BigBear.ai appoints Sean Ricker as chief financial officer

Introduction & Market Context

PulteGroup Inc. (NYSE:PHM) presented its second quarter 2025 financial results on July 22, showing a 4% decline in revenue amid a cooling housing market. The nation’s third-largest homebuilder reported that despite market headwinds, it maintained disciplined business practices and continued its share repurchase program. The stock was up 3.08% in premarket trading following the presentation, indicating investor confidence despite the mixed results.

The company’s performance reflects broader challenges in the housing sector, where higher incentives are being used to maintain sales velocity in an environment of persistent affordability concerns. Despite these challenges, PulteGroup maintained a strong balance sheet with improving debt metrics and continued to execute its land strategy focused on optioning rather than ownership.

Quarterly Performance Highlights

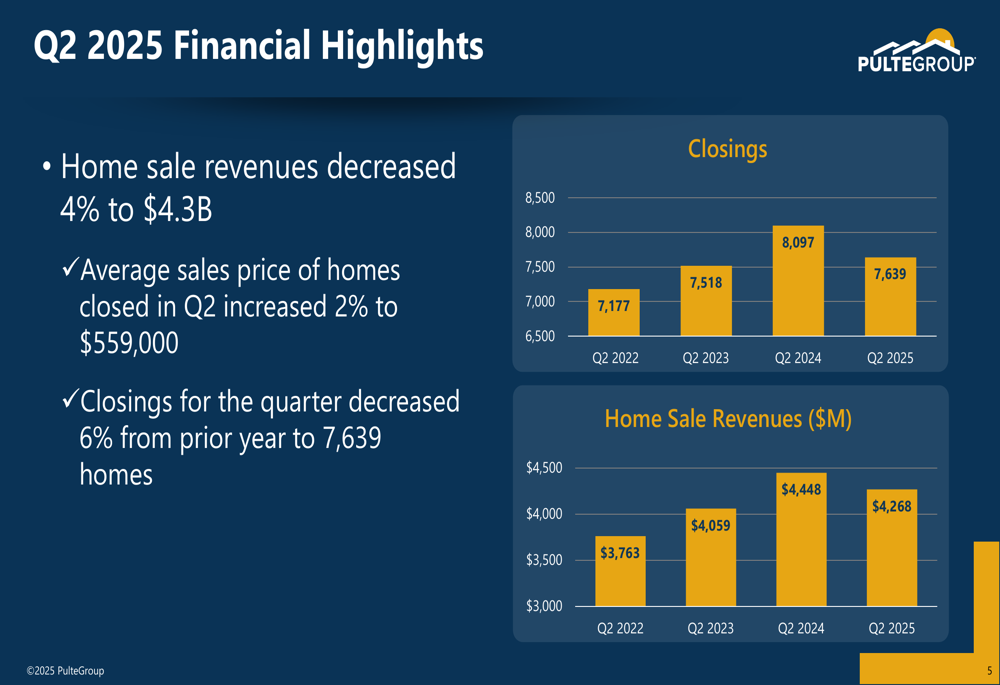

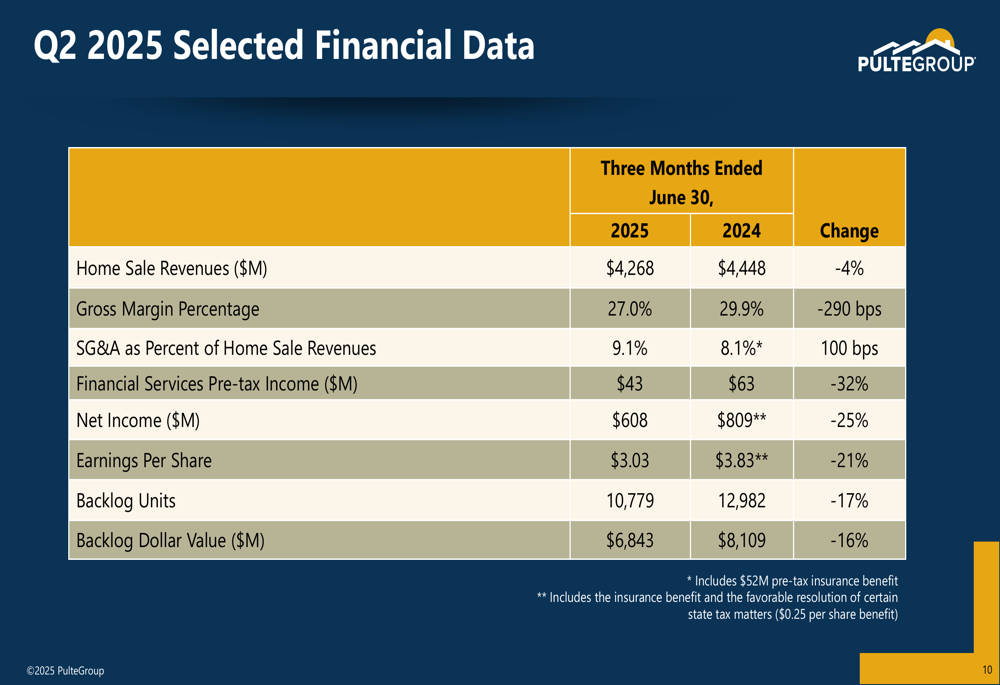

PulteGroup generated net income of $608 million, or $3.03 per share, in the second quarter of 2025. This represents a 25% decrease from the $809 million reported in Q2 2024. Home sale revenues decreased 4% to $4.3 billion, while closings for the quarter declined 6% to 7,639 homes compared to the prior year.

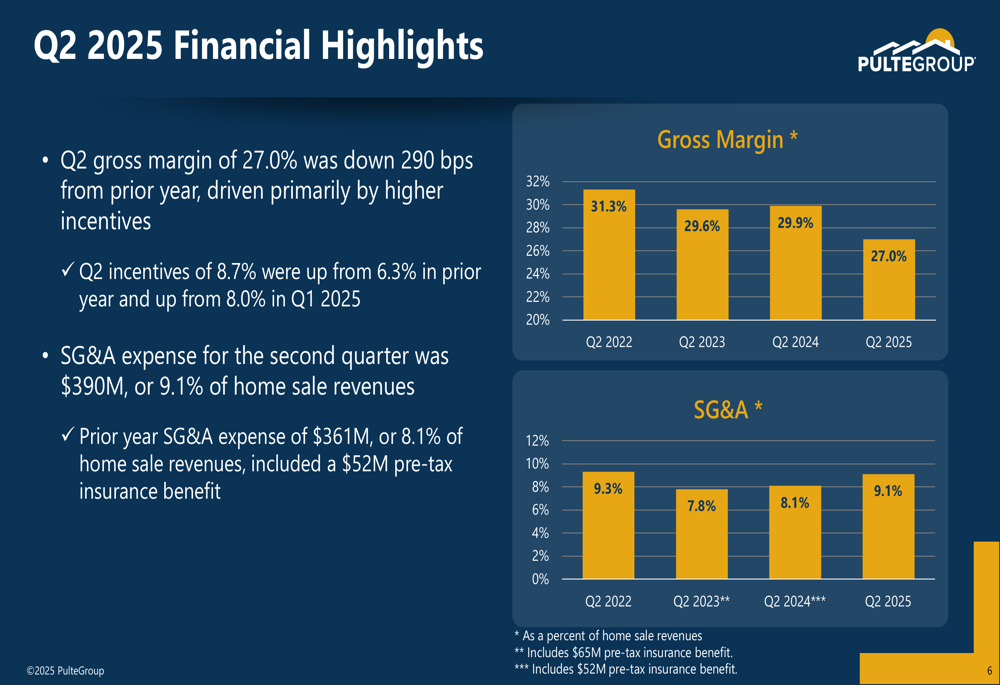

The company’s average sales price increased modestly by 2% to $559,000, helping to partially offset the impact of lower closing volume. However, gross margins compressed significantly, falling 290 basis points year-over-year to 27.0%, primarily due to higher incentives, which rose to 8.7% from 6.3% in the prior year.

