Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Quaker Chemical Corporation (NYSE:KWR) released its second quarter 2025 results on July 31, showing a mixed financial performance with volume growth and strong cash generation despite significant GAAP losses. The company’s stock closed at $129.51, up 1.43% following the earnings announcement, reflecting investor confidence despite the challenging market environment.

The specialty chemicals manufacturer reported net sales of $483 million for Q2 2025, representing a 4% year-over-year increase. This growth came amid what the company described as continued market softness, highlighting Quaker’s ability to outperform its served markets.

Quarterly Performance Highlights

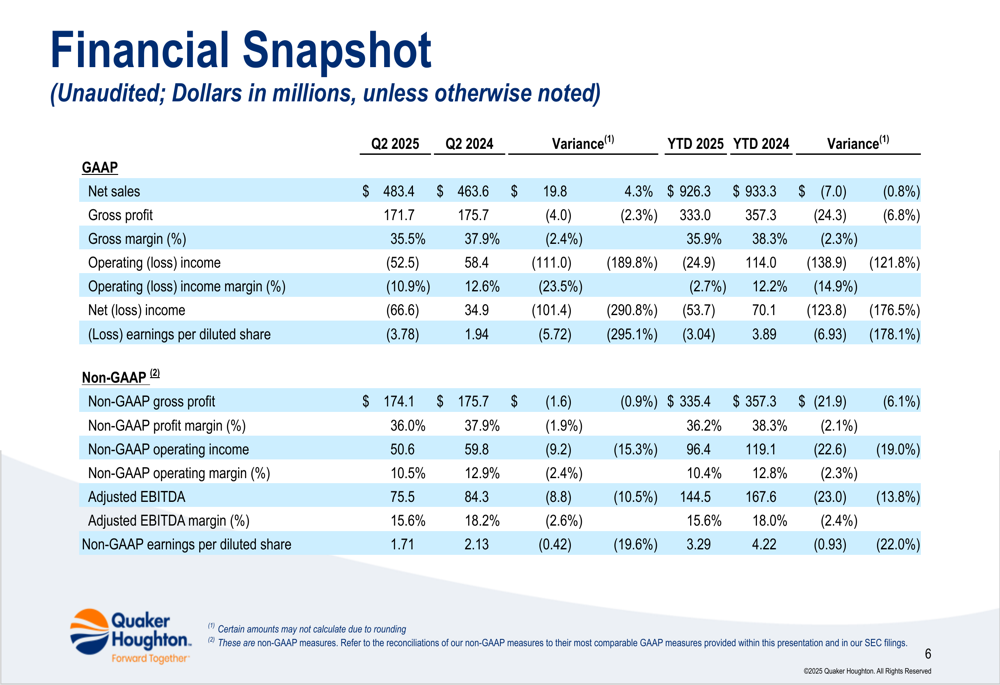

Quaker Chemical’s Q2 2025 results revealed a stark contrast between GAAP and non-GAAP metrics. While the company posted a GAAP operating loss of $(52.5) million and a net loss of $(66.6) million, its non-GAAP figures painted a more positive picture.

As shown in the following financial snapshot comparing current and prior periods:

On a non-GAAP basis, the company achieved an operating income of $50.6 million and adjusted EBITDA of $75.5 million, representing a margin of 15.6%. Non-GAAP earnings per diluted share came in at $1.71 for the quarter. The significant difference between GAAP and non-GAAP results suggests substantial one-time charges affecting the reported figures.

