SoFi shares rise as record revenue, member growth drive strong Q3 results

Introduction & Market Context

Powerfleet Inc. (NASDAQ:PWFL) presented its Q1 FY26 results on August 11, 2025, showcasing strong financial performance and strategic progress in its transformation initiatives. The company, which provides IoT and AI-powered solutions for managing mobile assets, reported significant year-over-year growth in revenue and EBITDA, driven primarily by expanding service revenue.

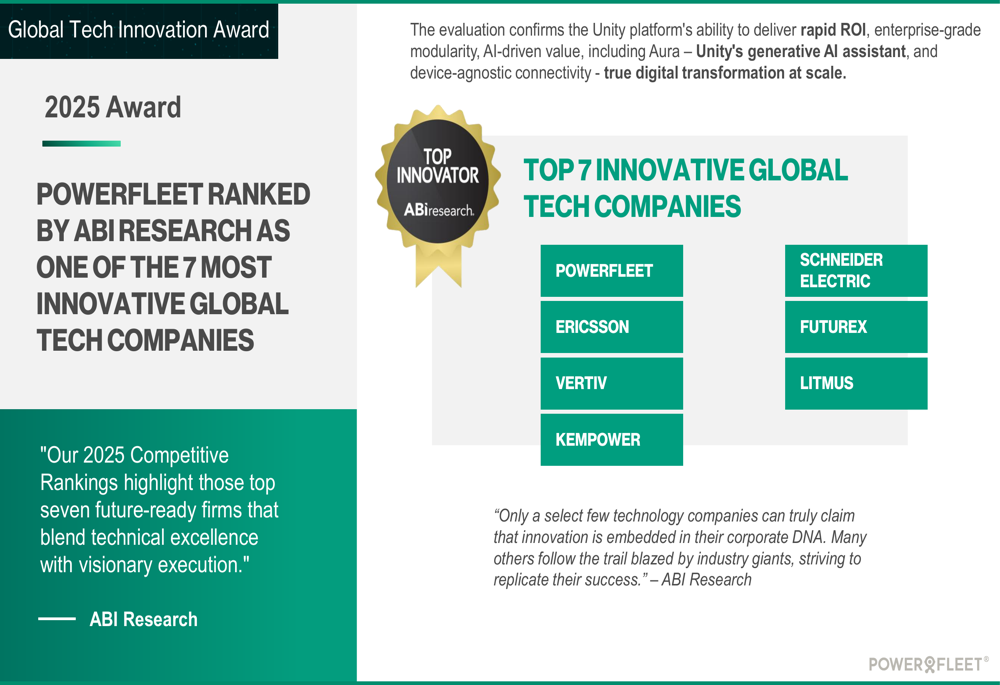

The presentation comes as Powerfleet continues to integrate its recent acquisitions and position itself as a leader in the AI-powered IoT space. The company was recently recognized by ABI Research as one of the seven most innovative global tech companies, alongside industry giants like Ericsson (BS:ERICAs) and Schneider Electric (EPA:SCHN).

As shown in the following recognition from ABI Research:

Quarterly Performance Highlights

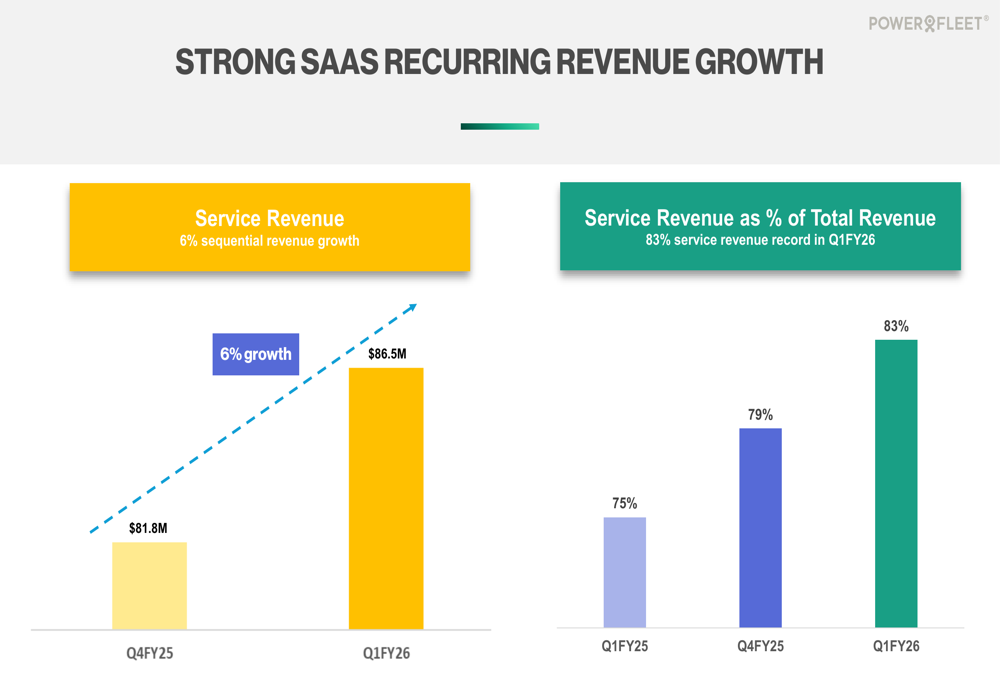

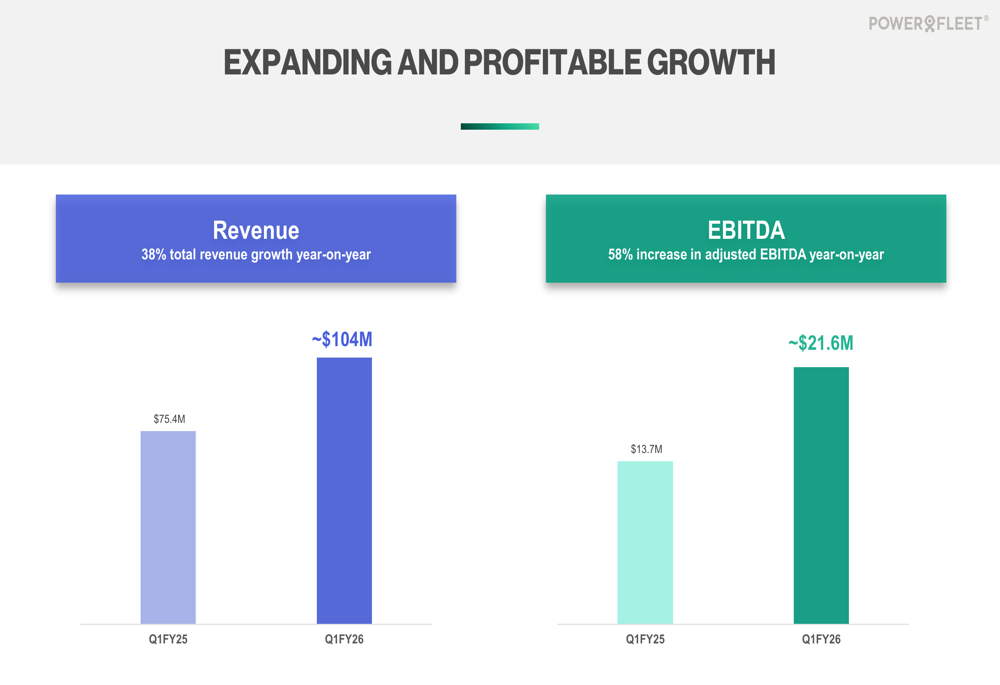

Powerfleet reported total revenue of $104.1 million in Q1 FY26, representing a 38% increase year-over-year. This growth was primarily driven by the company’s service revenue, which grew 6% sequentially and now accounts for 83% of total revenue, reaching a record high for the company.

The company’s adjusted EBITDA showed even stronger growth, increasing 58% year-over-year to $21.6 million. Gross margins also improved, with AEBITDA gross margins reaching 67%, up from 64% in the same period last year. Service gross margins were particularly strong at 76%.

These financial results demonstrate Powerfleet’s successful execution of its strategy to focus on high-margin recurring revenue streams, as illustrated in the following financial summary:

The company’s service revenue growth has been consistent, showing sequential improvement from $81.8 million in Q4 FY25 to $86.5 million in Q1 FY26. The proportion of service revenue to total revenue has also steadily increased from 75% in Q1 FY25 to 83% in Q1 FY26, highlighting the company’s successful transition to a SaaS-focused business model.

This service revenue growth is detailed in the following chart:

The overall revenue and EBITDA growth trends further underscore Powerfleet’s strong financial performance:

Strategic Partnerships and Enterprise Wins

Powerfleet reported significant momentum in its go-to-market strategy, with wins across 11 diverse sectors contributing to marquee deals exceeding $100,000 in annual recurring revenue (ARR). The company saw a 14% sequential increase in new logo wins, adding over 175 B2B customers in the quarter.

Particularly notable was the 52% increase in AI video ARR bookings compared to the previous quarter, driven by indirect channel partners. The company also reported a 24% increase in in-warehouse recurring revenue year-over-year and a 19% increase in ARR pipeline build versus the prior quarter.

These market momentum indicators are summarized in the following slide:

Among the key enterprise wins highlighted in the presentation were deals with several Fortune 500 companies, including a manufacturing leader ($750K+ TCV), an international agriculture company ($700K+ TCV), and companies in logistics, rental and leasing, and food and beverage, each with total contract values exceeding $400,000.