As shown in the following chart of quarterly closings and home sale revenues:

SG&A expenses as a percentage of home sale revenues increased to 9.1%, up from 8.1% in the prior year, reflecting the impact of lower revenue on the company’s cost structure. This trend in margins and expenses is illustrated in the following chart:

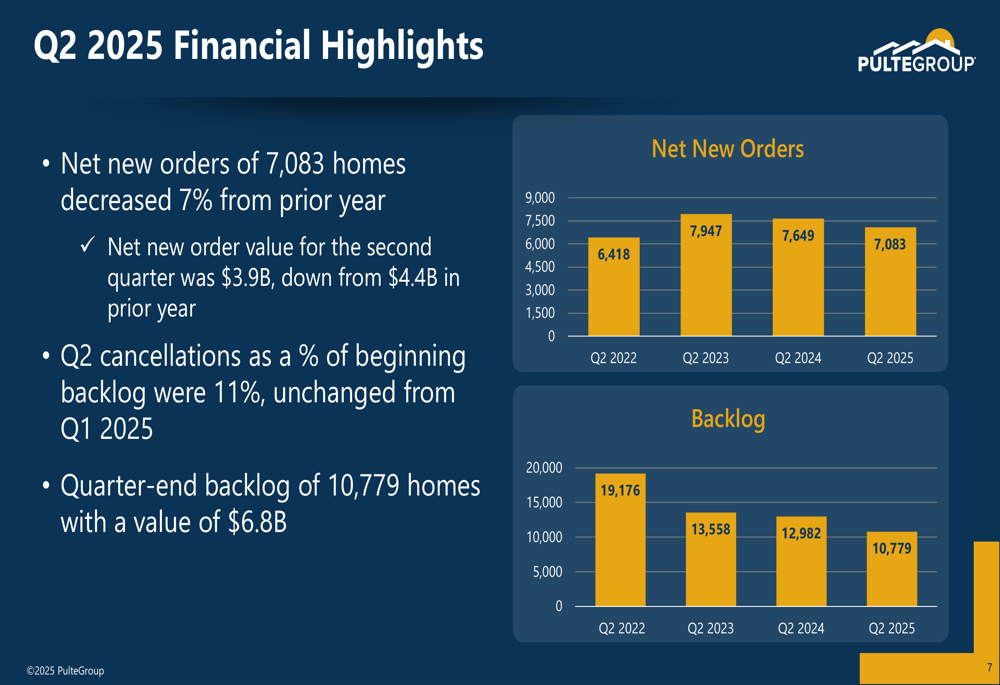

Net new orders of 7,083 homes decreased 7% from the prior year, with order value declining to $3.9 billion from $4.4 billion. The company’s backlog at quarter-end stood at 10,779 homes with a value of $6.8 billion, representing year-over-year declines of 17% and 16%, respectively.

The following chart shows the trends in net new orders and backlog:

Land Strategy and Capital Allocation

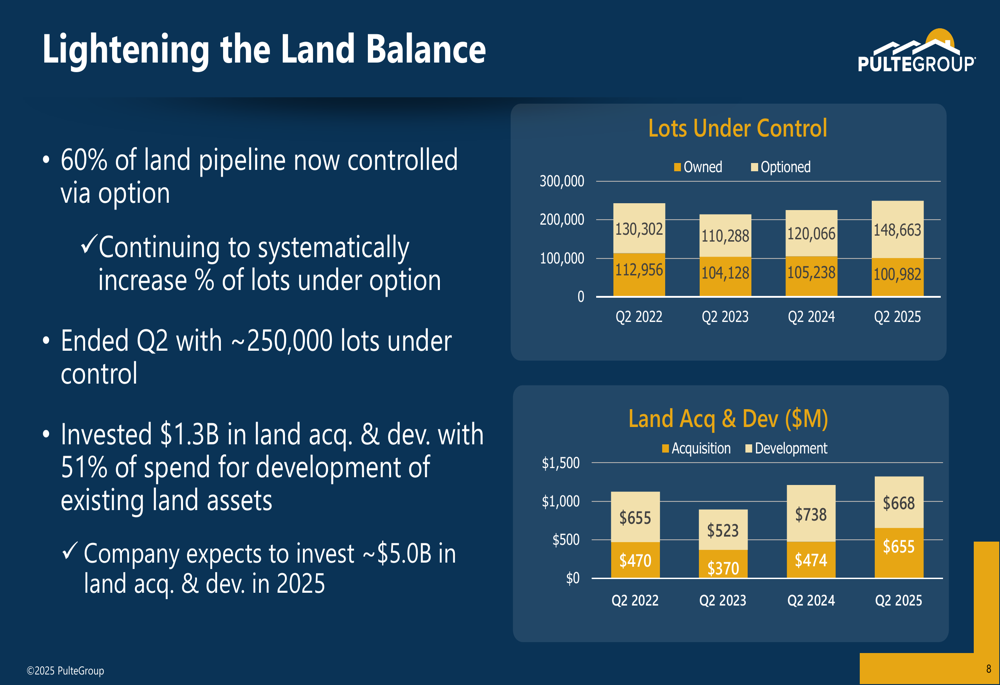

PulteGroup continues to execute its strategy of "lightening the land balance," with 60% of its land pipeline now controlled via option rather than outright ownership. This approach is designed to reduce capital intensity and risk while improving returns on invested capital.

The company ended Q2 with approximately 250,000 lots under control and invested $1.3 billion in land acquisition and development during the quarter, with 51% of spending directed toward the development of existing land assets. For the full year 2025, PulteGroup expects to invest approximately $5.0 billion in land acquisition and development.

The following chart illustrates the company’s progress in shifting toward optioned lots:

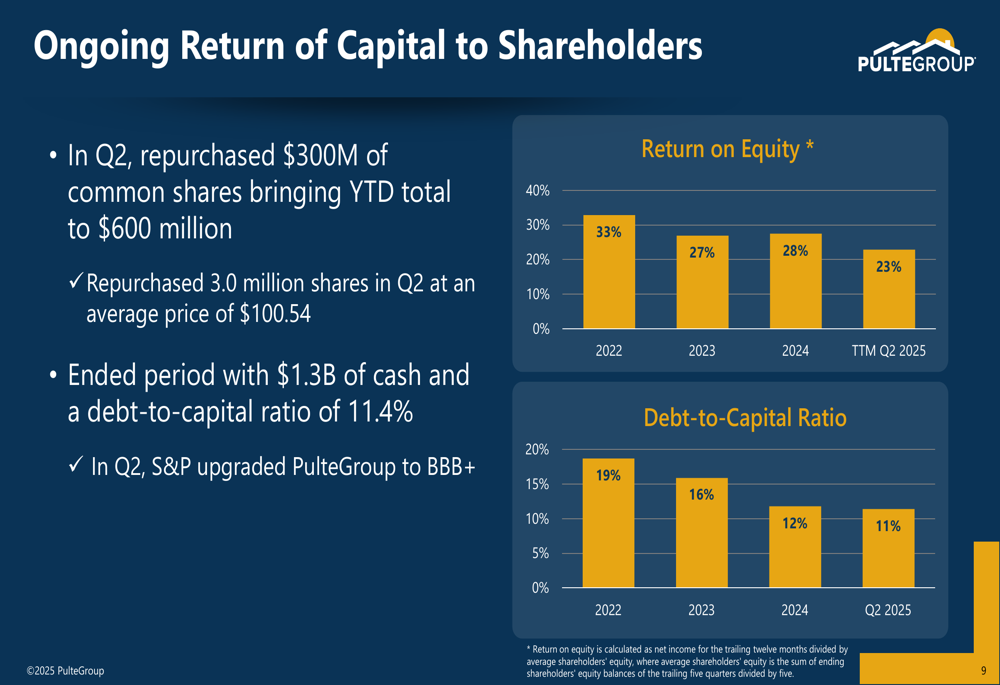

Despite the challenging market conditions, PulteGroup maintained its commitment to returning capital to shareholders. In Q2, the company repurchased $300 million of common shares at an average price of $100.54, bringing the year-to-date total to $600 million. The company ended the period with $1.3 billion of cash and a debt-to-capital ratio of 11.4%, down from 11.8% at the end of 2024.

This financial strength was recognized by S&P, which upgraded PulteGroup to BBB+ during the quarter. The company’s return on equity stood at 23% for the trailing twelve months, though this represents a decline from 28% in 2024.

