Gold rally takes a breather amid Gaza ceasefire, Fed minutes

Introduction & Market Context

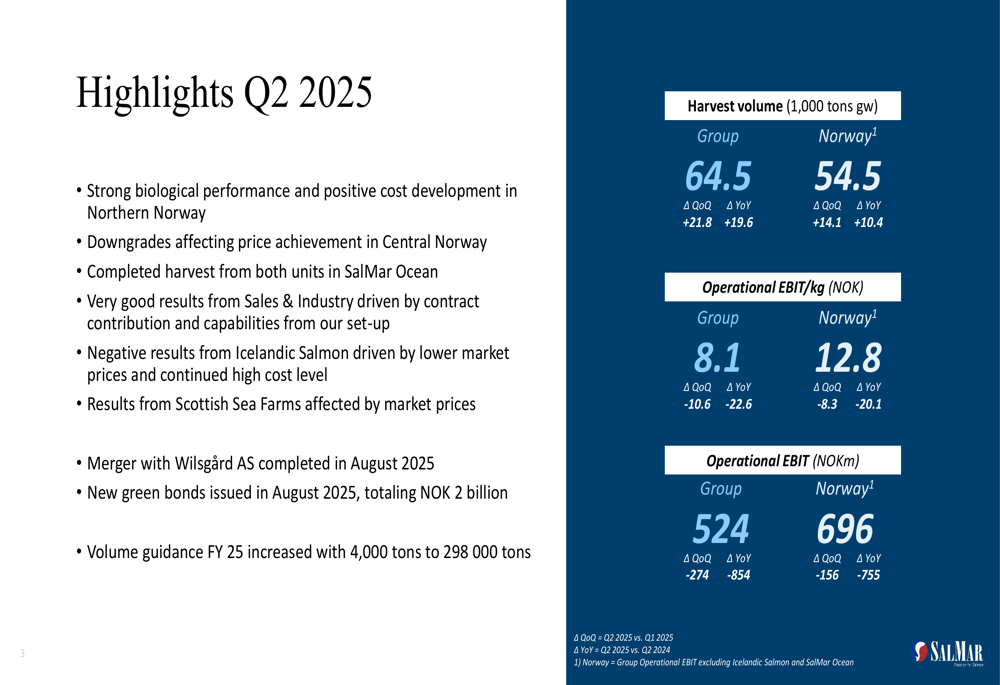

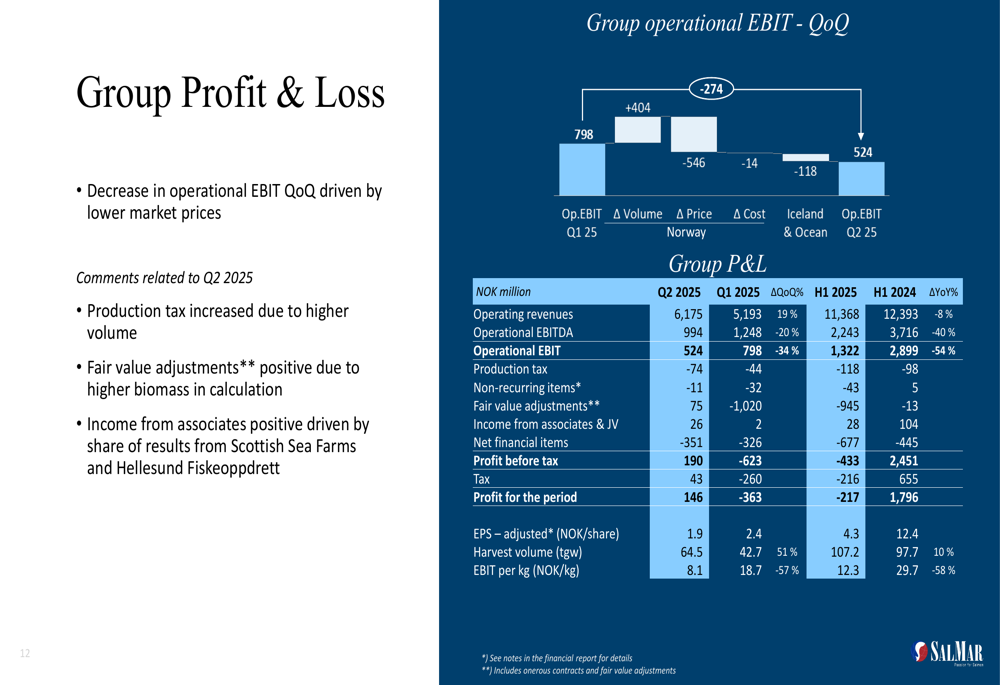

SalMar ASA (OB:SALM) presented its second quarter 2025 results on August 21, revealing a mixed performance across its operating regions while maintaining an optimistic outlook for the remainder of the year. The Norwegian salmon producer reported a profit of NOK 146 million for the period, a significant improvement from the NOK 363 million loss reported in Q1 2025. Despite this recovery, the company’s operational EBIT declined to NOK 524 million from NOK 798 million in the previous quarter.

SalMar’s stock closed at NOK 600.6 following the presentation, having gained 1.52% as investors responded positively to the company’s strategic initiatives and increased volume guidance for the full year, despite the operational challenges in some regions.

