Five things to watch in markets in the week ahead

Introduction & Market Context

PNC Financial Services Group (NYSE:PNC) presented its third quarter 2025 earnings on October 15, 2025, reporting strong financial results with record revenue and improved efficiency across business segments. Despite the positive performance, PNC’s stock declined 2.71% during regular trading to $189.73, with a further 5.18% drop to $179.90 in pre-market trading, reflecting investor concerns about the bank’s cautious outlook for the fourth quarter.

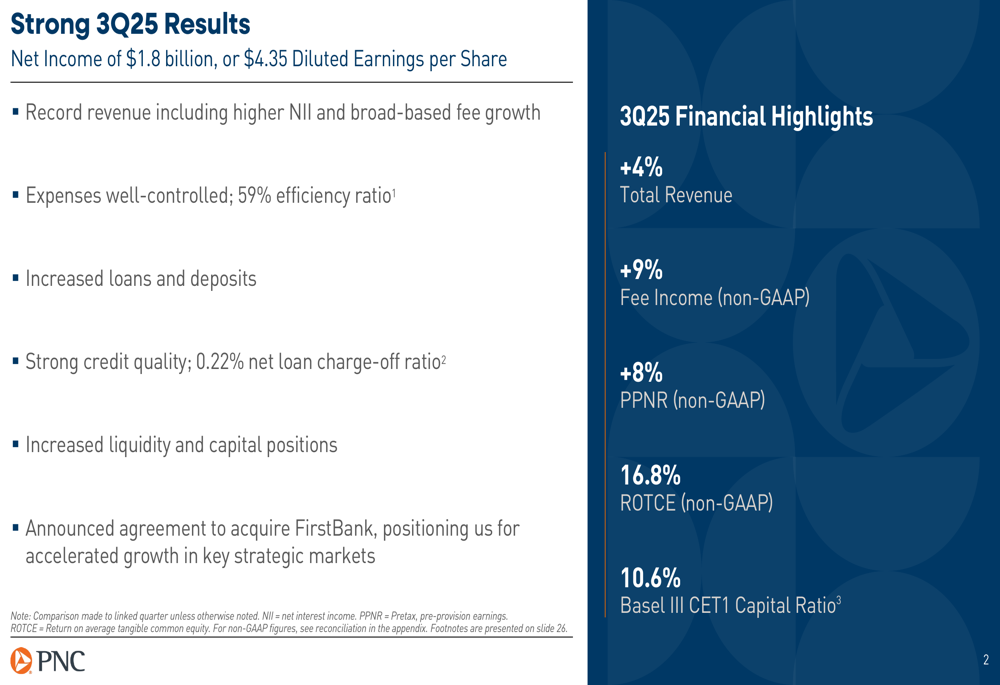

The banking giant reported net income of $1.8 billion, or $4.35 per diluted share, exceeding analyst expectations of $4.04 per share. Total revenue reached a record $5.9 billion, up 4% from the previous quarter and 9% year-over-year, driven by growth in both net interest income and fees.

Quarterly Performance Highlights

PNC delivered strong results across all key financial metrics in the third quarter. The company achieved record revenue of $5.9 billion, with net interest income increasing by 7% year-over-year to $3.65 billion and noninterest income rising by 12% to $2.27 billion. Fee income showed particularly strong growth, up 9% compared to the previous quarter.

As shown in the following chart of PNC’s income statement summary, the company demonstrated strong revenue growth while maintaining disciplined expense management:

The bank’s efficiency ratio improved to 58.5% in Q3 2025, compared to 61.2% in the same quarter last year, reflecting PNC’s ability to generate revenue while controlling costs. Pretax, pre-provision earnings increased by 8% quarter-over-quarter and 17% year-over-year to $2.45 billion.

