Adaptimmune stock plunges after announcing Nasdaq delisting plans

Introduction & Market Context

Laboratorios Farmaceuticos ROVI (BME:ROVI) presented its financial results for the first half of 2025 on July 24, revealing a complex performance landscape where strong specialty pharmaceutical growth partially counterbalanced weakness in its contract manufacturing business. The company’s stock closed at €58.45 on October 14, down 0.43% for the session, and currently trades significantly below its 52-week high of €80.20.

The Spanish pharmaceutical company’s results reflect a strategic transition period, with management characterizing 2025 as a foundation-building year focused on long-term growth despite near-term revenue challenges.

Executive Summary

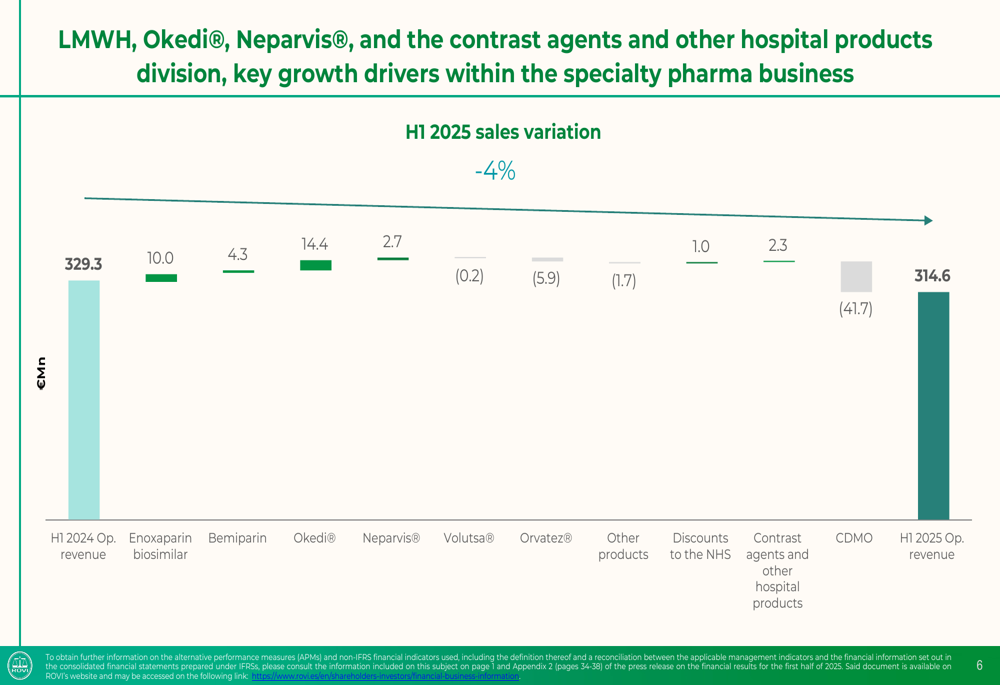

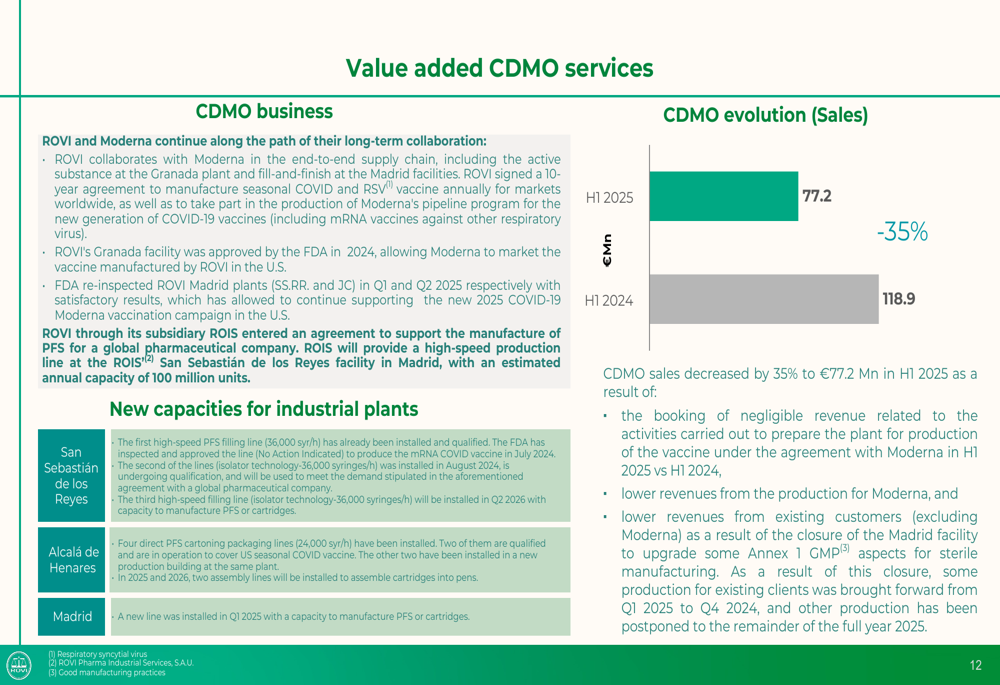

ROVI reported total operating revenue of €314.6 million for H1 2025, representing a 4% decrease compared to the same period in 2024. This decline was primarily driven by a 35% drop in Contract Development and Manufacturing Organization (CDMO) revenue, which fell to €77.2 million.

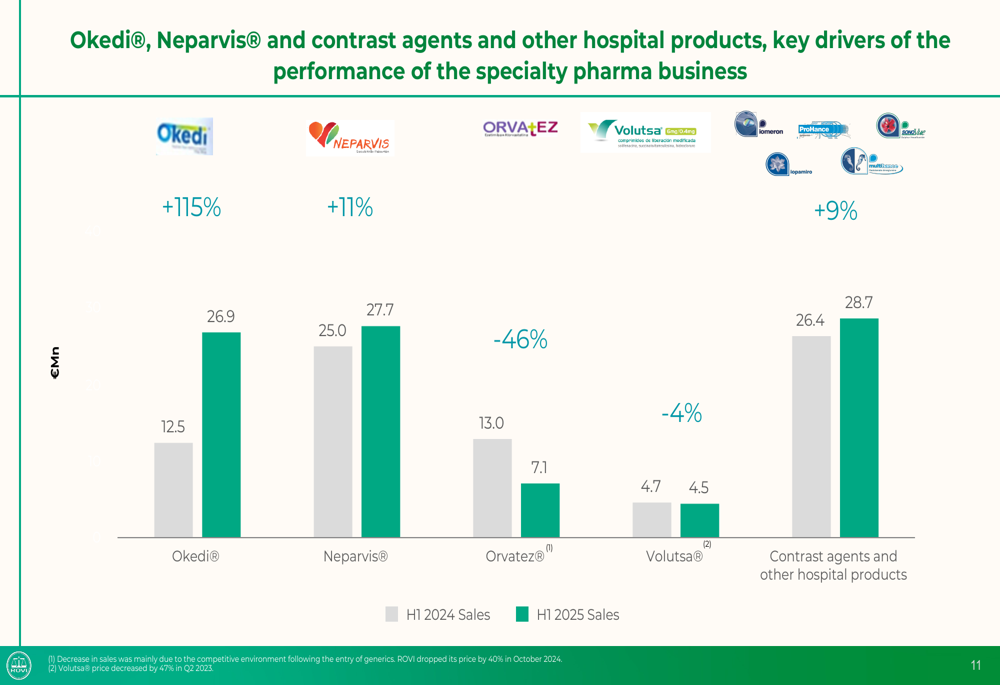

However, the company’s specialty pharmaceutical business demonstrated robust performance, growing 13% year-over-year to €237.4 million. Particularly impressive was Okedi®, which saw sales surge 115% to €26.9 million, while the heparin franchise increased 12% to €135.2 million.

