Trump administration authorizes CIA for covert action in Venezuela - Bloomberg

Introduction & Market Context

Starwood Property Trust (NYSE:STWD), a leading diversified finance company focused on the real estate and infrastructure sectors, reported solid second-quarter 2025 results according to its investor presentation released on August 7, 2025. The company demonstrated resilience through its multi-cylinder business model while continuing to strategically diversify its portfolio away from office properties.

Quarterly Performance Highlights

Starwood Property Trust reported GAAP earnings of $0.38 per diluted share and distributable earnings (DE) of $0.43 per diluted share for Q2 2025. The company maintained its consistent dividend policy, paying $0.48 per share for the quarter and declaring the same amount for Q3 2025. This marks over a decade of stable dividend payments, with total dividends paid or declared since inception reaching $8.4 billion.

As shown in the following earnings highlights, the company deployed significant capital during the quarter:

The company invested $3.2 billion in Q2 alone and $5.5 billion in the first half of 2025, already surpassing its total 2024 capital deployment. Since inception, Starwood has deployed $108 billion of capital and currently manages a portfolio exceeding $27 billion across debt and equity investments.

Strategic Portfolio Positioning

A key focus of Starwood’s strategy has been diversifying its portfolio to reduce exposure to potentially volatile sectors. The company’s total assets of $27.5 billion are strategically allocated across multiple property types and investment categories, with U.S. office representing only 9% of the diversified asset base (8% pro forma for the Fundamental acquisition).

The following chart illustrates the company’s diversified asset allocation:

Commercial loans comprise the largest portion at 56% of total assets, followed by residential lending (10%), infrastructure lending (11%), and owned properties (13%). Within the owned properties segment, multifamily represents 19%, highlighting the company’s focus on more stable property types.

This strategic shift is further evidenced in the commercial loan portfolio’s transformation over time:

The chart clearly demonstrates how Starwood has systematically reduced its exposure to office properties while increasing its allocation to multifamily assets, which now represent the largest property type in the portfolio. This transition positions the company to better weather market fluctuations and capitalize on stronger performing sectors.

Acquisition and Growth Initiatives

A significant development during the quarter was Starwood’s acquisition of Fundamental Income Properties, a $2.2 billion fully integrated net lease real estate operating platform and owned portfolio. This strategic acquisition expands the company’s capabilities and diversifies its revenue streams.

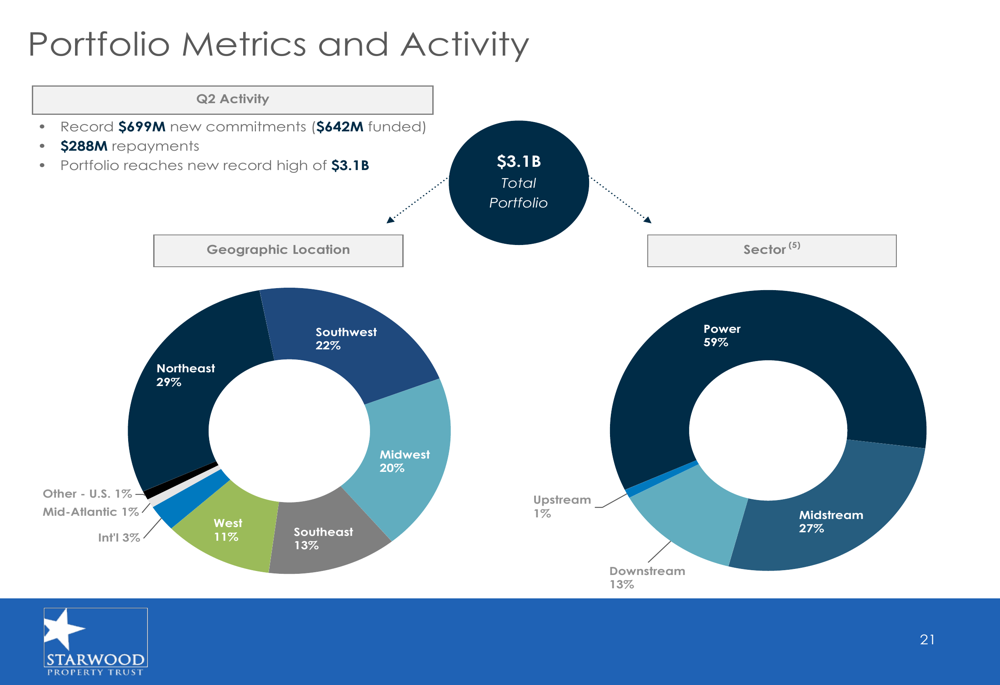

In the infrastructure lending segment, the company achieved record performance with $699 million in new commitments ($642 million funded) during Q2, bringing the portfolio to a new record high of $3.1 billion. The following chart shows the geographic and sector diversification of this growing segment:

The infrastructure portfolio maintains a balanced geographic distribution across the U.S., with the Northeast (29%), Southwest (22%), and Midwest (20%) representing the largest regions. By sector, power generation dominates at 59%, followed by midstream (27%) and downstream (13%) assets.

