With uncertainty rising, is gold’s bull run far from over?

Introduction & Market Context

Steel Authority of India Limited (SAIL) released its Q1 FY’26 results on July 28, 2025, showing significant year-over-year improvement in profitability despite challenging global steel market conditions. The company’s stock (NSE:SAIL) fell 4.11% to Rs. 125.30 following the announcement, suggesting investors may have expected even stronger results.

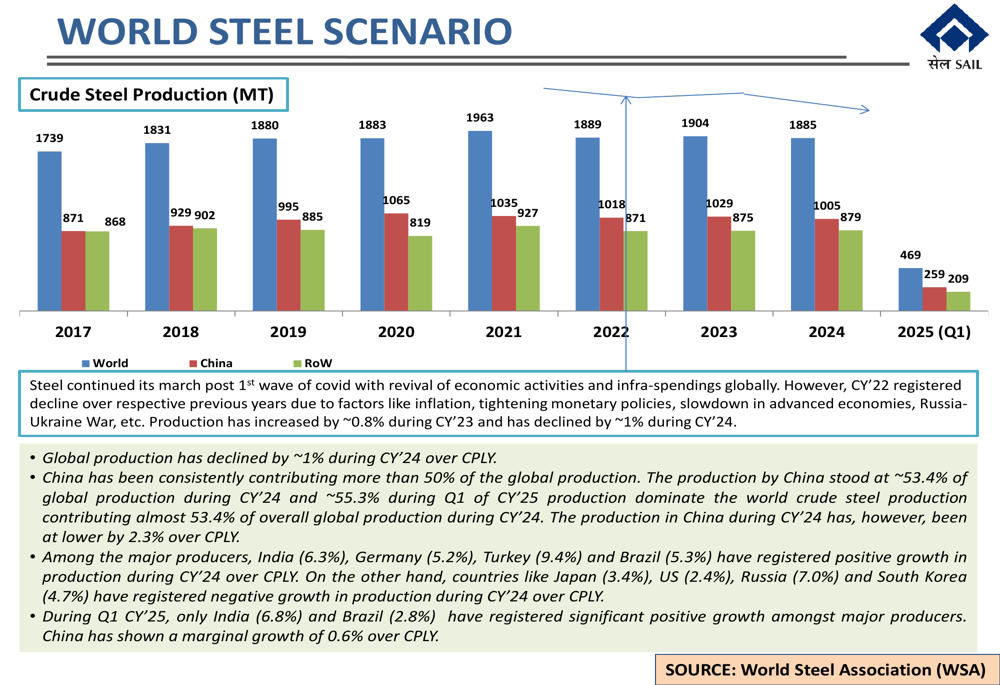

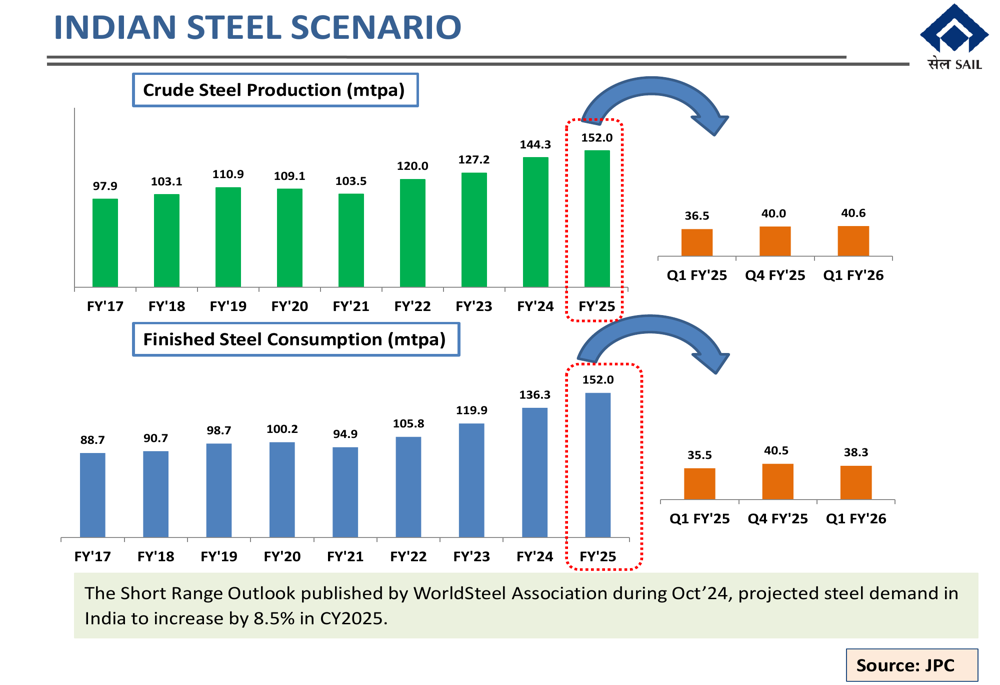

The presentation highlighted that global steel production declined by approximately 1% during calendar year 2024, with China continuing to dominate with more than 50% of global production. However, India, Germany, Turkey, and Brazil registered positive growth during this period.

