Oracle releases AI Database 26ai with built-in artificial intelligence

Introduction & Market Context

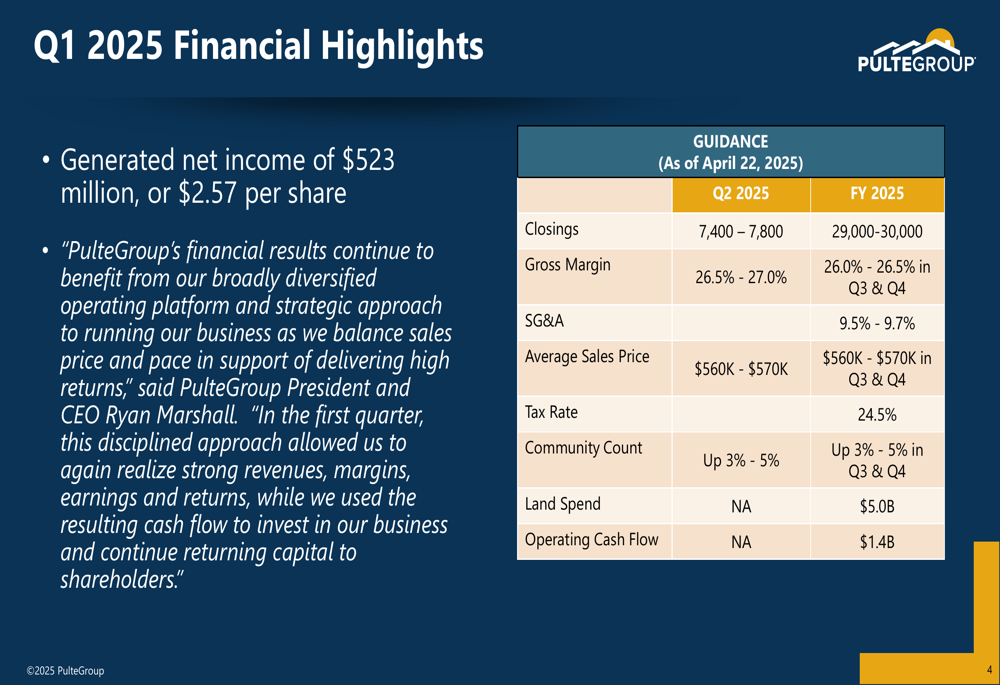

PulteGroup Inc. (NYSE:PHM), the nation’s third-largest homebuilder, reported mixed first-quarter 2025 results on April 22, showcasing resilience in a challenging housing market. The company posted a net income of $523 million, or $2.57 per share, while navigating headwinds that included higher incentives and lower closing volumes.

The homebuilder’s performance reflects broader market dynamics, with rising home prices partially offsetting lower transaction volumes. PulteGroup’s strategic focus on land management and capital allocation appears designed to maintain profitability despite market pressures.

Quarterly Performance Highlights

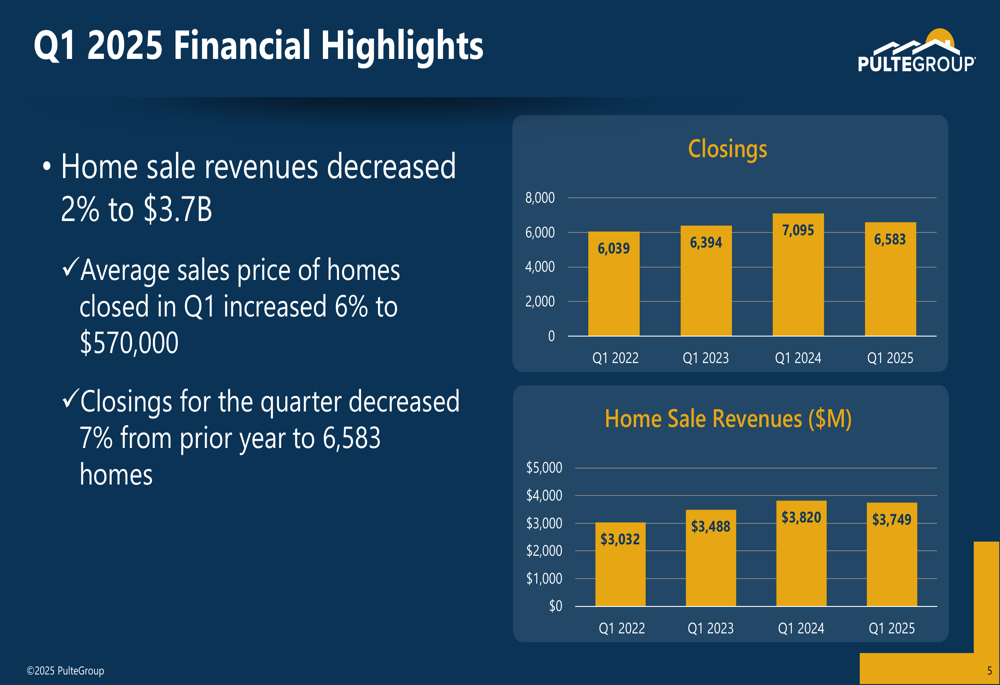

PulteGroup reported home sale revenues of $3.7 billion for Q1 2025, representing a 2% decrease from the prior year. This decline was driven by a 7% reduction in closings to 6,583 homes, partially offset by a 6% increase in average sales price to $570,000.

As shown in the following chart of home sale revenues and closings:

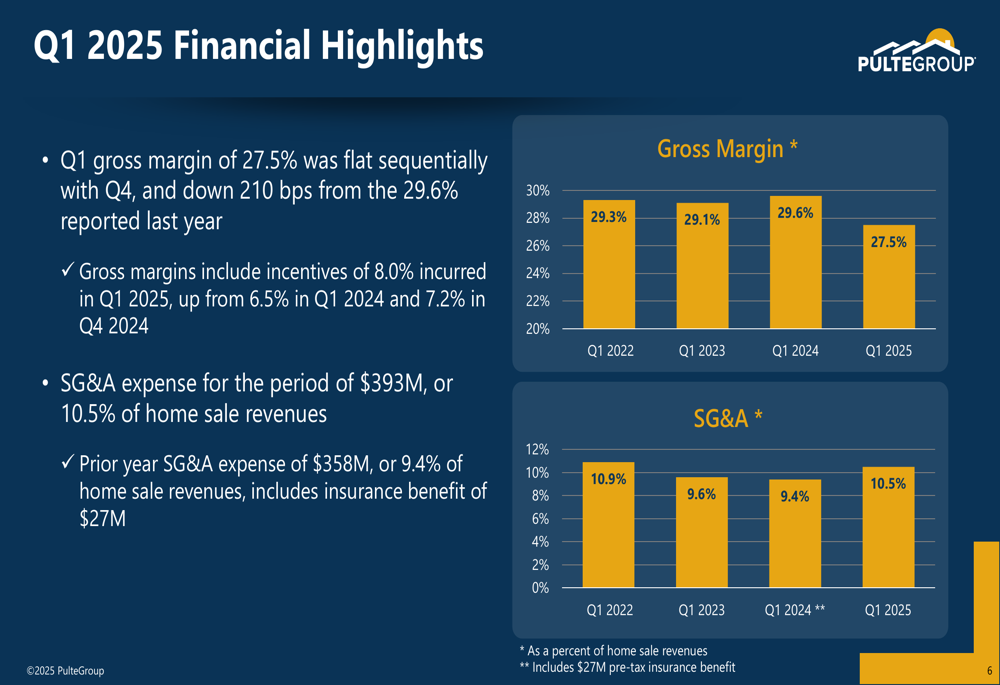

Gross margin declined to 27.5% in Q1 2025, down 210 basis points from 29.6% in the same period last year. The company noted that incentives increased to 8.0% in Q1 2025, up from 6.5% in Q1 2024 and 7.2% in Q4 2024, reflecting more competitive market conditions. Meanwhile, SG&A expenses rose to 10.5% of home sale revenues, compared to 9.4% in the prior year.