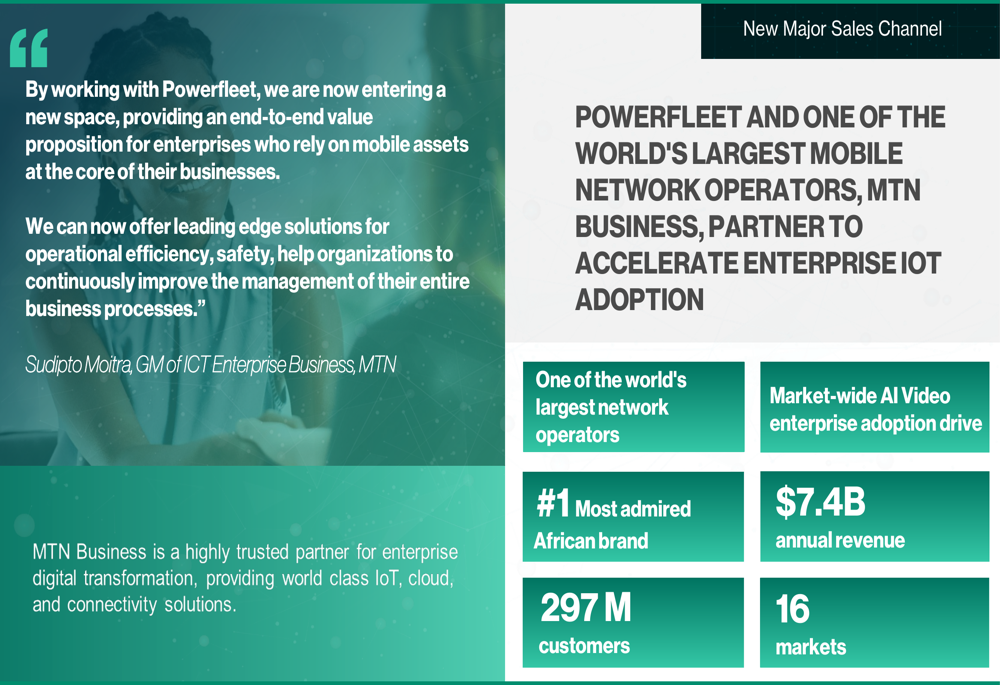

A significant new partnership announced in the quarter was with MTN Business, one of the world’s largest mobile network operators with 297 million customers across 16 markets. This partnership aims to accelerate enterprise IoT adoption, with a particular focus on market-wide AI video enterprise adoption.

The details of this strategic partnership are shown here:

Powerfleet also highlighted customer success stories, including Holcim (SIX:HOLN) Global, which achieved an 83% reduction in critical safety events across approximately 9,000 vehicles in 18 countries using Powerfleet’s Unity platform.

Transformation Initiatives and Cost Savings

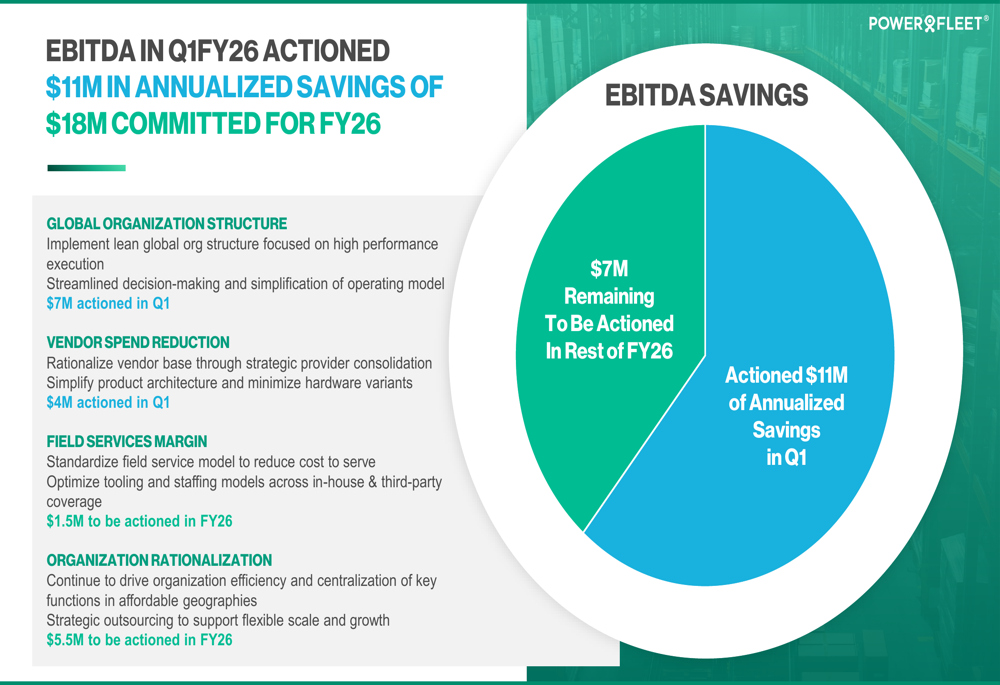

The company reported strong progress in its transformation initiatives during Q1 FY26, with $11 million in annualized EBITDA savings already actioned out of the $18 million committed for the fiscal year. These savings came primarily from implementing a lean global organizational structure ($7 million) and vendor spend reduction ($4 million).

