Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Rain Industries Limited (BSE:RAIN) reported a strong quarter-over-quarter performance in its Q2 2025 earnings presentation, with revenue from operations increasing by 17% compared to the previous quarter. The company’s performance comes amid a backdrop of expanding global aluminum production and stabilizing raw material prices, which have created a favorable operating environment for its core businesses.

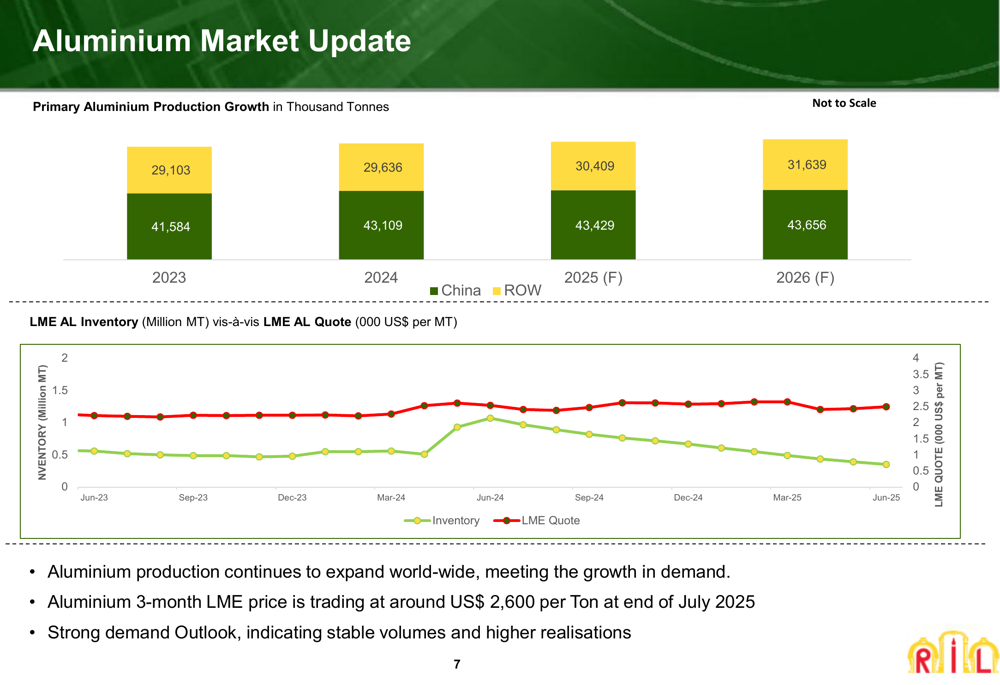

The company operates in three segments: Carbon, Advanced Materials, and Cement, with the Carbon segment continuing to be the primary revenue and profit driver. According to the presentation, aluminum production continues to expand worldwide to meet growing demand, with the 3-month LME aluminum price trading around US$ 2,600 per ton at the end of July 2025.

As shown in the following chart of aluminum production growth and pricing trends:

Quarterly Performance Highlights

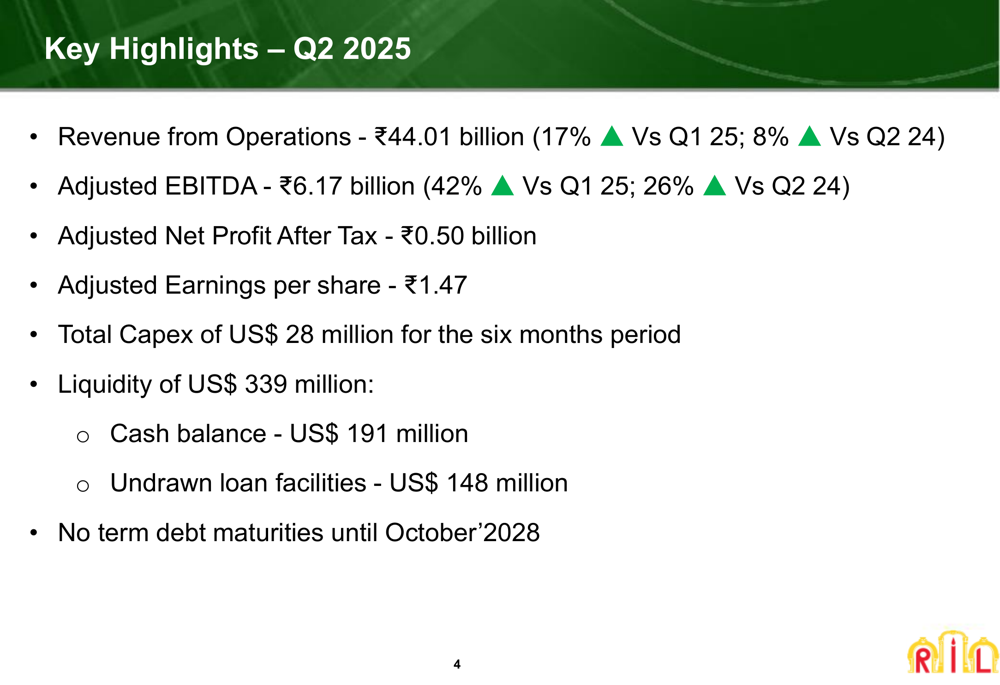

Rain Industries reported revenue from operations of ₹44.01 billion in Q2 2025, representing an 8% increase year-over-year and a 17% increase quarter-over-quarter. Adjusted EBITDA saw an even more significant improvement, rising to ₹6.17 billion, up 26% compared to Q2 2024 and 42% compared to Q1 2025.

The company’s key financial metrics for the quarter include:

- Adjusted Net Profit After Tax: ₹0.50 billion

- Adjusted Earnings per share: ₹1.47

- Total (EPA:TTEF) Capex: US$ 28 million for the six months period

- Liquidity: US$ 339 million, comprising cash balance of US$ 191 million and undrawn loan facilities of US$ 148 million

The following slide summarizes these key financial highlights:

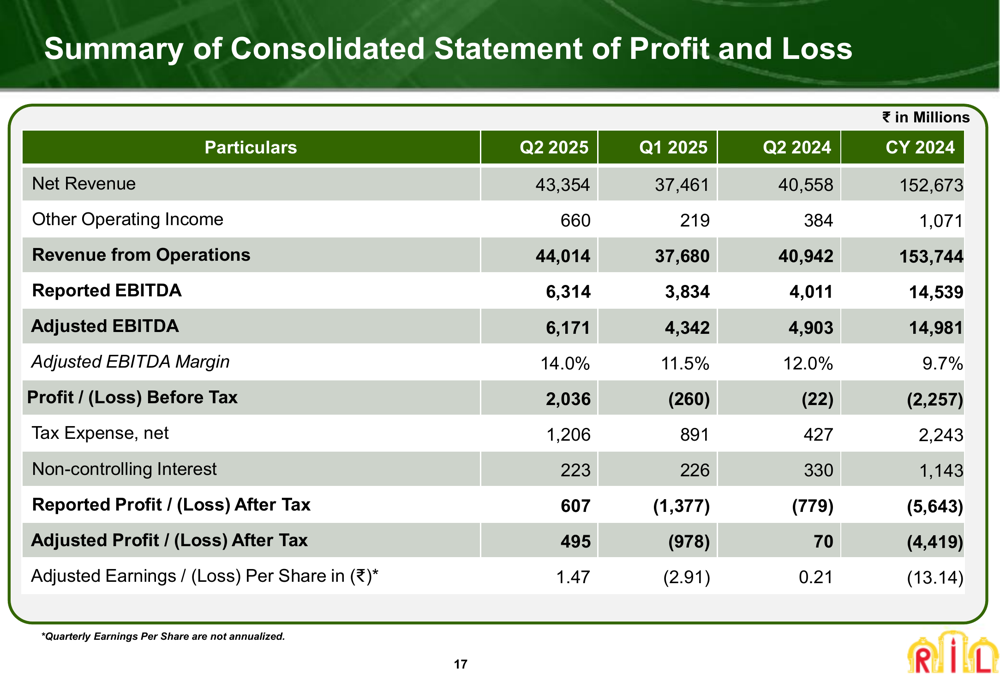

The company’s consolidated statement of profit and loss provides a more detailed view of its financial performance, showing the significant improvement in EBITDA margin to 14.0% in Q2 2025, compared to 11.5% in Q1 2025 and 12.0% in Q2 2024:

Segment Analysis

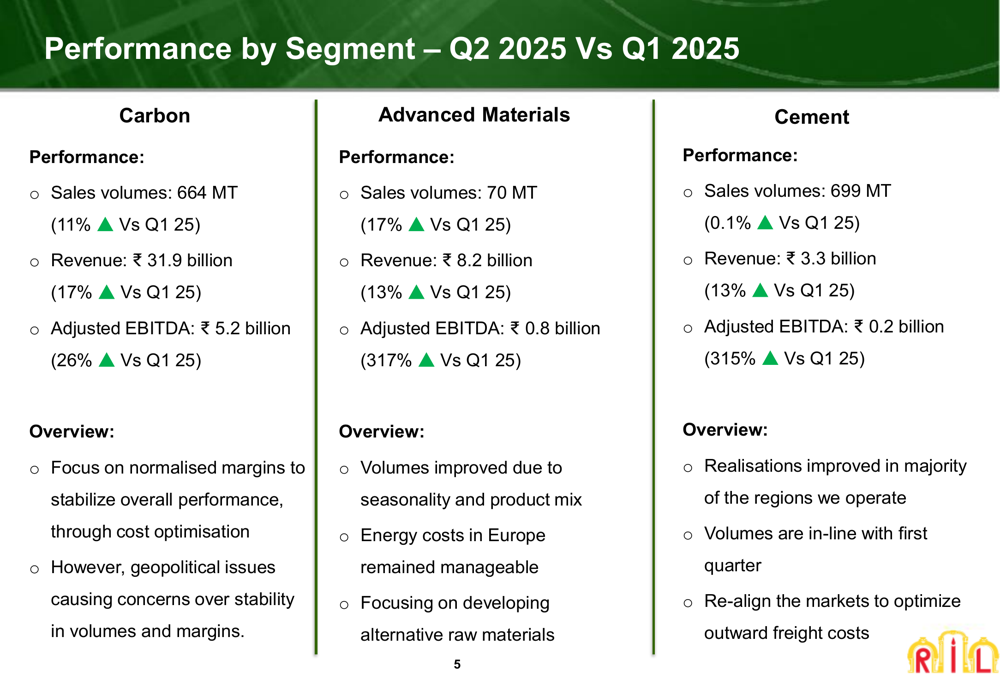

All three of Rain Industries’ business segments showed improvement in Q2 2025 compared to the previous quarter, with particularly strong performances in the Advanced Materials and Cement segments in terms of EBITDA growth.

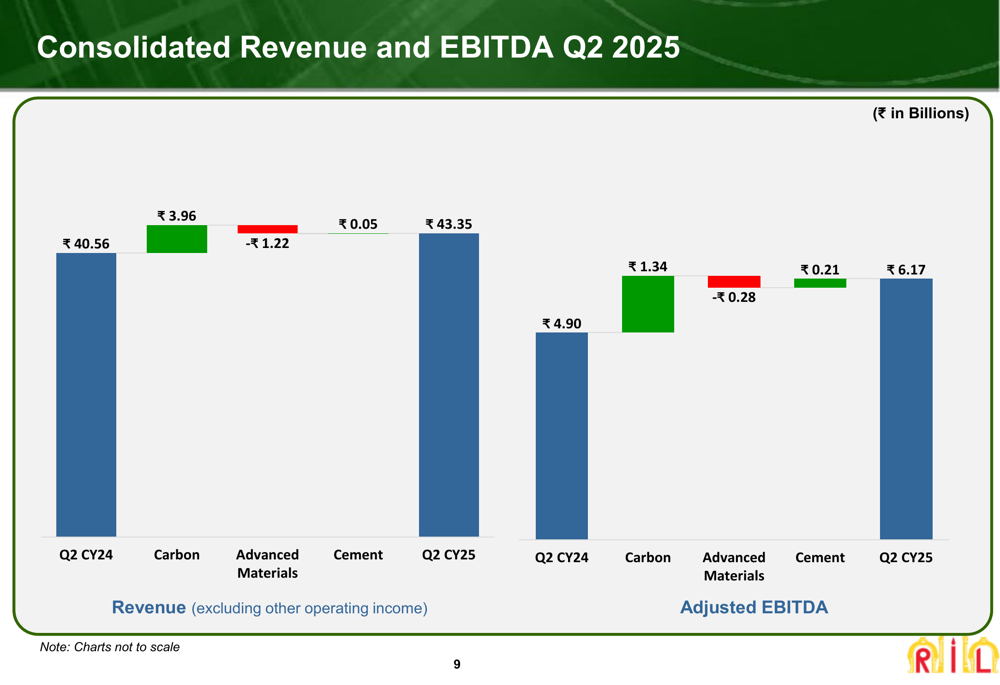

The Carbon segment, which remains the company’s largest business, reported sales volumes of 664,000 MT (up 11% quarter-over-quarter), revenue of ₹31.9 billion (up 17%), and adjusted EBITDA of ₹5.2 billion (up 26%). The company attributed this growth to higher calcined petroleum coke (CPC) volumes and prices, which offset lower distillation product volumes.

The Advanced Materials segment saw sales volumes increase by 17% quarter-over-quarter to 70,000 MT, with revenue rising 13% to ₹8.2 billion. Most notably, adjusted EBITDA surged by 317% to ₹0.8 billion, reflecting improved volumes due to seasonality and manageable energy costs in Europe.

