Street Calls of the Week

Introduction & Market Context

Quaker Chemical Corporation (NYSE:KWR) presented its first quarter 2025 financial results on May 2, showing continued challenges amid soft end market conditions. The specialty chemicals manufacturer reported declining metrics across key financial indicators, while highlighting strategic acquisitions to strengthen its portfolio.

The presentation comes as Quaker Chemical’s stock trades near its 52-week low of $95.91, closing at $106.01 on May 1, 2025, significantly below its 52-week high of $197.03. This follows a mixed performance in Q4 2024, when the company missed EPS forecasts but exceeded revenue expectations.

Quarterly Performance Highlights

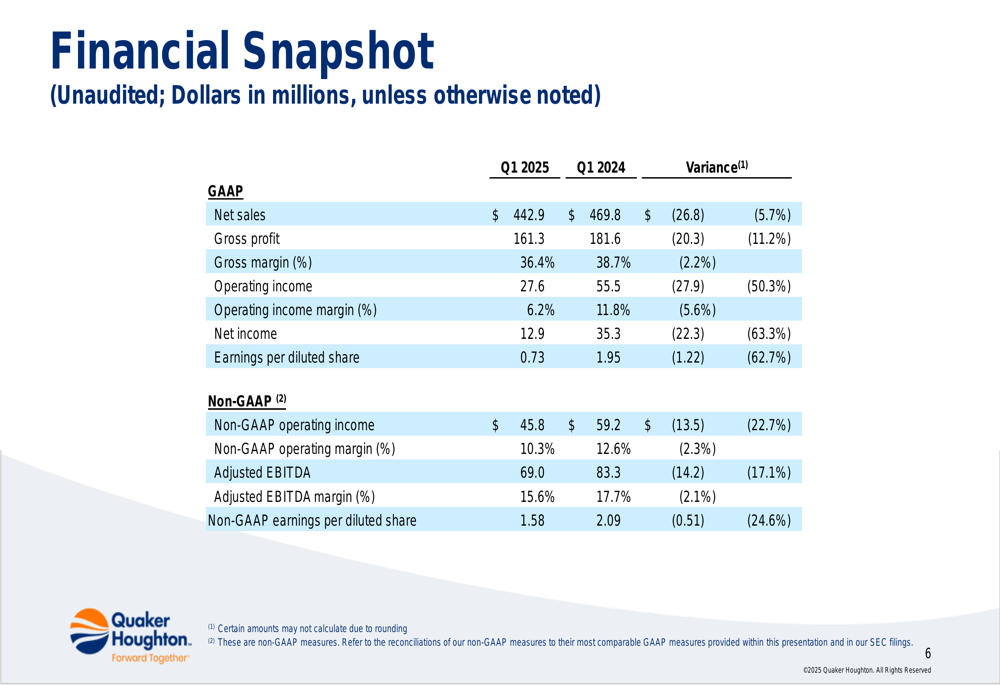

Quaker Chemical reported net sales of $443 million for Q1 2025, representing a 5.7% decrease from $469.8 million in the same period last year. The company’s adjusted EBITDA declined 17.1% year-over-year to $69 million, while non-GAAP earnings per diluted share fell 24.6% to $1.58.

As shown in the following financial snapshot comparing Q1 2025 to Q1 2024, the company experienced declines across both GAAP and non-GAAP metrics:

The company attributed the performance decline to several factors, including soft end market conditions, heightened uncertainty, higher raw material costs, and lower gross margins. These challenges were partially offset by lower SG&A expenses as the company focused on cost management.