As shown in the following breakdown of sales variation by division:

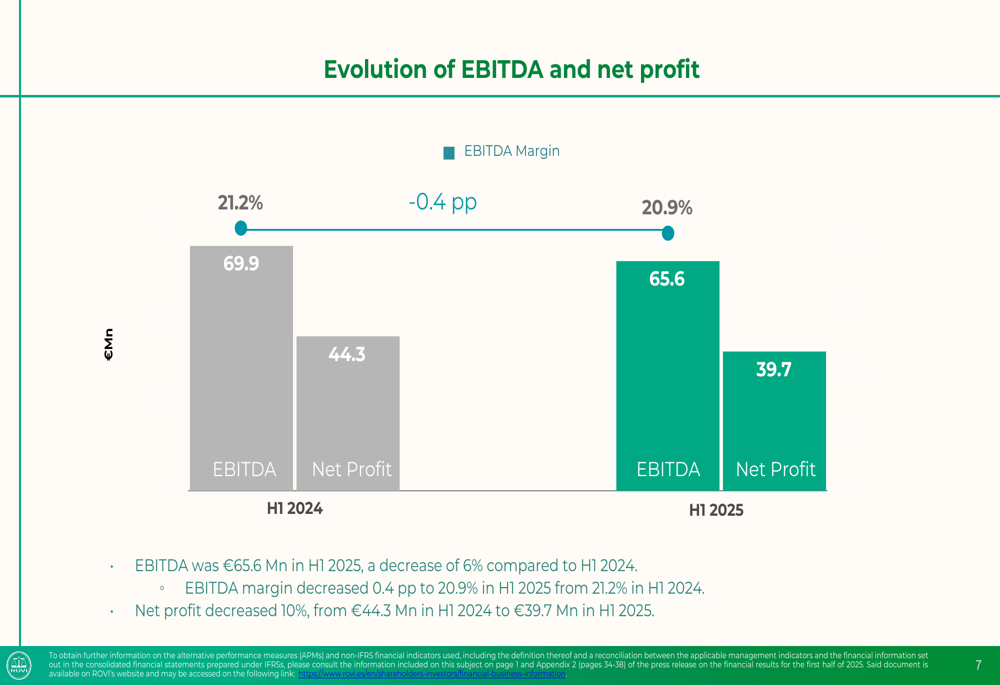

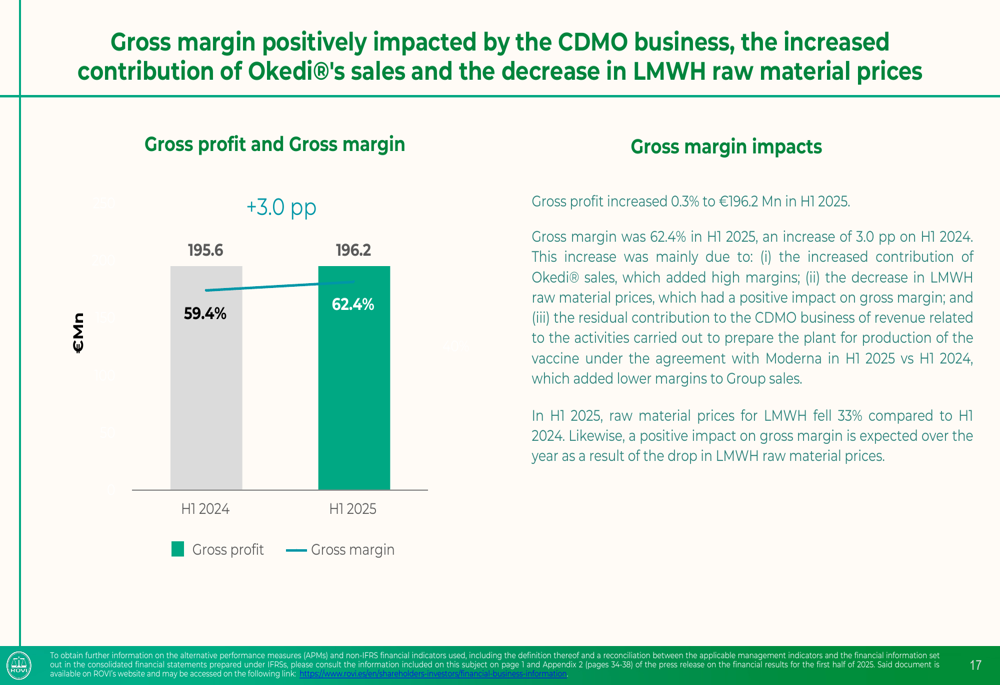

Gross margin improved significantly to 62.4%, up 3.0 percentage points from H1 2024, driven by increased contribution from higher-margin products and lower raw material costs. Despite this improvement, EBITDA decreased 6% to €65.6 million, and net profit fell 10% to €39.7 million, reflecting increased R&D investments.

