U.S. stocks edge higher with consumer sentiment data, AI boom in focus

Introduction & Market Context

Spotlio AS (SPOT), a digital solutions provider for attractions, waterparks, and ski areas, presented its fourth quarter and full-year fiscal 2025 results on June 19, 2025. The company, which trades at $0.26 as of June 18, has focused on cost rationalization initiatives throughout the year to improve profitability despite revenue challenges.

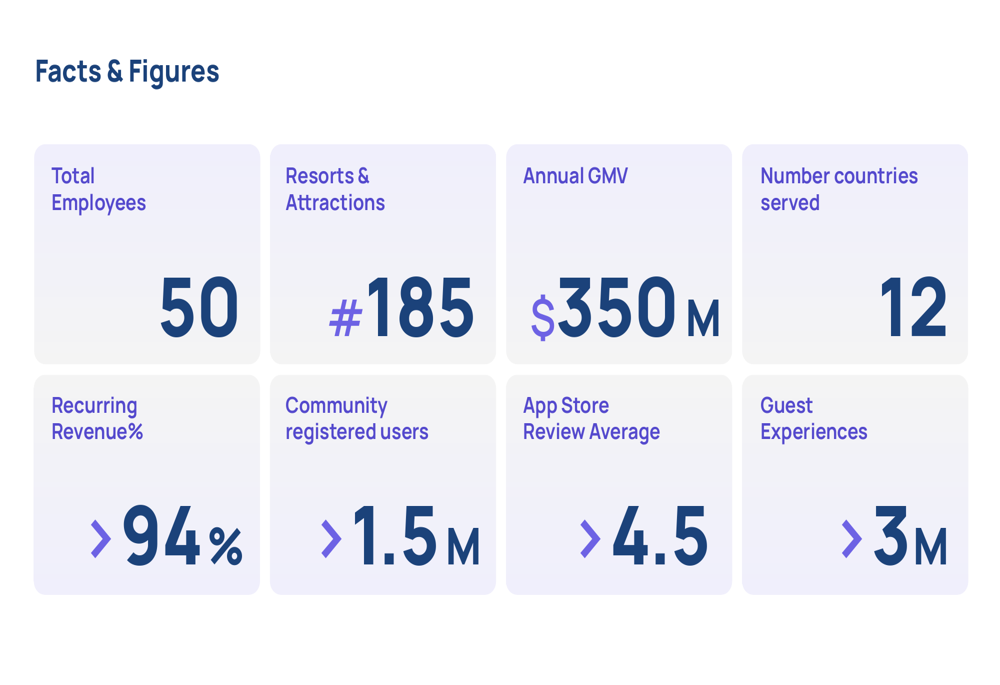

Spotlio’s business model centers on empowering ticketing businesses to maximize revenue and enhance guest experiences through digital solutions, with over 94% of its revenue coming from recurring sources. The company serves 185 resorts and attractions across 12 countries, processing approximately $350 million in annual gross merchandise value.

Executive Summary

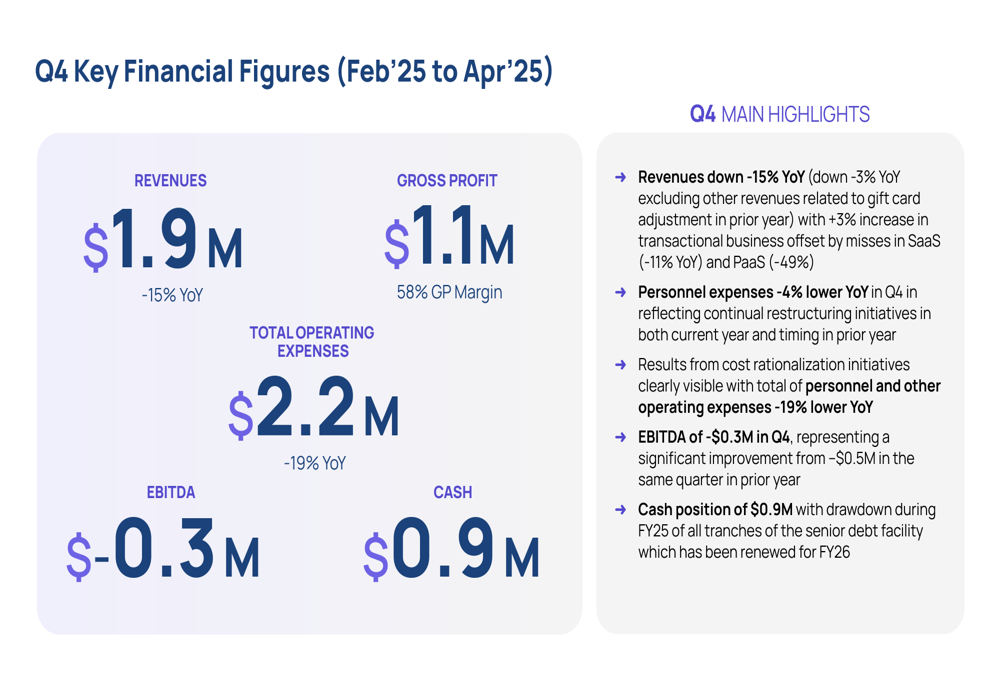

Spotlio’s fourth quarter showed continued progress in the company’s turnaround efforts, with significant cost reductions offsetting revenue declines. While Q4 revenue fell 15% year-over-year to $1.9 million, the company reduced operating expenses by 19%, resulting in an EBITDA loss of $0.3 million—an improvement from the $0.5 million loss in the same quarter last year.

