Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Fly Play hf (ICE:PLAY) shares surged 15.63% to $0.44 on August 7, 2025, following the release of the company’s Q2 2025 financial results presentation. The Icelandic low-cost carrier is implementing a significant business model shift toward leisure travel and ACMI (Aircraft, Crew, Maintenance, and Insurance) operations, even as it continues to face financial headwinds with declining revenue and mounting losses.

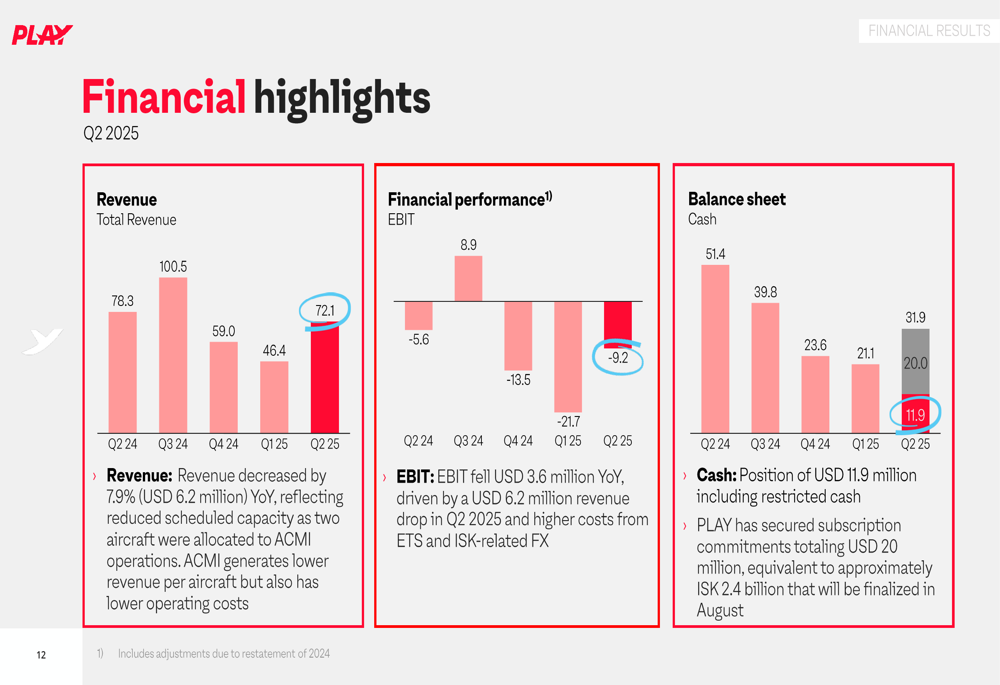

The airline reported a 7.9% year-over-year revenue decline to $72.1 million, while its negative EBIT position worsened to -$9.2 million. Despite these challenges, PLAY secured $20 million in subscription commitments for a convertible bond issuance to bolster its dwindling cash reserves, which stood at $11.9 million at quarter-end, down from $51.4 million a year earlier.

Quarterly Performance Highlights

PLAY’s passenger numbers increased in Q2 2025 to 521,000 compared to 442,000 in the same period last year. The company maintained a healthy load factor of 83.2%, though this represents a 2.7 percentage point decrease year-over-year. On-time performance remained strong at 91.3% for Keflavik operations.

As shown in the following operational overview:

The company’s passenger mix shows a balanced distribution with 39% flying from Iceland, 31% to Iceland, and 29% via Iceland as connecting passengers. This reflects PLAY’s continued focus on its hub-and-spoke model centered on Keflavik airport.

