Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

Grupo Rotoplas SA de CV (AGUA) presented its first quarter 2025 results on April 24, showing significant year-over-year profitability declines despite sequential improvements from the previous quarter. The water solutions company faces a challenging environment in its home market of Mexico, while experiencing strong growth in the United States and other Latin American markets. The stock closed at 10.71, up 5.04% on the day of the presentation, but remains well below its 52-week high of 29.79.

Quarterly Performance Highlights

Rotoplas reported a slight 1% year-over-year decrease in net sales to 2,636 million pesos for Q1 2025, but experienced a substantial 46% drop in EBITDA to 301 million pesos compared to 555 million pesos in Q1 2024. The EBITDA margin contracted significantly from 21% to 11%, though the company noted that excluding severance packages, the margin would have been 13.2%.

As shown in the comprehensive financial overview below, net income plummeted 92% to just 24 million pesos, while return on invested capital (ROIC) fell from 14.0% to 5.1%:

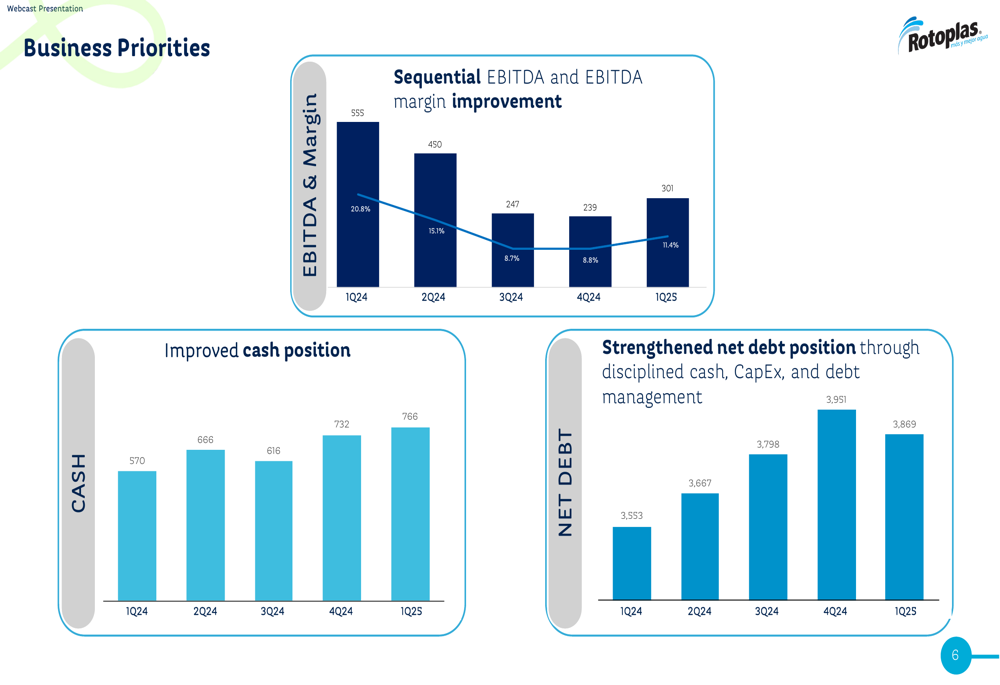

Despite these year-over-year declines, Rotoplas highlighted sequential improvements in its financial performance. EBITDA and EBITDA margin have shown consistent growth over the past three quarters, recovering from lows in Q4 2024:

Regional Performance Analysis

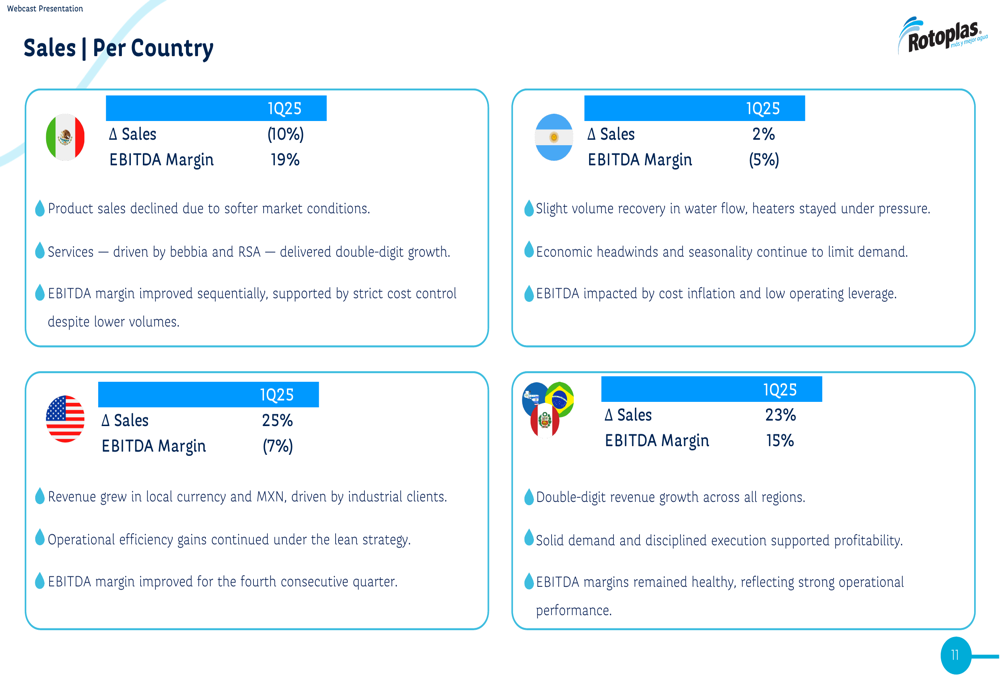

Rotoplas’ performance varied significantly across its geographic markets, with strong growth in the United States and other Latin American countries partially offsetting weakness in Mexico:

Mexico, the company’s largest market, experienced a 10% sales decline due to softer market conditions, though it maintained a healthy 19% EBITDA margin. The services segment in Mexico continued to show growth, driven by Bebbia and RSA.

The United States stood out with 25% sales growth, though it still operates at a negative 7% EBITDA margin. Management expressed optimism about reaching EBITDA breakeven in the US before 2026.

Other Latin American markets (excluding Argentina) delivered impressive 23% sales growth with a solid 15% EBITDA margin, demonstrating strong performance across all regions within this segment.

Argentina showed modest 2% sales growth but continues to face economic headwinds, resulting in a negative 5% EBITDA margin. The company noted slight volume recovery in water flow products and expressed cautious optimism about market recovery.

Strategic Initiatives and Business Priorities

Rotoplas outlined three key business priorities focused on sustainable growth, service development, and digital transformation:

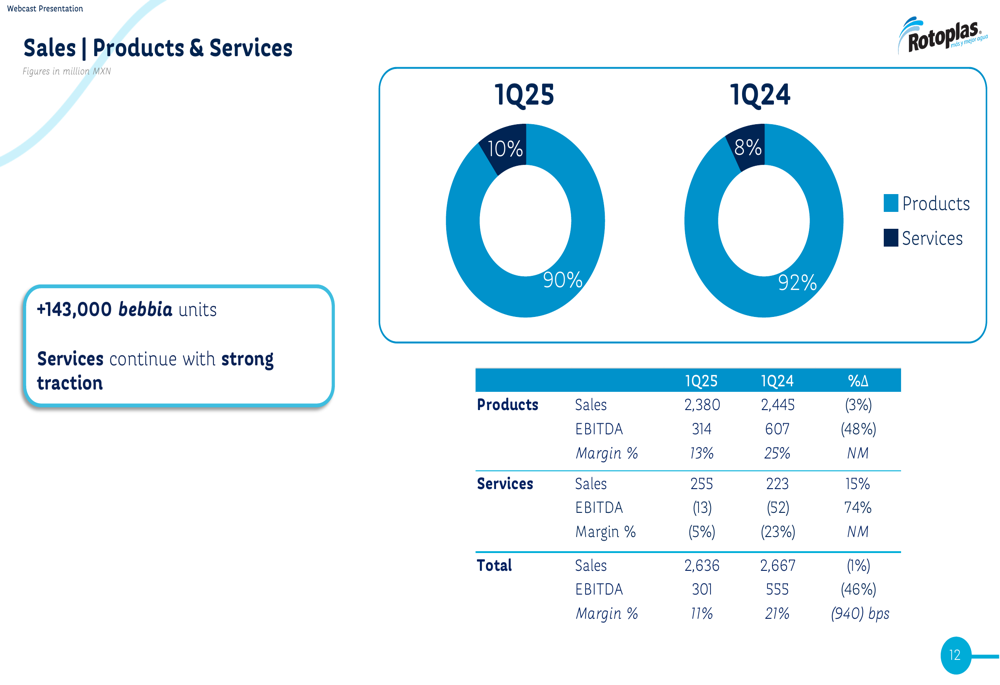

The company continues to push its services segment, with Bebbia water purification service surpassing 143,000 subscribers. While the services segment generated 255 million pesos in revenue (approximately 10% of total sales), it still operates at a negative 5% EBITDA margin:

Management emphasized their focus on tight cost and expense management, operational efficiency, and long-term value creation. This disciplined approach is particularly important as the company navigates challenging market conditions while investing in future growth areas.

