TSX lower as gold rally takes a breather

Renasant (NYSE:RNST) Corporation (NASDAQ:RNST) presented its first quarter 2025 earnings results on April 23, showing continued momentum with improved net interest margin, solid loan growth, and strong deposit performance as the bank prepares for its upcoming merger with First Bancshares.

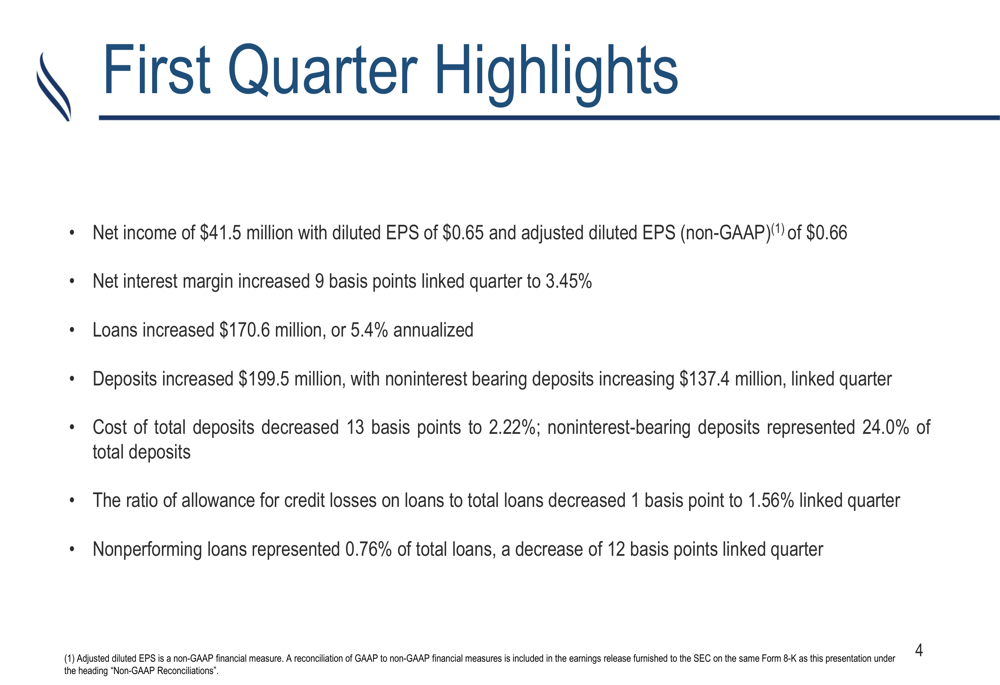

Quarterly Performance Highlights

Renasant reported net income of $41.5 million for Q1 2025, with diluted earnings per share (EPS) of $0.65 and adjusted diluted EPS of $0.66. The company’s net interest margin increased 9 basis points quarter-over-quarter to 3.45%, reflecting improved pricing discipline on both sides of the balance sheet.

Loans increased by $170.6 million during the quarter, representing annualized growth of 5.4%, while deposits grew by $199.5 million. Notably, noninterest-bearing deposits increased by $137.4 million, helping to reduce the company’s overall cost of funds.

As shown in the following first quarter highlights:

The cost of total deposits decreased 13 basis points to 2.22%, with noninterest-bearing deposits representing 24.0% of total deposits. Asset quality remained strong, with nonperforming loans decreasing 12 basis points to 0.76% of total loans.