Quarterly Performance Highlights

SalMar reported a Group Operational EBIT of NOK 524 million on a harvest volume of 64,500 tonnes, resulting in an Operational EBIT per kg of NOK 8.1. These results reflect a diverse regional performance, with Northern Norway delivering strong biological results while Central Norway and international operations faced significant headwinds.

As shown in the following quarterly highlights slide:

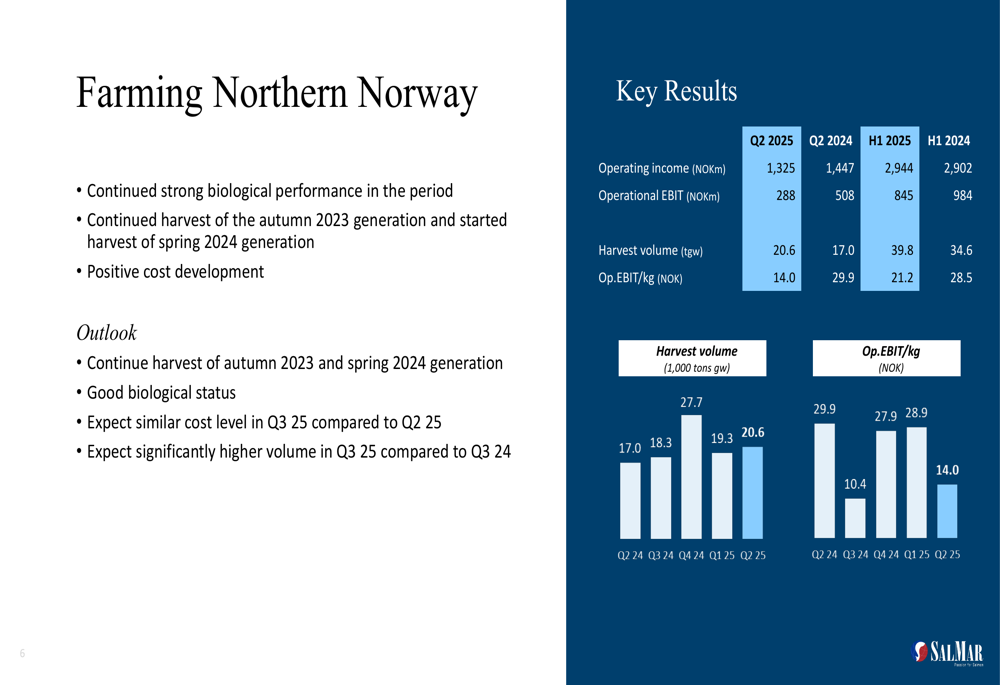

The company’s Northern Norway operations emerged as the standout performer, achieving an Operational EBIT of NOK 288 million on 20,600 tonnes harvested, translating to NOK 14.0 per kg. This strong performance was attributed to excellent biological conditions and positive cost development in the region.

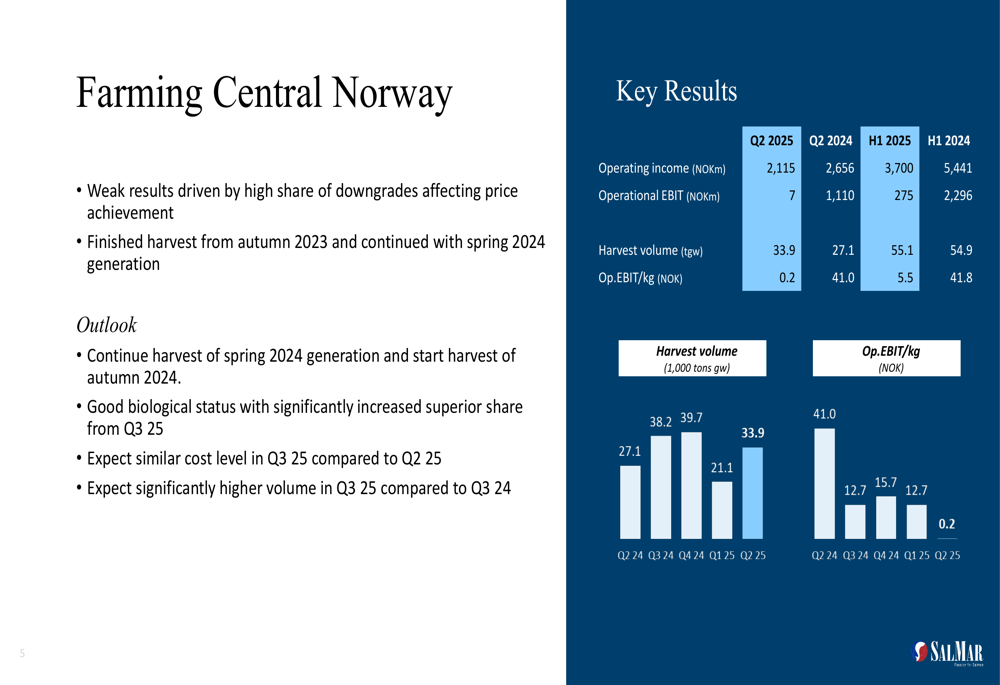

In contrast, Central Norway struggled with a high proportion of downgraded salmon affecting price achievement, resulting in a minimal Operational EBIT of just NOK 7 million on 33,900 tonnes harvested (NOK 0.2 per kg).

The regional performance breakdown shows stark differences in profitability:

International operations also faced challenges, with Icelandic Salmon reporting negative results (NOK -97 million Operational EBIT) due to biological challenges and high costs throughout the value chain. Similarly, Scottish Sea Farms reported an Operational EBIT of NOK -28 million, primarily affected by lower market prices despite good harvest weights and biological development.

Strategic Initiatives

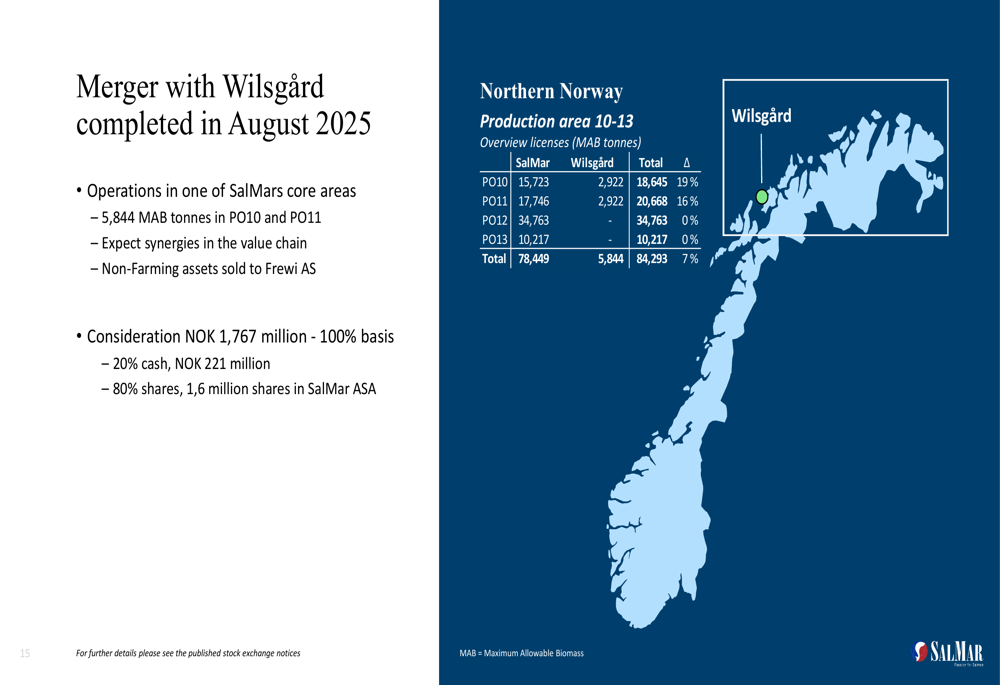

A significant development during the quarter was SalMar’s completion of its merger with Wilsgård AS in August 2025, strengthening the company’s position in one of its core operating areas. The NOK 1.767 billion acquisition (on a 100% basis) is expected to generate synergies throughout the value chain.

The merger details and regional license distribution are illustrated here:

SalMar also issued NOK 2 billion in green bonds in August 2025, enhancing its financial flexibility. The company’s balance sheet showed total assets increasing due to strong growth, though the equity ratio decreased to 32.8% following dividend approval at the June AGM. Available liquidity remained strong at NOK 8.2 billion.

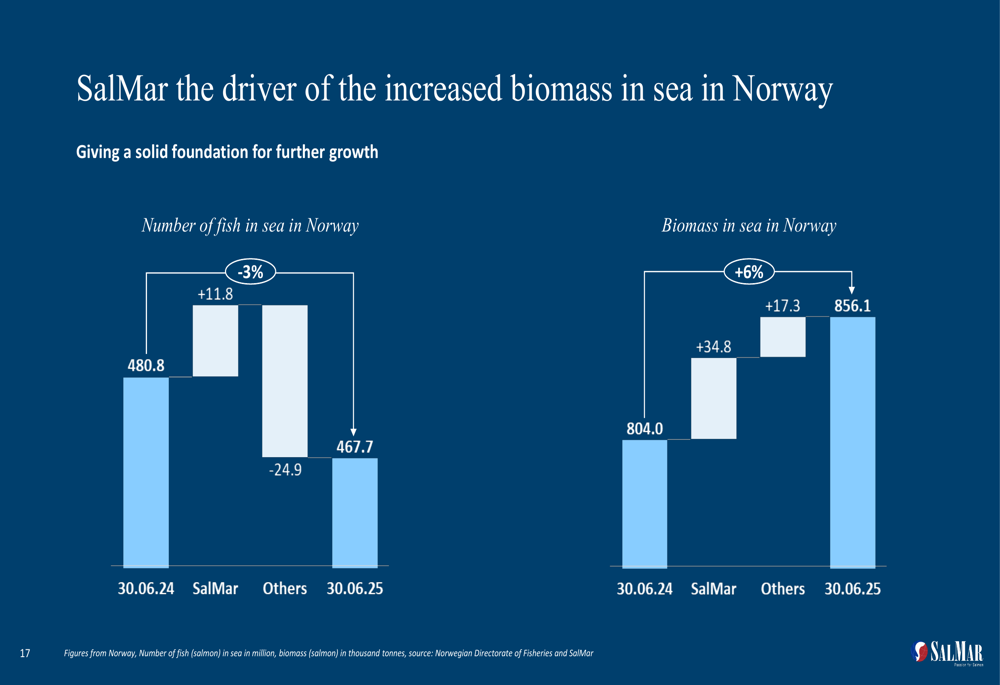

The company has positioned itself as the primary driver of increased biomass in Norway’s salmon industry, as demonstrated in the following slide:

Detailed Financial Analysis

SalMar’s Group Profit & Loss statement revealed that the decrease in operational EBIT quarter-over-quarter was primarily driven by lower market prices. Production tax increased due to higher volume, while fair value adjustments were positive due to higher biomass in calculation.