Additional savings are expected from field services margin improvements ($1.5 million) and further organization rationalization ($5.5 million) to be actioned throughout the remainder of FY26.

The breakdown of these cost-saving initiatives is illustrated in the following slide:

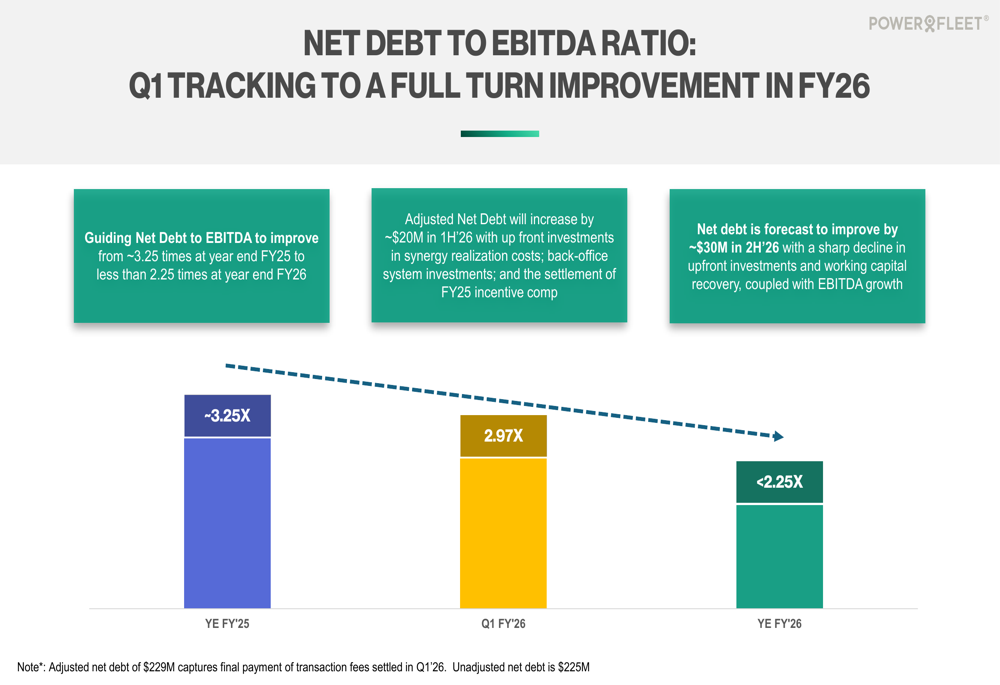

Powerfleet also reported improvement in its debt position, with the net debt to EBITDA ratio improving to 2.97x in Q1 FY26 from 3.17x in the previous quarter. The company is guiding for this ratio to improve to less than 2.25x by the end of FY26, representing a full turn improvement for the fiscal year.

Product Innovation and Forward-Looking Statements

During the quarter, Powerfleet launched a new automated AI risk intervention SaaS module for advanced driver safety. This AI-powered solution claims to reduce fatigue and distraction alerts by 95% and manual video review by 80%, while delivering quantifiable safety gains and lower insurance costs.

The company also announced its upcoming Powerfleet Investor 2025 Unity AloT Innovation Showcase, scheduled for November 2025, where it plans to provide more details on its product roadmap and growth strategy.

Looking forward, Powerfleet appears well-positioned to continue its growth trajectory, with strong momentum in recurring revenue, strategic partnerships, and cost-saving initiatives. The company’s focus on AI-powered solutions and its Unity platform as the key to digital transformation aligns with industry trends toward increased automation and data-driven decision-making.

However, investors should note that while the Q1 FY26 results show strong growth, the company’s previous earnings report for Q2 2025 showed more modest revenue growth of 7% year-over-year, suggesting potential volatility in performance. Additionally, despite strong EBITDA growth, the company reported a net loss of $1.9 million in that previous quarter, highlighting ongoing profitability challenges that may persist.

As Powerfleet continues its transformation journey, the success of its integration efforts, cost-saving initiatives, and ability to maintain its growth momentum will be key factors to watch in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.