Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

Roots Corp (TSX:ROOT) presented its Q1 2025 financial results on June 13, 2025, highlighting continued momentum across key performance metrics. The iconic Canadian apparel retailer, founded in 1973 and inspired by Algonquin Park’s wilderness, reported its third consecutive quarter of growth in sales, gross margin, and adjusted EBITDA.

The company’s stock closed at $3.20 on June 12, 2025, representing a 4.23% increase, as investors appeared to anticipate positive results. Roots continues to position itself as a premium casual wear brand focused on comfort, craftsmanship, and quality materials while executing its omni-channel strategy.

Quarterly Performance Highlights

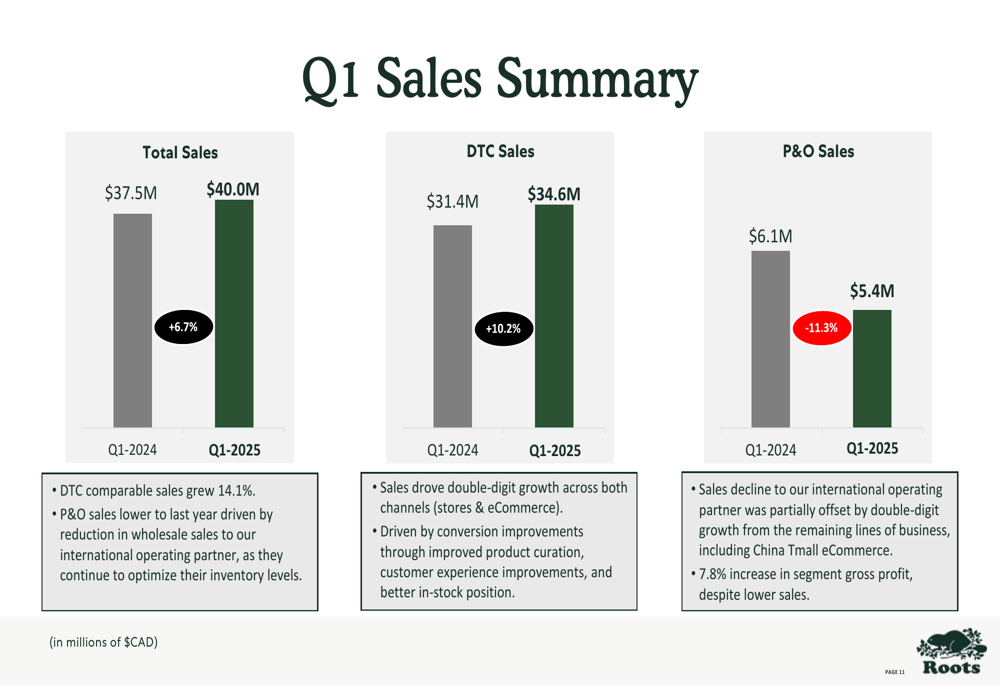

Roots reported Q1 2025 sales of $40.0 million, a 6.7% increase compared to $37.5 million in the same period last year. This growth was primarily driven by the Direct-to-Consumer (DTC) segment, which saw a 10.2% increase to $34.6 million and impressive comparable sales growth of 14.1%.

As shown in the following sales summary chart, the Partners & Other (P&O) segment experienced an 11.3% decline to $5.4 million, attributed mainly to reduced wholesale sales to international operating partners:

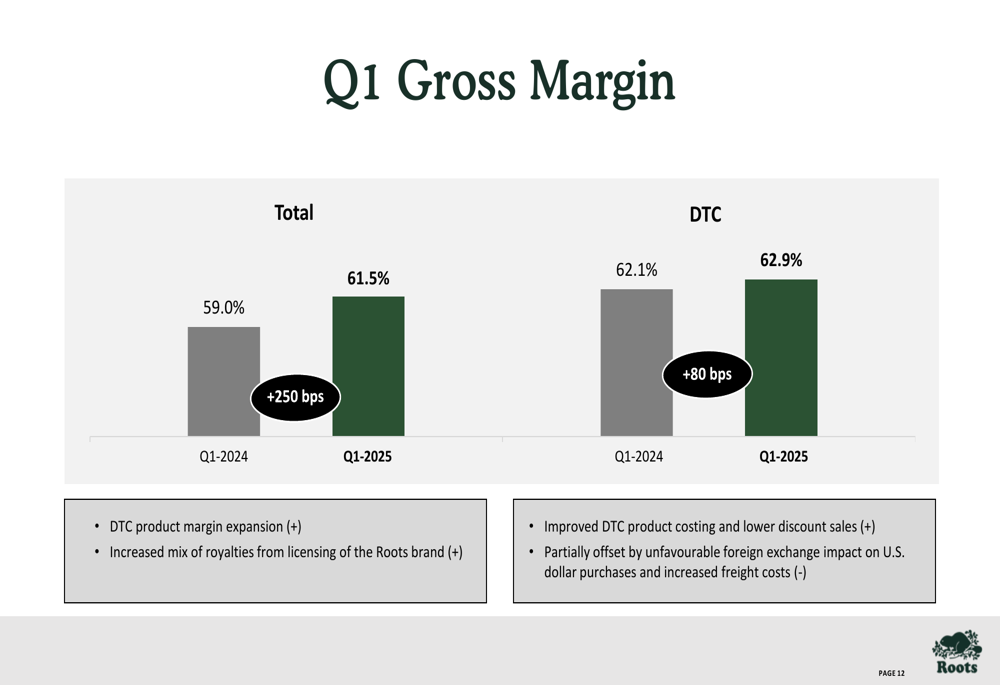

Gross margin performance showed significant improvement, with total gross margin increasing 250 basis points to 61.5%, while DTC gross margin rose 80 basis points to 62.9%. The company’s adjusted EBITDA loss narrowed to $7.1 million, a 10.7% improvement compared to an $8.0 million loss in Q1 2024.

The following chart illustrates the gross margin improvements across both total and DTC segments:

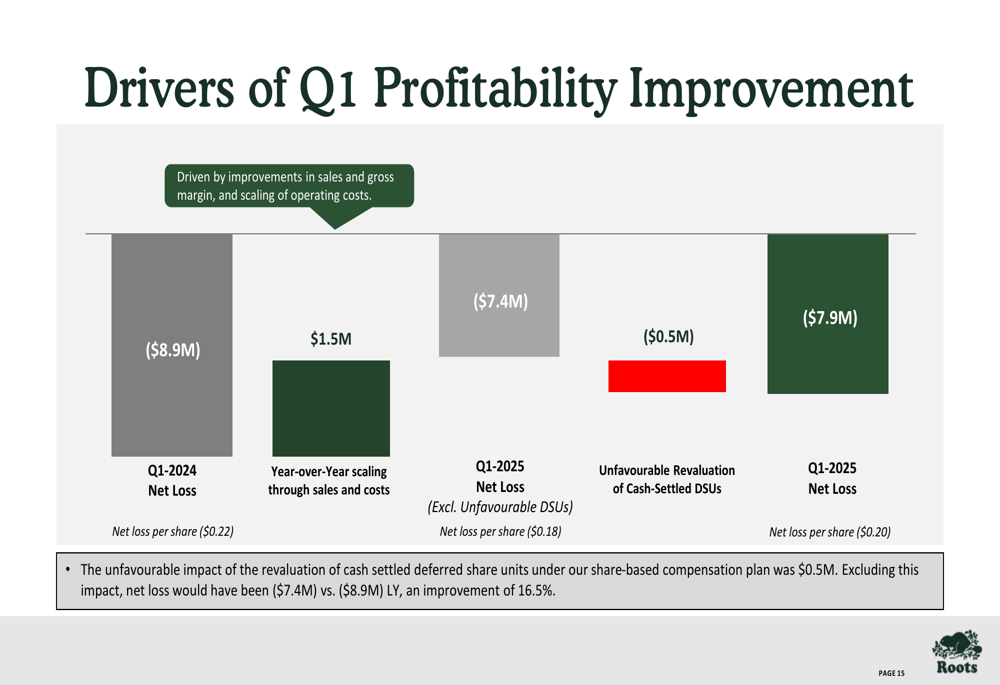

Net loss for the quarter was $7.9 million, improved from $8.9 million in the prior year period. On an adjusted basis, net loss was $7.4 million (18.4% of sales), compared to $8.1 million (21.7% of sales) in Q1 2024.