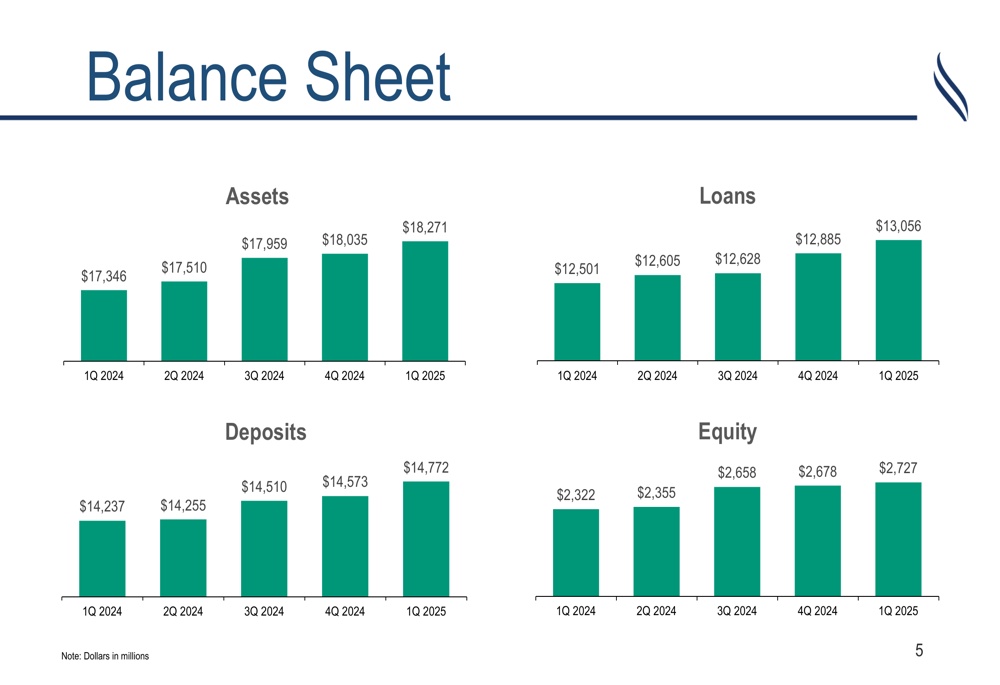

Balance Sheet and Liquidity

Renasant’s balance sheet continued to strengthen over the past five quarters, with total assets reaching $18.3 billion as of Q1 2025, up from $17.3 billion in Q1 2024. Loans grew to $13.1 billion, while deposits increased to $14.8 billion, maintaining a stable loan-to-deposit ratio of 88%.

The following chart illustrates the consistent growth across key balance sheet metrics:

The company’s liquidity position remains strong, with cash and securities representing 17.5% of total assets, up from 16.2% in Q1 2024. This provides Renasant with ample flexibility to support continued loan growth while maintaining appropriate liquidity buffers.

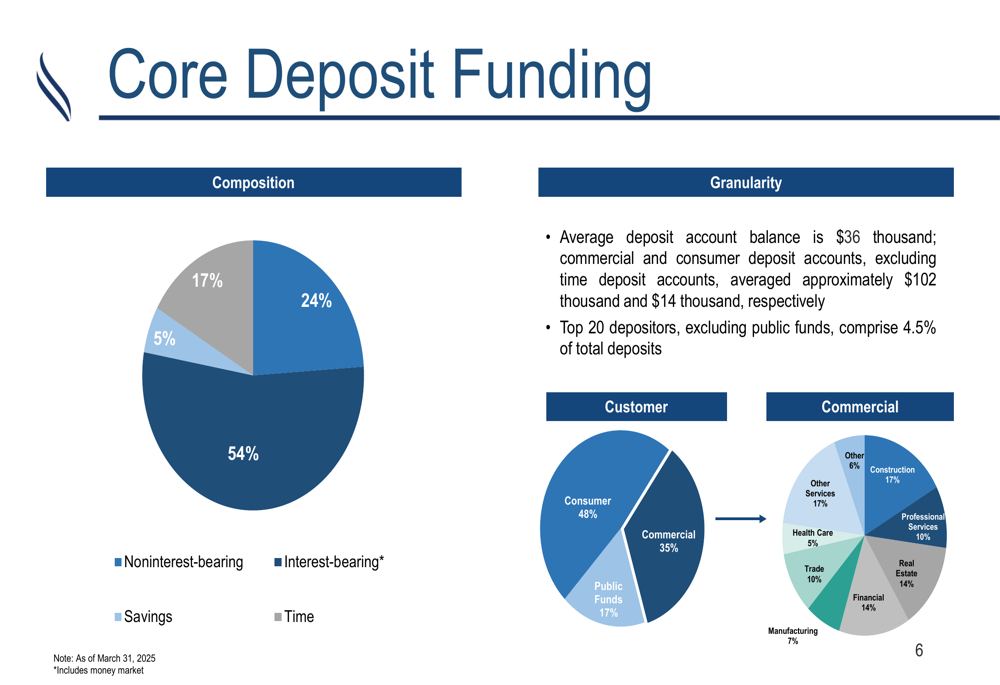

Renasant’s deposit base is well-diversified, with an average deposit account balance of $36,000. Commercial and consumer deposit accounts (excluding time deposits) averaged approximately $102,000 and $14,000, respectively. The top 20 depositors, excluding public funds, comprise only 4.5% of total deposits, highlighting the granular nature of the bank’s funding.

