UnitedHealth tests AI system to streamline medical claims processing - Bloomberg

Introduction & