United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Seacoast Banking Corporation of Florida (NASDAQ:SBCF) presented strong second quarter 2025 results, highlighting significant growth in net income and strategic expansion across Florida markets. The company’s stock closed at $30.57, up 3.3% on the day of the presentation, reflecting positive investor sentiment despite premarket trading indicating a slight decline of 1.31%.

As a leading Florida-based financial institution, Seacoast maintains strong market positions across the state, including being the #1 Florida-based bank in Orlando MSA and Palm Beach County, while holding the #15 position in overall Florida market share.

Quarterly Performance Highlights

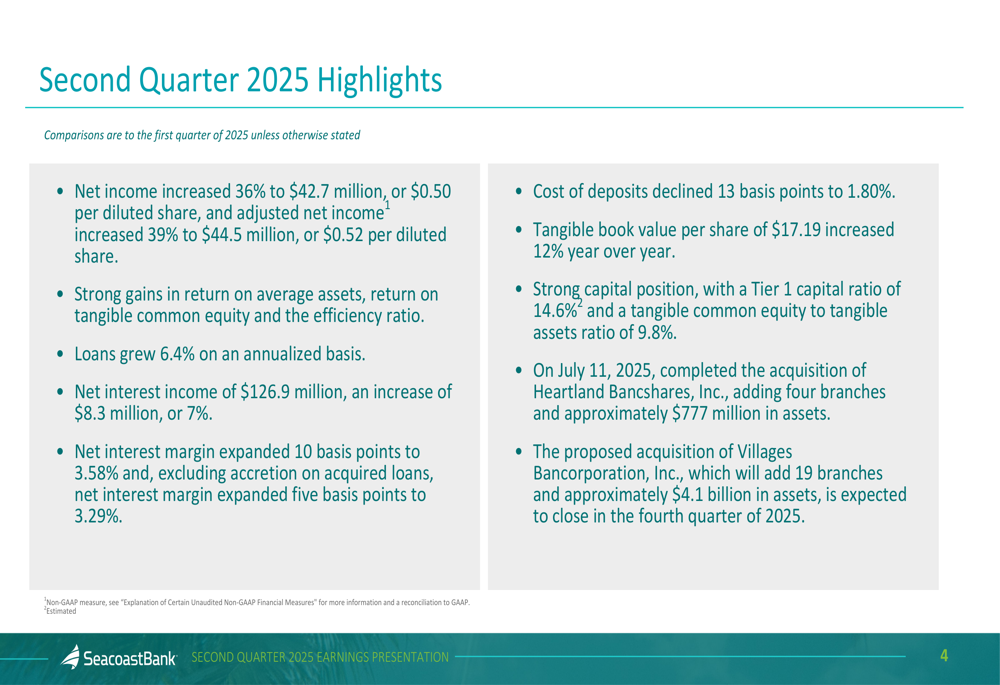

Seacoast reported substantial improvements across key financial metrics for Q2 2025, with net income increasing 36% to $42.7 million ($0.50 per diluted share) and adjusted net income rising 39% to $44.5 million ($0.52 per diluted share).

As shown in the following quarterly highlights slide, the bank demonstrated strong performance across multiple financial indicators:

The company’s efficiency ratio improved to 57.0%, while return on average assets reached 1.08% and return on tangible common equity climbed to 12.8%. These metrics indicate effective operational management and improved profitability compared to previous quarters.

Detailed Financial Analysis

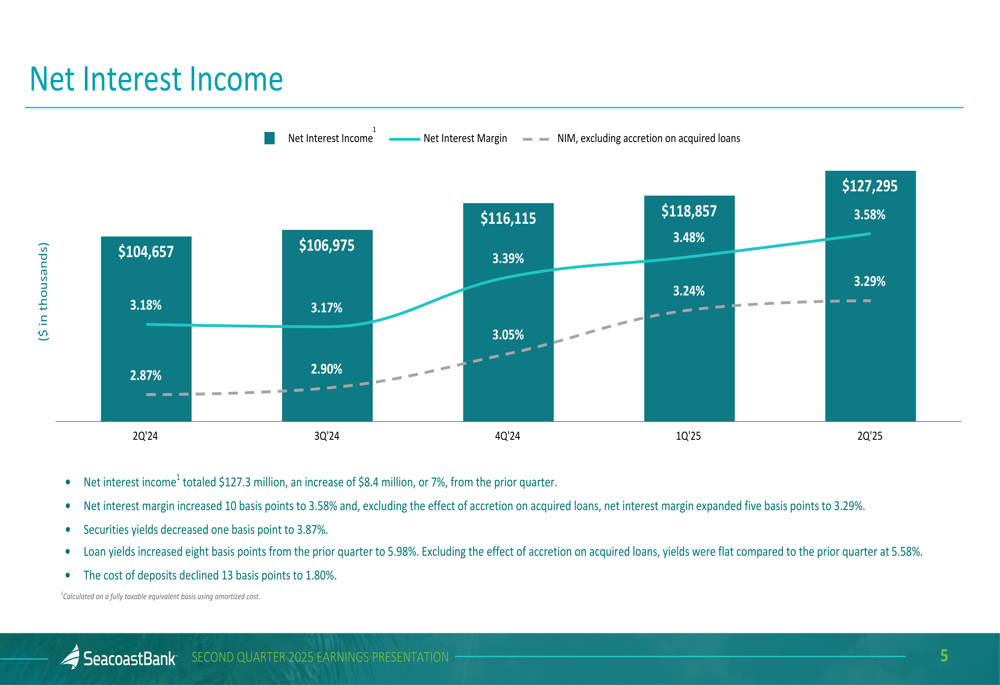

Net interest income, a critical revenue driver for banks, increased 7% to $126.9 million, with net interest margin expanding 10 basis points to 3.58%. This expansion occurred while the Federal Funds rate decreased from 5.50% in Q2 2024 to 4.50% in Q2 2025, demonstrating the bank’s effective asset-liability management.

The following chart illustrates the consistent growth in net interest income and margin expansion over the past five quarters:

On the deposit side, Seacoast has maintained a granular and diverse funding base while successfully reducing its cost of deposits by 13 basis points to 1.80%. This improvement in deposit costs has contributed significantly to the margin expansion.

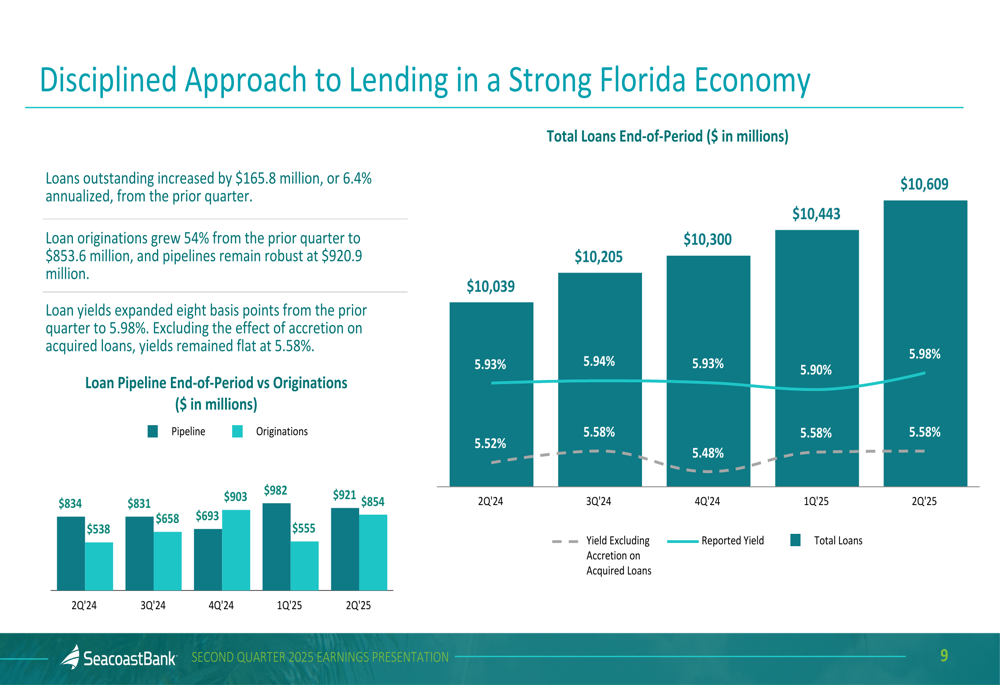

Loan growth remained solid at 6.4% on an annualized basis, with total loans outstanding increasing to $10.6 billion. Loan originations grew 54% from the prior quarter to $853.6 million, with pipelines remaining robust at $920.9 million, suggesting continued growth momentum.