Detailed Financial Analysis

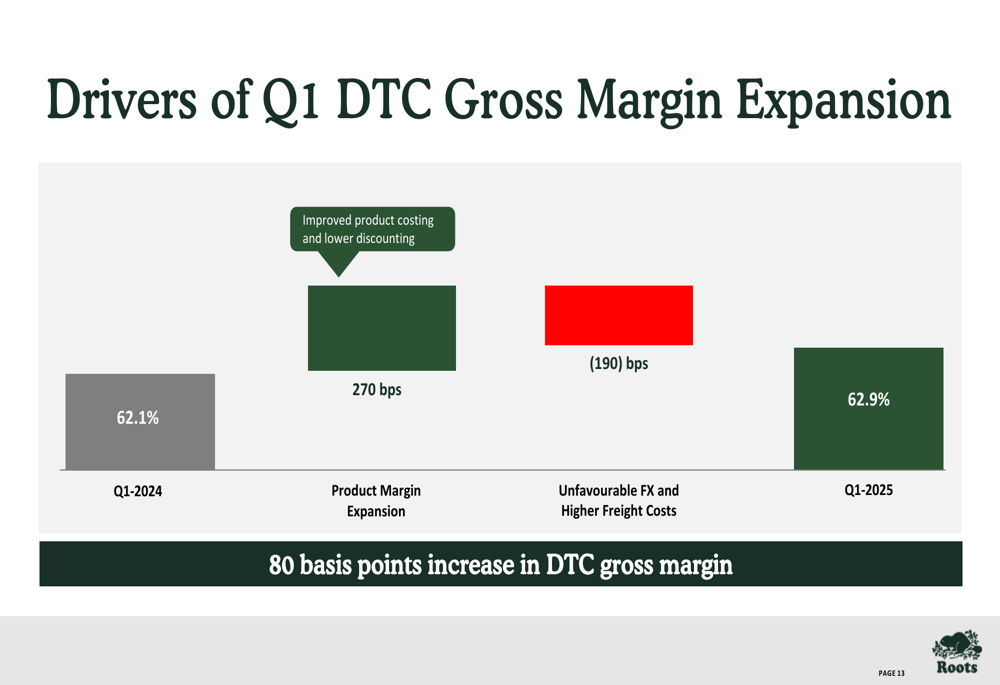

The improvement in DTC gross margin was primarily driven by better product costing and lower discounting, which contributed 270 basis points of expansion. However, these gains were partially offset by unfavorable foreign exchange movements and higher freight costs, which reduced margins by 190 basis points.

The following chart breaks down these drivers of DTC gross margin expansion:

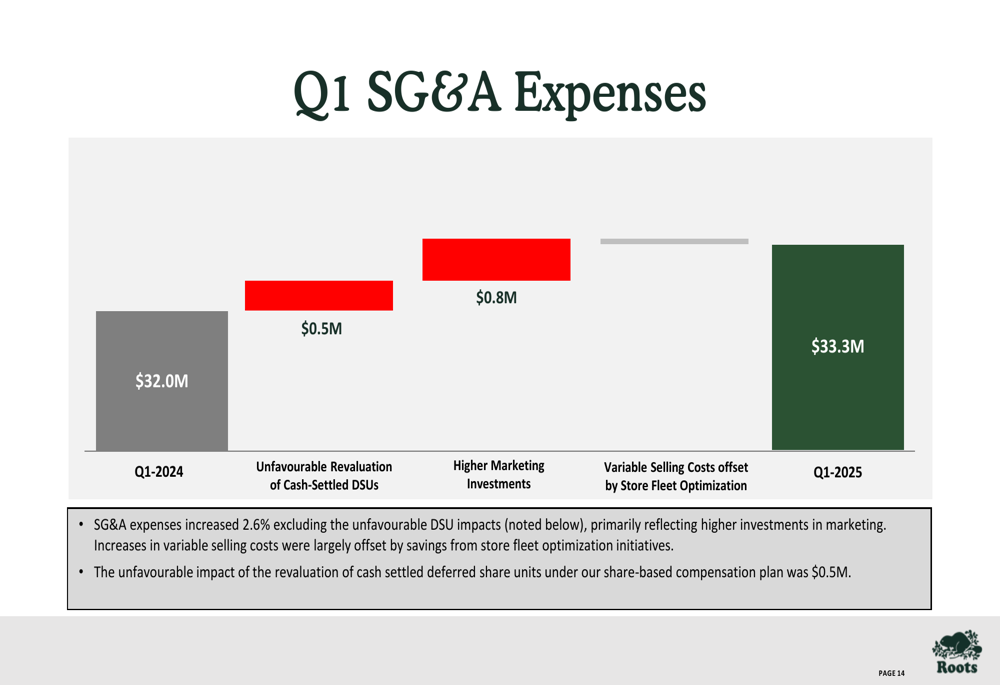

Selling, general and administrative (SG&A) expenses increased to $33.3 million from $32.0 million in the prior year period. This rise was largely attributable to a $0.5 million unfavorable revaluation of cash-settled deferred share units (DSUs) and $0.8 million in higher marketing investments, as illustrated below:

The company’s profitability improvement was driven by higher sales, improved gross margins, and effective scaling of operating costs, which contributed $1.5 million to the bottom line. This was partially offset by the $0.5 million DSU revaluation expense:

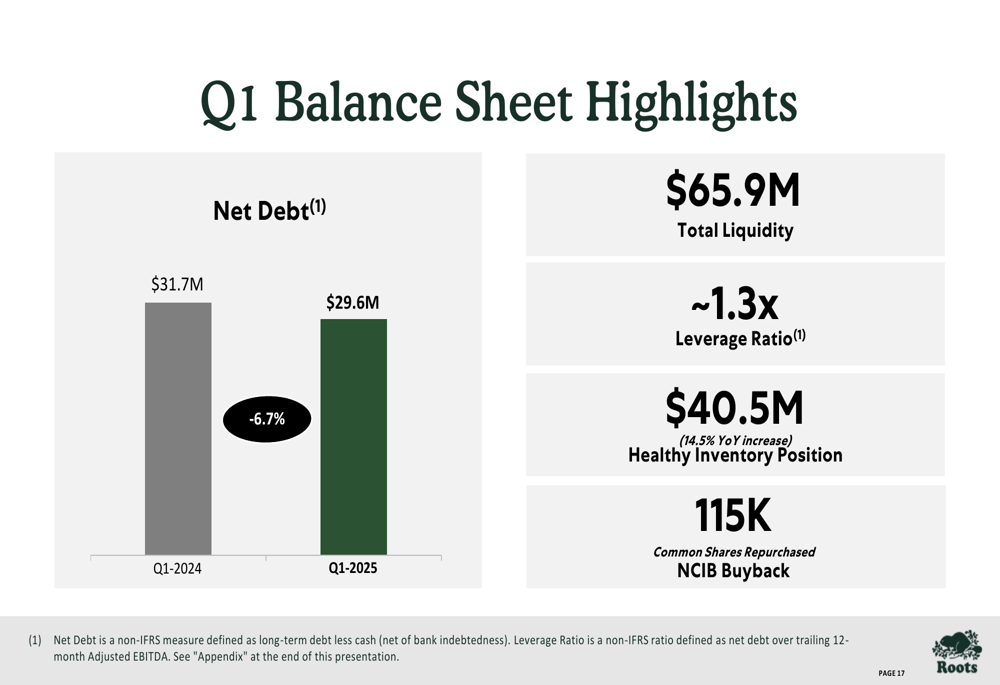

Roots maintained a strong balance sheet with net debt of $29.6 million, representing a 6.7% reduction from $31.7 million in the prior year period. The company reported total liquidity of $65.9 million and a healthy leverage ratio of approximately 1.3x.

The following chart highlights the company’s improving debt position:

Inventory levels increased 14.5% year-over-year to $40.5 million, which management described as "healthy" with improved availability in key collections to support sales growth. During the quarter, Roots repurchased 115,000 common shares under its Normal Course Issuer Bid (NCIB) program.

Strategic Initiatives

Roots outlined several strategic initiatives aimed at driving long-term growth and operational efficiency. The company executed a multi-pronged marketing strategy focused on paid media, customer engagement, and brand messaging elevation. Notable partnerships included a collaboration with Canadian NCAA basketball player Toby Fournier of Duke University to highlight the brand’s performance-based activewear.

The company’s brand ambassador program completed its first full-year cycle, exceeding internal impression and engagement benchmarks. Marketing investments increased year-over-year with strong returns reported.

On the operational front, Roots continued to invest in retail optimization by exiting underperforming stores while focusing on locations that support long-term profitability and customer engagement. The company began introducing elements of its "store of the future" design toolkit, featuring refreshed merchandising layouts and flexible fixture systems.

Technology investments included an automated replenishment system showing strong results, along with personalization technologies aimed at enhancing customer experience and improving efficiencies in customer service and returns processing.

Forward-Looking Statements

Looking ahead, Roots management indicated that the strong DTC sales momentum has continued during the first five weeks of Q2 2025. However, they cautioned that a significant period remains in the quarter, including the start of the back-to-school season in July.

The company remains focused on executing its strategic objectives while navigating what it describes as a "dynamic environment." With a strong balance sheet, low net debt leverage, and ample liquidity, Roots appears well-positioned to continue its growth trajectory while investing in brand-building and operational improvements.

Management emphasized the company’s commitment to long-term profitable growth, supported by its well-invested infrastructure and refined operating strategies. The continued strength in core fleece collections, along with updated cuts offering a more modern take on comfort, has resonated well with consumers and supported positive results across product lines.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.