Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

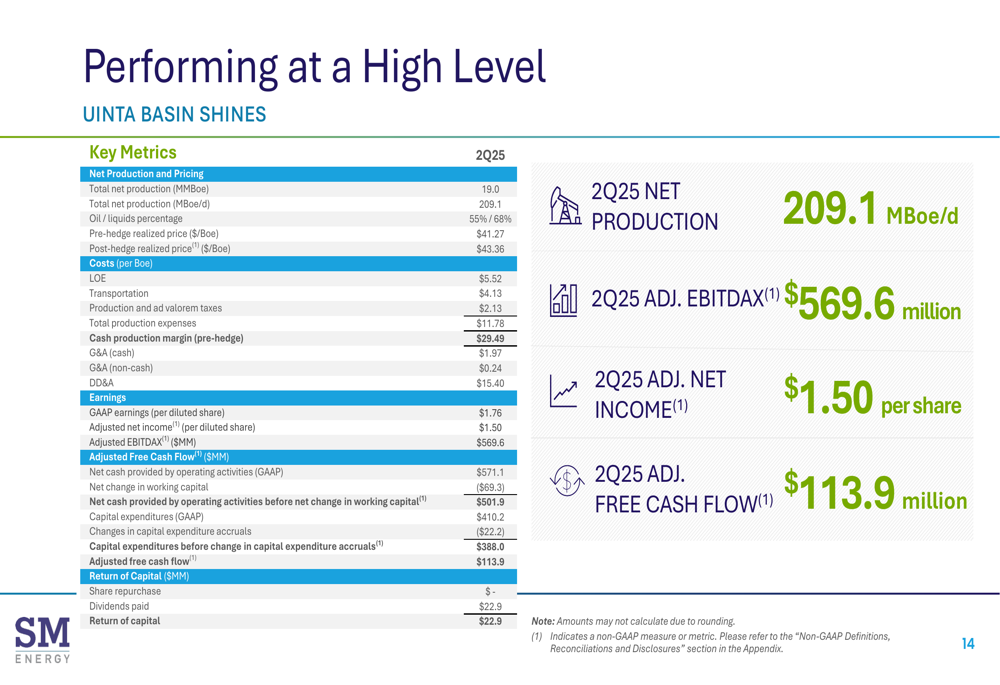

SM Energy Co (NYSE:SM) presented its second quarter 2025 financial and operating results on July 31, 2025, showcasing record production levels and strong financial performance that exceeded market expectations. The company reported adjusted earnings per share of $1.50, significantly above the forecasted $1.27, representing an 18.11% positive surprise. Following the announcement, SM Energy’s stock rose 5.51% in premarket trading to $29.11, reflecting investor confidence in the company’s operational execution and financial discipline.

The oil and gas producer has demonstrated substantial growth since 2020, with increases in both reserves and production while maintaining a focus on shareholder returns and debt reduction. SM Energy continues to position itself as a "Premier Operator of Top-Tier Assets" with operations across the Uinta Basin, Midland Basin, and South Texas regions.

Quarterly Performance Highlights

SM Energy delivered exceptional operational and financial results in the second quarter of 2025, highlighted by record-breaking production of 209.1 MBoe/d with 55% oil content. This strong production performance, coupled with operational efficiencies, contributed to adjusted net income of $1.50 per share and adjusted EBITDAX of $570 million.

As shown in the following performance summary slide, the company achieved significant financial results while continuing to return capital to shareholders:

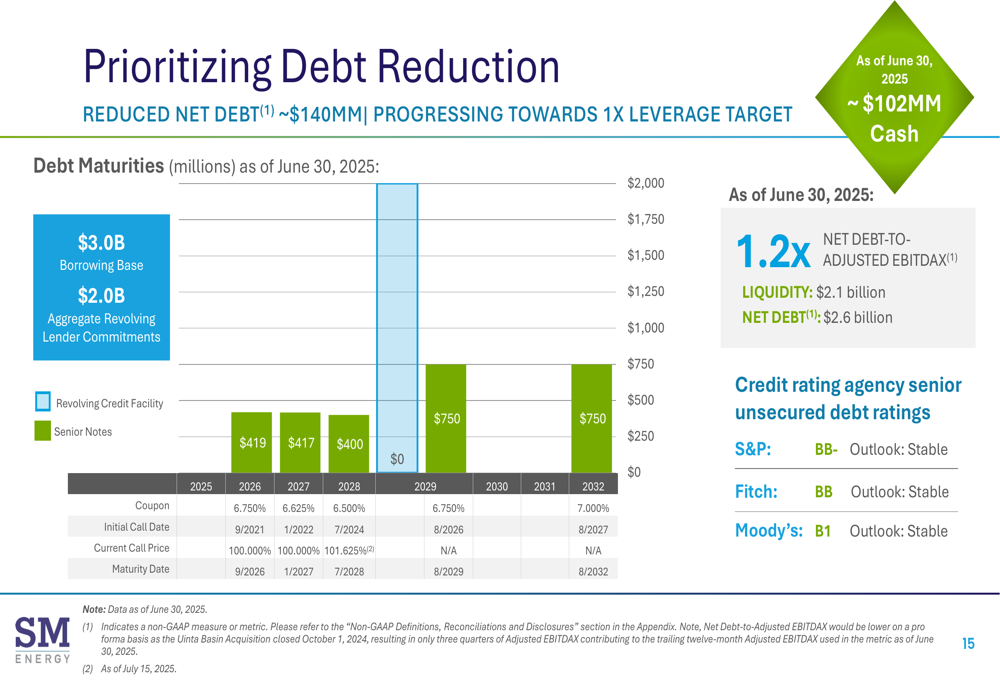

The company paid a quarterly dividend of $0.20 per share, representing an annualized yield of approximately 3%. Additionally, SM Energy reduced its net debt by approximately $140 million during the quarter, progressing toward its target leverage ratio of 1.0x.

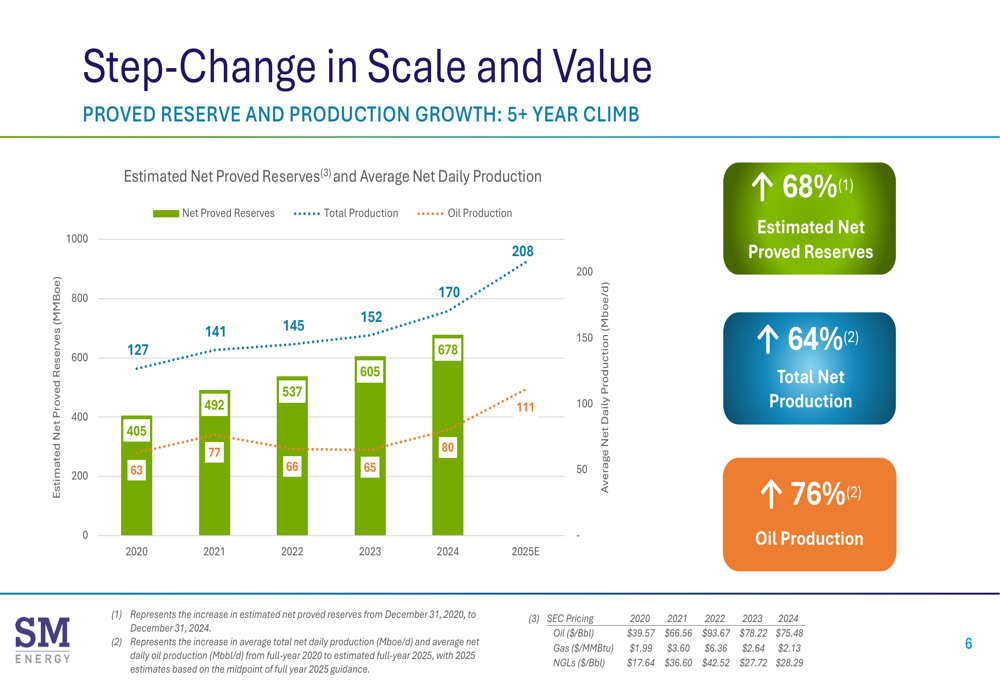

SM Energy’s long-term growth trajectory has been impressive, with substantial increases in both proved reserves and production since 2020:

The slide illustrates a 68% increase in estimated net proved reserves from 2020 to 2024 and projects a 64% increase in total net production from 2020 to 2025, with oil production growing by 76% during the same period. This growth has been achieved while maintaining capital discipline and without diluting shareholders.

