Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

PharmaCorp Rx Inc (TSXV:PCRX), a Canadian pharmacy consolidator, presented its Q2 2025 investor slides on August 15, highlighting strong same-store sales growth and continued execution of its acquisition-led strategy. The company, which operates under the PharmaChoice Canada banner, reported accelerating same-store sales growth of 11.3% in Q2, up significantly from 3.9% in Q1, demonstrating momentum in its core operations.

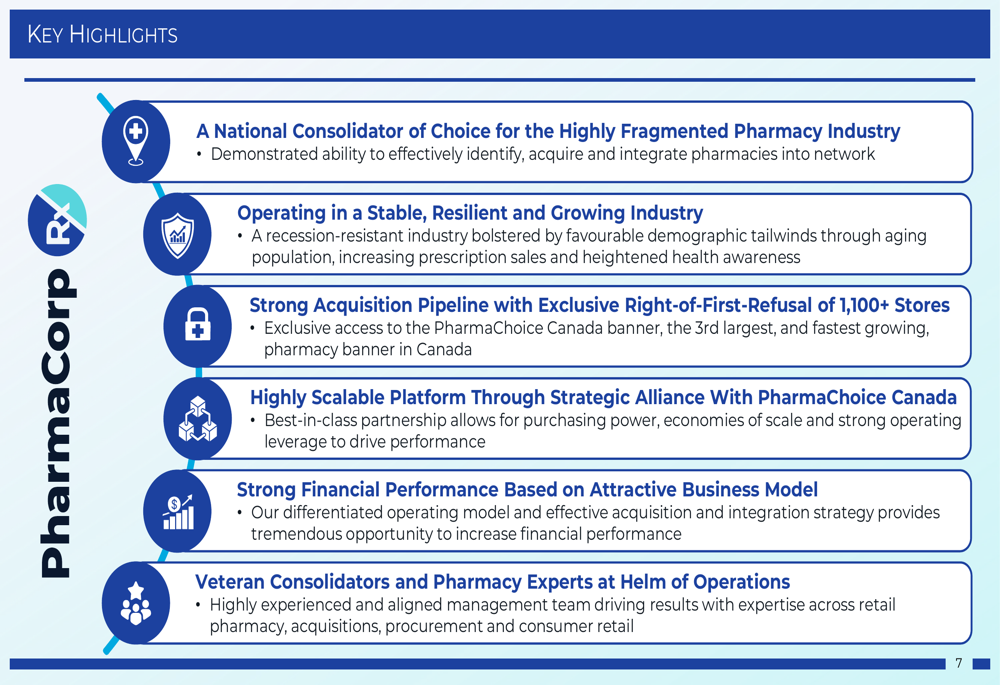

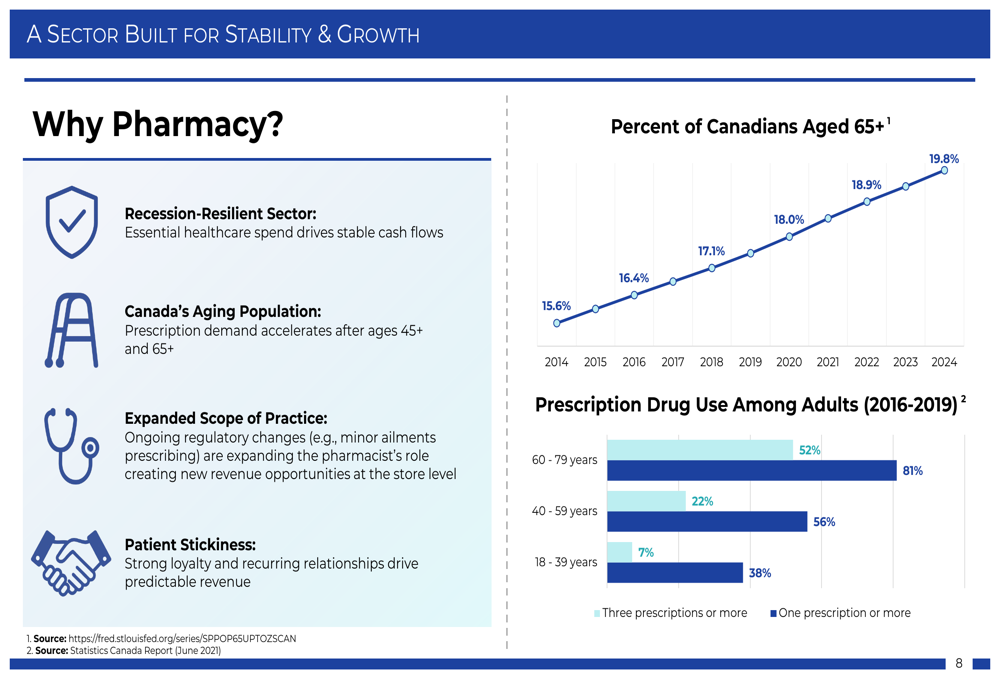

PharmaCorp operates in what it describes as a "stable, resilient and growing industry," benefiting from essential healthcare spending that drives consistent cash flows. The Canadian pharmacy sector is highly fragmented, with ownership models ranging from corporate chains to independent operators, creating opportunities for consolidation.

Strategic Positioning

PharmaCorp’s primary competitive advantage stems from its exclusive right-of-first-refusal (ROFR) agreement with PharmaChoice Canada, giving it priority access to acquire more than 1,100 independent pharmacies within the PCC network. This strategic alliance provides PharmaCorp with a built-in acquisition pipeline, as approximately 40-50 PCC stores change hands annually.

The company’s growth strategy leverages this ROFR agreement while maintaining flexibility to acquire non-PCC bannered pharmacies. Recent acquisitions include locations in Atlantic and Western Canada, expanding the company’s geographic footprint.

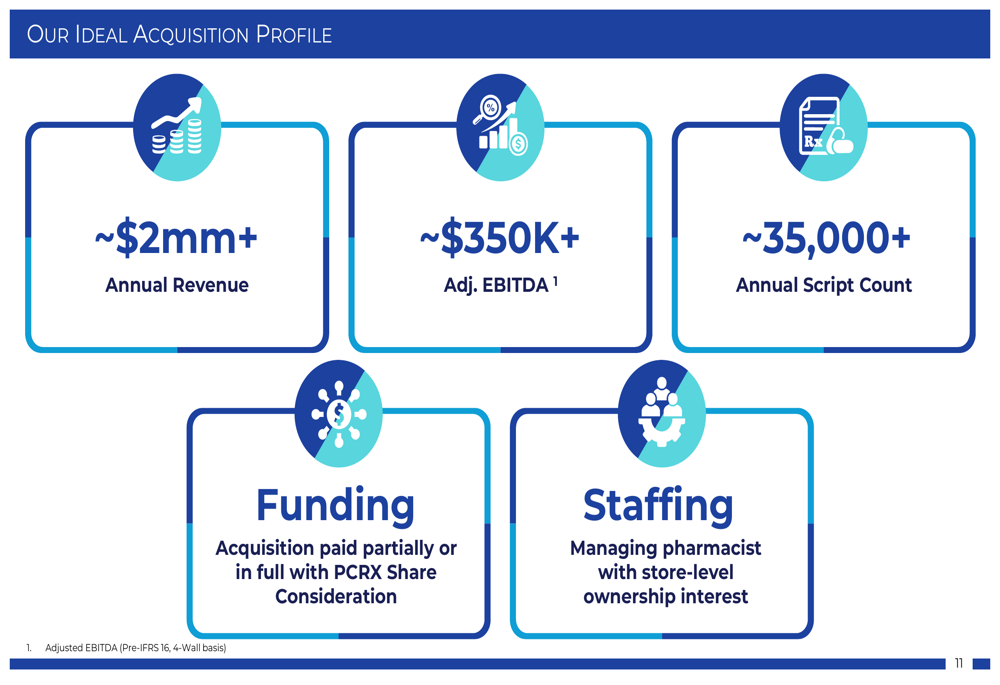

PharmaCorp has established a clear profile for its target acquisitions, focusing on pharmacies with approximately $2 million in annual revenue, $350,000+ in adjusted EBITDA, and over 35,000 annual prescription counts. The company typically structures deals to include partial or full payment with PCRX shares and emphasizes retaining managing pharmacists with store-level ownership interests.

Quarterly Performance Highlights

In Q2 2025, PharmaCorp reported same-store sales growth of 11.3%, a substantial increase from 3.9% in Q1. Same-store prescription count growth also improved slightly to 3.5% from 3.2% in the previous quarter. Adjusted EBITDA for Q2 was $688,000, a slight decrease from $707,400 in Q1.

The company maintains a strong balance sheet with $9.56 million in cash, total assets of $35.37 million, and limited liabilities of $4.94 million. This financial position, with low leverage, provides PharmaCorp with ample capacity to continue its acquisition strategy.

Growth Drivers

PharmaCorp highlighted several industry tailwinds supporting its growth strategy. Canada’s aging population is a significant driver, with the percentage of Canadians aged 65 and older increasing from 15.6% in 2014 to 19.8% in 2024. This demographic shift is particularly relevant as prescription drug use increases substantially with age - 81% of Canadians aged 60-79 take at least one prescription medication, and 52% take three or more.

The company also benefits from expanding scope of practice for pharmacists due to regulatory changes, and strong patient loyalty that creates predictable revenue streams.