As shown in the following chart of global crude steel production trends:

The World Steel Association projects steel demand in India to increase by 8.5% in CY2025, significantly outpacing global growth. This positive outlook for domestic demand provides a favorable backdrop for SAIL’s operations.

Quarterly Performance Highlights

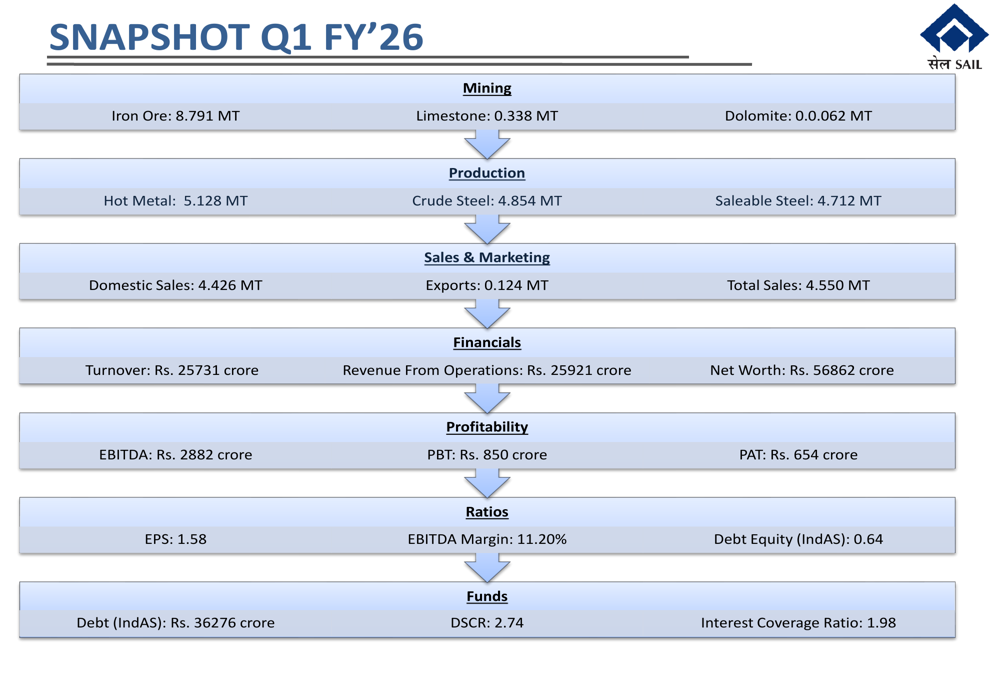

SAIL reported substantial improvement in its financial performance for Q1 FY’26 compared to the same quarter last year. The company’s Profit After Tax (PAT) surged to Rs. 685 crore, compared to just Rs. 11 crore in Q1 FY’25, representing a remarkable 62-fold increase.

