Asia stocks rise: Japan surges on Takaichi bets, China buoyed by positive GDP

Introduction & Market Context

SPS Commerce Inc (NASDAQ:SPSC) continues to demonstrate strong financial performance, as highlighted in its July 2025 presentation following the release of Q2 2025 results. The company reported a 22% year-over-year revenue increase to $187.4 million, marking its 90th consecutive quarter of revenue growth. SPS Commerce’s stock showed resilience in the current market environment, closing up 1.29% at $108.09 following the earnings announcement.

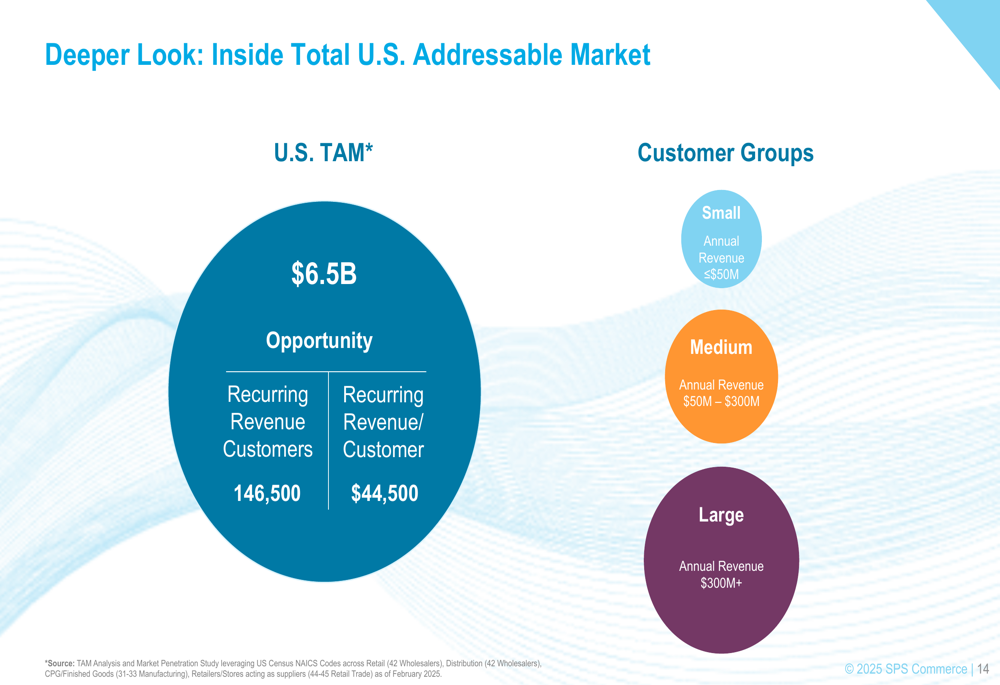

The company operates in a substantial addressable market, with its presentation highlighting a global Total Addressable Market (TAM) of $11.1 billion, of which $6.5 billion represents the U.S. opportunity alone. This expansive market provides significant runway for continued growth as the company currently serves approximately 54,500 recurring revenue customers.

As shown in the following market opportunity breakdown:

Strategic Positioning

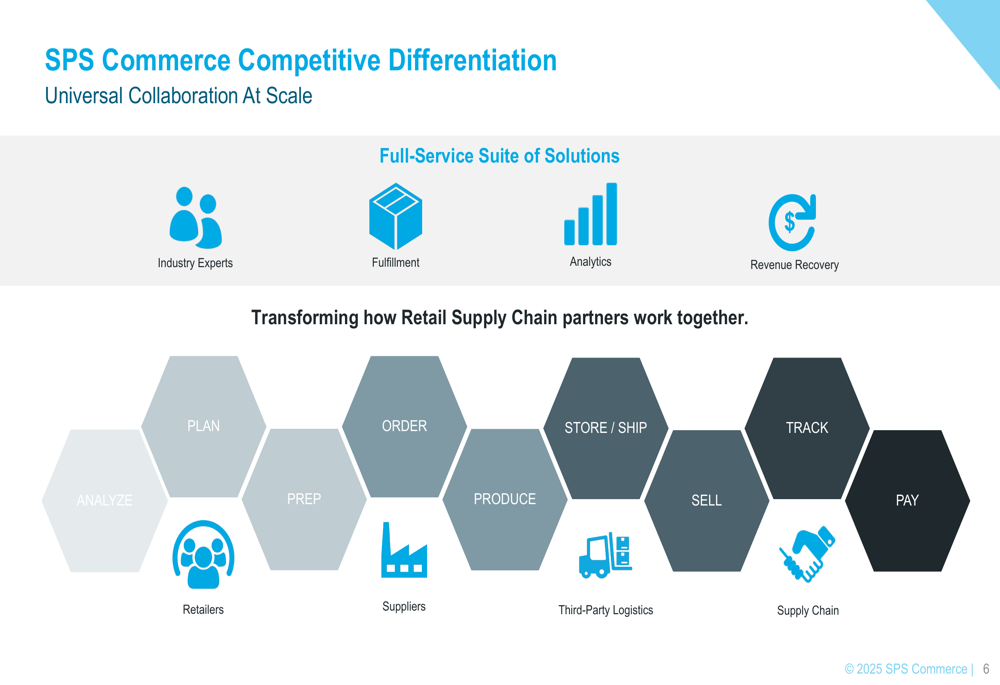

SPS Commerce has established itself as the only full-service EDI (Electronic Data Interchange) solution in the market, positioning itself as a critical infrastructure provider for retail supply chains. The company’s competitive differentiation stems from its ability to provide "Universal Collaboration At Scale" through a comprehensive suite of solutions that connect retailers, suppliers, and logistics providers.

The company’s strategic positioning is illustrated in this competitive differentiation diagram:

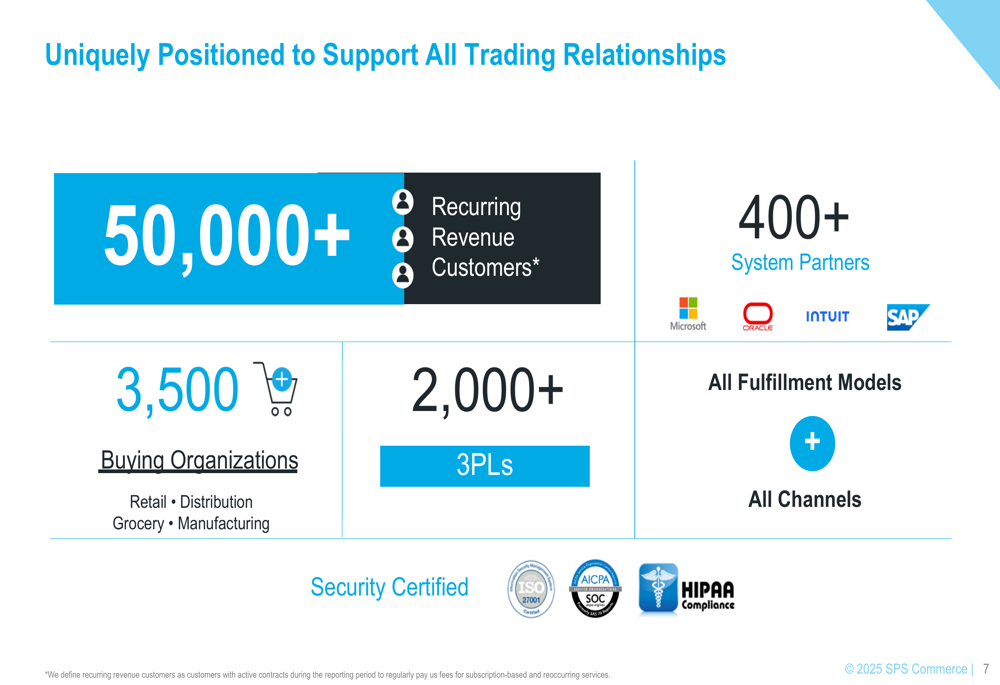

A key strength of SPS Commerce is its extensive network of connections across the retail ecosystem. The company serves over 50,000 recurring revenue customers, 3,500+ buying organizations, 2,000+ third-party logistics providers, and maintains partnerships with 400+ system partners including Microsoft, Oracle, Intuit, and SAP.