The bank’s loan portfolio remains well-diversified across various sectors, with a disciplined approach to lending in Florida’s strong economy:

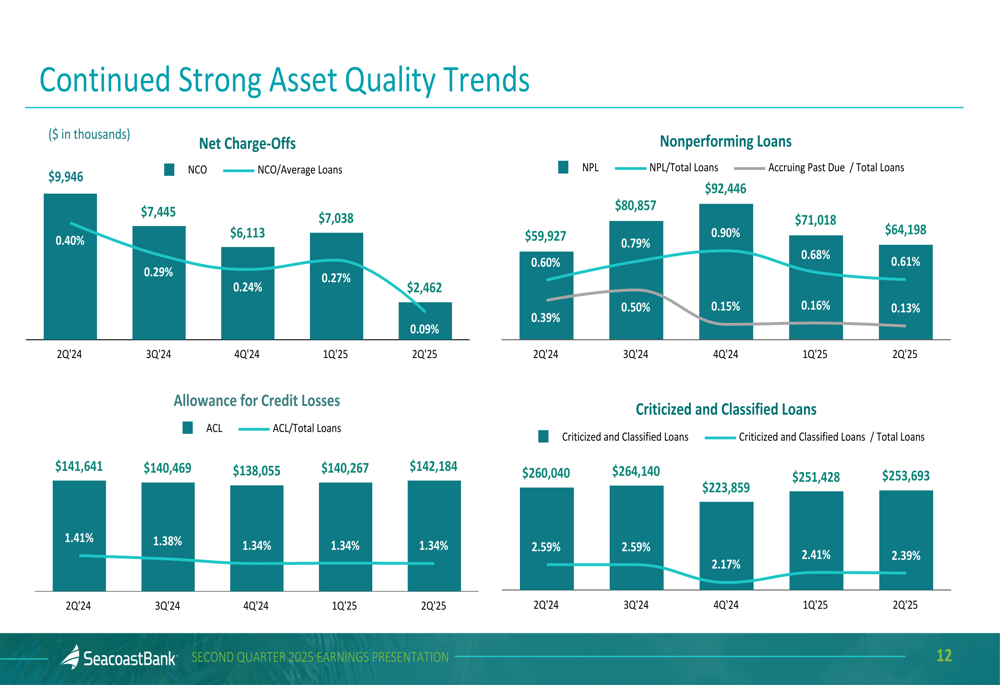

Asset quality remained strong, with net charge-offs decreasing to 0.09% of average loans in Q2 2025, down from 0.40% in Q2 2024. The allowance for credit losses to total loans ratio stood at 1.34%, slightly down from 1.41% a year earlier, reflecting the bank’s confidence in its loan portfolio quality.

The following chart demonstrates Seacoast’s continued strong asset quality trends:

Strategic Initiatives and Acquisitions

Seacoast’s growth strategy includes both organic expansion and strategic acquisitions. In July 2025, the company completed the acquisition of Heartland Bancshares, Inc., adding four branches and approximately $777 million in assets to its portfolio.