The comprehensive snapshot of SAIL’s Q1 FY’26 performance across key operational and financial metrics is illustrated below:

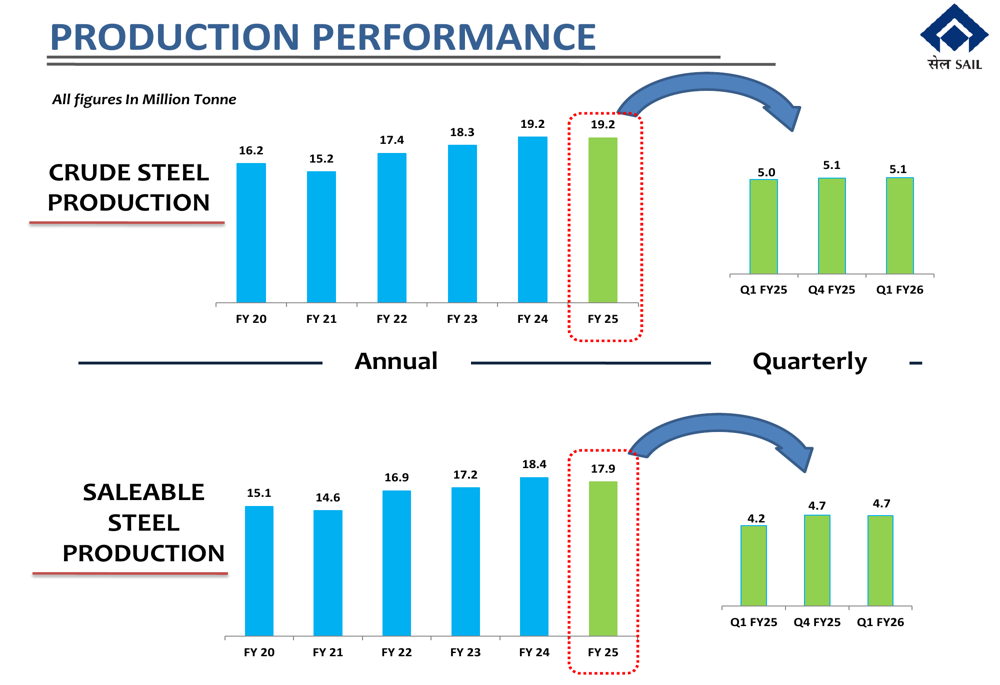

Production volumes showed improvement, with crude steel production reaching 5.1 million tonnes in Q1 FY’26, up from 5.0 million tonnes in Q1 FY’25. More significantly, saleable steel production increased to 4.7 million tonnes from 4.2 million tonnes in the same period last year.

The production performance trends are visualized in the following chart:

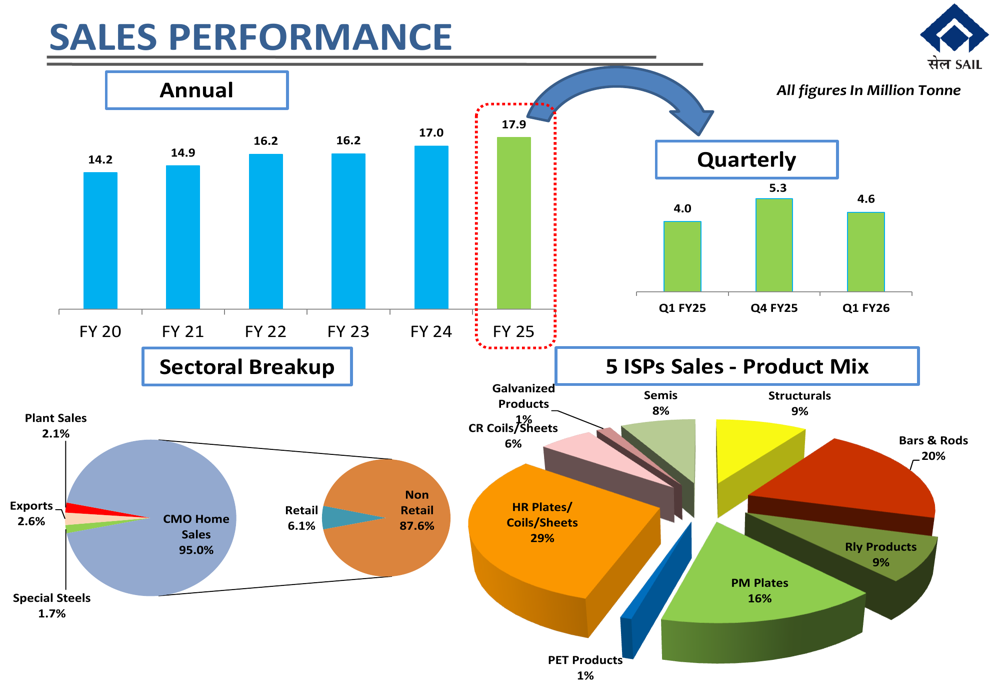

Sales volumes also increased substantially to 4.6 million tonnes in Q1 FY’26, compared to 4.0 million tonnes in Q1 FY’25, representing a 15% year-over-year growth. The sales breakdown by sector and product mix is detailed below:

Operational Improvements

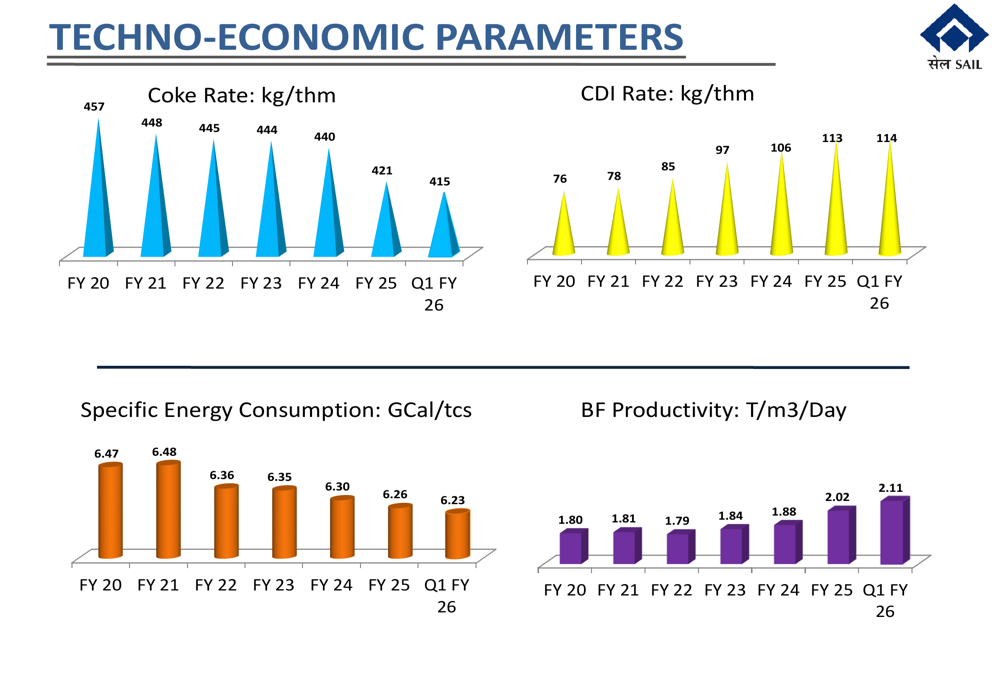

SAIL continued to make progress in operational efficiency during the quarter. Key techno-economic parameters showed improvement, with coke rate reduced to 415 kg/thm in Q1 FY’26 from 421 kg/thm in FY’25, and blast furnace productivity improved to 2.11 T/m³/day from 2.02 T/m³/day.

The company’s specific energy consumption also decreased to 6.23 GCal/tcs in Q1 FY’26 from 6.26 GCal/tcs in FY’25, reflecting ongoing efforts to optimize resource utilization.

