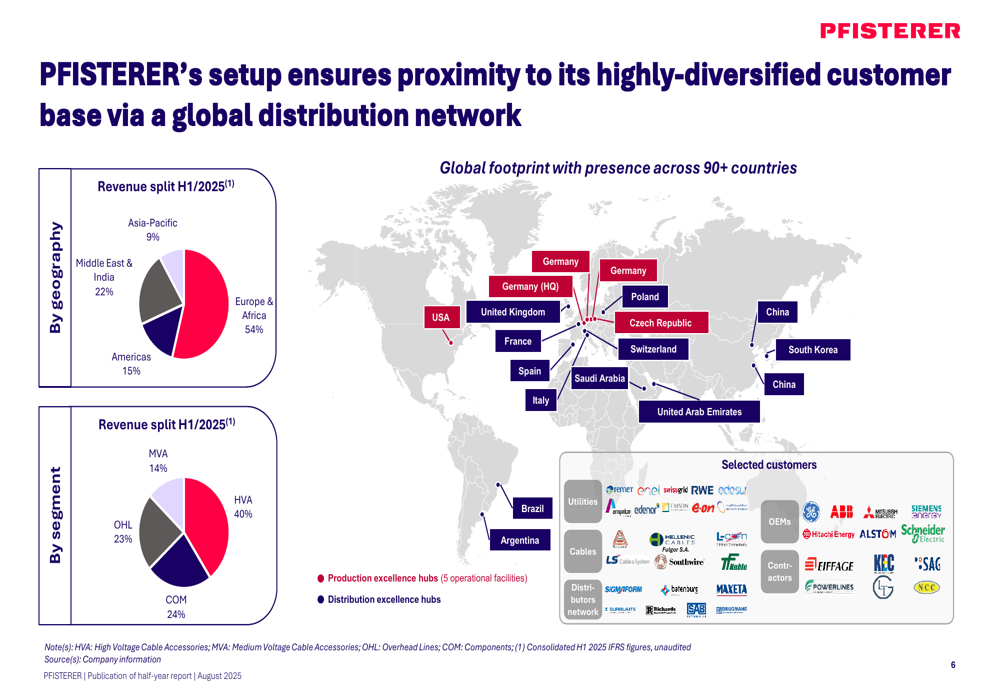

Geographic & Segment Analysis

Pfisterer’s revenue mix showed notable geographic shifts in H1 2025, with the Middle East & India region increasing its contribution to 21.9% of total revenue, up from 16.0% in the same period last year. This growth came primarily at the expense of Europe & Africa, which declined from 58.1% to 54.2% of revenue, despite generating higher absolute revenue.

The global distribution of Pfisterer’s business is visualized in the following map and charts:

From a segment perspective, High Voltage Applications (HVA) strengthened its position as the company’s largest business segment, growing to 40.2% of revenue in H1 2025 from 37.2% in H1 2024. Medium Voltage Applications (MVA) also showed strong growth, increasing its share to 13.5% from 11.9%. These gains came at the expense of the Overhead Lines ( OHL (BME:OHLA)) and Components (COM) segments, which declined to 22.8% and 23.5% of revenue, respectively.

Strategic Initiatives

Following the reporting period, Pfisterer announced two significant strategic investments to support future growth. The company received a building permit for a new HVDC High-Voltage Laboratory in Winterbach, representing a €30 million investment in state-of-the-art testing facilities. The lab is scheduled for commissioning in 2027 and will enhance Pfisterer’s capabilities in high-voltage direct current technology, an increasingly important area for long-distance power transmission.

Additionally, Pfisterer is strengthening its Kadaň site through the acquisition of 48,000 square meters of land adjacent to its existing plant. This expansion will provide capacity for future growth while leveraging operational synergies. To support these and other growth investments, the company has increased its Aval line by €30 million, enhancing its financial flexibility.

Forward-Looking Statements

Pfisterer is well-positioned to benefit from several major industry trends that are driving demand for its products and solutions. The company highlighted that AI data centers alone are expected to generate an additional 1,500 TWh of electricity demand by 2030, while Europe requires €2-2.3 trillion in grid modernization investments by 2050.

The U.S. market represents another significant opportunity, with over $2 trillion in infrastructure investments expected by 2050, strengthening demand for high-voltage connection systems. These market drivers support Pfisterer’s organic growth, which reached 7.8% in its electrification segments during the reporting period.

The company’s strong order book, which has grown consistently over five consecutive quarters, provides good visibility for continued revenue growth through the remainder of 2025 and into 2026. With its reduced debt levels and strategic capacity investments, Pfisterer appears well-equipped to capitalize on the global electrification trend while maintaining its healthy profit margins.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.