SoFi shares rise as record revenue, member growth drive strong Q3 results

Introduction & Market Context

Plexus Corp (NASDAQ:PLXS) released its fiscal third quarter 2025 presentation on July 23, 2025, highlighting continued revenue growth and achievement of its 6% operating margin target. Despite these positive results, the market reaction was cautious, with the stock experiencing volatility following the announcement. Currently trading at $138.06, Plexus shares remain well below their 52-week high of $172.89 but have recovered from their low of $103.43.

The electronic manufacturing services provider reported progress across all its market sectors, with particular strength in Healthcare/Life Sciences, which contributed $420 million to quarterly revenue. The company’s presentation emphasized improved financial metrics, robust free cash flow, and continued market share gains through its focus on complex products and demanding regulatory environments.

Quarterly Performance Highlights

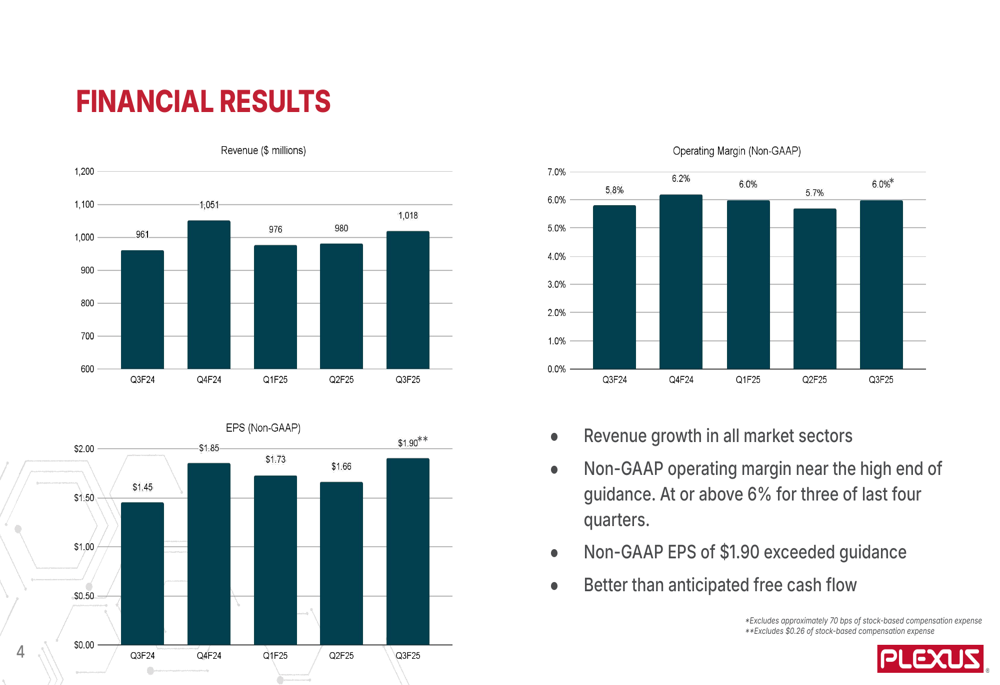

Plexus reported Q3 fiscal 2025 revenue of $1.051 billion, representing sequential growth from $1.018 billion in Q2. The company achieved a non-GAAP operating margin of 6.0%, meeting its stated goal, and delivered non-GAAP EPS of $1.90, which exceeded guidance. These results demonstrate the company’s continued financial strength and operational efficiency.

As shown in the following chart of quarterly financial results, Plexus has maintained consistent revenue growth while achieving its target operating margins:

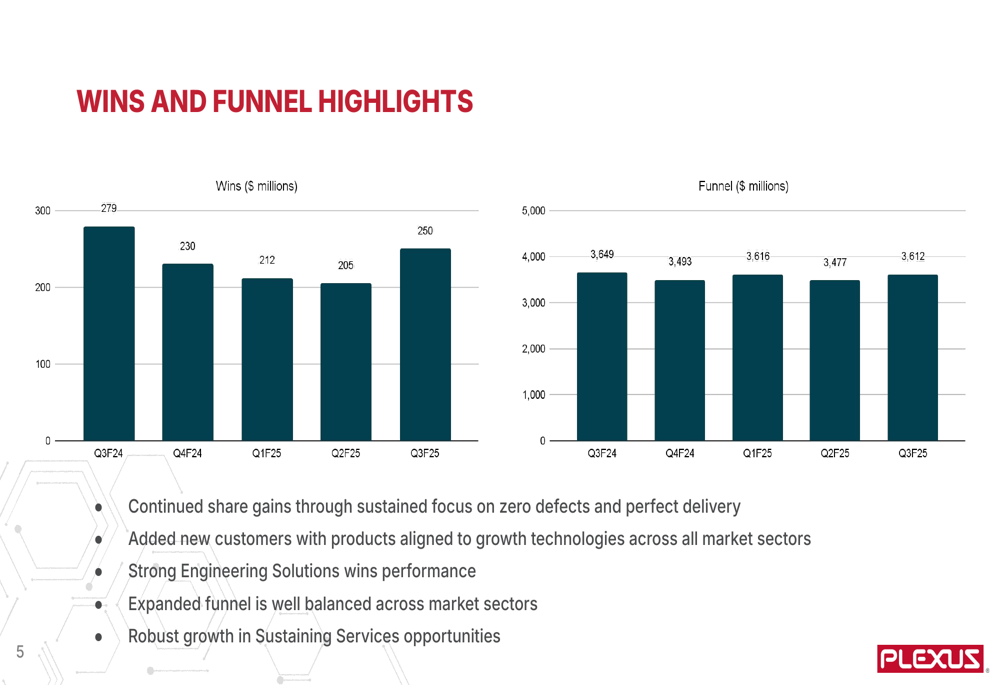

The company’s business development efforts showed positive momentum with $250 million in new program wins during Q3, an increase from $205 million in the previous quarter. The qualified manufacturing funnel remained robust at $3.612 billion, providing a solid foundation for future growth.

The following chart illustrates the company’s wins and funnel performance over recent quarters:

Market Sector Performance

In the Aerospace/Defense sector, Plexus reported Q3 revenue of $183 million, a 6% increase from the previous quarter. The company secured $51 million in new wins, including a new customer supporting satellite networks and broad-based wins in defense and space. Management expects this sector to remain flat in Q4 but projects robust growth in fiscal 2026.

The Healthcare/Life Sciences sector, Plexus’s largest segment, generated $420 million in revenue, a 2% increase from Q2. While Q3 wins decreased to $116 million, the company expanded relationships to support the global launch of new medical device technology and added a new customer in cancer treatment therapy solutions.

The Industrial sector experienced a 4% sequential decline to $415 million, as growth in broadband and energy was offset by semiconductor capital equipment push-outs. However, management expects this sector to return to growth in Q4, benefiting from legacy broadband equipment orders and new program ramps.