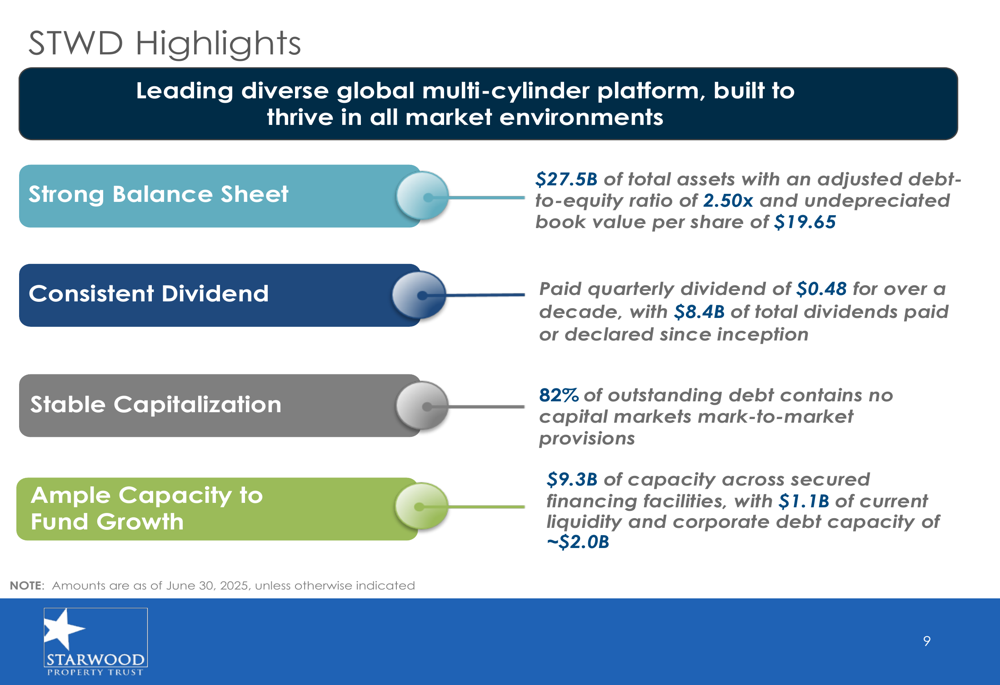

Balance Sheet and Capitalization

Starwood Property Trust maintains a strong balance sheet with $27.5 billion of total assets and an adjusted debt-to-equity ratio of 2.50x. The company’s undepreciated book value per share stands at $19.65.

The following slide highlights the company’s key credit metrics and capitalization structure:

A notable strength is that 82% of the company’s outstanding debt contains no capital markets mark-to-market provisions, providing stability in volatile market conditions. The company maintains ample capacity to fund growth with $9.3 billion available across secured financing facilities, $1.1 billion of current liquidity, and corporate debt capacity of approximately $2.0 billion.

Special Servicing and CMBS Business

Starwood’s special servicing business continues to perform well, with LNR’s commercial special servicer ratings of CSS1 and CS1 (the highest possible) reaffirmed by Fitch and Morningstar DBRS during the quarter. The company’s active servicing portfolio increased from $9.6 billion to $10.3 billion.

As illustrated in the following chart, the company’s special servicing business maintains a substantial presence in the CMBS market:

The company is named special servicer on 190 CMBS trusts with a loan balance of $102.1 billion. The active special servicing balance totals $10.3 billion, comprising $8.7 billion in special servicing loan balance and $1.6 billion in REO loan balance.

Forward-Looking Statements

Starwood Property Trust appears well-positioned for continued growth with its diversified business model and strong financial foundation. The company’s strategic reduction in office exposure and increased focus on multifamily and infrastructure assets should provide resilience against potential market headwinds.

The acquisition of Fundamental Income Properties represents a significant expansion opportunity, while record infrastructure lending commitments demonstrate the company’s ability to identify and capitalize on growth sectors. With substantial available liquidity and financing capacity, Starwood has the resources to pursue additional strategic investments while maintaining its consistent dividend policy.

As the real estate market continues to evolve, Starwood’s multi-cylinder platform and diversified approach position it to navigate changing conditions while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.