Detailed Financial Analysis

The company’s EBITDA and net profit performance shows the impact of strategic investments against the backdrop of revenue challenges:

ROVI’s gross margin improvement stands out as a bright spot in the financial results. The 3.0 percentage point increase to 62.4% was attributed to two primary factors: the increased contribution of higher-margin Okedi® sales and a decrease in low molecular weight heparin (LMWH) raw material prices.

As illustrated in this gross margin analysis:

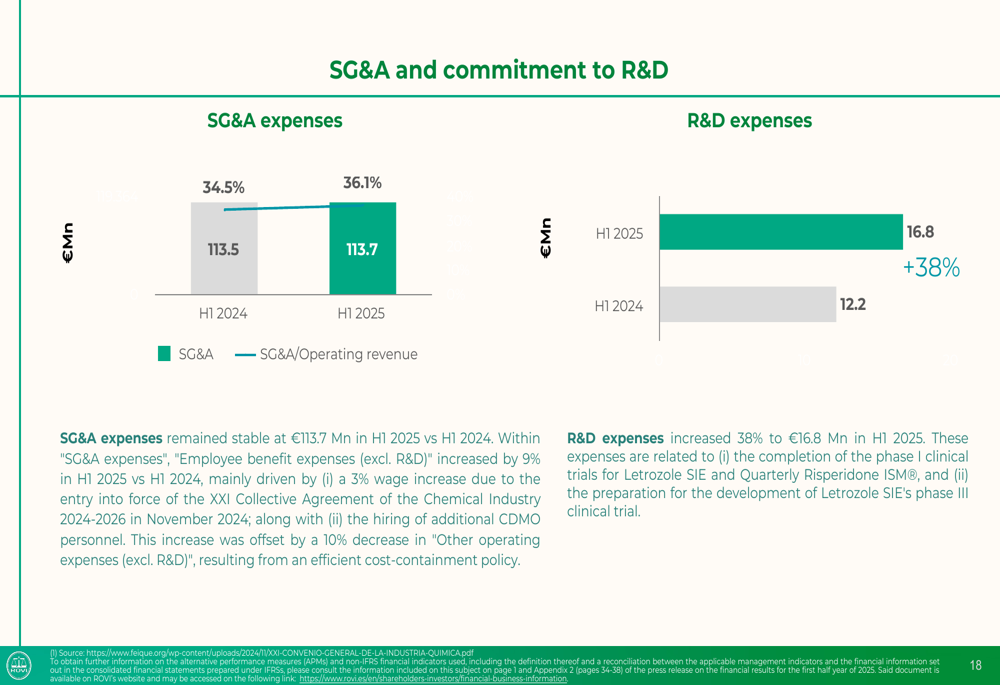

The company maintained stable selling, general, and administrative (SG&A) expenses at €113.7 million while significantly increasing R&D investment by 38% to €16.8 million. This strategic allocation of resources demonstrates ROVI’s commitment to future growth despite current revenue headwinds.

When excluding R&D expenses, ROVI’s underlying financial performance appears more stable. Pre-R&D EBITDA increased slightly by 0.4% to €82.4 million, suggesting that core operations remain solid while the company invests in future innovations.

Strategic Initiatives & Product Performance

ROVI’s heparin franchise continues to be a cornerstone of its business, representing 43% of operating revenue in H1 2025, up from 37% in H1 2024. The company’s enoxaparin biosimilar has been approved in 26 European countries and 33 countries in other regions, with direct marketing in seven European markets and distribution agreements covering 81 territories globally.

