SoFi shares rise as record revenue, member growth drive strong Q3 results

Introduction & Market Context

Swisscom AG (OTC:SCMWY) (SWX:SCMN) presented its Q2 2025 results on August 7, 2025, revealing revenue and profitability declines across both its Swiss and Italian operations. Despite these challenges, Switzerland’s leading telecommunications provider maintained its full-year guidance and highlighted progress on strategic initiatives, including network expansion and the integration of its Italian acquisitions.

The company continues to face competitive pressures in both markets, with slight market share erosion in Switzerland and ongoing challenges in Italy. However, Swisscom (SIX:SCMN) emphasized its network leadership position and strong customer satisfaction metrics as key differentiators.

Quarterly Performance Highlights

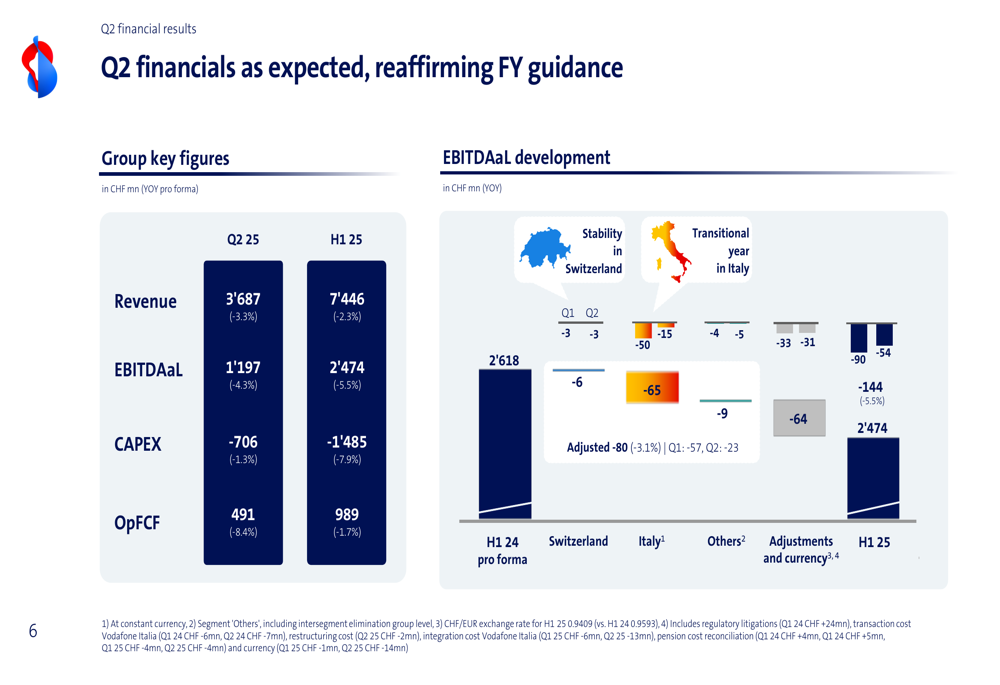

Swisscom reported Q2 2025 revenue of CHF 3,687 million, representing a 3.3% year-over-year decline. EBITDAaL (earnings before interest, taxes, depreciation, and amortization after leases) fell 4.3% to CHF 1,197 million. For the first half of 2025, revenue totaled CHF 7,446 million (-2.3%) with EBITDAaL of CHF 2,474 million (-5.5%).

As shown in the following financial summary:

The decline in EBITDAaL was attributed to challenges in both the Swiss and Italian markets, with currency effects also playing a role. This represents a steeper revenue decline compared to Q1 2025, when the company reported a 1% year-over-year decrease.

Despite these headwinds, Swisscom highlighted several positive developments, including recognition as the strongest telecom brand in Switzerland, winning a hotline test, and the successful launch of its "beem" service. The company also noted that integration and synergy efforts related to its Italian operations are progressing as planned.

Detailed Financial Analysis

Swisscom’s operational free cash flow (OpFCF) declined 8.4% year-over-year to CHF 491 million in Q2, with H1 OpFCF down 1.7% to CHF 989 million. Capital expenditures (CAPEX) decreased slightly by 1.3% to CHF 706 million in Q2, while H1 CAPEX fell 7.9% to CHF 1,485 million.