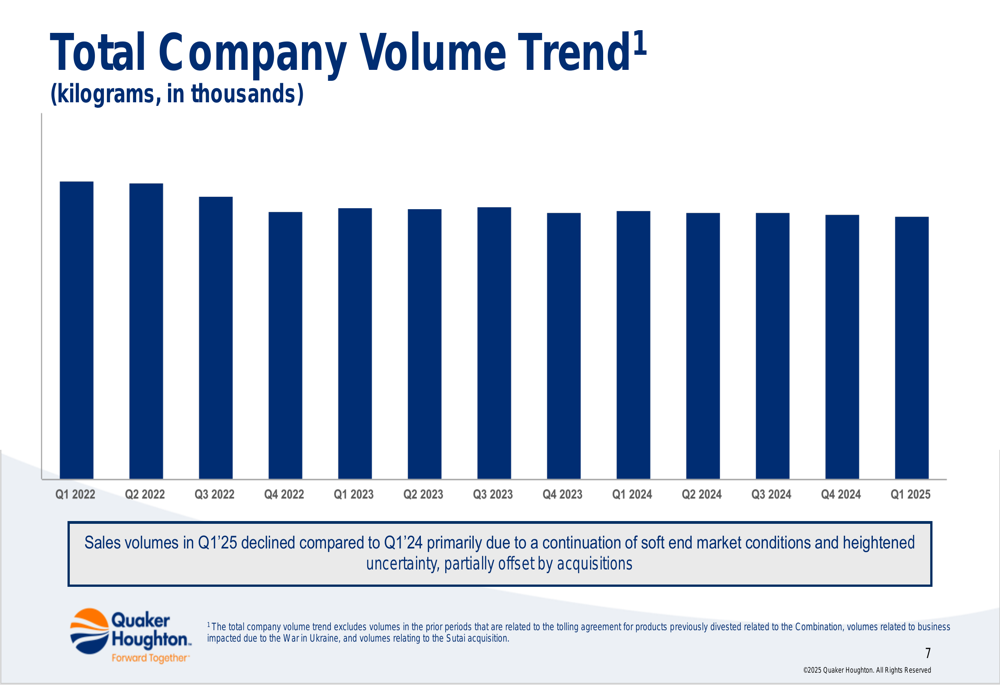

Sales volumes have continued their downward trend, as illustrated in the following chart showing total company volume from Q1 2022 through Q1 2025:

Strategic Initiatives

Despite challenging market conditions, Quaker Chemical has pursued strategic growth through acquisitions. The company highlighted three recent acquisitions aimed at strengthening its portfolio of advanced solutions and metalworking fluids: Chemical Solutions & Innovations, Dipsol Chemicals, and Natech.

The Q1 highlights slide showcases these acquisitions alongside the quarter’s key financial metrics:

The Dipsol acquisition was funded with borrowings under the company’s existing credit facility, according to the presentation. These strategic moves align with the company’s previous statements about focusing on growth opportunities despite market headwinds.

Detailed Financial Analysis

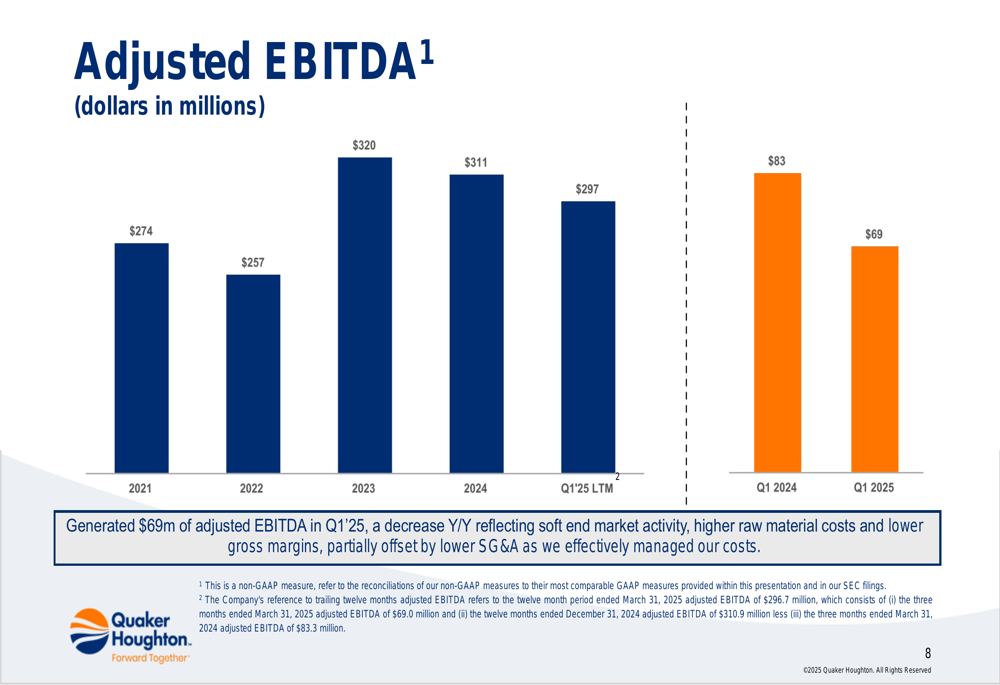

Quaker Chemical’s adjusted EBITDA has shown fluctuations over recent years, with the Q1 2025 figure of $69 million representing a decline from both the previous quarter and the same period last year. The following chart illustrates the adjusted EBITDA trend:

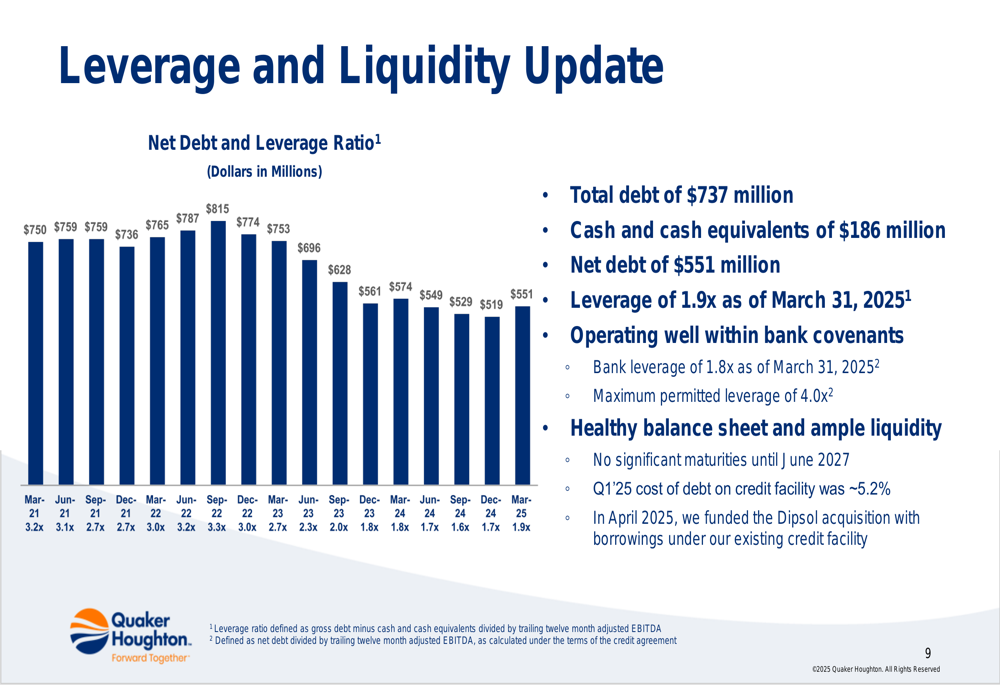

Despite the performance challenges, the company maintains a healthy balance sheet with a net debt leverage ratio of 1.9x as of March 31, 2025. Total (EPA:TTEF) debt stood at $737 million, with cash and cash equivalents of $186 million, resulting in net debt of $551 million.

The company’s leverage and liquidity position is illustrated in the following chart:

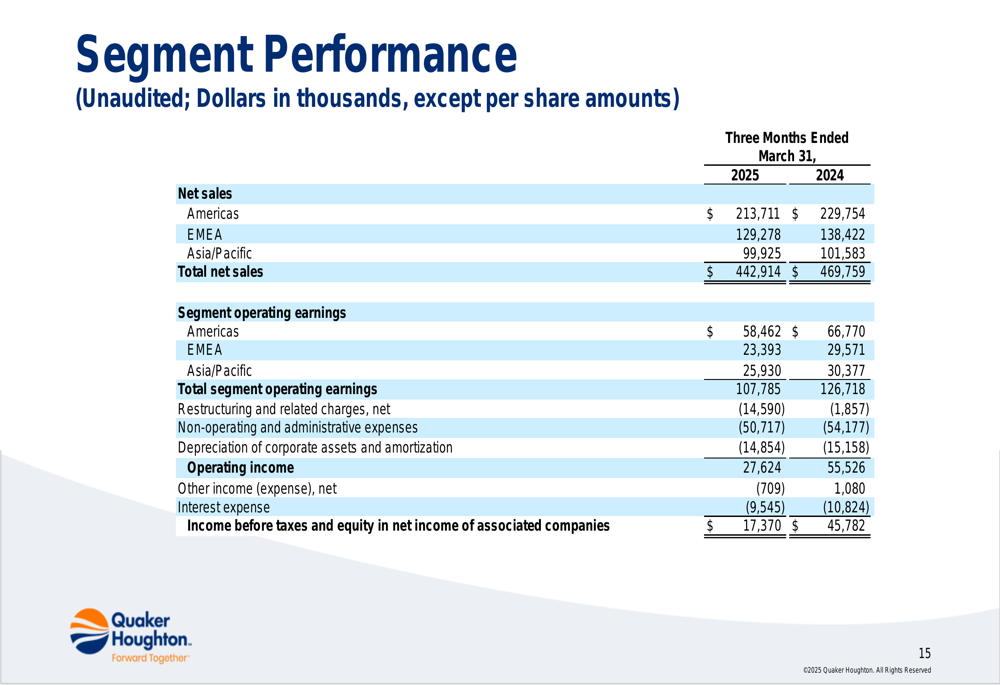

From a segment perspective, Quaker Chemical’s performance varied by region. The Americas remained the largest contributor to net sales at $213.7 million, followed by EMEA (Europe, Middle East, and Africa) at $129.3 million, and Asia/Pacific at $99.9 million. The segment breakdown provides insight into the geographic distribution of the company’s business:

Forward-Looking Statements

While the Q1 2025 presentation did not provide specific forward guidance, the company’s focus on strategic acquisitions suggests a commitment to long-term growth despite current challenges. The company’s healthy balance sheet, with no significant debt maturities until June 2027 and a cost of debt on the credit facility of approximately 5.2%, provides financial flexibility to navigate the current environment.

This contrasts somewhat with statements made during the Q4 2024 earnings call, where CEO Joe Bergquist had expressed expectations for revenue, adjusted EBITDA, and earnings growth in 2025. The Q1 results indicate that the company continues to face headwinds in achieving these growth targets, at least in the early part of the year.

The ongoing challenges of soft end market conditions, higher raw material costs, and lower gross margins will likely remain key factors for investors to monitor in upcoming quarters. Meanwhile, the integration of recent acquisitions may provide opportunities for revenue synergies and expanded market presence as Quaker Chemical positions itself for eventual market recovery.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.