Operational Excellence

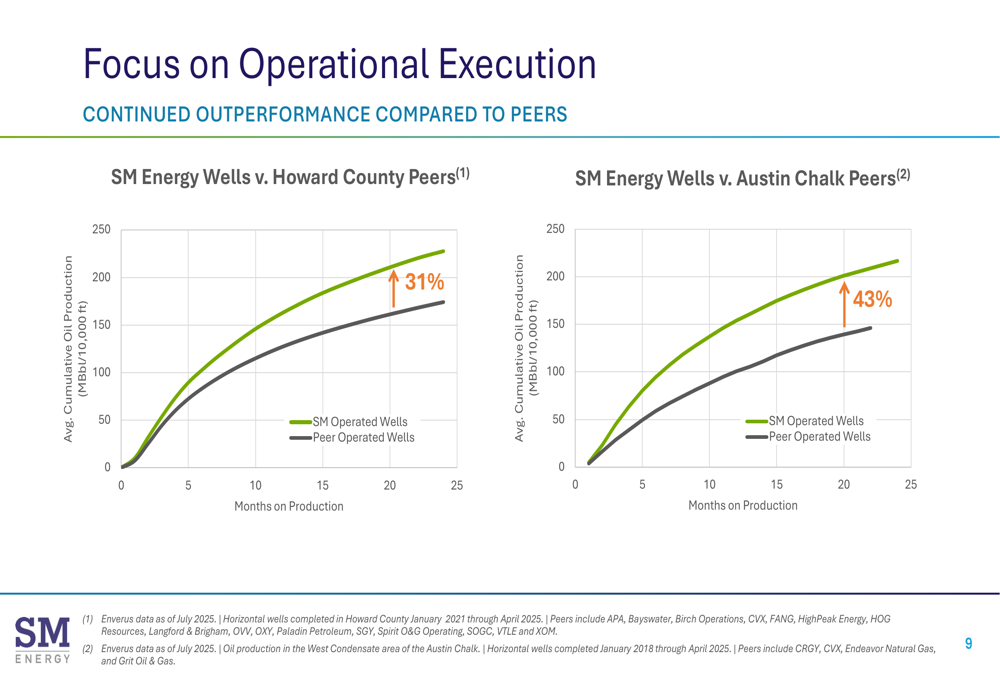

SM Energy’s operational excellence is evident across all its operating regions, with particularly strong results in the Uinta Basin, where integration is complete and optimization efforts are underway. The company has demonstrated superior well performance compared to peers in key areas:

In Howard County, SM Energy’s wells outperformed peer-operated wells by 31%, while in the Austin Chalk formation, the outperformance reached 43%. These results underscore the company’s technical expertise and operational efficiency.