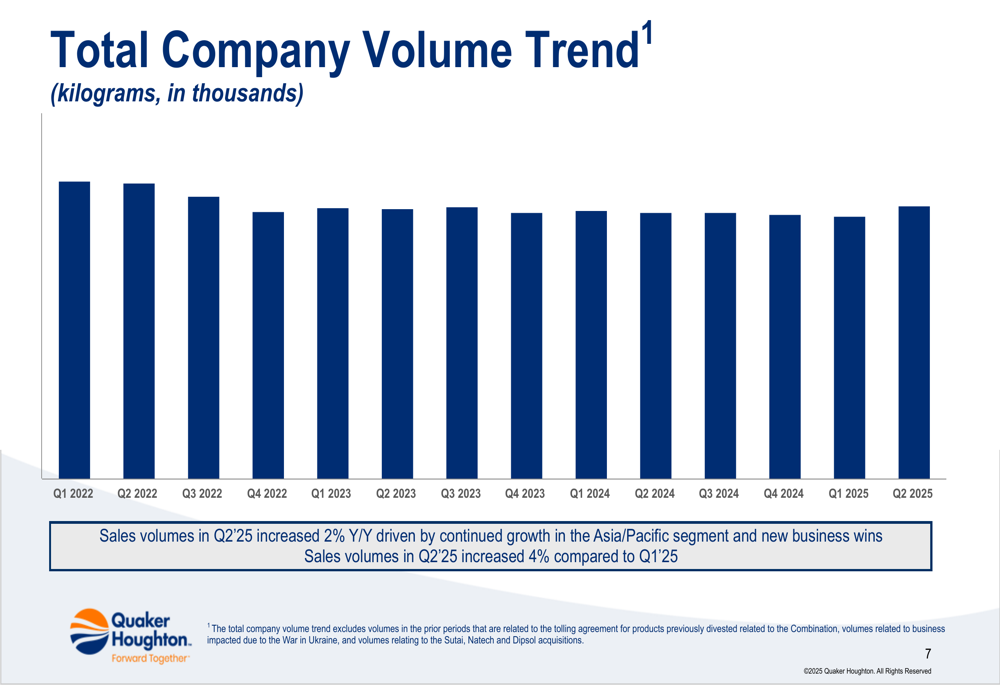

A key positive indicator was the company’s volume growth, which increased by 2% year-over-year and 4% sequentially from Q1 2025. This growth was primarily driven by continued strength in the Asia/Pacific segment and new business wins, demonstrating Quaker’s ability to gain market share despite challenging conditions.

The following chart illustrates the company’s volume trend over recent quarters:

Detailed Financial Analysis

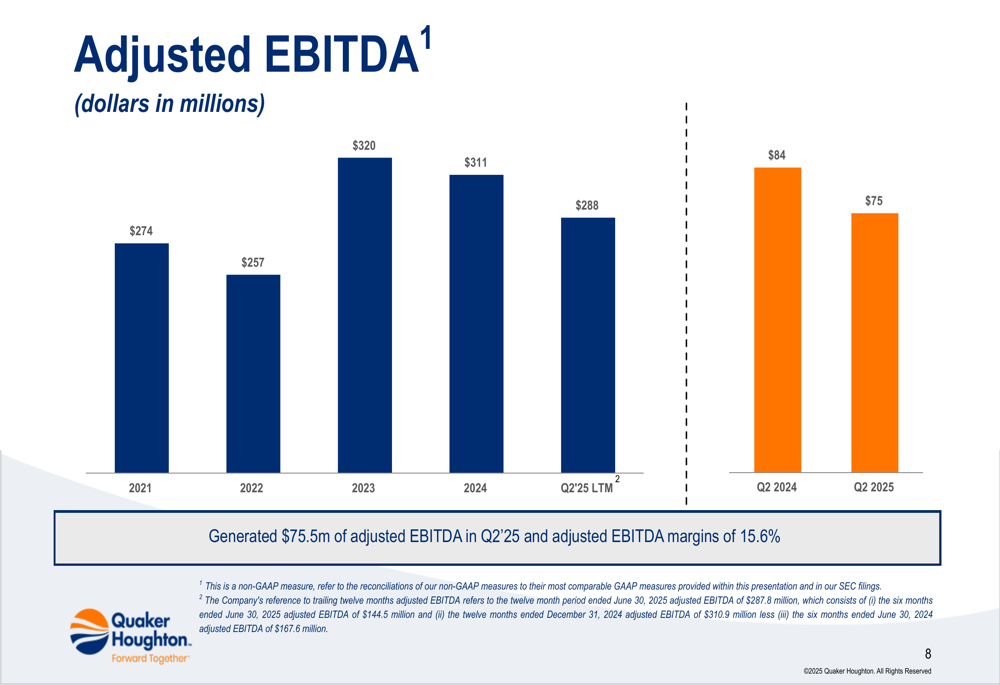

Quaker Chemical’s adjusted EBITDA for Q2 2025 was $75.5 million, down from $84 million in Q2 2024. This reflects ongoing margin pressures facing the company. The longer-term EBITDA trend shows a decline from the peaks seen in 2023-2024, with the last twelve months (LTM) figure at $288 million compared to $311 million for full-year 2024.

The following chart shows the adjusted EBITDA trend from 2021 through Q2 2025:

The company’s gross margin remained solid at 36.0% on a non-GAAP basis, within the company’s target range and reflecting its pricing discipline despite input cost pressures. Operating cash flow was $42 million for the quarter, demonstrating the company’s ability to generate cash despite challenging market conditions.

Segment performance varied across regions. While the Asia/Pacific region showed continued growth, other markets faced more significant headwinds. This regional variance aligns with broader global economic trends, where Asian markets have shown more resilience compared to slower growth in North America and Europe.

