Elastic launches GPU-accelerated inference service for AI workflows

Introduction & Market Context

Ryder System Inc (NYSE:R) presented its second quarter 2025 earnings results on July 24, 2025, highlighting continued progress in its strategic transformation toward a more asset-light business model. The transportation and logistics company reported an 11% increase in comparable earnings per share despite mixed market conditions, demonstrating the resilience of its evolving business model.

The company’s stock closed at $172.82 on July 23, representing a 0.62% increase, and has traded between $123.36 and $177.40 over the past 52 weeks. This performance follows a slight earnings miss in Q1 2025, when Ryder reported EPS of $2.46 versus an expected $2.47.

Quarterly Performance Highlights

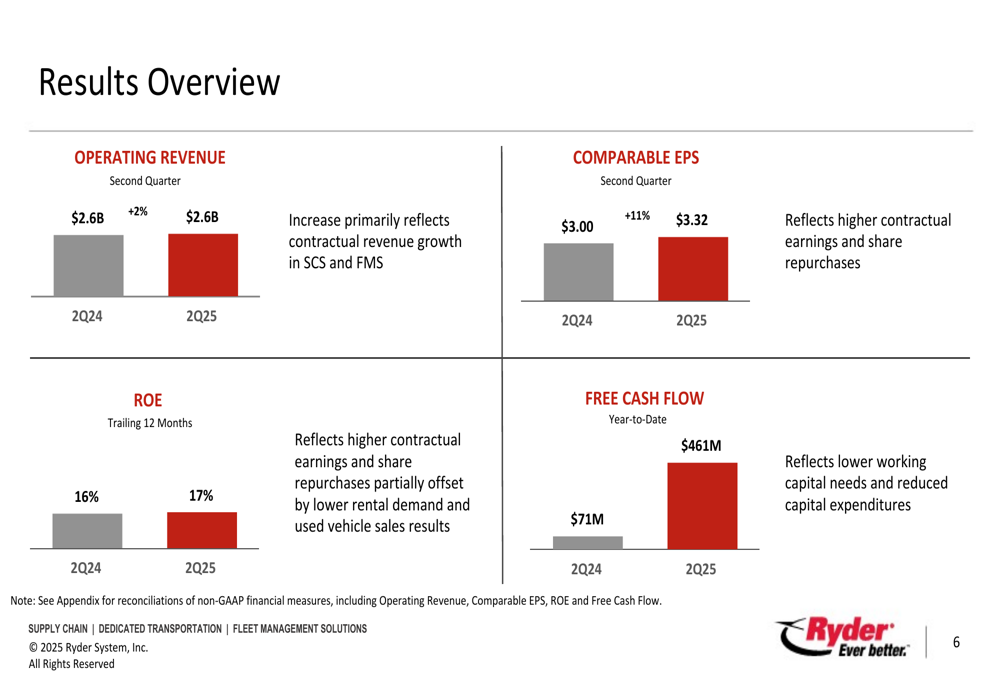

Ryder reported Q2 2025 operating revenue of $2.6 billion, a 2% increase compared to the same period in 2024. Comparable earnings per share rose 11% to $3.32, up from $3.00 in Q2 2024, while return on equity improved to 17% from 16% a year earlier. Free cash flow saw dramatic improvement, reaching $461 million year-to-date compared to just $71 million in the prior-year period.

As shown in the following results overview, Ryder’s performance metrics demonstrated solid improvement across key financial indicators:

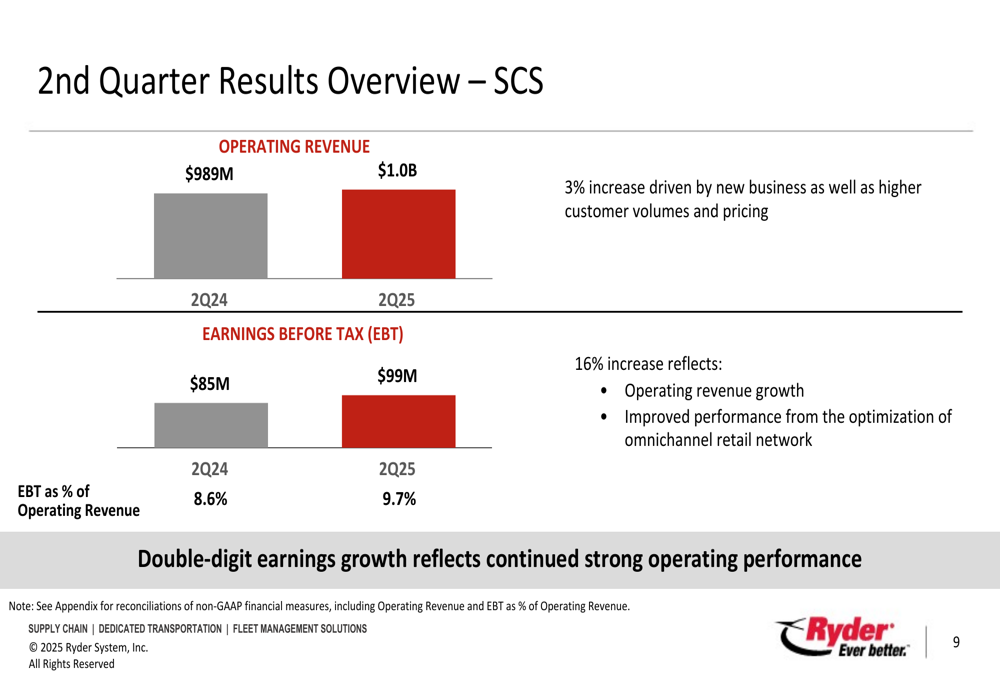

The company’s Supply Chain Solutions (SCS) segment was a standout performer, with earnings before tax increasing 16% to $99 million and operating margins improving to 9.7% from 8.6% in Q2 2024. This strong performance reflects revenue growth and improved efficiency in Ryder’s omnichannel retail network.

Meanwhile, the Fleet Management Solutions (FMS) segment faced some headwinds, with earnings before tax decreasing from $133 million to $126 million due to lower used vehicle sales and pricing pressure. The Dedicated Transportation Solutions (DTS) segment maintained stable earnings despite a 3% revenue decline, with earnings before tax of $37 million and improved margins of 7.9%.

Business Transformation Progress

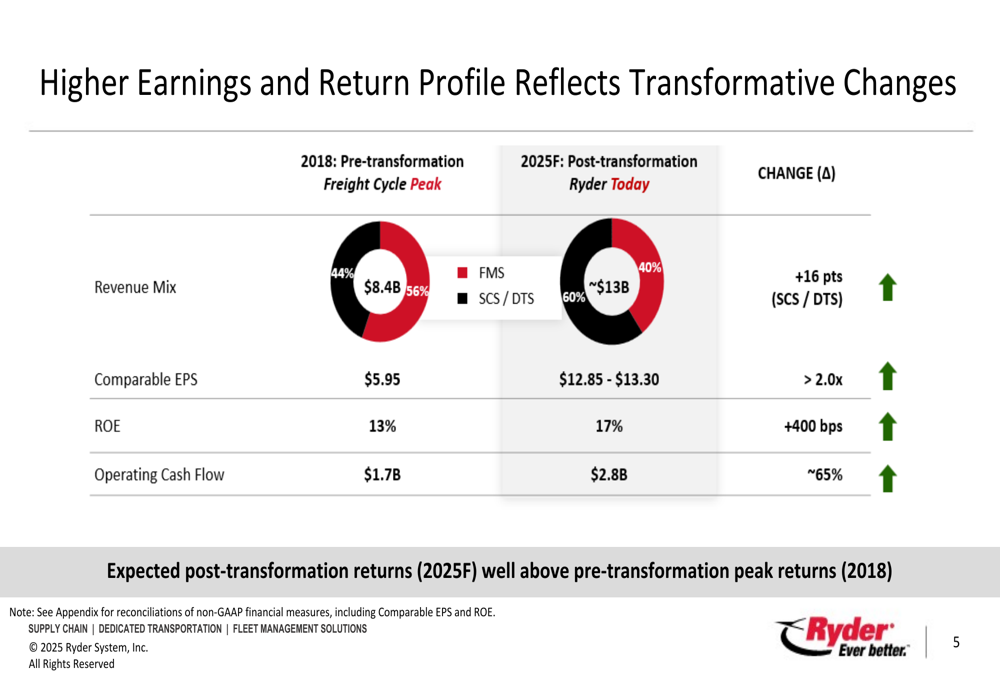

Ryder’s presentation emphasized the company’s ongoing transformation from a capital-intensive fleet management business toward a more balanced model with greater emphasis on supply chain and dedicated transportation services. This shift is designed to deliver higher returns and more stable earnings throughout economic cycles.