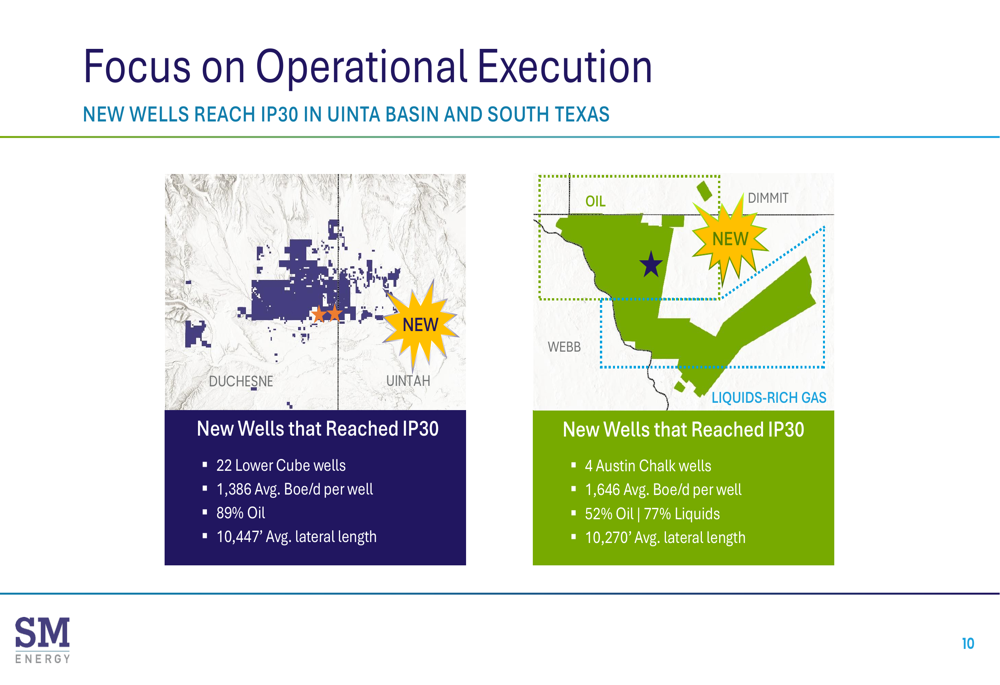

New wells reaching initial production (IP30) also showed strong performance:

In the Uinta Basin, 22 Lower Cube wells achieved average production of 1,386 Boe/d per well with 89% oil content, while in South Texas, 4 Austin Chalk wells delivered 1,646 Boe/d per well with 52% oil and 77% liquids.

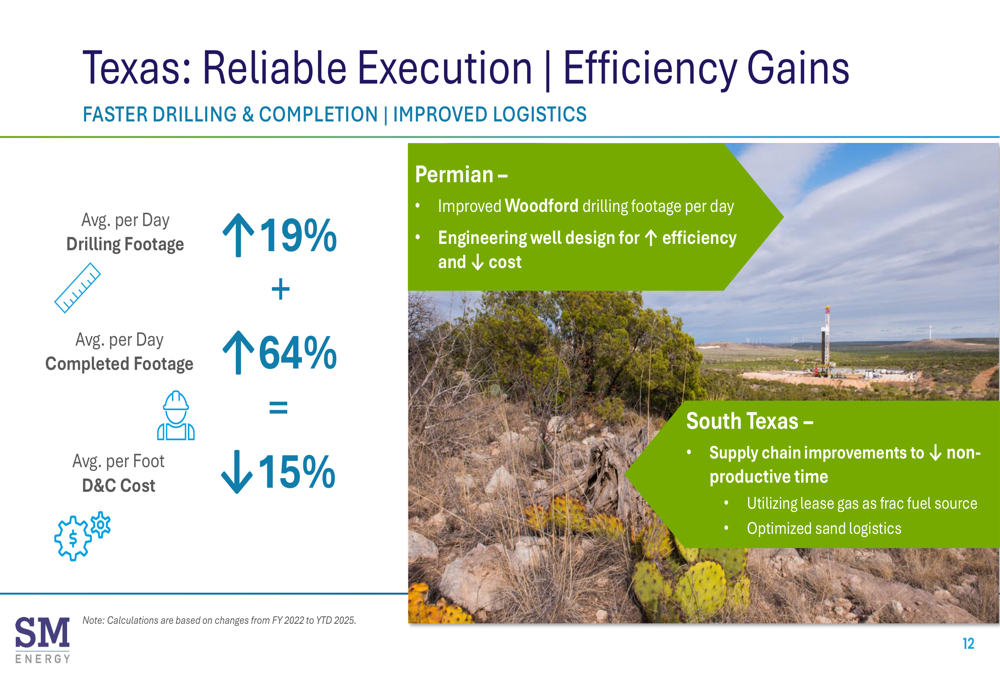

The company has made significant efficiency gains in Texas operations, resulting in faster drilling and completion times and lower costs:

Average drilling footage per day increased by 19%, while average completed footage per day jumped by 64%. These improvements contributed to a 15% reduction in drilling and completion costs per foot, enhancing capital efficiency and returns.

Financial Position & Capital Allocation

SM Energy continues to prioritize debt reduction as part of its capital allocation strategy. The company reduced net debt by approximately $140 million in Q2 2025 and is progressing toward its target leverage ratio of 1.0x:

As of June 30, 2025, SM Energy maintained strong liquidity of $2.1 billion with net debt of $2.6 billion. The company’s credit ratings remain stable, with S&P rating the senior unsecured debt at BB- (Stable outlook), Fitch at BB (Stable), and Moody’s at B1 (Stable).