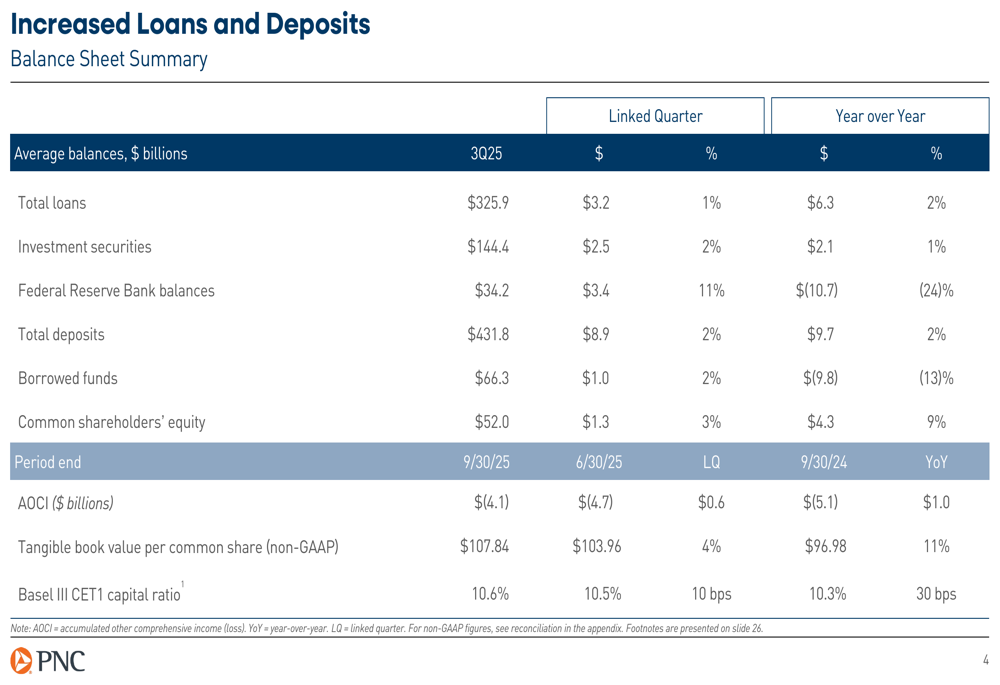

PNC’s balance sheet continued to strengthen, with average loans increasing by 1% from the previous quarter to $325.9 billion and average deposits growing by 2% to $431.8 billion. The company also reported improved capital and liquidity positions, with the Basel III CET1 capital ratio increasing to 10.6%, up 30 basis points year-over-year.

The following balance sheet summary illustrates PNC’s growth in loans, deposits, and capital:

Detailed Financial Analysis

PNC’s loan portfolio growth was primarily driven by Commercial & Industrial (C&I) loans, which increased by $4.4 billion during the quarter, while Commercial Real Estate (CRE) loans decreased by $1.0 billion and consumer loans decreased slightly by $0.2 billion. This shift reflects PNC’s strategic focus on expanding its commercial banking business.

The loan growth dynamics are illustrated in the following chart:

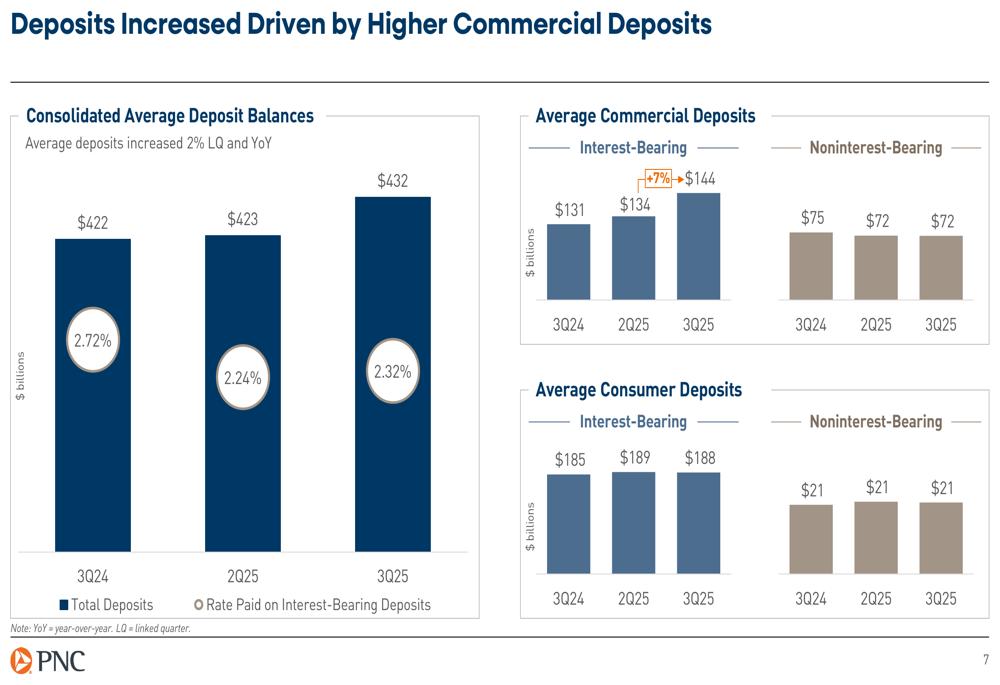

Deposit growth was primarily driven by higher commercial deposits, which increased to $216 billion in Q3 2025, up from $206 billion in Q3 2024. Interest-bearing commercial deposits showed particularly strong growth, increasing from $131 billion to $144 billion year-over-year. Consumer deposits remained relatively stable at $209 billion.

The following chart shows the composition and trends in PNC’s deposit base:

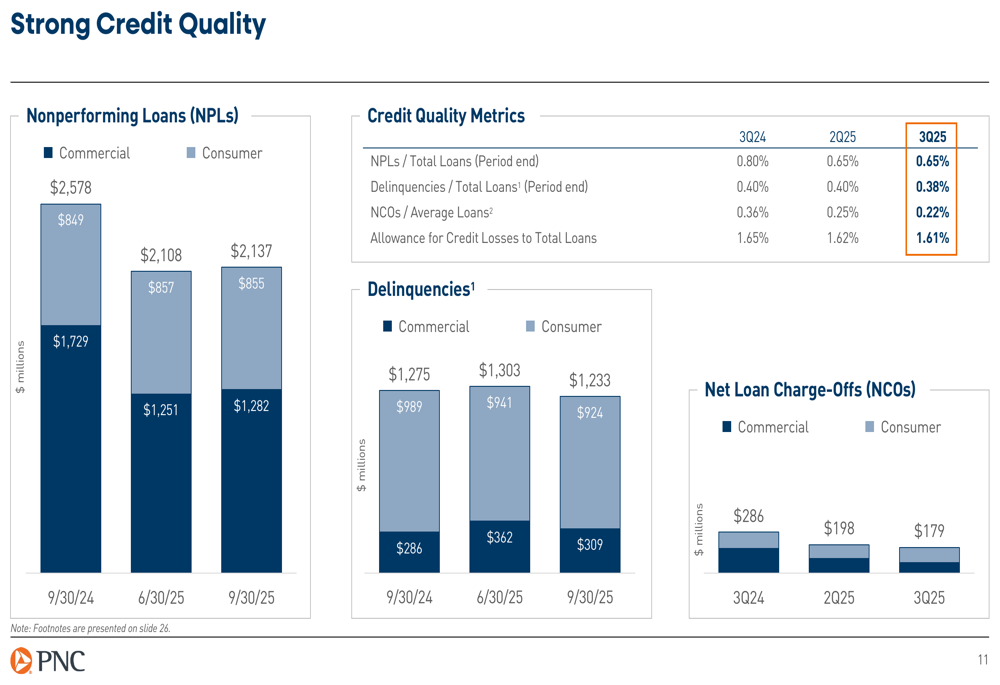

Credit quality remained strong, with nonperforming loans decreasing to 0.65% of total loans from 0.80% a year ago. Net charge-offs declined to 0.22% of average loans, down from 0.36% in Q3 2024 and 0.25% in Q2 2025. This improvement in credit metrics reflects PNC’s disciplined risk management approach and the overall health of its loan portfolio.

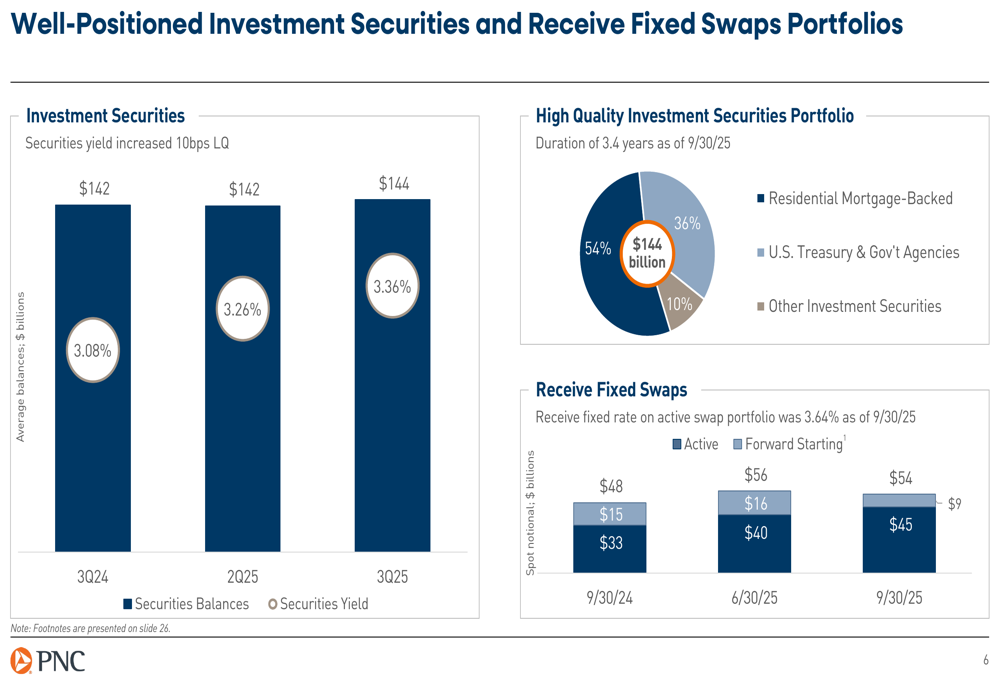

The bank’s investment securities portfolio remained well-positioned, with a yield of 3.36% in Q3 2025, up from 3.08% a year earlier. The portfolio is primarily composed of high-quality securities, with 54% in U.S. Treasury and government agencies and 36% in residential mortgage-backed securities.

