Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

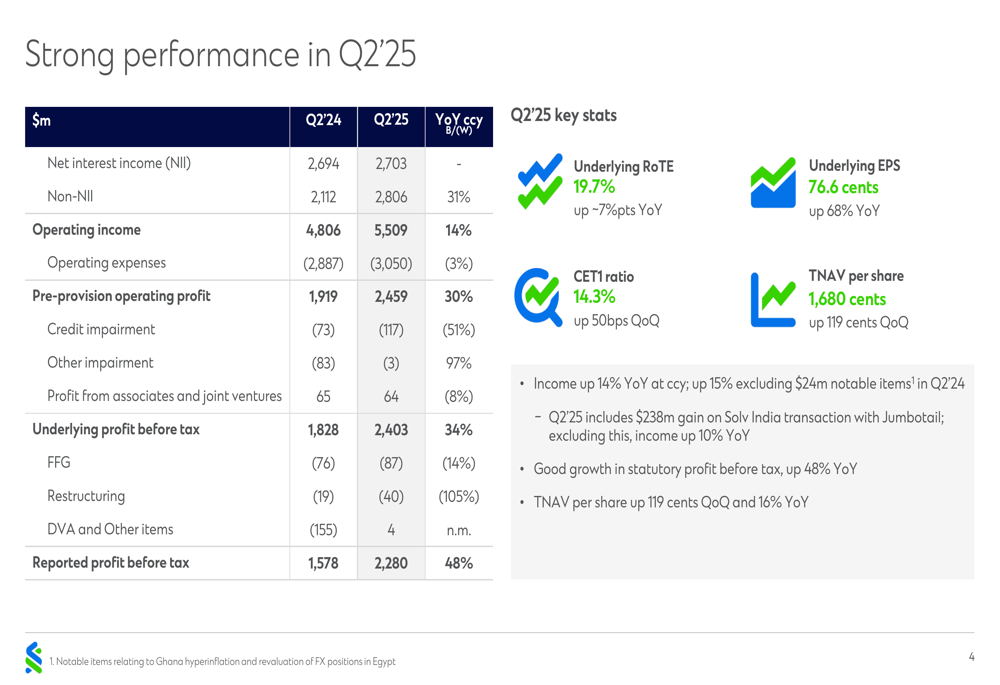

Standard Chartered (LON:STAN) PLC (OTC:SCBFF) (LSE:STAN) delivered strong second-quarter results for 2025, with reported profit before tax surging 48% year-over-year to $2.28 billion, according to the company’s half-year results presentation released on July 31, 2025. The bank announced a new $1.3 billion share buyback program while upgrading its 2025 income growth guidance, demonstrating confidence in its strategic direction despite challenging interest rate environments.

The robust Q2 performance builds upon the positive momentum seen in Q1 2025, when the bank reported a 19% rise in earnings per share and a 12% increase in profit before tax. The latest results show an acceleration of this growth trajectory, particularly in non-interest income segments.

As shown in the following key highlights from the presentation, Standard Chartered is making significant progress on its strategic initiatives while delivering substantial returns to shareholders:

Quarterly Performance Highlights

Standard Chartered’s Q2 2025 financial performance demonstrated considerable strength across multiple metrics, with underlying profit before tax increasing 34% year-over-year to $2.4 billion. This performance was primarily driven by a 14% rise in operating income to $5.5 billion, while the bank maintained disciplined cost management with expenses increasing by just 3%.

The detailed financial breakdown reveals that while Net Interest Income (NII) remained relatively flat year-over-year at $2.7 billion, Non-NII surged 31% to $2.8 billion. This growth helped offset pressure on interest margins from the changing rate environment. Notably, the bank’s underlying Return on Tangible Equity (RoTE) reached an impressive 19.7%, up approximately 7 percentage points from the previous year.

The following chart illustrates the key financial metrics for Q2 2025:

A significant contributor to the quarter’s performance was a $238 million gain from the Solv India transaction with Jumbotail. Even excluding this one-off gain, income still grew by 10% year-over-year, demonstrating the underlying strength of the bank’s core businesses.

Credit quality remained strong, with credit impairment at just $117 million, representing a loan-loss rate of only 12 basis points. While this represents a 51% increase from the exceptionally low impairment in Q2 2024, it remains well below the historical through-the-cycle average of 30-35 basis points.