The following chart illustrates the trends in gross margin and SG&A:

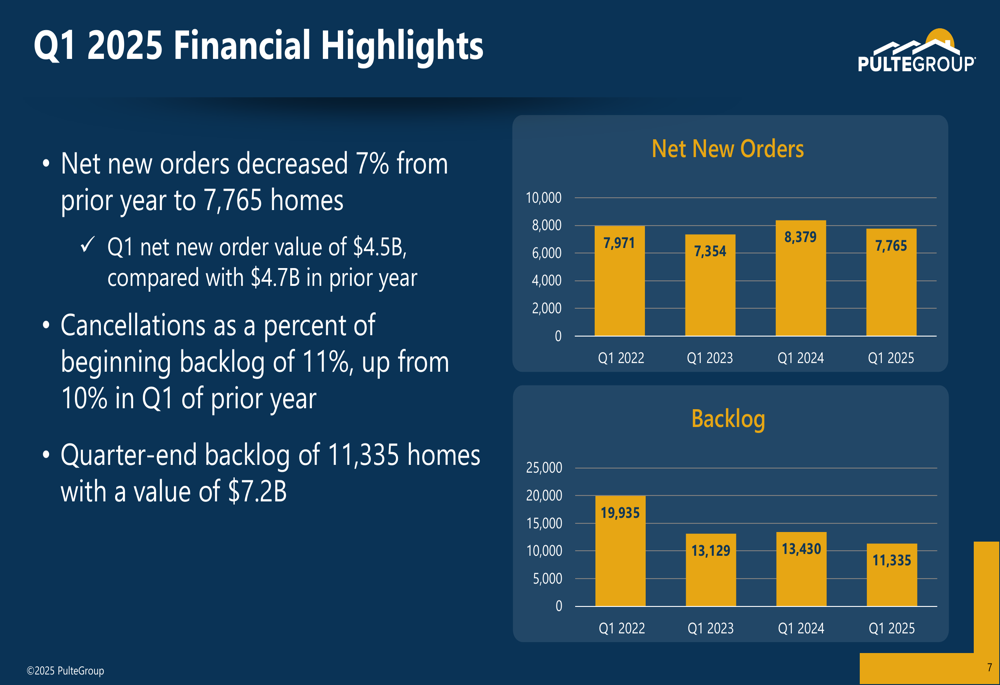

Net new orders decreased by 7% year-over-year to 7,765 homes, with a total value of $4.5 billion compared to $4.7 billion in the prior year. The company’s quarter-end backlog stood at 11,335 homes valued at $7.2 billion, representing year-over-year declines of 16% in units and 12% in value.

The following chart shows the trends in net new orders and backlog:

Land Strategy and Capital Allocation

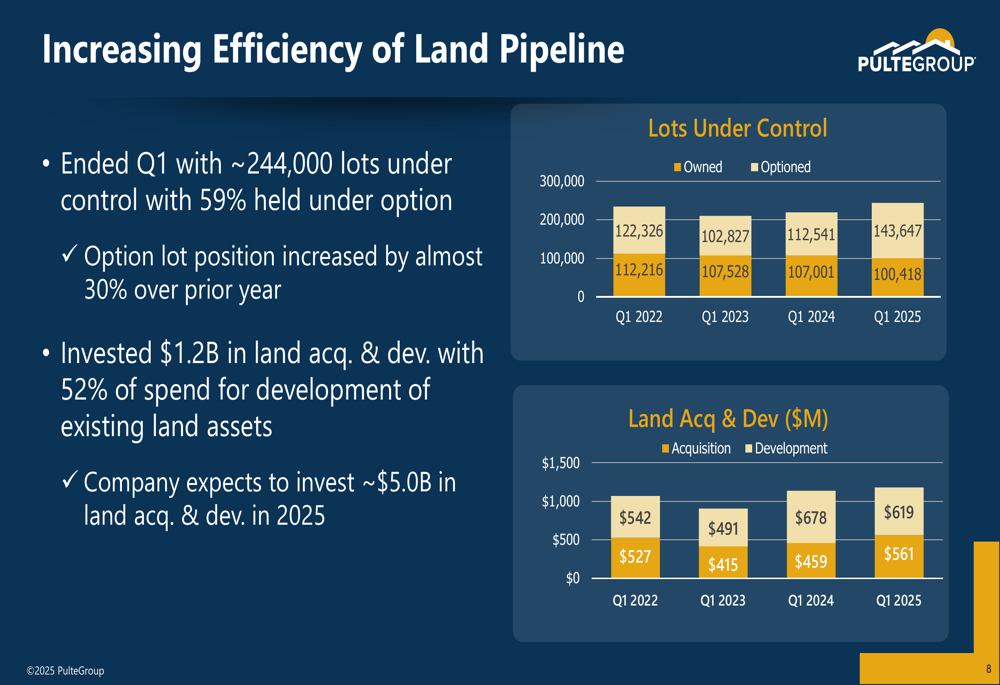

A key focus of PulteGroup’s strategy is optimizing its land pipeline. The company ended Q1 with approximately 244,000 lots under control, with 59% held under option – an increase of almost 30% over the prior year. This shift toward optioned land provides greater flexibility while reducing capital intensity.

The company invested $1.2 billion in land acquisition and development during the quarter, with 52% dedicated to developing existing land assets. For the full year 2025, PulteGroup expects to invest approximately $5.0 billion in land acquisition and development.

As shown in the following chart of the company’s land pipeline efficiency:

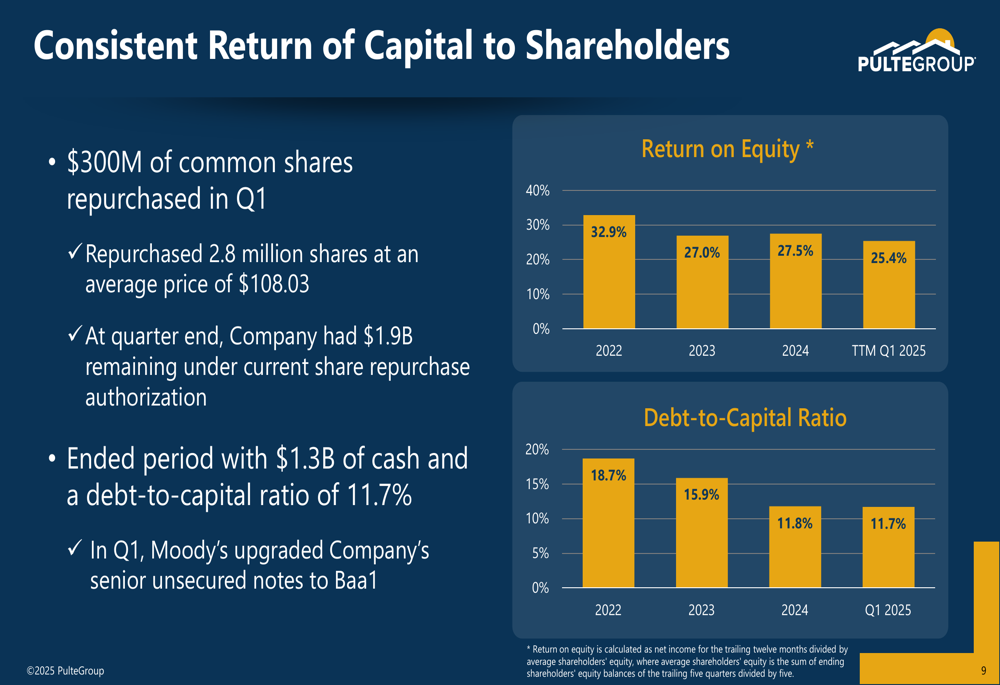

PulteGroup continued its robust capital return program, repurchasing $300 million of common shares in Q1 2025. The company bought back 2.8 million shares at an average price of $108.03 and ended the quarter with $1.9 billion remaining under its current share repurchase authorization.

The company’s financial position remains strong with $1.3 billion of cash and a debt-to-capital ratio of 11.7%. In Q1, Moody’s upgraded the company’s senior unsecured notes to Baa1, reflecting its improved financial profile.

The following chart illustrates the company’s consistent return of capital to shareholders:

Forward Guidance

For Q2 2025, PulteGroup provided the following guidance:

- Closings: 7,400-7,800

- Gross margin: 26.5%-27.0%

- SG&A: 9.5%-9.7%

- Average sales price: $560,000-$570,000

For the full year 2025, the company expects:

- Closings: 29,000-30,000

- Gross margin: 26.0%-26.5% in Q3 & Q4

- Community count growth: 3%-5% over prior year

- Land spend: $5.0 billion

- Operating cash flow: $1.4 billion

As shown in the following comprehensive financial highlights and guidance summary:

Strategic Positioning

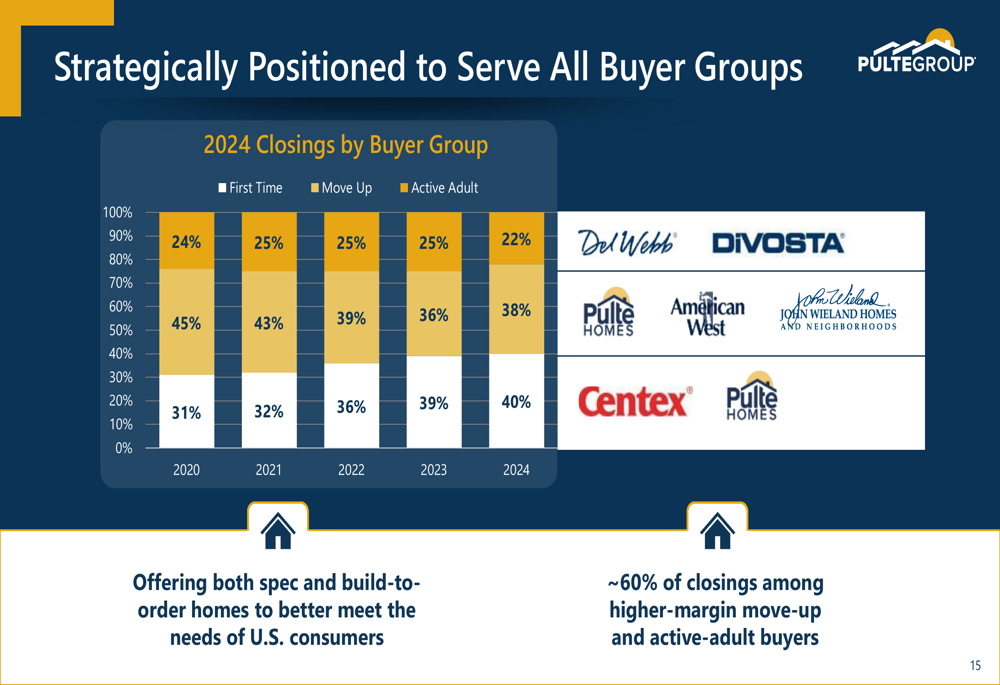

PulteGroup maintains a diversified business model serving various buyer segments and price points. The company’s 2024 closings were distributed across buyer groups with 22% first-time buyers, 40% move-up buyers, and 38% active adult buyers. This strategic positioning allows the company to adapt to shifting market demands.

The following chart illustrates the company’s positioning across buyer segments:

PulteGroup’s operating model, launched a decade ago, focuses on return-driven capital allocation, efficient land pipeline management, and consistent cash flow generation. The company aims to increase its lot option percentage to 70%, further enhancing capital efficiency while maintaining strong margins.

The company claims to have achieved superior total shareholder returns compared to competitors over multiple time horizons, positioning itself as a leader in the homebuilding sector despite current market challenges.

Looking ahead, PulteGroup’s long-term investment thesis includes growing volumes by 5-10% annually while maintaining high returns on equity and a strong balance sheet. The company plans to continue generating positive cash flows to fund its capital allocation priorities, including business investment, dividends, share repurchases, and opportunistic debt reduction.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.