The comprehensive financial performance is detailed here:

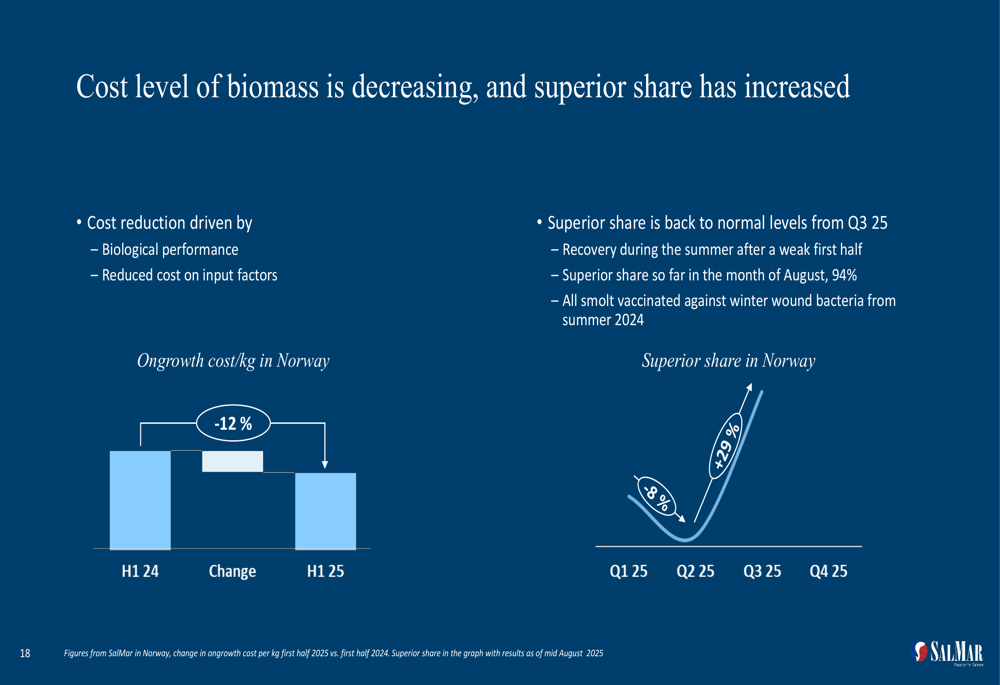

On the cost front, SalMar reported encouraging developments with a 12% reduction in ongrowth cost per kg in Norway and a 29% increase in superior share, indicating improved biological performance and efficiency:

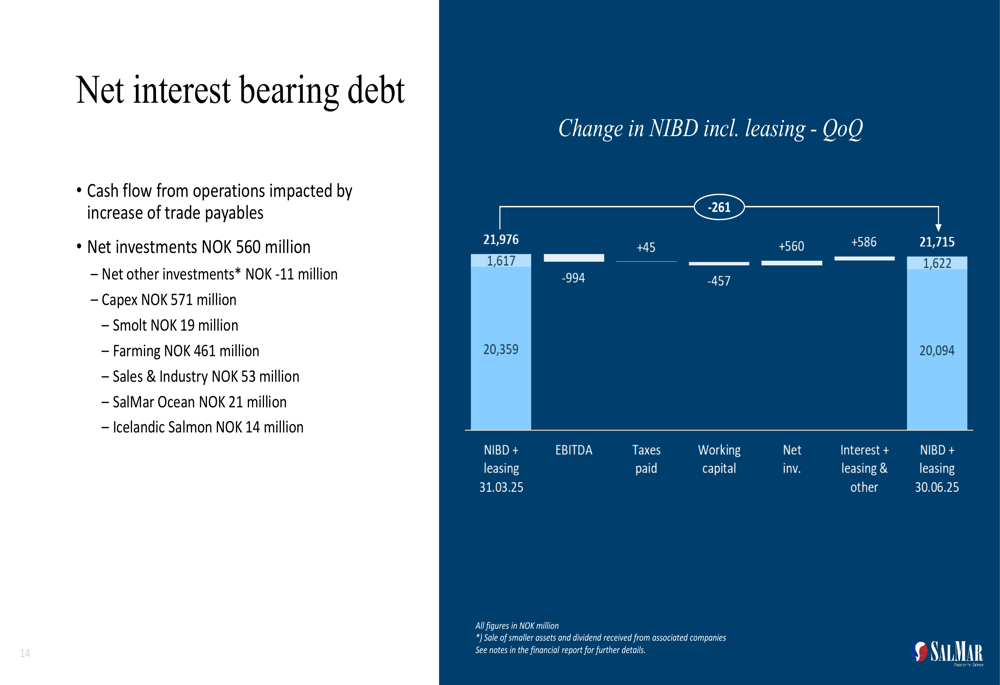

The company’s net interest-bearing debt including leasing decreased to NOK 21.7 billion, with cash flow from operations positively impacted by an increase in trade payables:

Forward-Looking Statements

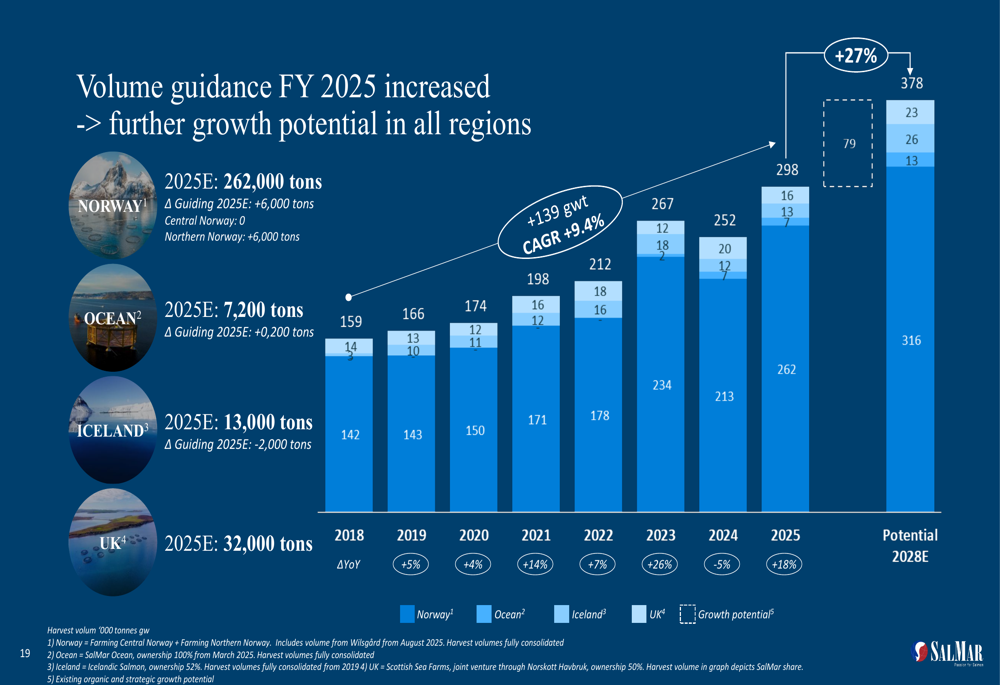

In a significant vote of confidence in its operational outlook, SalMar increased its volume guidance for FY 2025 by 4,000 tonnes to a total of 298,000 tonnes. The breakdown by region shows Norway accounting for 262,000 tonnes, Ocean operations 7,200 tonnes, Iceland 13,000 tonnes, and UK operations 32,000 tonnes.

This upward revision continues the company’s growth trajectory since 2018:

SalMar expects lower global supply growth for the remainder of 2025 compared to the first half of the year, which should support market prices. The company also highlighted strong demand for sustainable proteins across all markets despite global economic uncertainty, with good interest for new contracts.

CEO Frode Arntsen reiterated the company’s commitment to sustainable practices during the presentation, consistent with his previous statement that "Healthy, sustainable protein production on the salmon terms is something we have in our blood," as noted in the Q1 earnings call.

Looking ahead to Q3 2025, SalMar expects to continue harvesting the spring 2024 generation in Central Norway with significantly increased superior share, while Northern Norway should maintain its strong biological performance. Both regions anticipate similar cost levels to Q2 but significantly higher volumes compared to Q3 2024. The company also projects continued high cost levels in Iceland but with increased harvest volumes.

With its strategic acquisitions, improved biological performance in key regions, and increased volume guidance, SalMar appears well-positioned to navigate the market challenges while pursuing sustainable growth for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.