TSMC earnings; Oracle analyst meeting; Gold’s new high - what’s moving markets

Introduction & Market Context

Sprouts Farmers Market (NASDAQ:SFM) presented its second quarter 2025 earnings results on July 30, showcasing continued strong performance across key metrics. The specialty grocery retailer, known for its focus on health and wellness products, reported significant growth in both sales and profitability, building on momentum from the previous quarter.

The company’s stock closed at $156.94 on the day of the presentation, up 0.74% in regular trading, though it edged slightly lower by 0.12% in after-hours trading. Sprouts shares have performed strongly over the past year, with the stock trading well above its 52-week low of $91.36, reflecting investor confidence in the company’s health-focused strategy.

Quarterly Performance Highlights

Sprouts reported impressive financial results for Q2 2025, with net sales increasing by 17% compared to the same period last year. Comparable store sales (comps) grew by 10.2%, indicating strong customer traffic and basket size across existing locations.

The company’s diluted earnings per share reached $1.35, representing a substantial 44% year-over-year increase. While this marks a sequential decrease from the $1.81 EPS reported in Q1 2025, it demonstrates continued strong profitability. Cash generation for the quarter totaled $111 million, with $73 million allocated to share repurchases.

As shown in the following quarterly highlights slide:

The company also continued its store expansion strategy, opening 12 new locations during the second quarter. This brings the total new store openings for the first half of 2025 to 15, keeping Sprouts on track to meet its full-year target of at least 35 new stores.

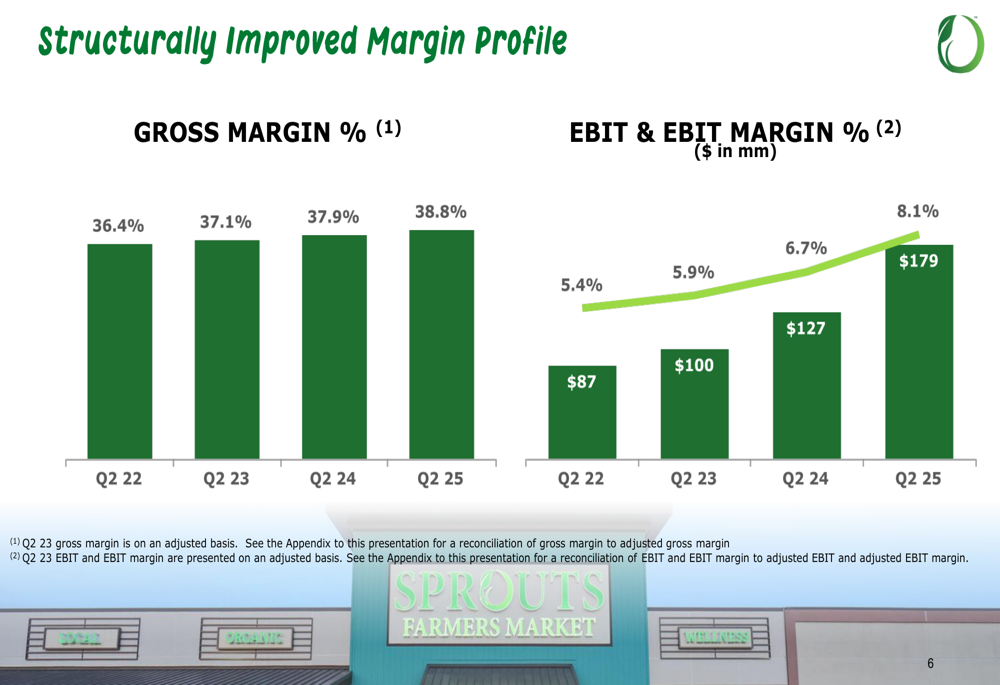

Margin Expansion and Financial Strength

One of the most notable aspects of Sprouts’ Q2 performance was the continued improvement in its margin profile. The company achieved a gross margin of 38.8% in Q2 2025, representing a 90 basis point improvement from 37.9% in Q2 2024 and continuing a multi-year trend of margin expansion.

Even more impressive was the growth in EBIT (earnings before interest and taxes) margin, which reached 8.1% in Q2 2025, up from 6.7% in the same period last year. This translated to EBIT of $179 million, a significant increase from $127 million in Q2 2024.

The following chart illustrates this structural margin improvement over time:

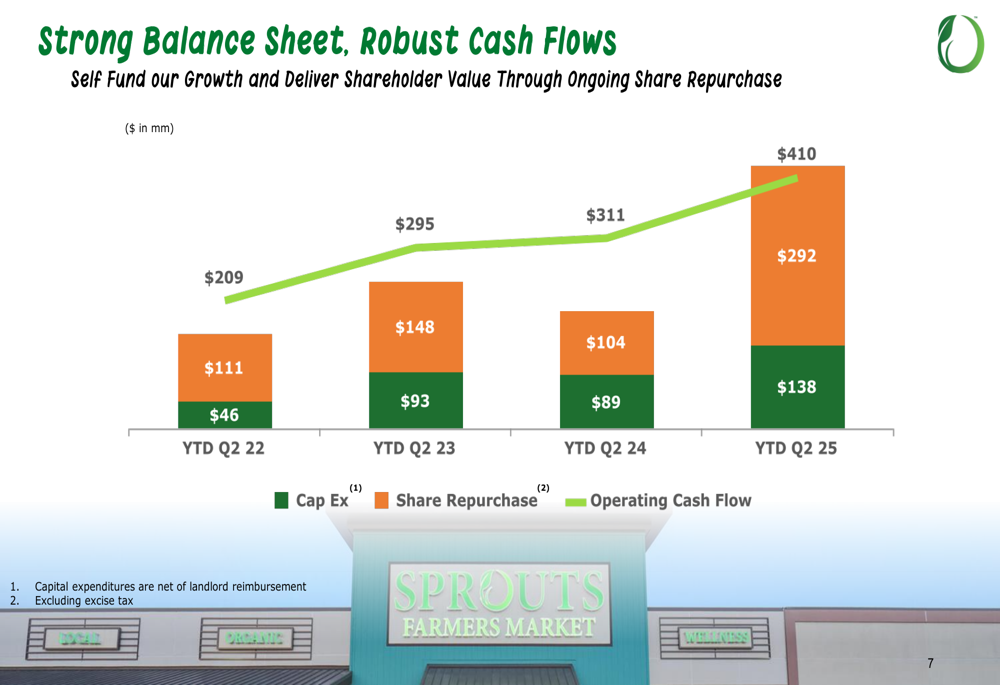

Sprouts’ financial strength is further evidenced by its robust cash flow generation. Year-to-date operating cash flow reached $410 million, up from $311 million in the same period last year. This has allowed the company to increase both capital expenditures to support growth ($138 million YTD) and shareholder returns through share repurchases ($292 million YTD).

The balance sheet and cash flow trends are visualized in this chart:

Strategic Growth Drivers

Sprouts attributed its strong sales performance to several key factors, including balanced growth across product categories, channels, and geographical regions. The company noted that traffic was the primary driver of comparable sales growth, suggesting increasing customer visits rather than just higher prices.

Management highlighted that customers continue to be drawn to Sprouts’ quality, fresh, and innovative products with healthy attributes. The company is also benefiting from broader tailwinds in healthy living and wellness trends, which align with its core value proposition.

As illustrated in the sales drivers slide:

E-commerce growth across all partner platforms was also cited as a contributor to overall performance, indicating successful omnichannel execution. Additionally, the company reported compelling comparable sales in recent store vintages, suggesting that newer locations are ramping up effectively.

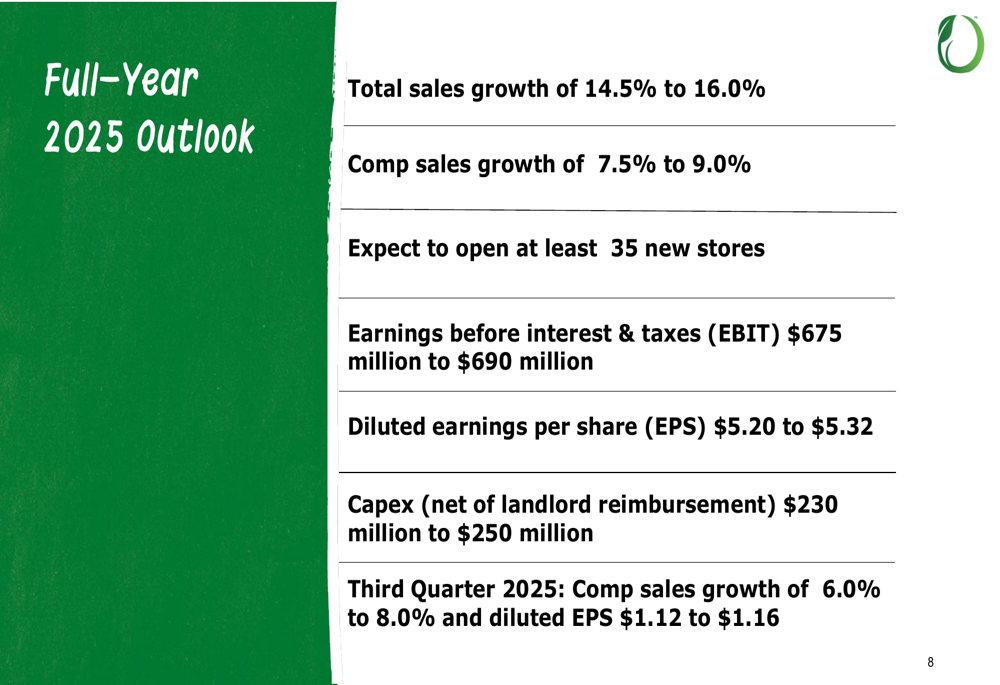

Updated 2025 Outlook

Following the strong first-half performance, Sprouts raised its full-year 2025 guidance across multiple metrics. The company now expects:

- Total (EPA:TTEF) sales growth of 14.5% to 16.0% (up from previous guidance of 12-14%)

- Comparable store sales growth of 7.5% to 9.0% (up from previous 5.5-7.5%)

- At least 35 new store openings (unchanged)

- EBIT of $675 million to $690 million

- Diluted EPS of $5.20 to $5.32 (up from previous $4.94-$5.10)

- Capital expenditures of $230 million to $250 million (net of landlord reimbursement)

For the upcoming third quarter of 2025, Sprouts projects comparable sales growth of 6.0% to 8.0% and diluted EPS of $1.12 to $1.16.

The full-year outlook is detailed in this slide:

The raised guidance reflects management’s confidence in the company’s ability to maintain sales momentum while continuing to expand margins. The projected full-year EPS growth demonstrates Sprouts’ commitment to translating top-line growth into enhanced profitability and shareholder value.

As Sprouts continues to execute its expansion strategy and capitalize on growing consumer interest in health and wellness, the company appears well-positioned to deliver on its updated financial targets for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.