One & One Green Technologies stock soars 100% after IPO debut

Introduction & Market Context

Strauss Group (TASE:STRS) presented its Q2 and H1 2025 earnings results on August 26, 2025, showcasing significant operational improvements despite ongoing commodity price challenges. The stock traded down 1.41% following the presentation, a milder reaction compared to the 2.38% decline seen after Q1 results.

The food and beverage company delivered strong sales growth across key segments, with particularly impressive performance in its Coffee International division. This comes against a backdrop of extreme commodity price inflation, with Robusta coffee prices up 309%, Arabica coffee up 226%, and cocoa prices up 179% from their 2020 levels.

Quarterly Performance Highlights

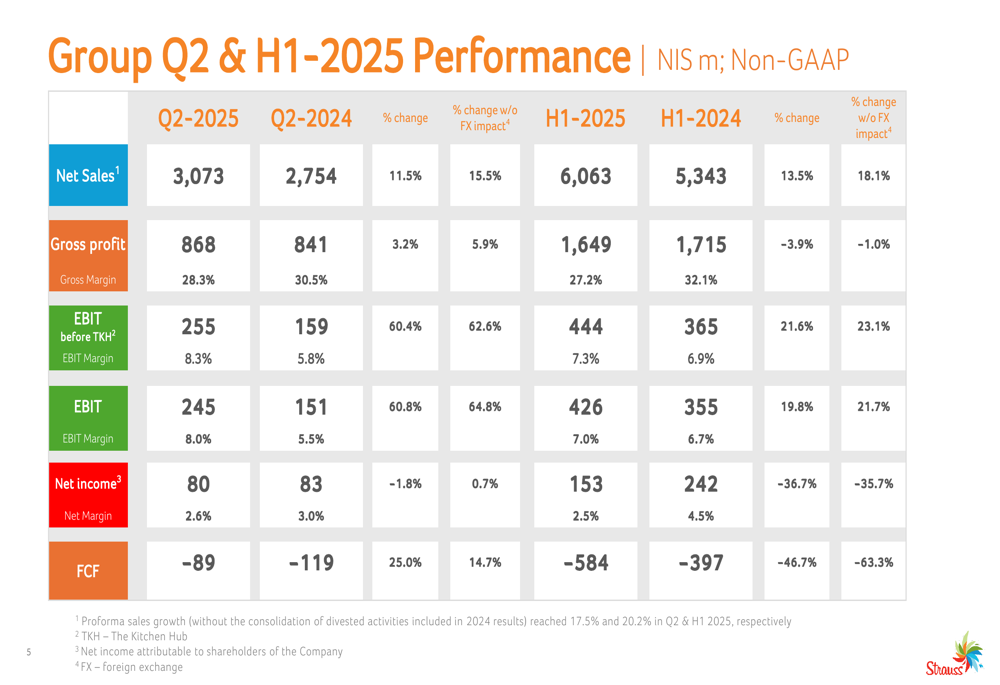

Strauss Group reported Q2 2025 net sales of NIS 3,073 million, representing an 11.5% increase year-over-year (15.5% excluding foreign exchange impact). More impressively, Q2 EBIT surged 60.8% to NIS 245 million, with EBIT margin expanding to 8.0% from 5.5% in the same period last year.

As shown in the following comprehensive financial performance table, the company’s first half results also showed solid improvement in most operational metrics:

Despite the strong operational performance, net income for Q2 2025 decreased slightly by 1.8% to NIS 80 million, while H1 net income fell more significantly by 36.7% to NIS 153 million. This decline was primarily attributed to higher financial expenses and increased tax payments, offsetting the operational improvements.