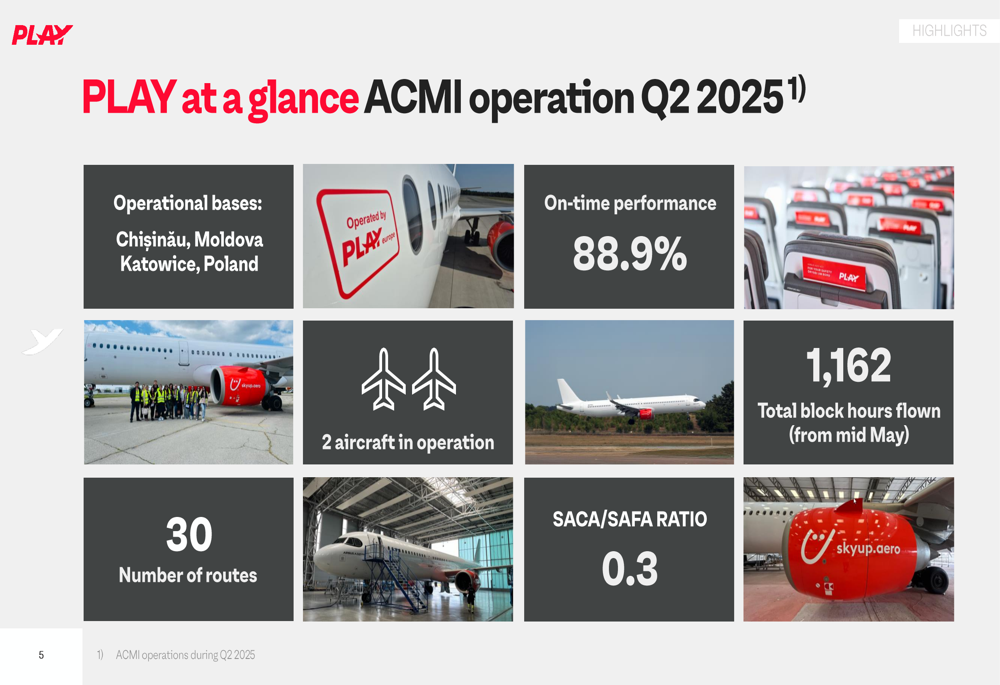

PLAY has also expanded its ACMI operations, now with bases in Chișinău, Moldova, and Katowice, Poland, utilizing two aircraft across 30 routes. These operations contributed $6 million in revenue during the quarter, marking a significant step in the company’s business model diversification.

As illustrated in this ACMI operations summary:

Customer satisfaction has shown remarkable improvement, with the Net Promoter Score (NPS) increasing by 74% year-over-year, from 31 in Q2 2024 to 54 in Q2 2025. This suggests that despite financial challenges, the airline is successfully enhancing its service quality and passenger experience.

Detailed Financial Analysis

PLAY’s financial performance in Q2 2025 presents a mixed picture. While revenue declined 7.9% year-over-year to $72.1 million, the company saw improvements in yield per passenger (up 4.1%) and Total (EPA:TTEF) Revenue per Available Seat Kilometer (TRASK), which increased 2.9% to 5.2 cents.

The following financial snapshot highlights key metrics for the quarter:

However, costs continue to outpace revenue improvements, with Cost per Available Seat Kilometer (CASK) increasing 10.4% year-over-year to 5.95 US cents. This cost increase was primarily driven by a weaker USD, which increased ISK and EUR-denominated costs by 0.28 US cents.

The company’s financial position has deteriorated significantly over the past year, as shown in this comparative financial overview:

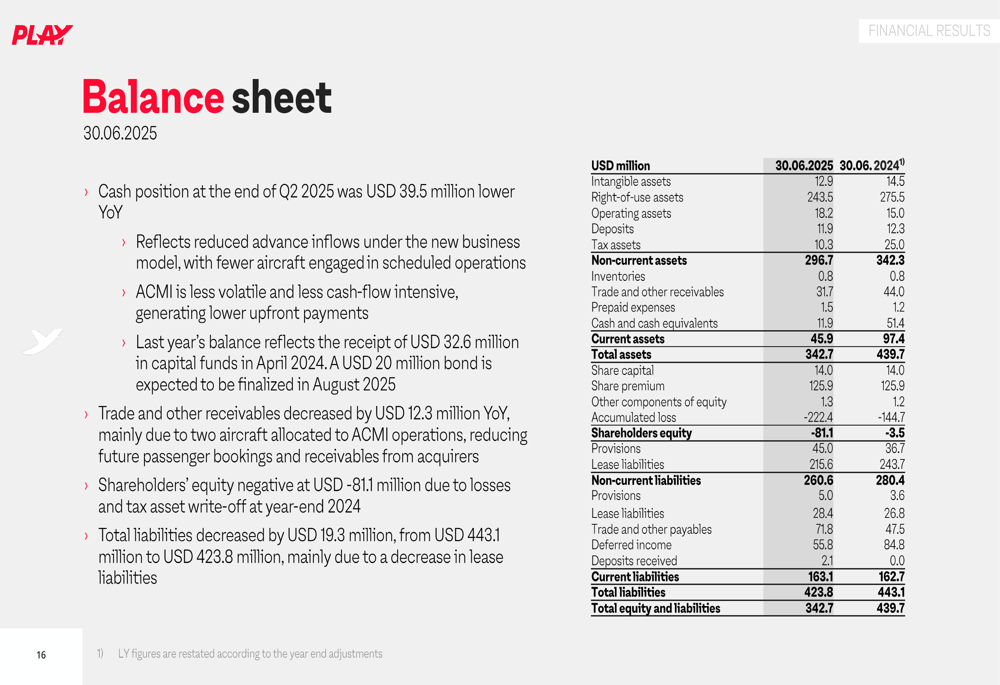

PLAY’s balance sheet reveals concerning trends, with shareholders’ equity now negative at -$81.1 million compared to -$3.5 million a year earlier. Total assets have declined from $439.7 million to $342.7 million year-over-year.

As illustrated in the balance sheet summary:

The cash flow situation remains challenging, with net cash from operations in Q2 2025 amounting to $5.5 million, insufficient to cover lease liabilities of $12.8 million. The company’s cash position declined from $21.1 million in Q1 2025 to $11.9 million at the end of Q2, highlighting the urgent need for the recently announced $20 million convertible bond issuance.

Strategic Initiatives

PLAY is actively pivoting its business model to address financial challenges. The company has increased its focus on leisure destinations, with a 15% increase in leisure capacity compared to Q2 2024. New routes to Antalya, Turkey, and Faro, Portugal, were launched in April 2025, expanding the airline’s presence in popular vacation markets.

A cornerstone of PLAY’s strategic shift is the expansion of ACMI operations. Four of the airline’s ten aircraft are now committed to long-term ACMI damp lease agreements with SkyUp, commencing in May 2025 and running through the end of 2027. This approach aims to ensure stable revenue streams and stronger fleet utilization during off-peak periods.

As shown in this forward-looking strategy overview:

The company has also established a Maltese AOC (Air Operator Certificate), enabling more cost-efficient ACMI operations. This development, combined with labor agreements renewed in line with general market increases, is part of PLAY’s effort to reduce costs and improve operational efficiency.