As shown in the following key facts and figures about the company:

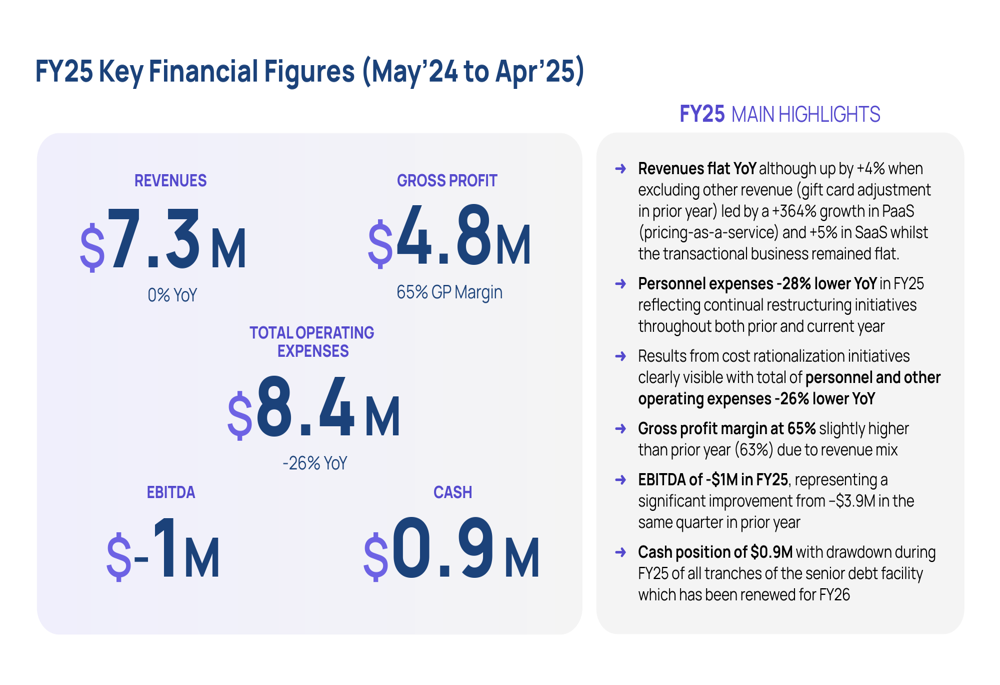

For the full fiscal year 2025, Spotlio maintained flat revenue at $7.3 million while dramatically reducing operating expenses by 26% year-over-year. This cost discipline resulted in a significantly improved EBITDA loss of $1 million, compared to a $3.9 million loss in fiscal 2024.

Quarterly Performance Highlights

Spotlio’s Q4 FY25 performance reflected mixed results across its business segments. The company’s transactional business grew 3% in the quarter, but this was offset by weakness in SaaS (-11% YoY) and PaaS (-49% YoY). When excluding one-time gift card adjustments from the prior year, the overall revenue decline was a more modest 3%.

The following slide details Spotlio’s key Q4 financial metrics:

Gross profit for the quarter reached $1.1 million, representing a 58% margin. The company’s cost rationalization initiatives were clearly visible in the results, with personnel expenses down 4% year-over-year and total operating expenses reduced by 19%.

Spotlio ended the quarter with $0.9 million in cash, having drawn down all tranches of its senior debt facility, which has been renewed for fiscal year 2026.

Detailed Financial Analysis

For the full fiscal year 2025, Spotlio demonstrated significant progress in its business transformation. While overall revenue remained flat at $7.3 million, the company achieved 4% growth when excluding one-time gift card adjustments from the prior year.

The company’s performance across business segments varied significantly, with PaaS (pricing-as-a-service) growing an impressive 364% year-over-year and SaaS increasing by 5%, while the transactional business remained flat.

The following slide illustrates Spotlio’s full-year financial performance:

Spotlio’s income statement reveals the extent of its cost-cutting measures. Employee benefits expense decreased from $5.9 million in FY24 to $4.2 million in FY25, a 28% reduction. Similarly, other operating expenses were reduced by 40%, falling from $2.7 million to $1.6 million.

These cost reductions helped narrow the company’s operating loss from $7.4 million in FY24 to $4.2 million in FY25, despite ongoing depreciation and amortization expenses of $3.2 million.

The balance sheet shows total assets of $10.7 million as of April 30, 2025, down from $13.4 million a year earlier. Total (EPA:TTEF) equity declined to $5.3 million from $9.9 million, while liabilities increased to $5.3 million from $3.6 million, reflecting the company’s increased debt utilization.

Forward-Looking Statements

While Spotlio did not provide specific guidance for fiscal year 2026 in the presentation materials, the renewal of its senior debt facility for FY26 suggests continued financial support for the company’s operations.

The significant growth in Spotlio’s PaaS business segment (364% year-over-year) indicates a potential strategic shift toward this high-growth area. However, the decline in SaaS revenue during Q4 (-11% YoY) after growing 5% for the full year bears watching, as it could signal challenges in what has traditionally been a core business segment.

The company’s continued focus on cost discipline has yielded substantial improvements in EBITDA, reducing losses by nearly 75% year-over-year. If Spotlio can stabilize or return to growth in its revenue while maintaining this cost discipline, the path to profitability could become clearer in fiscal year 2026.

With a community of over 1.5 million registered users and more than 3 million guest experiences, Spotlio has built a substantial digital platform that serves as the foundation for its future growth initiatives in the attractions and ticketing market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.