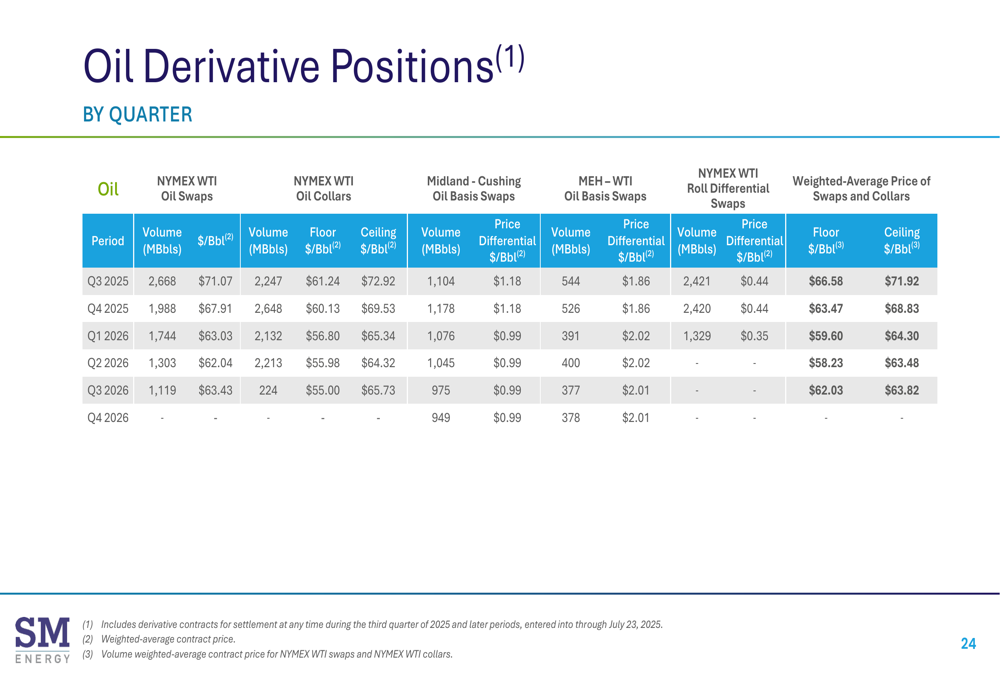

To manage commodity price risk, SM Energy has implemented a comprehensive hedging program:

The company has hedged approximately 9,600 MBbls of oil at prices ranging from $65.07/Bbl to $70.42/Bbl, providing downside protection while maintaining upside potential.