Segment Performance

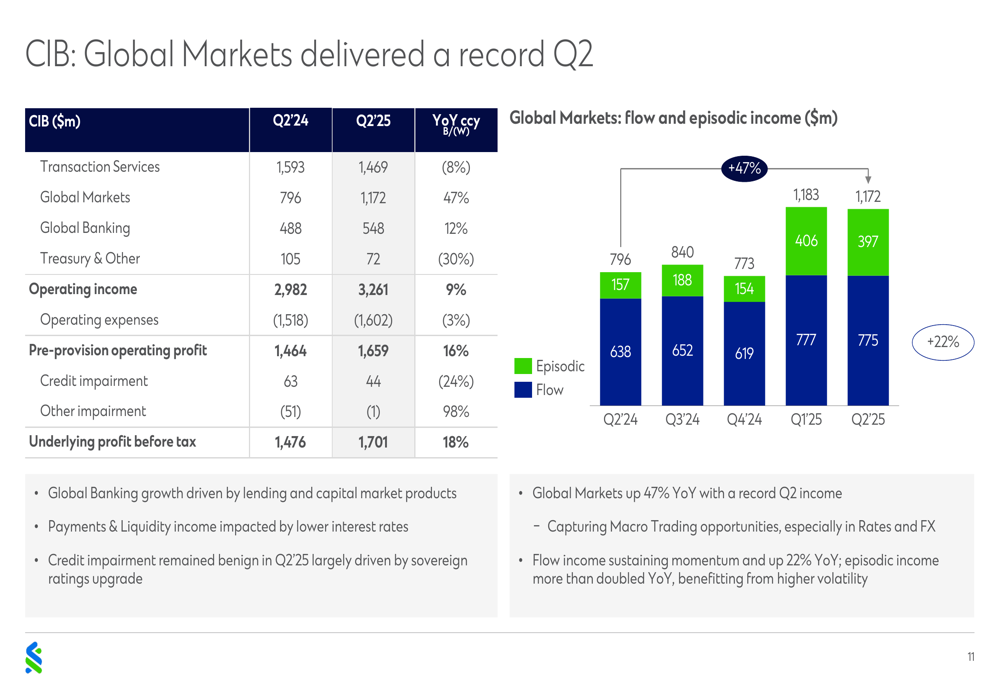

Standard Chartered’s Corporate and Investment Banking (CIB) division delivered exceptional results, with Global Markets achieving a record second quarter. Income in this segment jumped 47% year-over-year to $1.17 billion, driven by strong performance in both flow business and episodic income.

As shown in the following segment breakdown, Global Markets capitalized on macro trading opportunities, especially in Rates and FX, while Global Banking income grew 12% to $548 million:

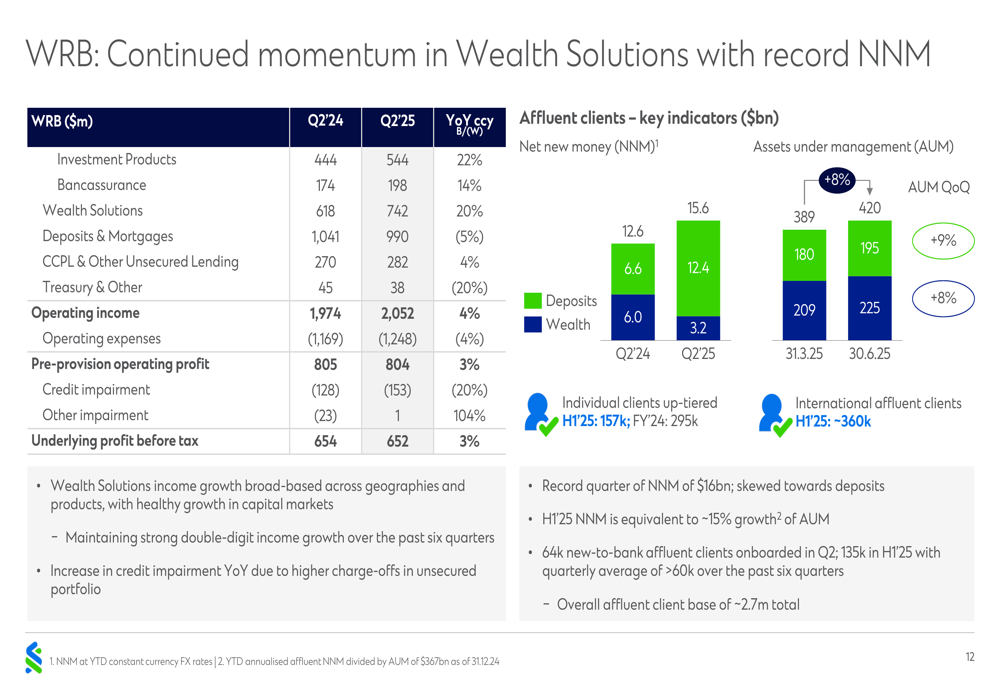

The Wealth and Retail Banking (WRB) division also performed well, with Wealth Solutions income growing 20% year-over-year to $742 million. This growth was broad-based across geographies and products, with healthy expansion in capital markets activities. Investment Products and Bancassurance grew by 22% and 14% respectively, offsetting a 5% decline in Deposits & Mortgages income.