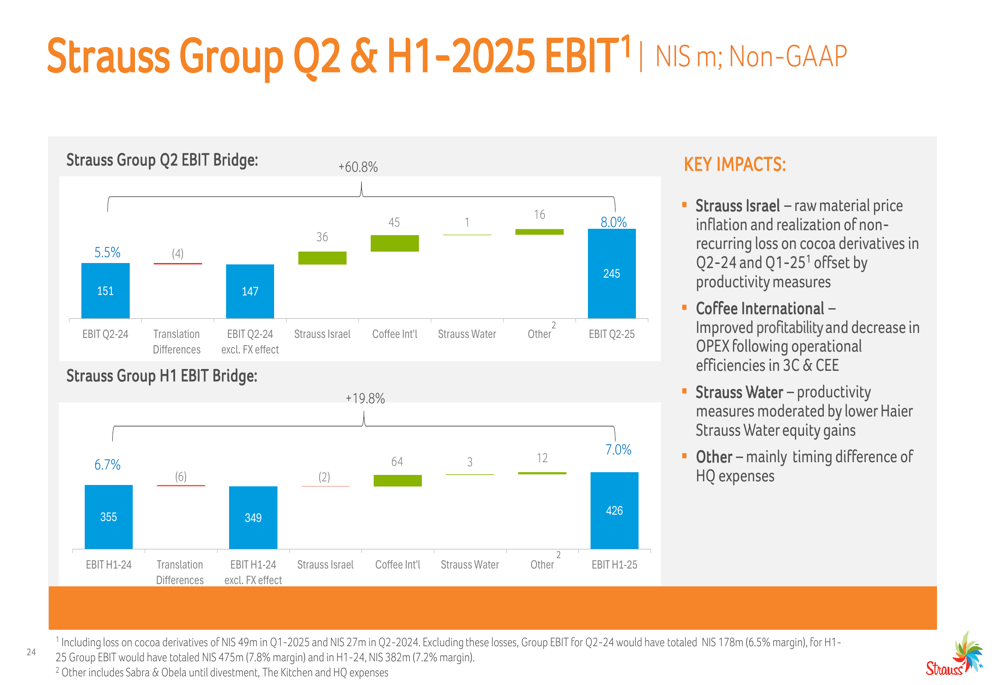

The following chart illustrates the key factors affecting the company’s EBIT performance in both Q2 and H1 2025:

Segment Analysis

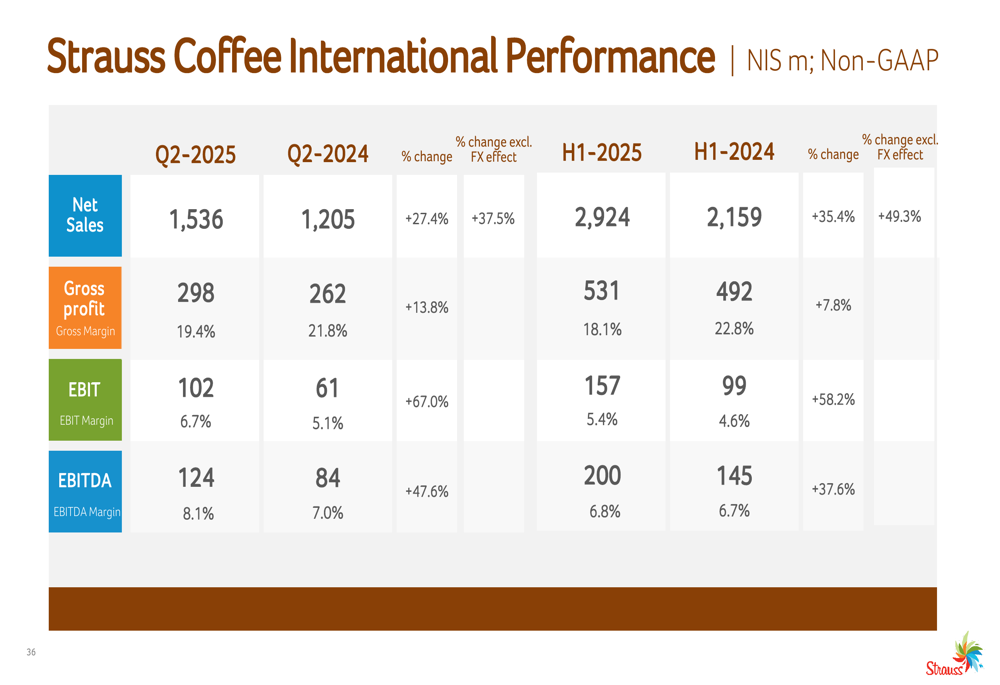

Coffee International emerged as the standout performer, with Q2 sales reaching NIS 1,536 million, a 27.4% increase year-over-year. The segment’s EBIT nearly doubled to NIS 102 million, with margins expanding to 6.7% from 5.1% in Q2 2024. This growth was achieved despite significant commodity price pressures.

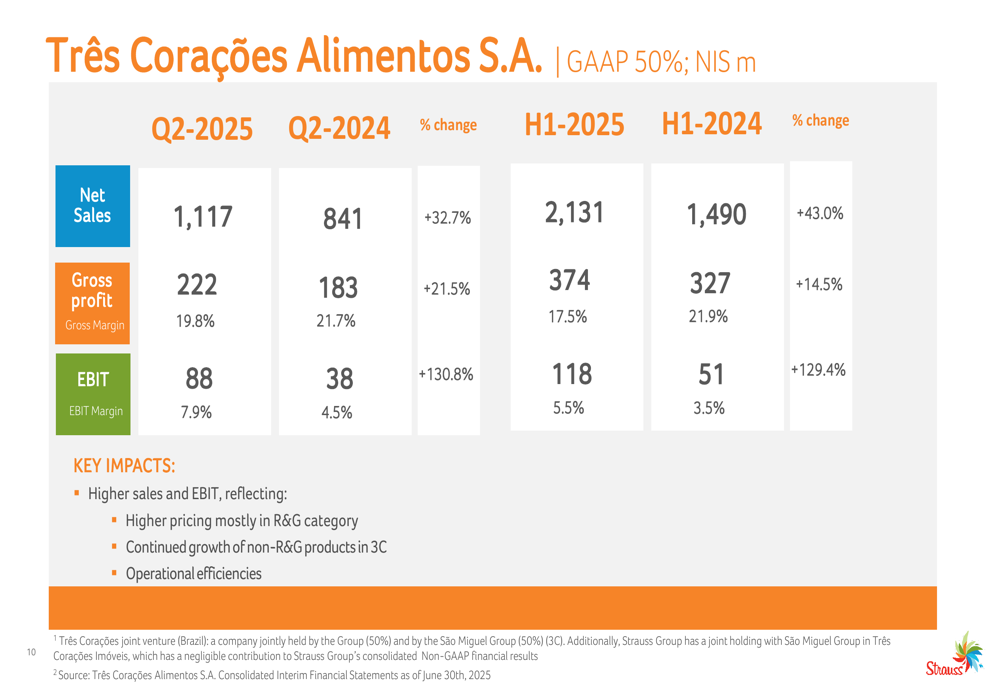

The Brazilian coffee business, Três Corações, delivered exceptional results with Q2 sales of BRL 3,536 million (up 49.7%) and EBIT of BRL 280 million (up 161.3%):

Strauss Israel also showed improvement, with Q2 sales increasing 8.9% to NIS 1,319 million and EBIT rising to NIS 135 million from NIS 99 million in Q2 2024. The segment’s EBIT margin expanded to 10.3% from 8.2%, reflecting successful pricing strategies and productivity initiatives to offset raw material inflation.

The Coffee International segment’s detailed performance metrics highlight the strong contribution from Brazil, which accounts for 72% of the division’s sales:

Strategic Initiatives and Outlook

Strauss Group continues to execute its "Double Down On The Core" strategy, focusing on three key pillars: strengthening its home base in Israel, expanding its Brazil coffee business, and growing as an international water player.