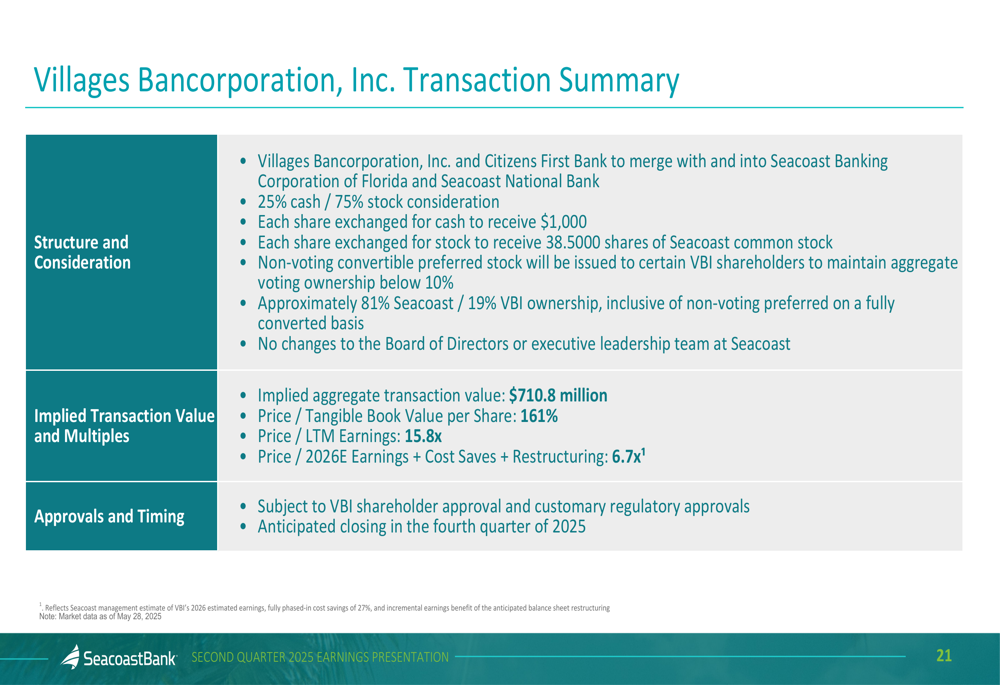

Additionally, Seacoast announced the proposed acquisition of Villages Bancorporation, Inc., expected to close in Q4 2025. This significant transaction will add 19 branches and approximately $4.1 billion in assets, substantially expanding the bank’s Florida footprint.

The following slide details the Villages Bancorporation transaction summary:

Beyond acquisitions, Seacoast continues to build its wealth management business, with assets under management reaching $2.2 billion as of June 30, 2025, representing a 16% year-over-year increase. Since 2021, assets under management have grown at a compound annual growth rate of 23%.

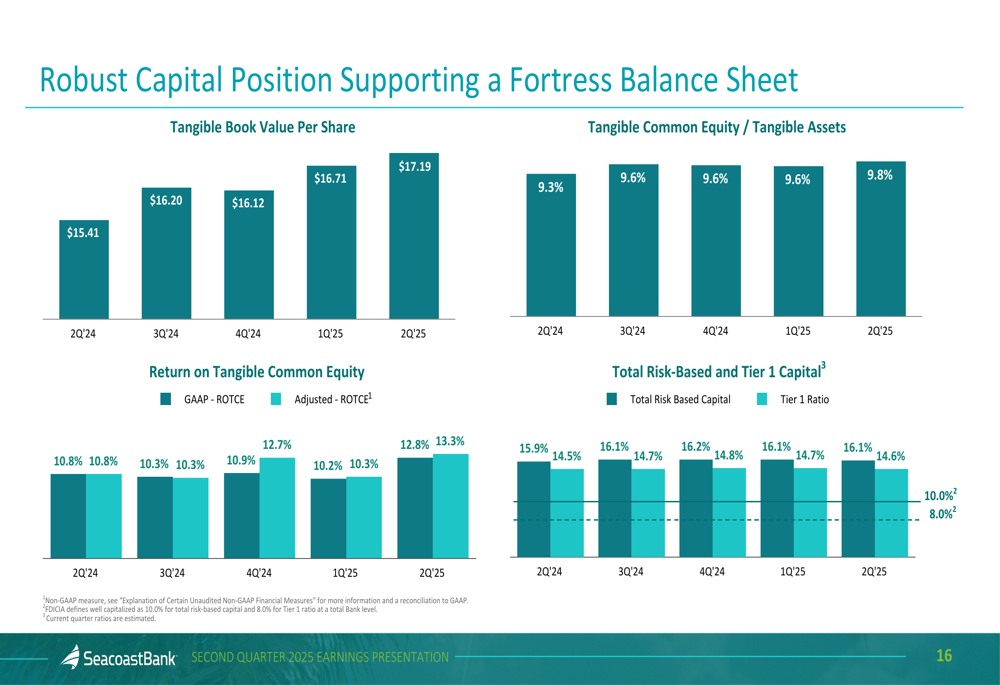

Capital Position and Forward Outlook

Seacoast maintains a robust capital position, with a Tier 1 capital ratio of 14.6% and tangible book value per share increasing 12% year-over-year to $17.19. This strong capital base supports both organic growth and the company’s acquisition strategy.

The following slide illustrates the bank’s capital strength:

Looking ahead, management anticipates mid to high single-digit loan growth in Q3 and throughout 2026. The core net interest margin is projected to be 3.35% for 2025, with expectations of margin expansion to 3.45% due to acquisitions.

CEO Charles Shaffer emphasized the company’s strong positioning, stating, "We operate with a very sound, strong capital position in a differentiated way." This approach appears to be resonating with investors, as evidenced by the company’s stock performance and continued growth trajectory.

While the bank faces challenges including competitive pressures in the commercial real estate market and potential integration risks associated with recent and proposed acquisitions, its diversified loan portfolio, strong capital position, and strategic market presence position it well for continued success in Florida’s growing banking market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.