This extensive network creates a powerful competitive moat and growth engine, as shown in the following slide:

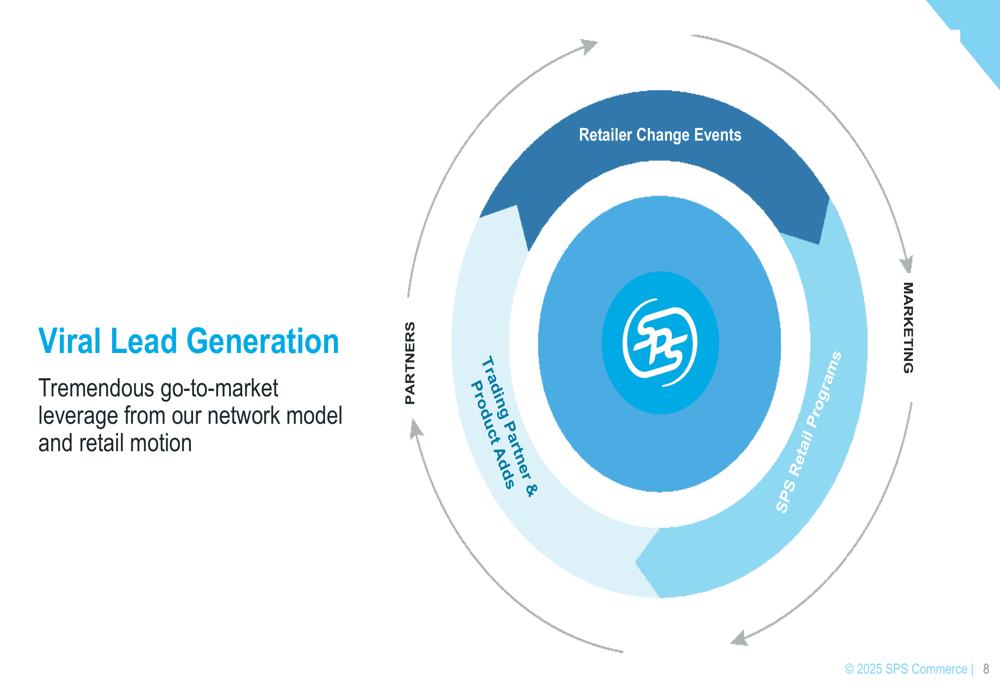

One of SPS Commerce’s most compelling advantages is its "viral lead generation" model, where existing network connections drive new customer acquisition. This creates a self-reinforcing growth cycle that reduces customer acquisition costs and accelerates expansion.

The company explained this unique go-to-market leverage in its presentation:

Financial Performance

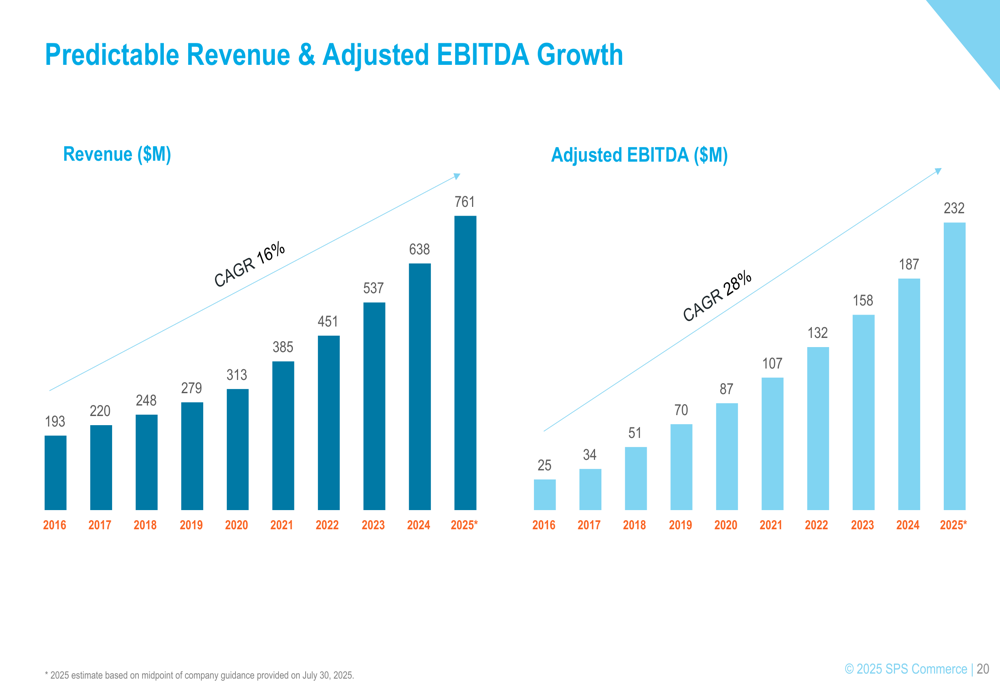

SPS Commerce has demonstrated consistent financial growth over an extended period. Revenue has grown at a 16% CAGR from 2016 to 2025, while Adjusted EBITDA has expanded at an even more impressive 28% CAGR during the same period. This reflects the company’s ability to scale efficiently and generate increasing profitability as it grows.

For Q2 2025 specifically, the company reported revenue of $187.4 million (up 22% year-over-year) and Adjusted EBITDA of $56.1 million (a 27% increase). These results align with the long-term growth trajectory illustrated in the presentation:

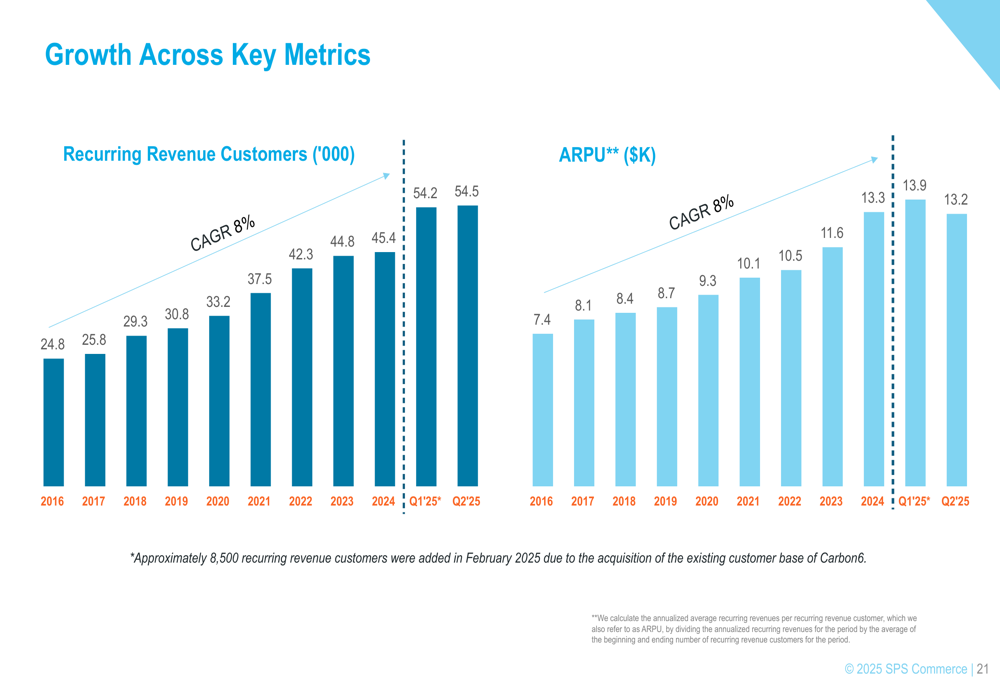

The company’s growth is driven by two key metrics: expanding its customer base and increasing the Average Revenue Per User (ARPU). Both metrics have shown steady growth at an 8% CAGR from 2016 to Q2 2025, with the customer base reaching 54,500 and ARPU hitting $13,200.