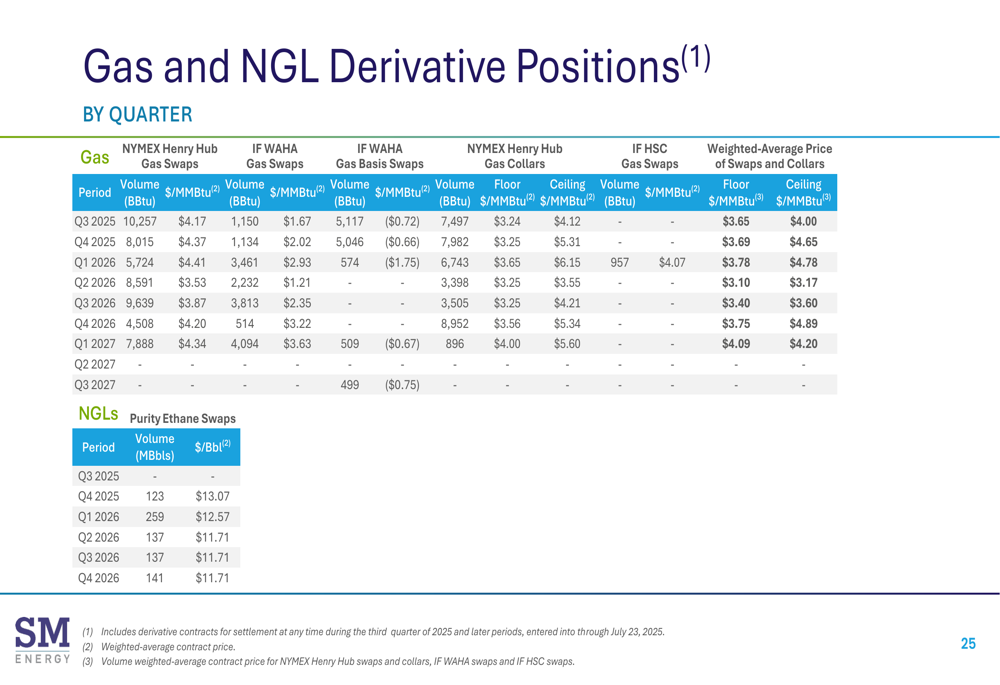

Similarly, SM Energy has hedged its natural gas exposure:

These hedging positions help stabilize cash flows and support the company’s capital allocation priorities, including debt reduction, dividend payments, and potential share repurchases.

Forward Outlook

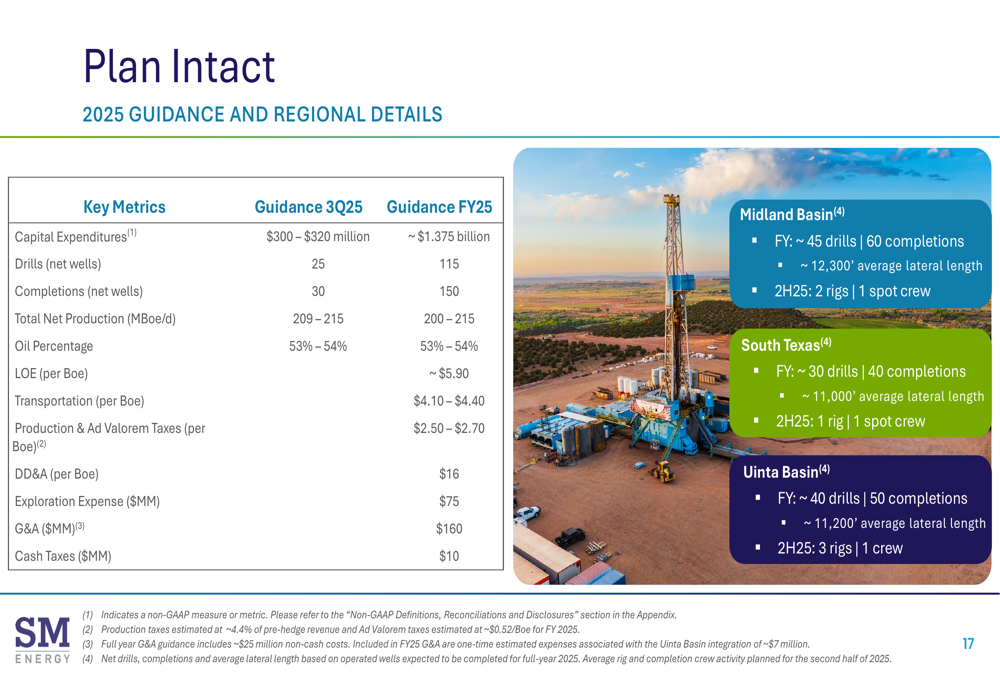

SM Energy’s guidance for the remainder of 2025 remains intact, with detailed regional plans for production and capital expenditures:

The company continues to focus on operational execution, returning capital to stockholders, and expanding its portfolio of top-tier economic drilling inventory. With the Uinta Basin integration complete, SM Energy is now in optimization mode, implementing efficiency improvements and cost-reduction initiatives.

CEO Herb Vogel highlighted the company’s achievements during the earnings call, stating, "We have delivered a step change in scale and de-risked the balance sheet all while not diluting our shareholders." This statement underscores SM Energy’s commitment to creating shareholder value through operational excellence and financial discipline.

Looking ahead, SM Energy is well-positioned to continue generating free cash flow and optimizing its operations across all regions. The company has authorized a $500 million share repurchase program and may implement opportunistic buybacks as leverage targets are achieved. With its diversified asset base, strong operational performance, and disciplined financial approach, SM Energy appears poised for continued success in the evolving energy landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.