These operational improvements are illustrated in the following chart:

Labor productivity also showed positive trends, reaching 643 tcs/man/year in Q1 FY’26, compared to 592 tcs/man/year in Q1 FY’25. The company continued its manpower optimization, with total workforce reducing by 1,017 during the quarter to 52,142 as of July 1, 2025.

Financial Analysis

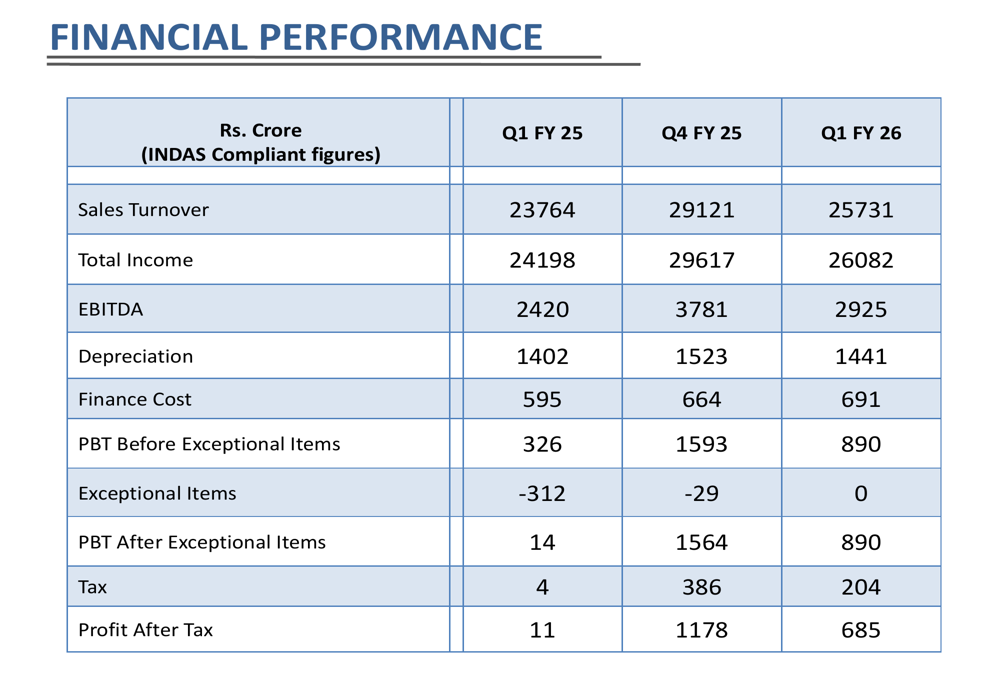

SAIL’s financial performance for Q1 FY’26 showed marked improvement across key metrics compared to the same period last year. Revenue from operations reached Rs. 25,921 crore, while EBITDA stood at Rs. 2,925 crore, representing an EBITDA margin of 11.20%.

The detailed financial figures for the quarter compared to previous periods are presented below:

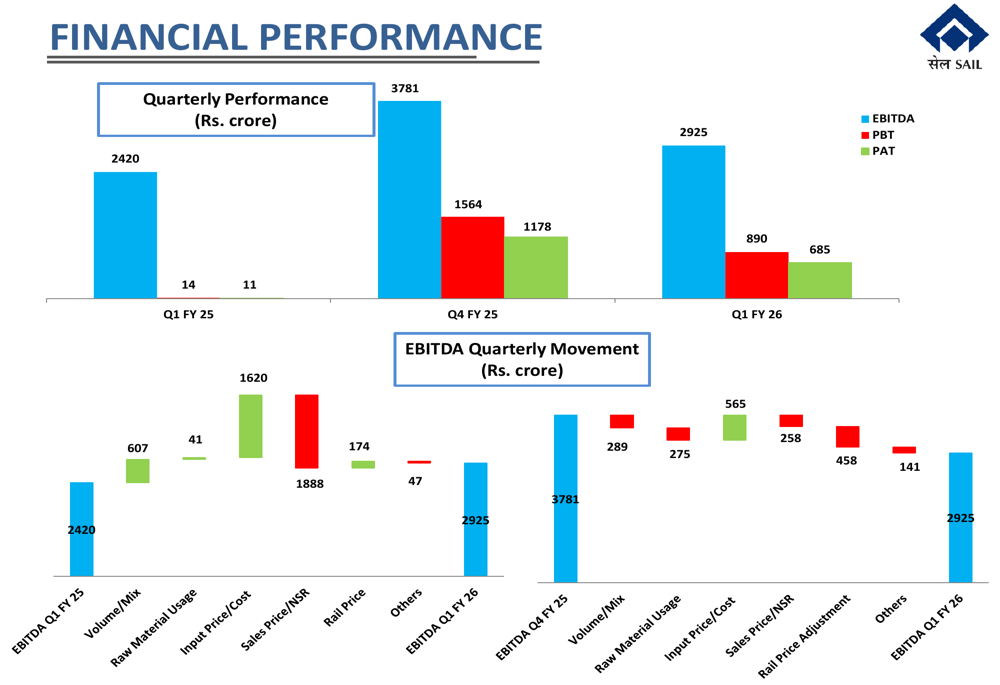

The company’s EBITDA, PBT, and PAT showed significant improvement on a year-over-year basis, though there was some sequential decline compared to Q4 FY’25. The quarterly movement in EBITDA, broken down by contributing factors, is visualized in the following chart:

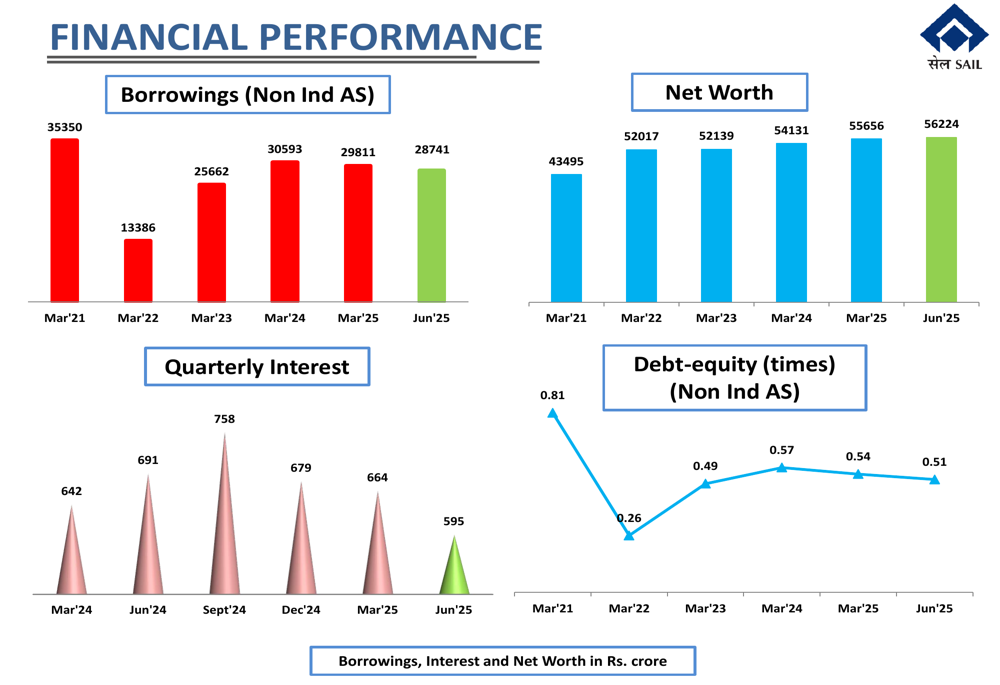

SAIL’s financial position continued to strengthen, with net worth increasing to Rs. 56,224 crore as of June 30, 2025, up from Rs. 55,656 crore as of March 31, 2025. The company’s borrowings (Non Ind AS) decreased to Rs. 28,741 crore from Rs. 29,811 crore during the same period, improving the debt-equity ratio to 0.51 times.