Detailed Financial Analysis

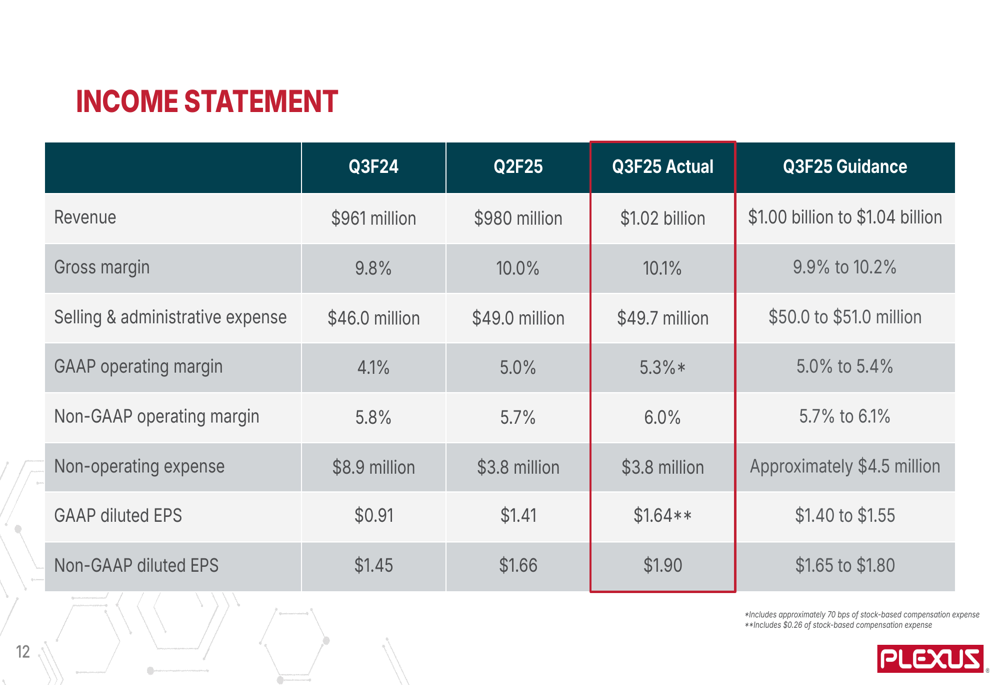

Plexus’s income statement reflects strong operational execution, with gross margin improving to 10.1% in Q3F25 from 10.0% in the previous quarter. The company maintained disciplined expense management with selling and administrative expenses of $49.7 million, slightly below guidance.

The following income statement details the company’s financial performance:

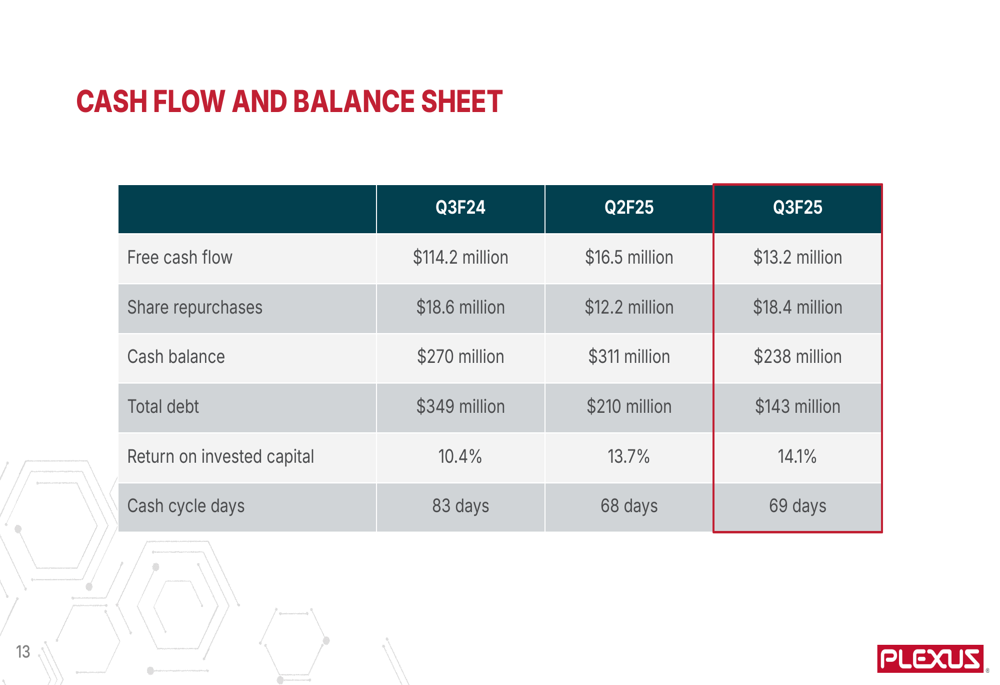

The company’s balance sheet continued to strengthen, with total debt reduced to $143 million in Q3F25 from $349 million in the year-ago period. Cash balance stood at $238 million, and return on invested capital improved to 14.1%, reflecting efficient capital deployment.