The WRB division achieved a record quarter for Net New Money (NNM) of $16 billion, albeit skewed toward deposits. The bank’s position as the third-largest wealth manager in Asia by Assets Under Management (AUM) continues to strengthen, with affluent AUM growing at an 11% CAGR since 2016.

The bank’s digital strategy is also gaining traction, with the Ventures segment turning profitable thanks to the Solv India transaction gain. Digital Banks income increased 48% year-over-year to $46 million, driven by volume growth and product innovation.

Capital Management & Shareholder Returns

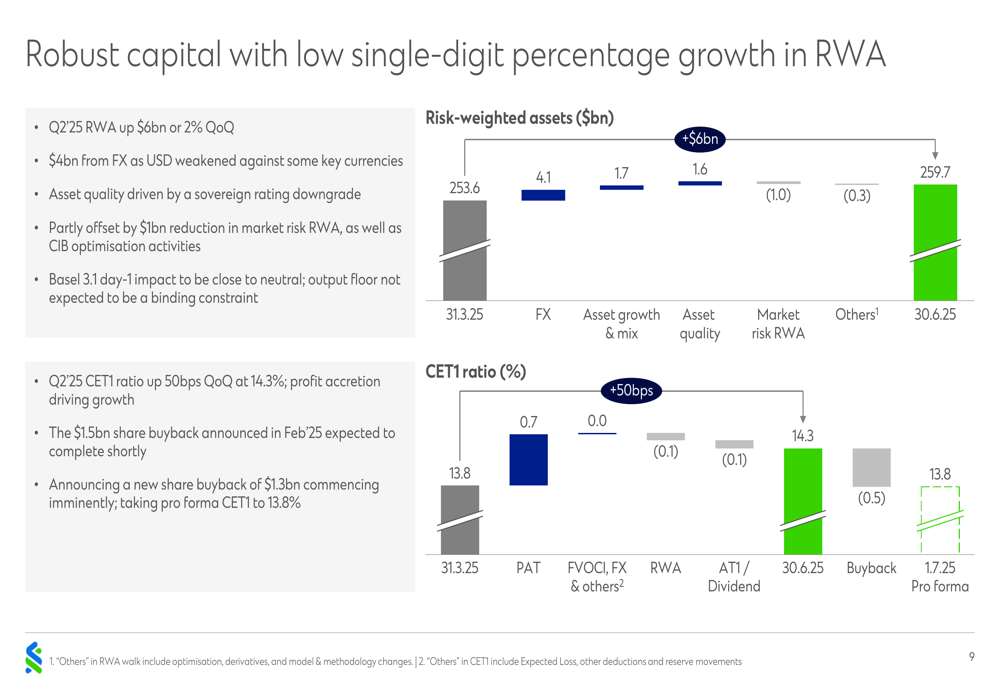

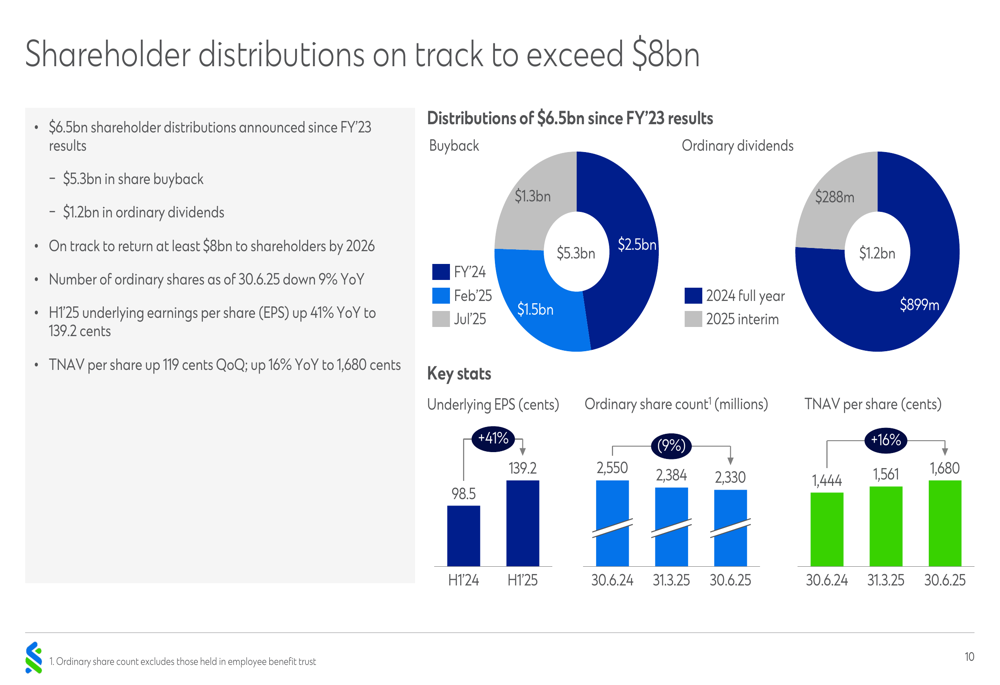

Standard Chartered’s capital position strengthened during the quarter, with the CET1 ratio increasing by 50 basis points quarter-over-quarter to 14.3%. This robust capital position has enabled the bank to announce a new $1.3 billion share buyback program, which will commence imminently.