This dual-growth strategy is visualized in the following chart:

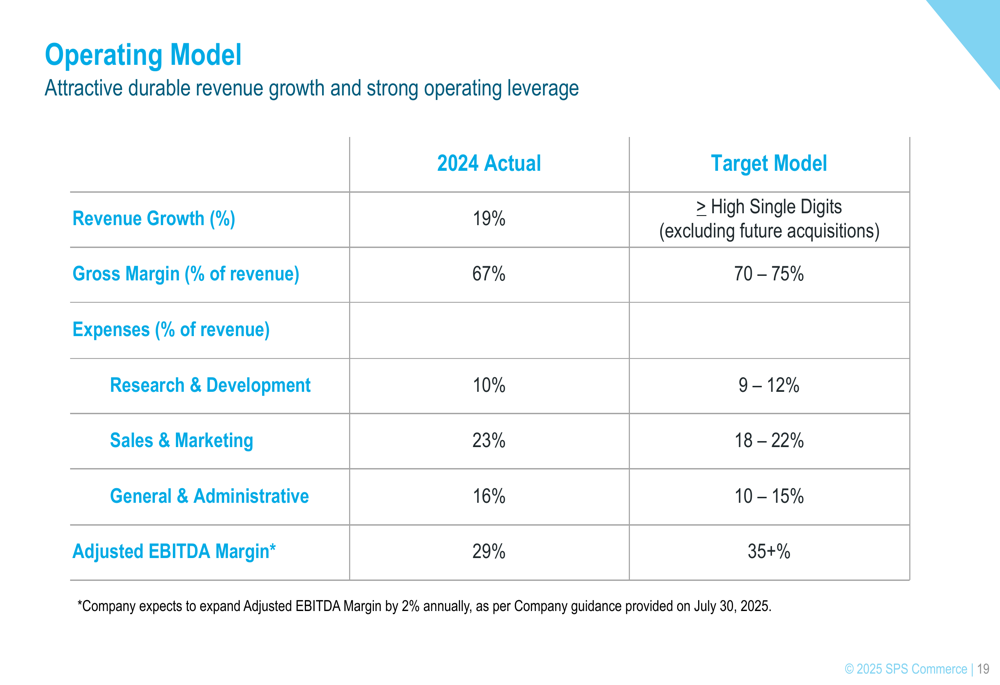

SPS Commerce’s operating model demonstrates strong fundamentals, with 2024 actual results showing 19% revenue growth, 67% gross margins, and a 29% Adjusted EBITDA margin. The company’s target model aims to maintain high-single-digit revenue growth while expanding Adjusted EBITDA margins to 35%+.