The following chart shows the company’s return on equity and debt-to-capital ratio trends:

Forward Guidance

Looking ahead, PulteGroup provided guidance for the remainder of 2025. For the third quarter, the company expects closings of 7,200-7,600 homes with an average sales price of $560,000-$570,000 and gross margins of 26.0%-26.5%.

For the full year 2025, PulteGroup anticipates:

- 29,000 home closings

- Gross margins of 26.0%-26.5% in Q4

- SG&A of 9.5%-9.7%

- Average sales price of $560,000-$570,000 in Q4

- Tax rate of 24.5%

- Community count growth of 3%-5%

- Land spend of $5.0 billion

- Operating cash flow of $1.4 billion

This guidance suggests that the company expects margin pressure to continue in the second half of the year, with gross margins projected to be below the 27.0% achieved in Q2.

The following table provides a comprehensive summary of PulteGroup’s Q2 2025 financial performance compared to the prior year:

Strategic Positioning

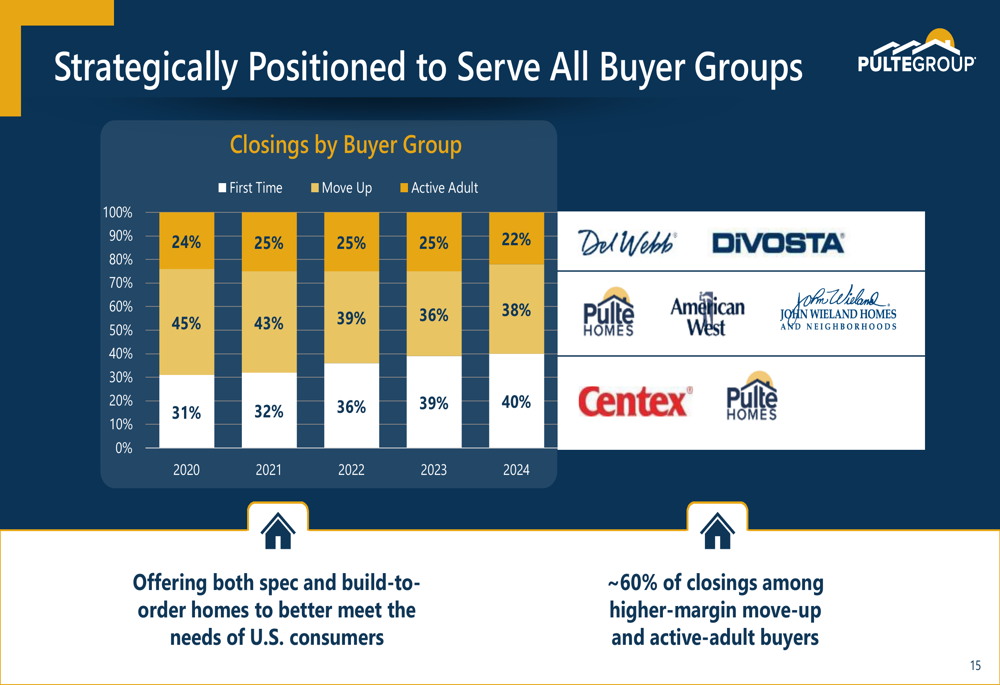

PulteGroup continues to leverage its national operating platform and diversified product offerings to serve all buyer groups. The company’s strategic positioning across different buyer segments has evolved over time, with a current mix of 38% first-time buyers, 40% move-up buyers, and 22% active adult buyers.

The following chart illustrates this strategic positioning across buyer groups:

The company is also well-diversified across price points, with 37% of its business in the $500,000-$749,000 range and 22% in the $750,000 and above segment. This diversification helps PulteGroup navigate market cycles and respond to shifts in demand.

PulteGroup’s long-term investment thesis remains focused on:

1. Growing volumes 5%-10% annually

2. Maintaining high returns on equity

3. Building long-term shareholder value while maintaining a strong balance sheet

4. Driving positive cash flows to fund capital allocation priorities

Despite the current market challenges, the company’s disciplined approach to land investment, focus on capital efficiency, and strong balance sheet position it to navigate the housing cycle while continuing to deliver returns to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.