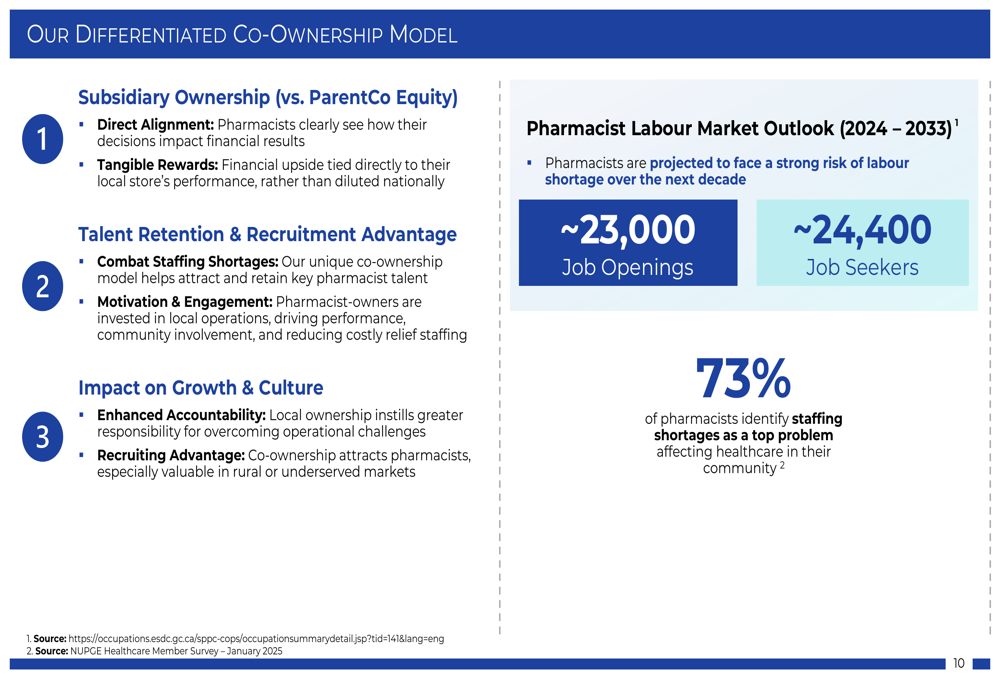

A key differentiator in PharmaCorp’s approach is its co-ownership model, which addresses challenges in the pharmacist labor market. Rather than offering equity in the parent company, PharmaCorp provides ownership opportunities at the subsidiary level, creating direct alignment and tangible rewards for pharmacists. This strategy helps combat staffing shortages - a concern for 73% of pharmacists - while enhancing accountability and providing a recruiting advantage.

Forward-Looking Statements

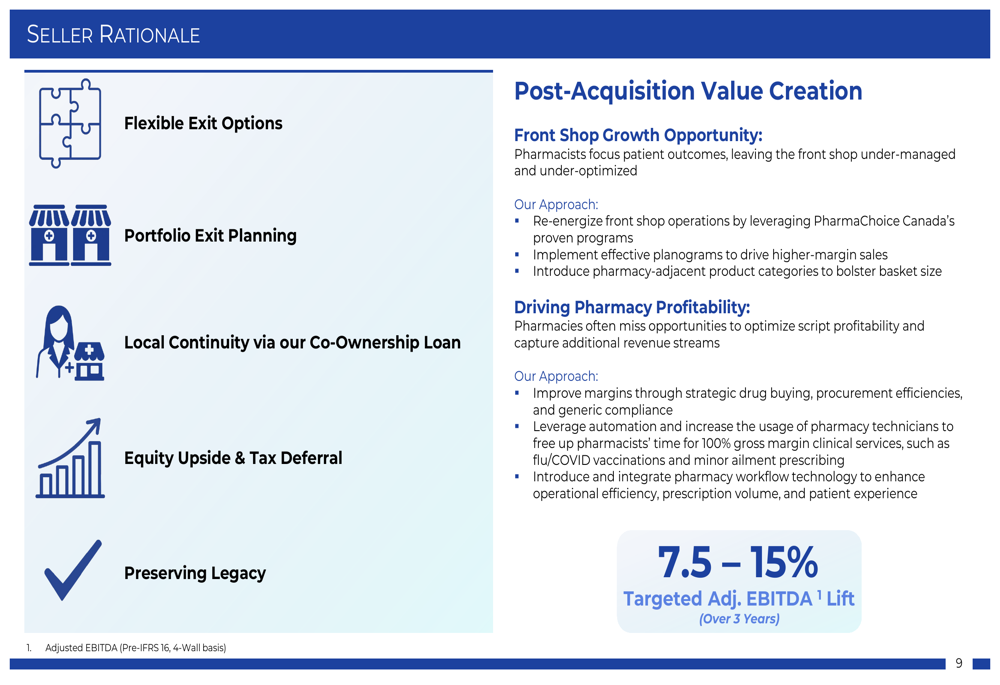

PharmaCorp’s post-acquisition value creation strategy focuses on front shop growth opportunities and driving pharmacy profitability. The company targets adjusted EBITDA improvements of 7.5-15% over three years for acquired locations.

The company has secured a new credit facility with CIBC that provides acquisition financing capacity and supports its pharmacist co-ownership loan program. With a strong balance sheet, established acquisition pipeline, and demonstrated ability to improve same-store performance, PharmaCorp appears well-positioned to continue executing its consolidation strategy in the Canadian pharmacy sector.

PharmaCorp’s stock was recently trading at $0.48, up 6.67%, with a 52-week range of $0.40-$0.75, suggesting investor interest in the company’s growth story and strategic positioning within the healthcare sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.