The following chart illustrates the bank’s capital movements and shareholder distribution strategy:

The new buyback follows the $1.5 billion program announced in February 2025, which is expected to complete shortly. Together with ordinary dividends, Standard Chartered has announced $6.5 billion in shareholder distributions since its FY 2023 results and is well on track to return at least $8 billion to shareholders by 2026.

This capital return strategy has contributed to a 9% year-over-year reduction in the number of ordinary shares outstanding, helping drive a 41% increase in underlying earnings per share for H1 2025 to 139.2 cents. Tangible Net Asset Value (TNAV) per share also increased significantly, up 119 cents quarter-over-quarter and 16% year-over-year to 1,680 cents.

Forward-Looking Statements

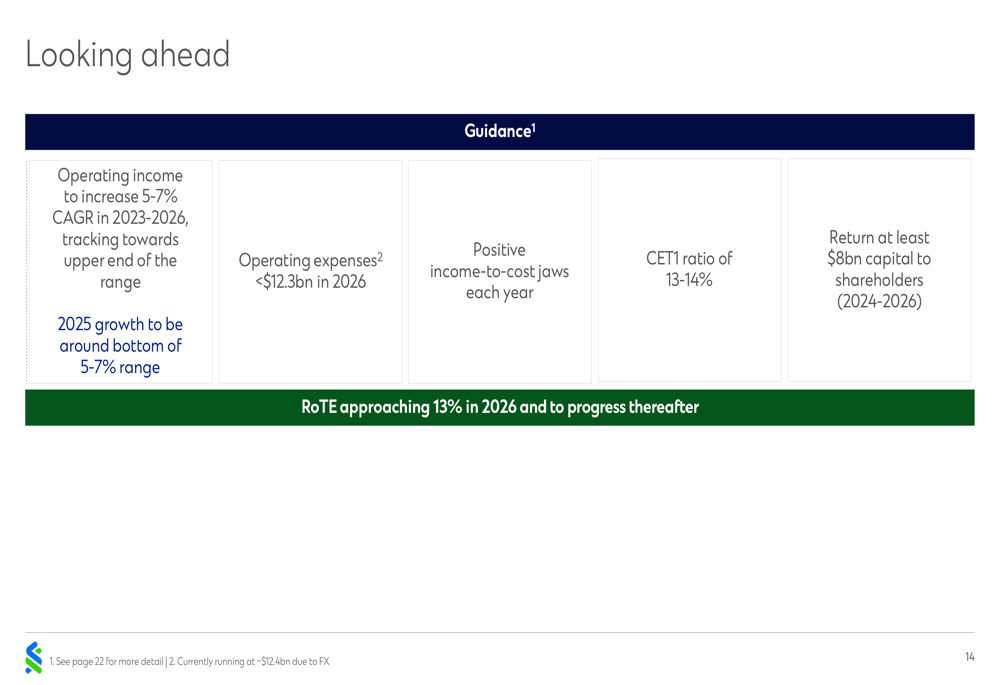

Standard Chartered has upgraded its 2025 income growth guidance to be around the bottom of the 5-7% range at constant currency, excluding notable items. This reflects confidence in the bank’s ability to continue growing despite challenges in the interest rate environment.

For the full year 2025, Net Interest Income is now expected to be down by a low single-digit percentage year-over-year, as the bank navigates through rates-driven margin compression and lower passthrough on deposits. However, this is expected to be more than offset by continued strong performance in non-interest income areas, particularly in Global Markets and Wealth Solutions.

The bank maintains its 2026 expense target of below $12.3 billion and expects positive income-to-cost jaws each year. It also reaffirmed its commitment to achieving a Return on Tangible Equity approaching 13% by 2026, with further progress expected thereafter.

Looking ahead, Standard Chartered remains confident in its long-term prospects while staying watchful of the external environment. The bank’s strategy of focusing on wealth management, transaction banking, and financial markets appears to be delivering results, positioning it well for continued growth despite macroeconomic uncertainties.

As CEO Bill Winters noted in the Q1 earnings call, "We are confident in our trajectory and in the long-term prospects for the group." The Q2 results appear to validate this confidence, with the bank demonstrating resilience and growth across its key business segments while maintaining a strong capital position and delivering substantial returns to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.