The following chart breaks down the company’s deposit composition:

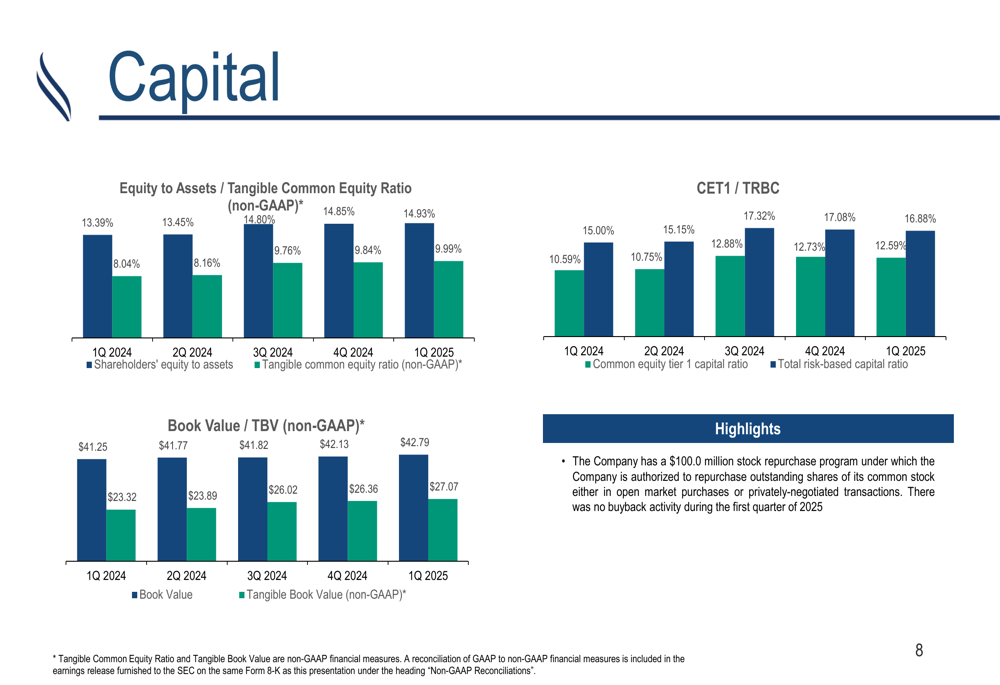

Capital and Asset Quality

Renasant’s capital position continued to strengthen, with the tangible common equity ratio (non-GAAP) improving to 9.99% in Q1 2025, up from 8.04% a year earlier. The common equity tier 1 capital ratio reached 12.88%, while the total risk-based capital ratio stood at 16.88%.

Tangible book value per share increased to $27.07, up from $23.32 in Q1 2024, representing growth of 16% year-over-year.

The following chart shows the improvement in capital ratios:

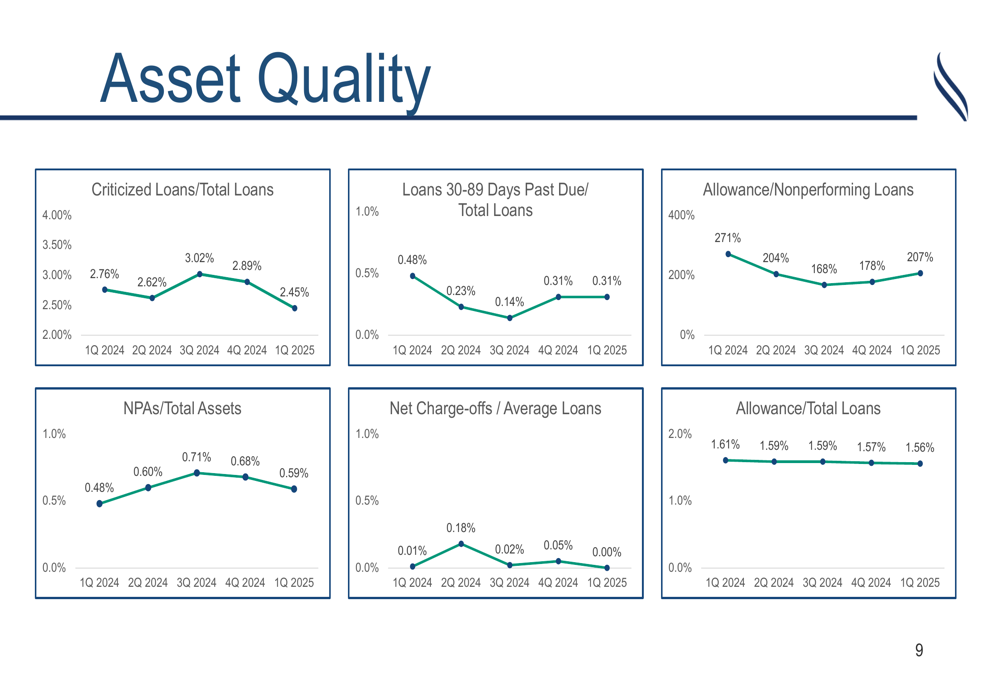

Asset quality metrics showed continued improvement, with criticized loans decreasing to 2.45% of total loans in Q1 2025, down from a peak of 3.02% in Q3 2024. The allowance for credit losses to nonperforming loans ratio stood at 207%, indicating strong coverage for potential problem loans.

The following chart illustrates the trends in asset quality metrics:

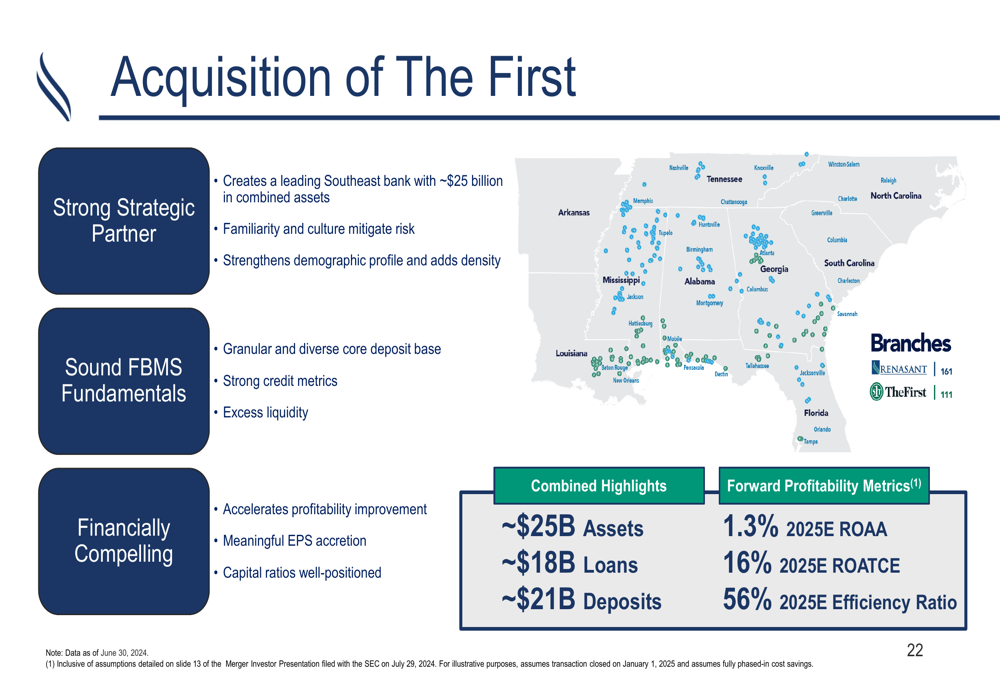

Strategic Merger with First Bancshares

A key strategic focus for Renasant is its pending merger with First Bancshares, which is expected to close in the first half of 2025. The combination will create a leading Southeast bank with approximately $25 billion in combined assets, strengthening Renasant’s demographic profile and adding density to its footprint.