The following chart illustrates the dramatic improvement in Ryder’s financial profile since beginning this transformation:

As shown above, Ryder has shifted its revenue mix from 44% FMS/56% SCS+DTS in 2018 to a projected 40% FMS/60% SCS+DTS in 2025, while more than doubling comparable EPS from $5.95 to a projected $12.85-$13.30. Return on equity has improved from 13% to 17%, and operating cash flow has grown from $1.7 billion to $2.8 billion.

The company’s used vehicle sales segment showed mixed results, with tractor prices declining 17% compared to both Q2 2024 and Q1 2025, while truck prices increased 3% year-over-year but fell 10% sequentially. Used vehicle inventory stood at 9,600 units, slightly above Ryder’s long-term target range of 7,000-9,000 units.

Capital Allocation & Cash Flow

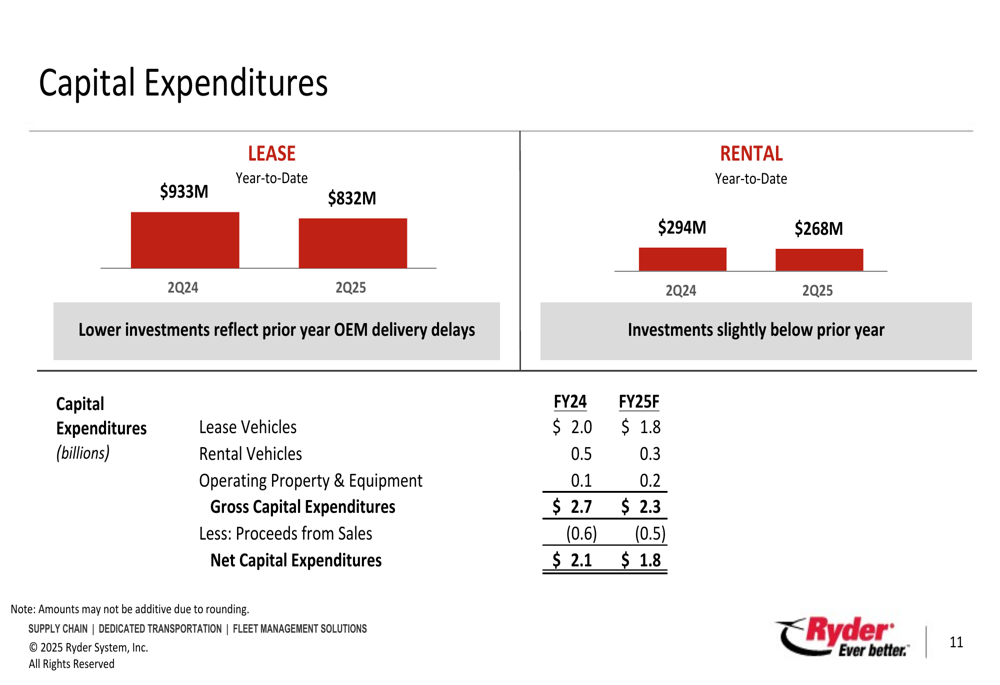

Ryder highlighted significant improvements in capital efficiency and cash flow generation. The company reduced its capital expenditure forecast for 2025 to $2.3 billion, down from $2.7 billion in 2024, while maintaining its growth initiatives.

The following slide details Ryder’s capital expenditure plans:

The improved cash flow has enabled Ryder to increase shareholder returns, with a 12% increase in the quarterly dividend and $330 million returned to shareholders through dividends and share repurchases. The company also raised its full-year 2025 free cash flow forecast to $900 million to $1 billion, up $500 million from previous guidance.