The following chart illustrates key cash flow and balance sheet metrics:

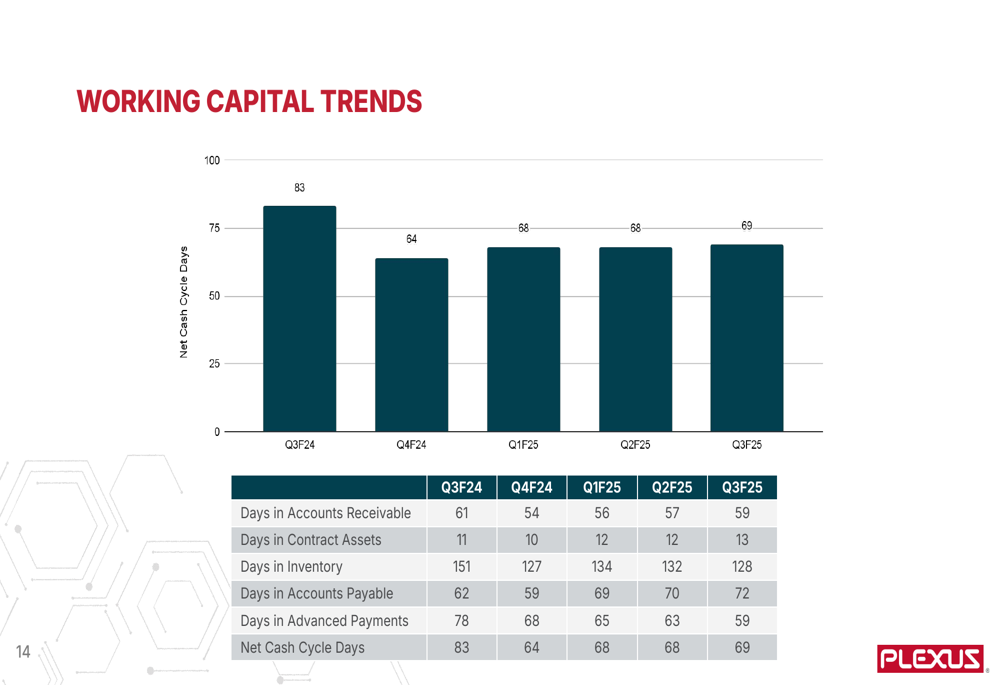

Working capital management remained a focus area, with cash cycle days at 69 days in Q3F25, slightly higher than the 68 days reported in Q2F25 but significantly improved from 83 days in Q3F24. Inventory days continued to decrease, reaching 128 days compared to 151 days a year ago, demonstrating the company’s commitment to operational efficiency.

Sustainability Highlights

Plexus emphasized its commitment to sustainability and corporate responsibility, noting several achievements during the quarter. The company was named one of America’s Greatest Workplaces in Manufacturing 2025 by Newsweek, and its Chicago facility was recognized as a 2025 Best and Brightest Company to Work For at both national and regional levels. Customer satisfaction survey results reached a seven-year high, underscoring the company’s focus on service excellence.