The company’s internationalization strategy shows a slight shift in geographical revenue distribution:

Okedi® emerged as a standout performer with 115% growth, while Neparvis® also showed strong momentum with an 11% increase. Contrast agents and other hospital products grew by 9%, helping to offset declines in other areas such as Orvatez (-46%) and Volutsa (-4%).

The CDMO business, which includes ROVI’s collaboration with Moderna, experienced a significant 35% decline in H1 2025. Despite this setback, management emphasized the continuation of their long-term partnership with Moderna and noted that the FDA had re-inspected ROVI’s Madrid manufacturing facilities.

ROVI also highlighted two significant milestones achieved in H1 2025: securing a €36.3 million subsidy from the Technological Development and Innovation Centre (CDTI) for its LAISOLID project, and acquiring a majority position in Cells IA Technologies, an artificial intelligence company specializing in pathological anatomy.

Forward-Looking Statements

Looking ahead, ROVI anticipates a mid-single-digit percentage decrease in operating revenue for the full year 2025 compared to 2024. The company identified two key growth levers for the future: its specialty pharmaceutical business and the CDMO division.

For specialty pharmaceuticals, ROVI plans to launch Risperidone ISM in new countries while securing additional product distribution licenses. The CDMO business will continue to focus on its agreement with Moderna while increasing manufacturing capacity.

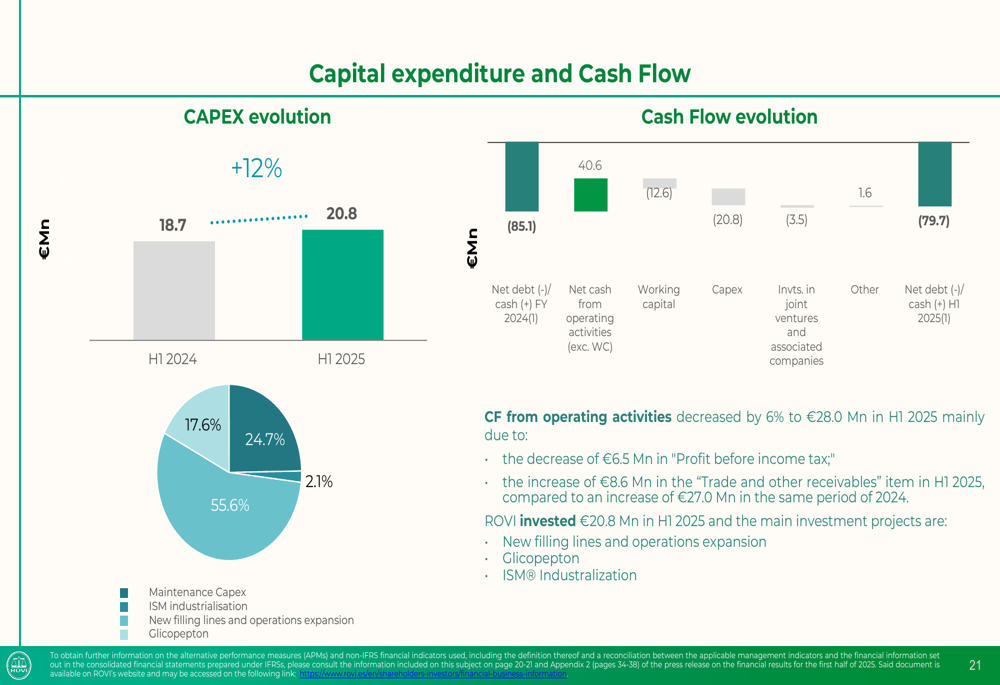

Capital expenditures increased by 12% to €20.8 million in H1 2025, primarily directed toward new filling lines and operations expansion. This investment underscores management’s confidence in long-term growth prospects despite near-term challenges.

CEO Juan López-Belmonte characterized 2025 as "a transition year in which the company continues to invest, laying the foundation for sustainable growth and value creation in the years ahead." This perspective frames the current financial results as part of a longer-term strategic vision rather than a concerning trend.

With a solid balance sheet showing €79.7 million in net debt and continued investment in R&D and manufacturing capacity, ROVI appears positioned to weather the current revenue challenges while building capabilities for future growth. Investors will be watching closely to see if the company’s strategic investments translate into renewed momentum in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.