The merger is expected to accelerate profitability improvement with meaningful EPS accretion, while maintaining strong capital ratios. Both banks have complementary cultures and business models, which should facilitate a smooth integration.

As shown in the following slide detailing the strategic benefits of the acquisition:

This merger builds on Renasant’s existing strong presence in the Southeast, where it currently has a diversified footprint across Mississippi, Georgia, Alabama, Tennessee, and Florida. The combined entity will benefit from First Bancshares’ granular and diverse core deposit base, strong credit metrics, and excess liquidity.

Securities Portfolio and Loan Composition

Renasant’s securities portfolio represents 11.5% of total assets, with a duration of 4.6 years. The portfolio is well-diversified, with agency CMO securities representing 39% of the total, followed by agency MBS at 27% and municipal securities at 14%.

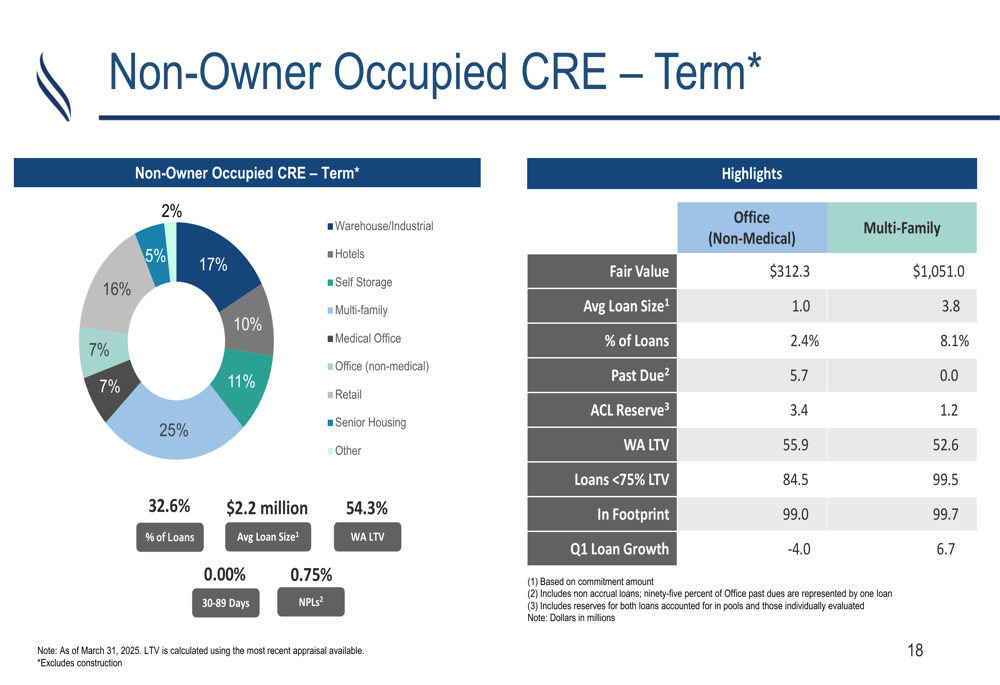

The company’s commercial real estate (CRE) loan portfolio is also well-diversified, with senior housing (25%), self-storage (17%), and multi-family (16%) representing the largest segments. Office loans, which have been a concern for many banks, represent only 7% of the non-owner occupied CRE term loan portfolio.

The following chart shows the composition of the non-owner occupied CRE term loan portfolio:

Forward Outlook

Looking ahead, Renasant is well-positioned to benefit from its strong balance sheet, improving profitability metrics, and pending merger with First Bancshares. The company’s focus on disciplined pricing, expense management, and credit quality should continue to support solid performance in the coming quarters.

The stock closed at $28.63 on April 22, 2025, up 2.58% for the day, and has traded between $26.97 and $39.63 over the past 52 weeks. With the merger expected to close in the first half of 2025, investors will be closely watching for updates on the regulatory approval process and integration planning.

Renasant’s continued improvement in net interest margin, coupled with solid loan growth and strong deposit performance, provides a solid foundation as the company prepares for its next chapter as a larger regional banking institution in the Southeast.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.