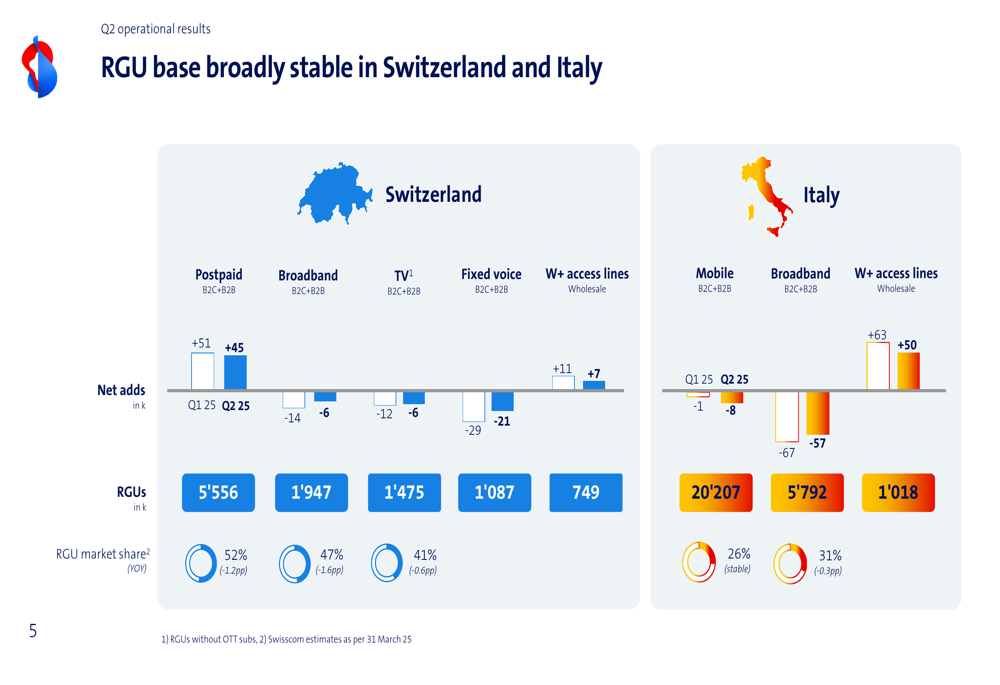

The company’s subscriber metrics showed mixed results. In Switzerland, postpaid mobile subscriptions continued to grow with 45,000 net additions in Q2, bringing the total to 5,556,000 subscribers. However, Swisscom faced declines in broadband (-6,000), TV (-6,000), and fixed voice (-21,000) connections. The Italian operations saw declines in both mobile (-8,000) and broadband (-57,000) subscribers.

The following chart illustrates the RGU (Revenue Generating Unit) trends in both markets:

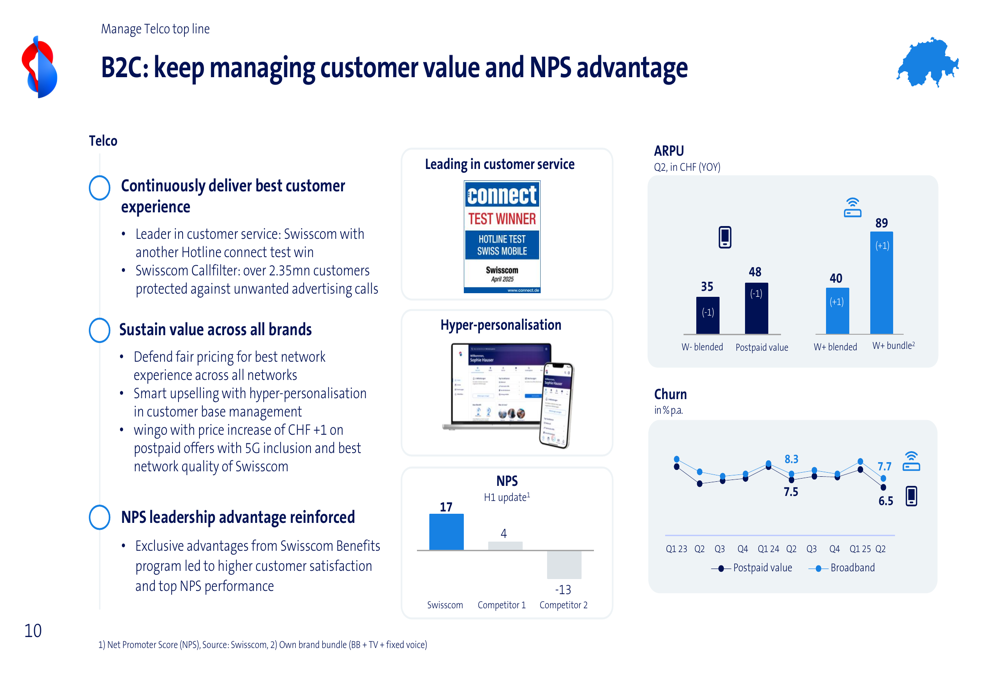

In the B2C segment, Swisscom is focusing on defending its RGU base through differentiation strategies, including reinforced brand awareness, family offerings, and promotional activities. The company reported stable ARPU (Average Revenue Per User) metrics, with postpaid value ARPU increasing slightly to CHF 48 (+1) in Q2.

Customer satisfaction remains a strong point for Swisscom, with a Net Promoter Score (NPS) of 17, significantly outperforming competitors who scored 4 and -13 respectively. The company also highlighted its success in managing churn rates.

Strategic Initiatives

Swisscom outlined its strategic priorities for both Switzerland and Italy. In Switzerland, the company aims to cement its #1 position by managing telco top-line revenue, executing cost transformation, and achieving profitable IT growth. In Italy, priorities include integrating Vodafone (NASDAQ:VOD) Italia, stabilizing B2C telco top-line, growing beyond the core business, and scaling up B2B IT and wholesale operations.

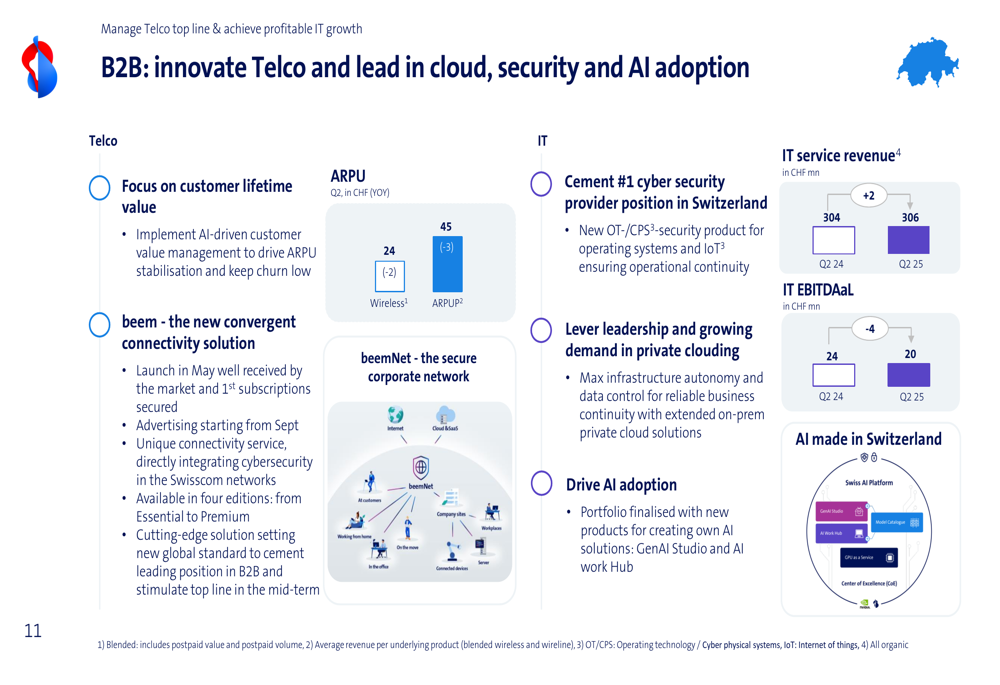

In the B2B segment, Swisscom is focusing on innovation in cloud services, security, and AI adoption. The company emphasized its position as Switzerland’s #1 cybersecurity provider and its leadership in private cloud solutions.