Cash Position and Capital Allocation

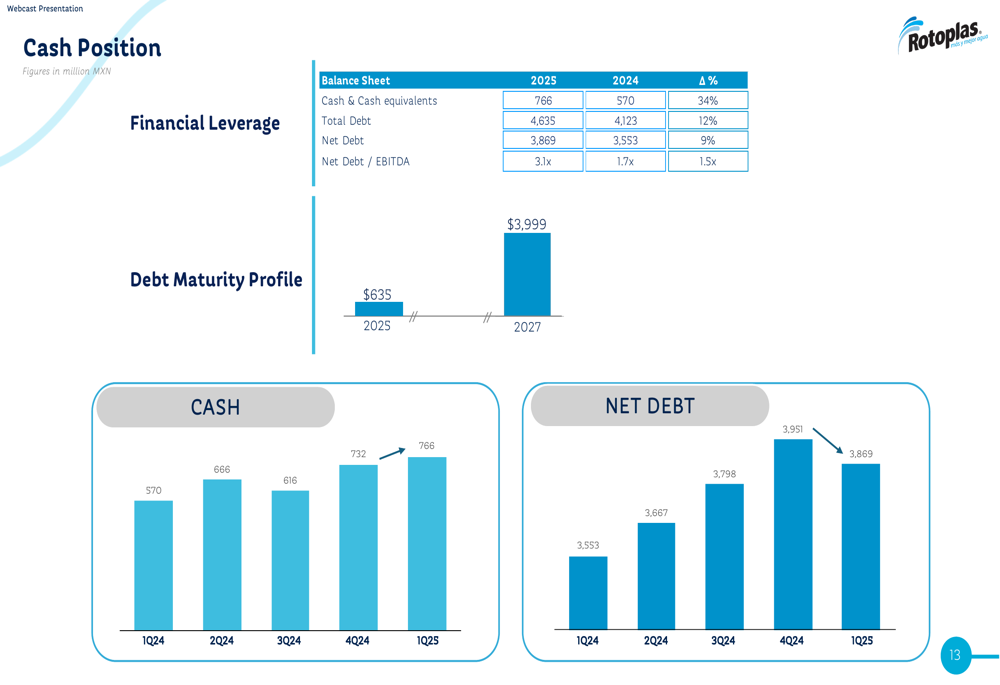

Despite profitability challenges, Rotoplas improved its cash position by 34% year-over-year to 766 million pesos. However, total debt increased by 12% to 4,635 million pesos, resulting in net debt of 3,869 million pesos and a net debt/EBITDA ratio of 3.1x:

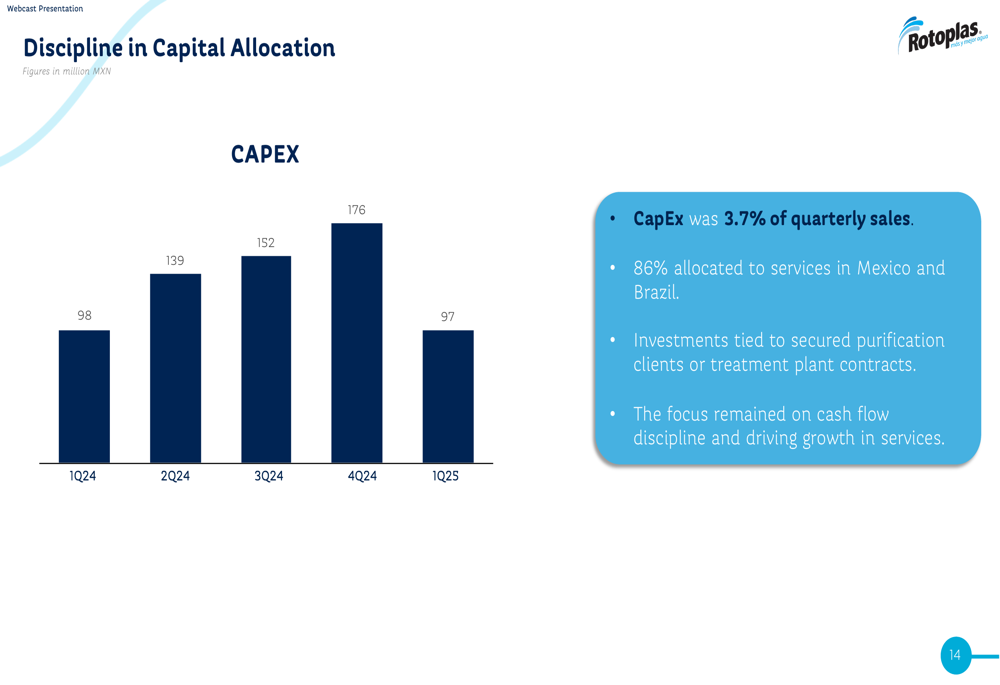

The company maintained discipline in capital allocation, with Q1 2025 CAPEX of 97 million pesos representing 3.7% of quarterly sales, down from 98 million pesos in Q1 2024. The majority (86%) of this investment was directed toward services in Mexico and Brazil, focusing on secured purification clients:

Forward-Looking Statements

Rotoplas highlighted its sustainability achievements in its 2024 Annual Integrated Report, including a 17% reduction in water intensity and a 12% decrease in Scope 1 & 2 CO₂e emissions intensity:

Looking ahead, the company expects to maintain its focus on sequential improvements across its businesses. Management anticipates reaching EBITDA breakeven in the services segment and achieving positive EBITDA in US operations before 2026. The company also expressed optimism about Argentina’s market recovery, which could contribute to future growth.

With a continued emphasis on cost discipline, operational efficiency, and strategic investments in high-growth areas like services and digital transformation, Rotoplas aims to navigate current challenges while positioning itself for long-term success in the water solutions market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.