Balance Sheet and Liquidity

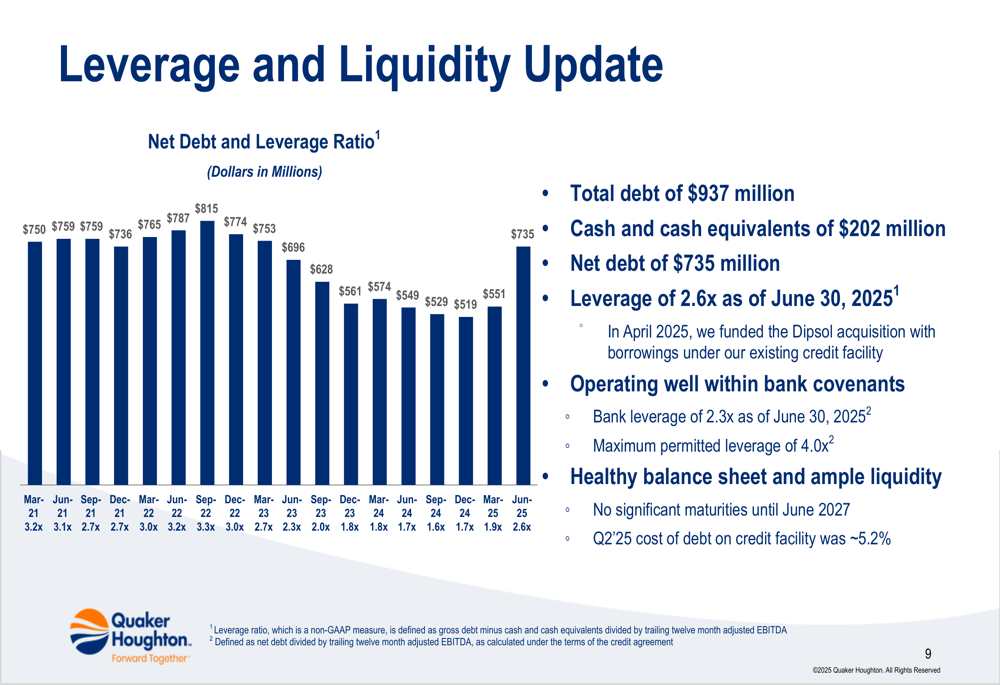

Quaker Chemical maintained a stable financial position with total debt of $937 million and cash and cash equivalents of $202 million, resulting in a net debt of $735 million as of June 30, 2025. The company’s leverage ratio stood at 2.6x, well within its bank covenant maximum of 4.0x.

The following chart illustrates the company’s leverage and liquidity position:

The company continued its share repurchase program, buying back $33 million worth of shares during the quarter. This reflects management’s confidence in the company’s long-term prospects and commitment to returning value to shareholders despite near-term challenges.

Quaker Chemical’s debt maturity profile remains favorable, with no significant maturities until June 2027, providing financial flexibility. The cost of debt on its credit facility was approximately 5.2% during Q2 2025, a manageable level in the current interest rate environment.

Strategic Initiatives and Outlook

During the earnings call, CEO Joseph Berquist emphasized the company’s strategic focus on strengthening customer relationships: "We are gaining traction with our key objectives, refocusing and strengthening the organization around the customer." This customer-centric approach appears to be yielding results, as evidenced by the new business wins contributing to volume growth.

The company has implemented a cost optimization program expected to yield $5-8 million in savings in the second half of 2025. This initiative aims to improve operational efficiency while maintaining the company’s competitive position in key markets.

Quaker Chemical forecasts continued market softness through the second half of 2025, with expectations for revenue and earnings to remain similar to 2024 levels. Despite these near-term challenges, the company is targeting a long-term organic growth rate of 2-4% and anticipates improved performance in the latter half of the year.

Risk Factors

The presentation highlighted several risk factors that could impact future performance, including economic conditions, tariffs, inflation, supply chain constraints, customer financial stability, interest rates, geopolitical disruptions, and cybersecurity threats. These factors create uncertainty in the operating environment and may affect the company’s ability to achieve its growth targets.

The impact of tariffs on customer sentiment was specifically addressed during the earnings call, indicating this remains an area of concern for management. Additionally, regional market conditions vary significantly, requiring tailored approaches to maintain growth across the company’s global footprint.

Conclusion

Quaker Chemical’s Q2 2025 presentation reveals a company navigating challenging market conditions with a focus on volume growth, cash generation, and strategic customer relationships. While GAAP results show significant losses, the non-GAAP metrics paint a picture of operational resilience with solid margins and positive cash flow.

The contrast between regional performances, particularly the strength in Asia/Pacific versus challenges in other markets, highlights the importance of the company’s global diversification strategy. As Quaker Chemical implements its cost optimization initiatives and continues to focus on customer-centric growth, investors will be watching closely to see if the company can maintain its volume momentum while improving its GAAP performance in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.