Forward-Looking Statements

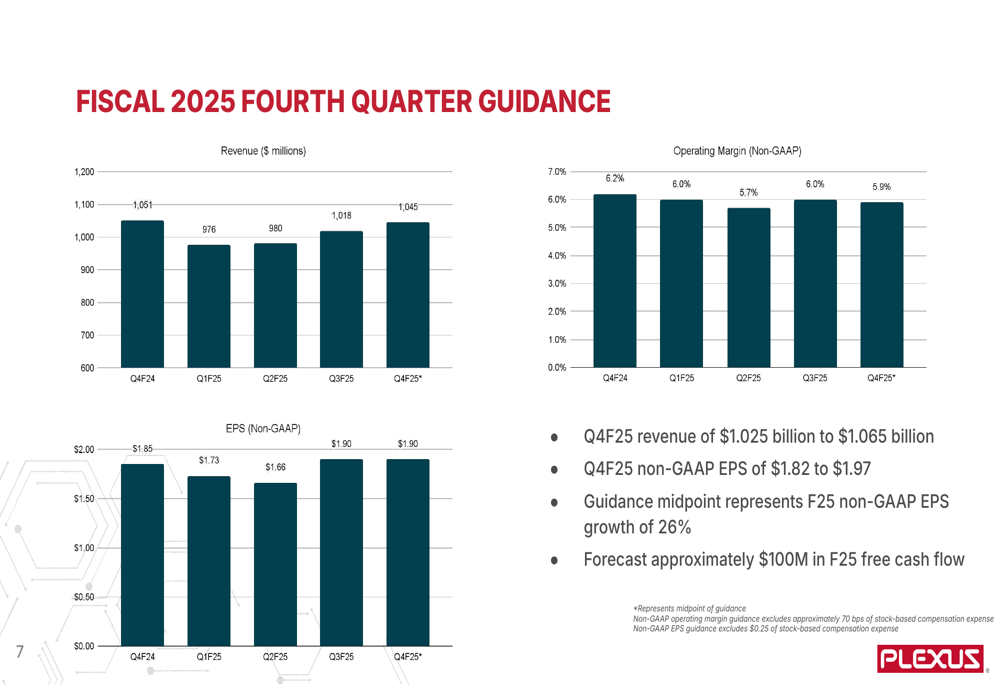

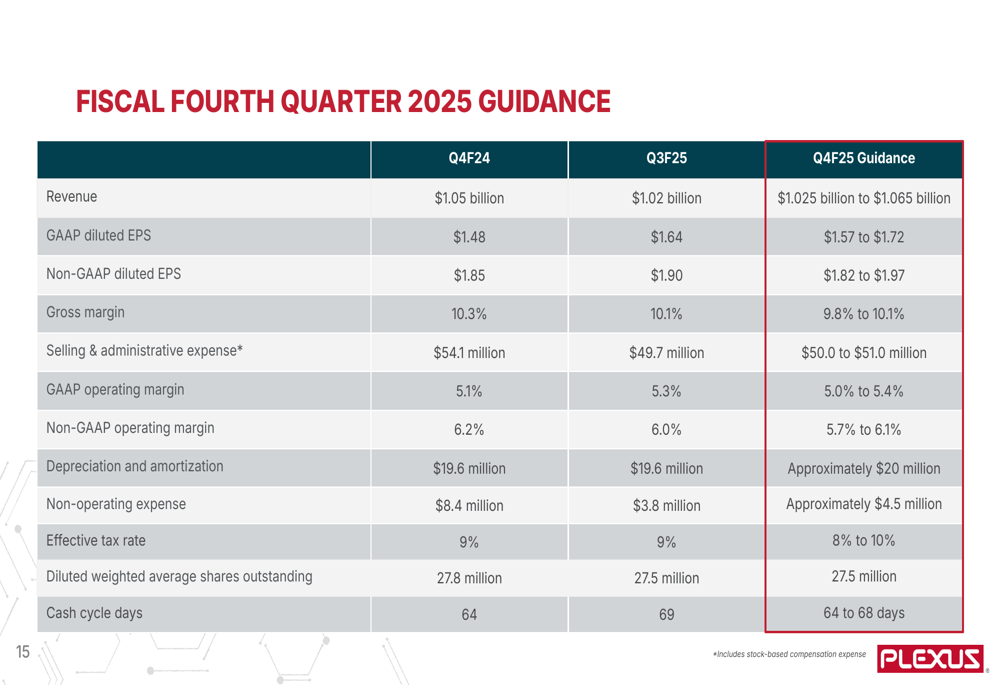

Looking ahead to the fourth quarter of fiscal 2025, Plexus provided guidance for revenue between $1.025 billion and $1.065 billion, with non-GAAP EPS expected to range from $1.82 to $1.97. The company anticipates maintaining strong operating margins, with non-GAAP operating margin guidance of 5.7% to 6.1%.

The following chart details the company’s Q4 fiscal 2025 guidance:

Management forecasts approximately $100 million in free cash flow for fiscal 2025 and expects continued growth across all market sectors in fiscal 2026. The company’s guidance midpoint represents fiscal 2025 non-GAAP EPS growth of 26%, reflecting confidence in its business model and market positioning.

A more detailed breakdown of the Q4 guidance is shown below:

Analyst Perspectives

Despite the positive results presented in the slides, market reaction suggests some investor concerns. According to the earnings call transcript, analysts questioned management about semiconductor capital equipment demand softening and potential tariff impacts, though the company indicated these impacts remain minimal.

The discrepancy between the company’s optimistic outlook and the market’s cautious response highlights the challenges Plexus faces in a complex macroeconomic environment. While the company continues to execute well operationally, investors appear concerned about potential headwinds in certain sectors and the sustainability of growth rates.

Nevertheless, Plexus’s strong financial position, consistent operational execution, and robust pipeline of opportunities position the company well for continued success in the highly complex electronics manufacturing services market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.