Growth Strategy

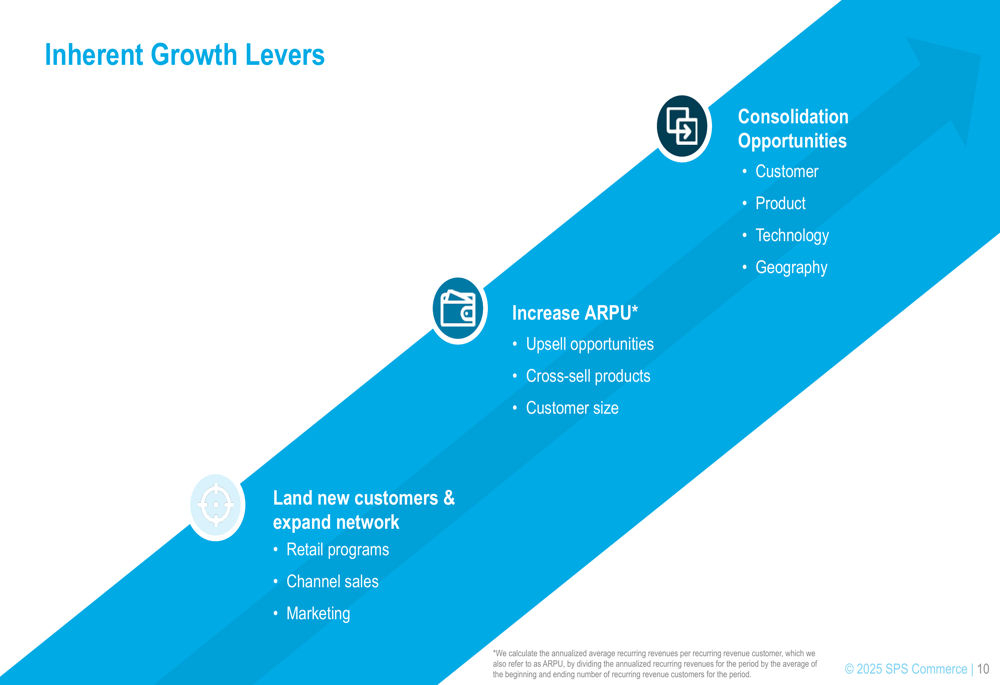

SPS Commerce outlined several growth levers in its presentation, focusing on three main strategies: acquiring new customers and expanding the network, increasing ARPU through upsell and cross-sell opportunities, and pursuing consolidation opportunities.

The company’s growth strategy is summarized in this slide:

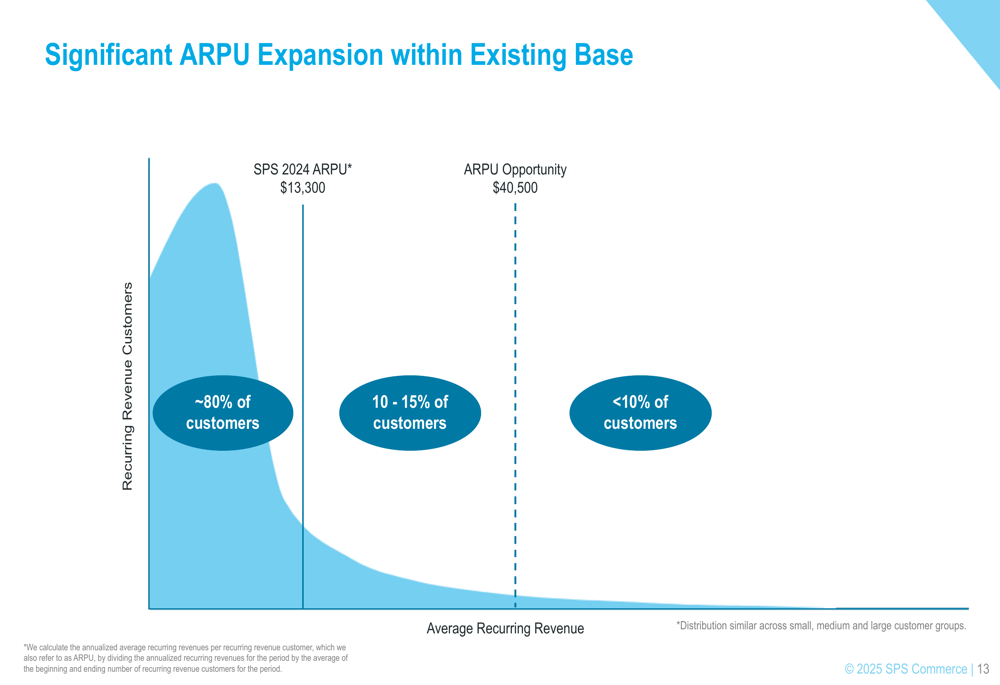

A significant growth opportunity exists in expanding ARPU within the existing customer base. According to the presentation, approximately 80% of customers are currently below the 2024 ARPU of $13,300, representing substantial room for expansion toward the opportunity ARPU of $40,500.