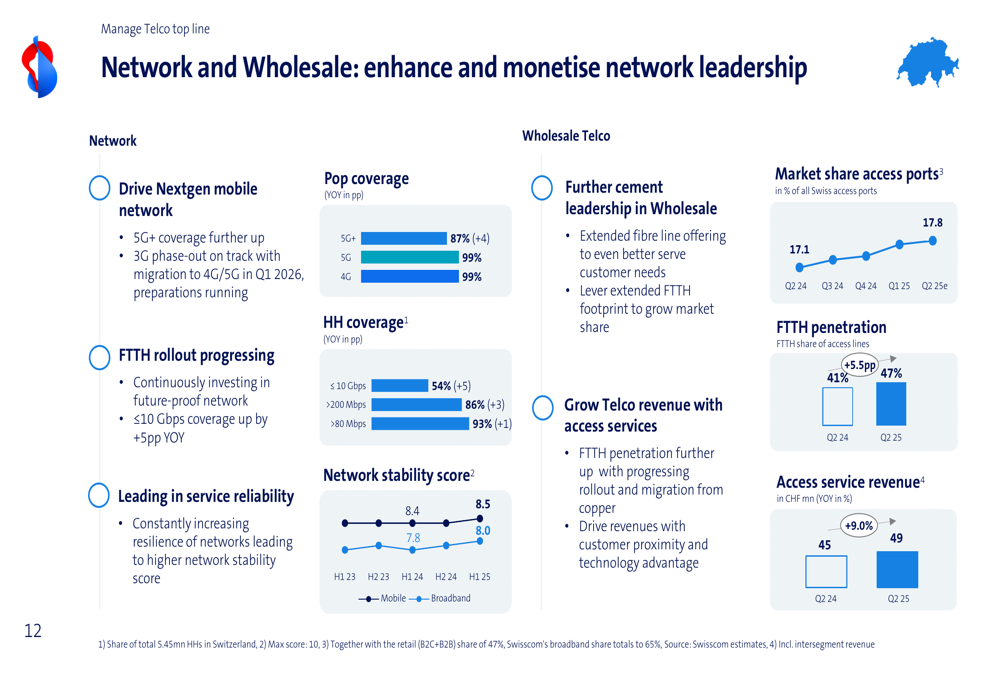

Network leadership remains a key strategic focus. Swisscom reported 5G+ coverage of 87% (+4pp year-over-year), with both 5G and 4G reaching 99% coverage. The company’s fiber-to-the-home (FTTH) rollout is progressing, with coverage increasing by 5 percentage points year-over-year.

Forward-Looking Statements

Despite the revenue and profitability declines in Q2, Swisscom confirmed its full-year 2025 guidance, projecting:

- Revenue of CHF 15.0-15.2 billion

- EBITDAaL of approximately CHF 5.0 billion

- CAPEX of CHF 3.1-3.2 billion

- OpFCF of CHF 1.8-1.9 billion

This guidance suggests the company expects improved performance in the second half of the year, particularly as integration and synergy efforts in Italy begin to yield results. The company specifically noted that these efforts are "progressing as planned" with synergy ramp-up on track for H2.

The maintained guidance comes despite increasing competitive pressures, as evidenced by Swisscom’s declining market shares in Switzerland: Postpaid mobile at 52% (-1.2pp YOY), Broadband at 47% (-1.6pp YOY), and TV at 41% (-0.6pp YOY). In Italy, mobile market share remained stable at 26%, while broadband market share declined slightly to 31% (-0.3pp YOY).

Given the performance in the first half of 2025, Swisscom will need to accelerate growth initiatives and cost optimization efforts to meet its full-year targets. The company’s ability to maintain pricing power while defending market share will be crucial factors to watch in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.