Forward-Looking Statements

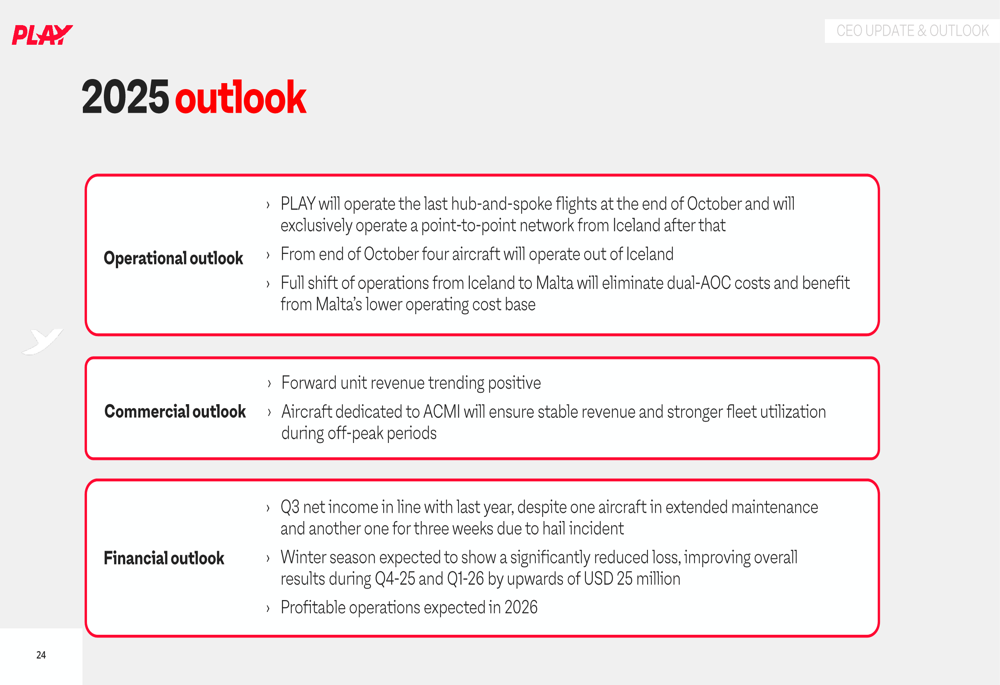

Looking ahead, PLAY expects its new business model to significantly improve financial performance. Management projects that the winter season will show a substantially reduced loss, improving overall results during Q4 2025 and Q1 2026 by upwards of $25 million.

The company’s outlook for the remainder of 2025 is summarized in this forward guidance:

From the end of October, four aircraft will operate out of Iceland, with the remainder dedicated to ACMI operations. This approach is expected to ensure more stable revenue and stronger fleet utilization during traditionally challenging winter months.

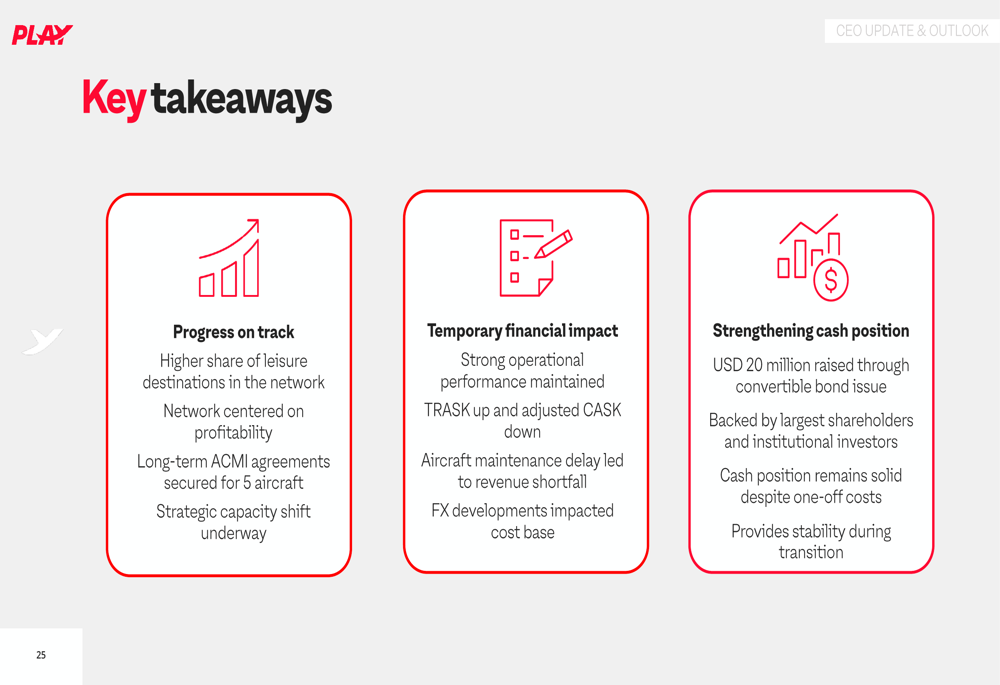

The key takeaways from PLAY’s presentation highlight both progress and challenges:

While PLAY’s strategic pivot shows promise, the company continues to face significant financial hurdles. The recently secured $20 million convertible bond issuance will provide some breathing room, but the negative shareholders’ equity and continuing operational losses underscore the challenges ahead as the airline works to transform its business model and return to profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.