The trends in borrowings, net worth, and debt-equity ratio are illustrated in the following chart:

Sustainability Initiatives

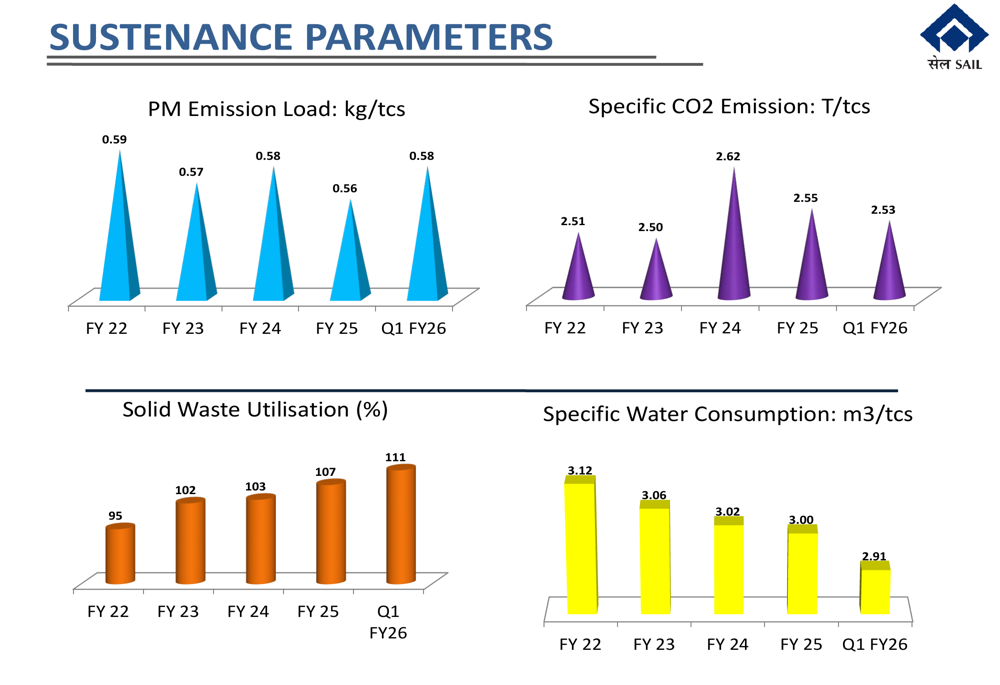

SAIL demonstrated progress in its sustainability parameters during Q1 FY’26. Notably, solid waste utilization reached 111%, indicating that the company is not only utilizing all of its current waste but also processing previously accumulated waste.

Specific water consumption decreased to 2.91 m³/tcs in Q1 FY’26 from 3.00 m³/tcs in FY’25, reflecting improved water management practices. The company’s specific CO2 emissions also showed a slight reduction to 2.53 T/tcs from 2.55 T/tcs.

These sustainability metrics are visualized in the following chart:

The company highlighted its ongoing Corporate Social Responsibility (CSR) initiatives, with total CSR spending since FY’15 reaching approximately Rs. 716 crore. Key focus areas include education (26% of spending), healthcare (11%), and drinking water & sanitation (9%).

Forward-Looking Statements

Looking ahead, SAIL is positioned to benefit from the projected 8.5% growth in Indian steel demand for CY2025, as forecasted by the World Steel Association. The domestic steel consumption trends, as shown in the presentation, indicate a robust market environment:

The company’s continued focus on operational efficiency, cost reduction, and sustainability initiatives is expected to support margin improvement in the coming quarters. However, global steel market volatility and input cost pressures remain potential challenges.

With its improved financial position, reduced debt levels, and enhanced operational parameters, SAIL appears well-positioned to capitalize on the growing domestic steel demand while navigating the challenges in the global steel industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.