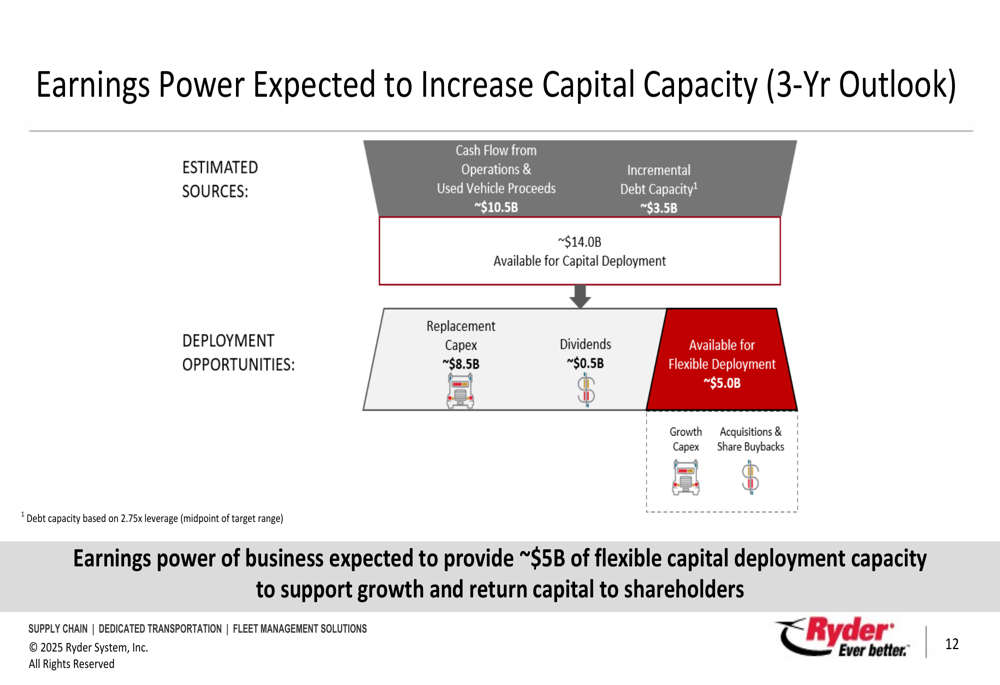

Ryder’s three-year capital deployment outlook reveals substantial financial flexibility:

This capital capacity projection shows approximately $14 billion available for deployment over the next three years, with about $5 billion available for flexible allocation between growth capital expenditures, acquisitions, and share repurchases after accounting for replacement capital expenditures and dividends.