The Cement segment reported essentially flat volumes at 699,000 MT but achieved a 13% increase in revenue to ₹3.3 billion and a remarkable 315% increase in adjusted EBITDA to ₹0.2 billion, driven by improved realizations and optimization of outward freight costs.

The following slide details the performance of each segment:

The waterfall chart below illustrates how each segment contributed to the overall revenue and EBITDA growth compared to the same quarter last year:

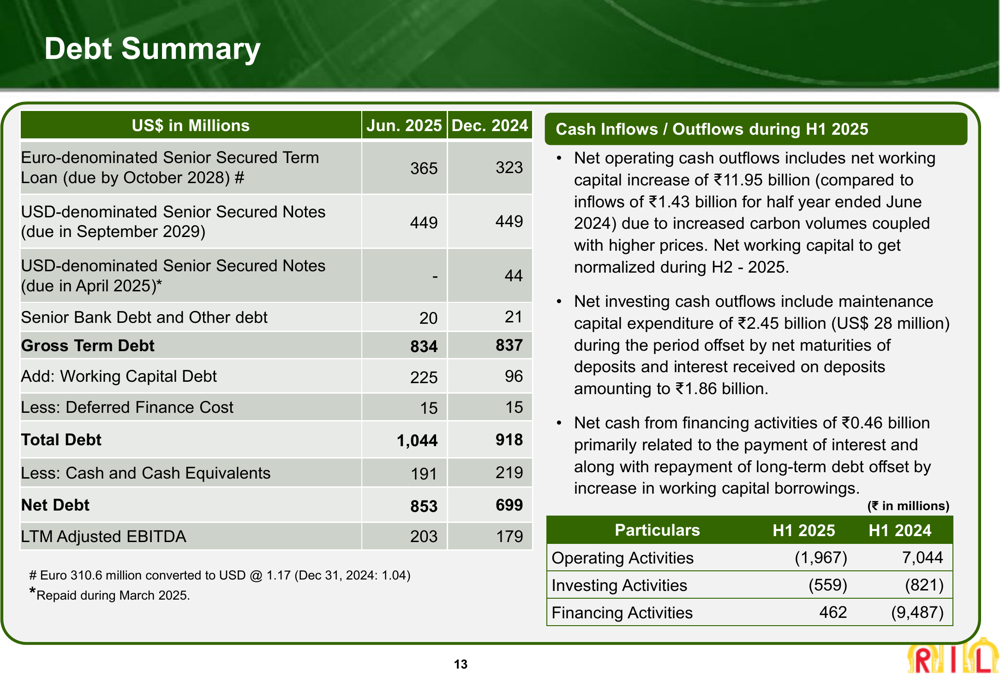

Debt Position and Cash Flow

Despite the strong operational performance, Rain Industries’ debt position has deteriorated somewhat. The company’s net debt increased to US$ 853 million as of June 2025, up from US$ 699 million in December 2024. This increase occurred despite the company having no term debt maturities until October 2028.

The company’s cash flow from operating activities was negative at ₹1,967 million for H1 2025, compared to a positive ₹7,044 million in H1 2024. This decline in operating cash flow, combined with the increase in net debt, raises some concerns about the company’s financial health despite the improved EBITDA performance.

The detailed debt summary is presented in the following slide:

Strategic Initiatives and Outlook

Rain Industries is focusing on several strategic initiatives to address challenges and position itself for future growth. These include:

1. Conducting advanced research and testing of next-generation energy storage technologies at its North America demonstration facility

2. Ongoing development and refinement of proprietary NOVARES® products to meet evolving market demands

3. Expanding the use of alternative raw materials to mitigate supply chain disruptions

4. Investigating the application of biocarbon materials in its carbon-based product portfolio

5. Operational enhancements in India, including setting up a new CTP remelting unit and reinstating blending operations

The company’s business outlook acknowledges ongoing challenges with raw material availability but emphasizes its focus on cost-saving measures, ESG compliance, and debt optimization. Rain Industries is also closely monitoring potential tariff impacts, though it reports no material impact as of the presentation date.

The company’s safety performance has shown significant improvement, with the Total Recordable Incident Rate (TRIR) decreasing to 0.03 in H1 2025, compared to 0.13 in 2024 and 0.26 in 2023.

Looking ahead, Rain Industries appears well-positioned to benefit from strong demand in the aluminum sector, though it will need to address its increasing debt levels and negative operating cash flow to ensure long-term financial stability. The company’s strategic focus on R&D and alternative raw materials could help it navigate market challenges and capitalize on emerging opportunities in energy storage and other advanced materials applications.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.