The company is on track to achieve NIS 300-400 million in run-rate savings by 2026 through its productivity initiatives, which include strategic procurement, operational excellence, revenue growth management, and capability building.

As illustrated in the following slide, Strauss Group has established clear long-term targets for 2026:

The company is also investing in future growth, with the recent launch of a new plant-based factory producing Alpro products and ongoing construction of a new facility at Yotvata expected to be completed by the end of 2025. These investments align with the company’s focus on expanding its core business segments, which are targeted to represent 85% of total sales by 2026.

Financial Position and Debt

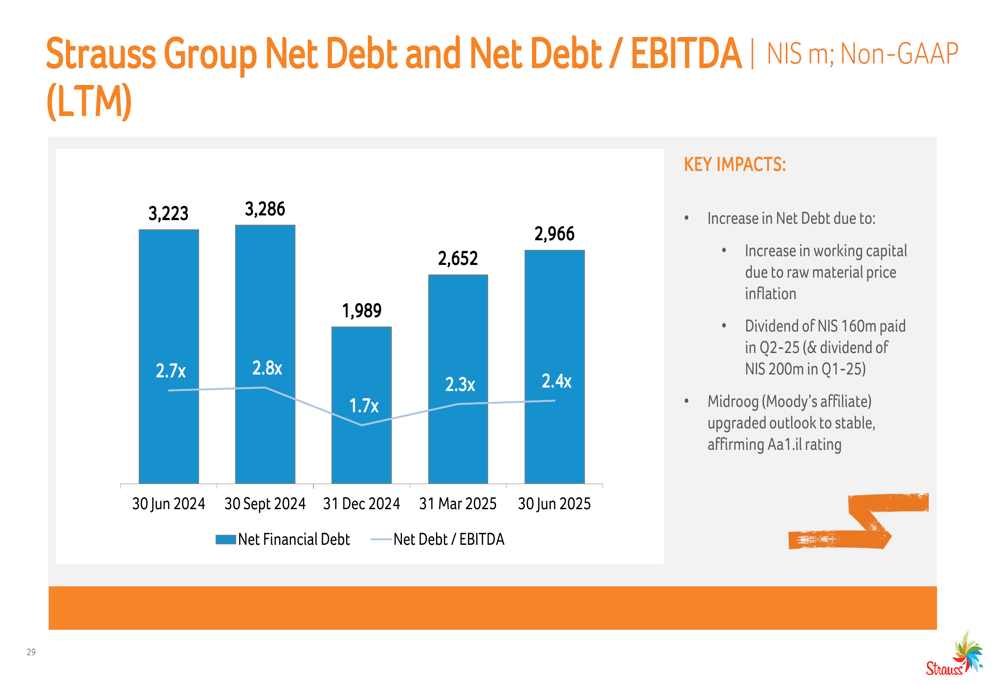

Strauss Group’s net financial debt stood at NIS 2,966 million as of June 2025, with a net debt to EBITDA ratio of 2.4x. While this represents an increase from December 2024’s 1.7x ratio, it remains within manageable levels and reflects increased working capital needs and dividend payments.

The following chart shows the evolution of the company’s debt position over the past year:

The company’s financial position was further strengthened by Midroog (Moody’s affiliate) upgrading its outlook to stable while affirming its Aa1.il rating. Additionally, Strauss successfully expanded its bonds series F by NIS 465 million with oversubscription, demonstrating strong market confidence.

Operating cash flow remained negative at NIS -89 million in Q2 2025, though this represented a 25% improvement compared to Q2 2024. The negative cash flow was primarily attributed to increased working capital requirements and higher finance payments.

While Strauss Group continues to face challenges from commodity price inflation and higher financial expenses, the Q2 2025 results demonstrate significant operational improvements and successful execution of the company’s strategic initiatives, positioning it well to achieve its long-term targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.