Outlook & Strategic Initiatives

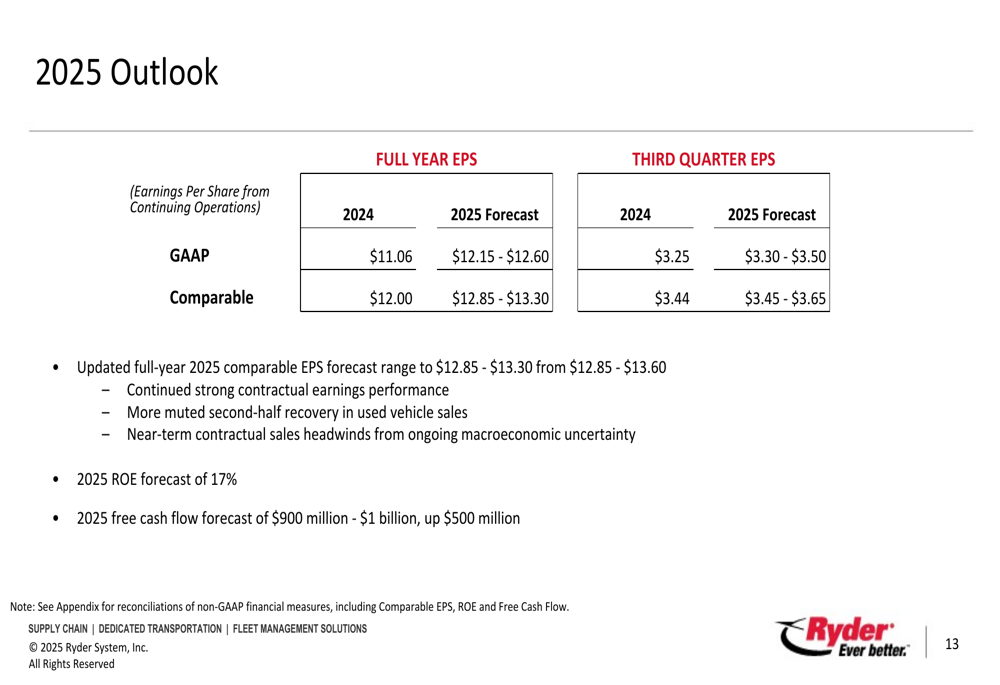

Ryder raised its full-year 2025 guidance, projecting comparable EPS of $12.85-$13.30, up from its previous forecast. For the third quarter, the company expects comparable EPS of $3.45-$3.65.

The detailed outlook is presented in the following slide:

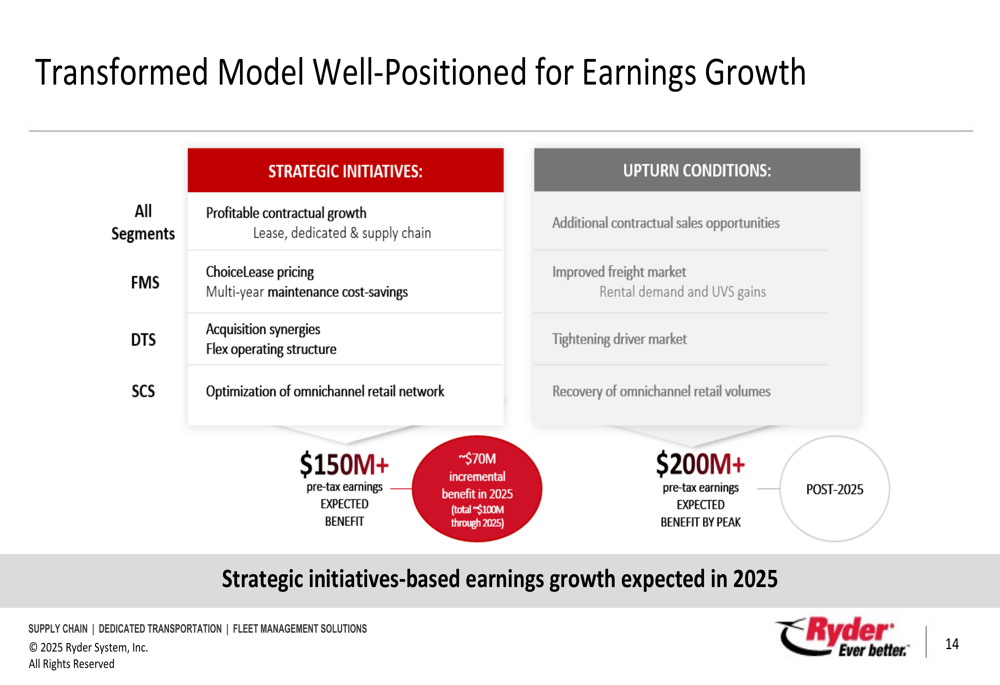

The company’s strategic initiatives are expected to generate over $150 million in pretax earnings benefits, with an additional $200+ million potential benefit during market upturn conditions. These initiatives include profitable contractual growth across all segments, ChoiceLease pricing improvements in FMS, acquisition synergies in DTS, and optimization of the omnichannel retail network in SCS.

Ryder emphasized that its transformed business model is designed to achieve higher returns throughout economic cycles while maintaining growth opportunities. The company’s long-term targets include ROE in the low twenties, operating revenue growth in high single digits, and EBT as a percentage of operating revenue in the low teens.

In conclusion, Ryder’s Q2 2025 results demonstrate continued progress in its strategic transformation, with improved earnings, strong cash flow generation, and increased shareholder returns. While some segments face market challenges, the company’s shift toward a more balanced, asset-light business model appears to be delivering the intended benefits of higher returns and more stable earnings.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.