Strategic Initiatives & Growth Drivers

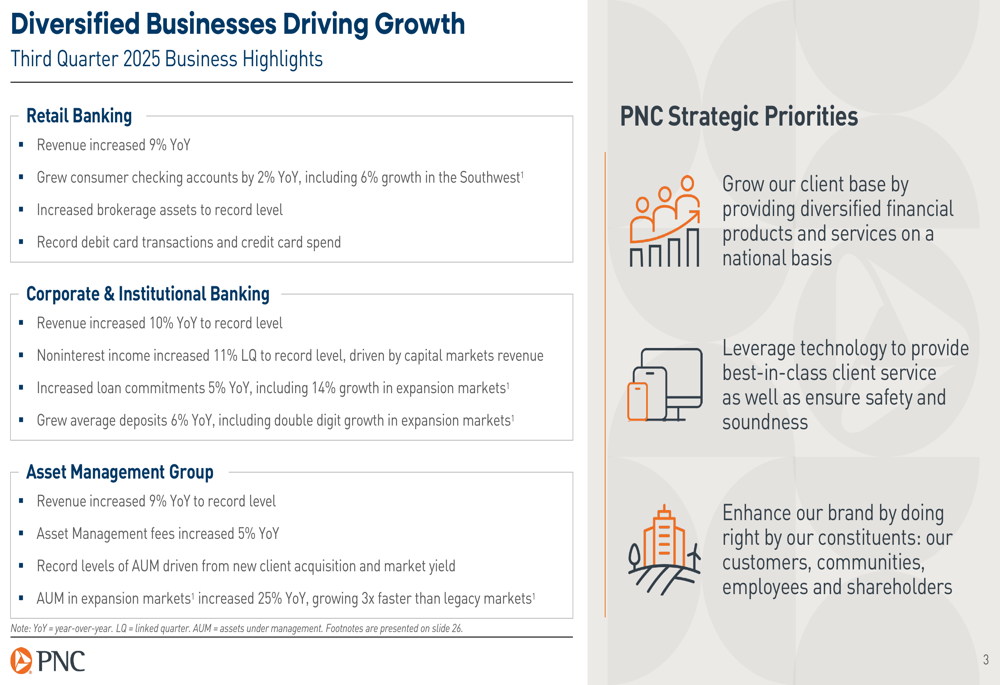

PNC reported strong growth across all business segments, demonstrating the success of its diversified business model. Retail Banking revenue increased by 9% year-over-year, with consumer checking accounts growing by 2% overall and 6% in the Southwest region. Corporate & Institutional Banking revenue rose by 10% to a record level, with loan commitments increasing by 5% year-over-year, including 14% growth in expansion markets. Asset Management Group revenue also grew by 9% to a record level, with assets under management reaching record levels.

The following chart highlights the performance of PNC’s diverse business segments:

The company’s strategic focus on expansion markets is yielding positive results, with double-digit deposit growth in these regions and a 25% year-over-year increase in assets under management. PNC also announced an agreement to acquire FirstBank, which will further enhance its market presence and growth potential.

PNC’s office commercial real estate portfolio has been an area of focus given market concerns about this sector. The bank has managed to reduce its exposure in this area, with net loan charge-offs from office CRE decreasing significantly to $13 million in Q3 2025 from $95 million in Q3 2024.

Forward-Looking Statements

Looking ahead to the fourth quarter of 2025, PNC provided a cautious outlook that may have contributed to the negative stock reaction despite strong Q3 results. The bank expects average loans to be stable to up 1% and net interest income to increase by approximately 1.5%. However, fee income is projected to decrease by approximately 3%, resulting in total revenue being stable to down 1% compared to the third quarter. Noninterest expense is expected to increase by 1% to 2%, and net charge-offs are anticipated to be between $200 million and $225 million.

The following guidance summary outlines PNC’s expectations for Q4 2025:

Despite the cautious near-term outlook, PNC’s management remains confident in the bank’s long-term growth prospects. According to the earnings call, CEO Bill Demchak emphasized the bank’s strategic focus, stating, "We will be comfortably above $1 billion on top of this year for 2026," while CFO Rob Reilly added, "Our NII trajectory is in place," underscoring confidence in the bank’s financial strategy.

PNC’s strong capital position, improved efficiency, and strategic growth initiatives provide a solid foundation for navigating the challenging economic environment ahead. However, investors appear concerned about potential headwinds, including anticipated GDP growth below 2% in 2025, potential regulatory changes, and expected Federal Reserve rate cuts that may affect net interest margins.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.