This ARPU expansion opportunity is illustrated in the following chart:

The company presented several case studies demonstrating successful growth with existing customers across different segments. For small customers (annual revenue under $50M), SPS Commerce showed a 6x revenue increase through trading partner expansion. For medium customers ($50M-$300M), the company achieved a remarkable 110x revenue growth over 11 years through cross-selling and increased document volume. Even with large customers (over $300M), SPS Commerce demonstrated 15x revenue growth over 14 years.

Forward Outlook

Looking ahead, SPS Commerce provided guidance for 2025, projecting revenue between $759 million and $763 million, representing 19-20% growth. The company expects to continue expanding its adjusted EBITDA margin by approximately 2 percentage points annually.

SPS Commerce’s long-term strategy remains focused on capturing a greater share of its large addressable market through both organic growth and strategic acquisitions. As noted in the earnings call, the company "expects to remain acquisitive over time in keeping with our disciplined and effective M&A strategy."

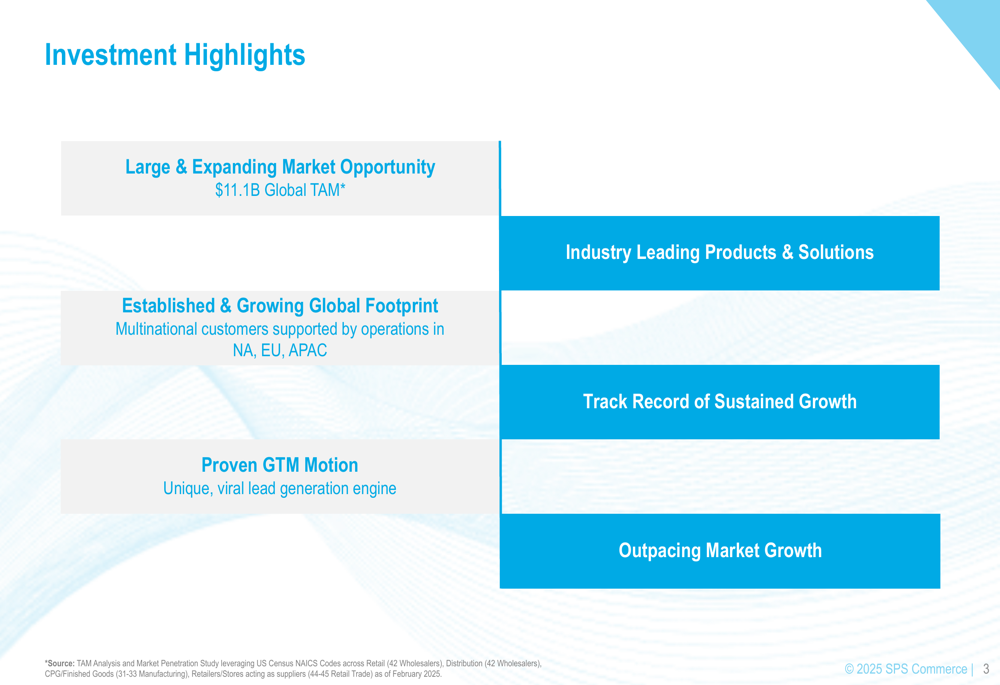

Despite some macroeconomic uncertainties affecting supplier spending, particularly in the mid-market segment, SPS Commerce’s network-based business model and essential role in retail supply chains position it well for continued growth. The company’s investment highlights emphasize its large and expanding market opportunity, established global footprint, proven go-to-market motion, industry-leading solutions, and track record of sustained growth.

With $108 million in cash and investments as of Q2 2025, SPS Commerce maintains a strong balance sheet to support both organic growth initiatives and potential acquisitions. The company also returned value to shareholders through a $20 million share repurchase during the quarter, demonstrating confidence in its long-term prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.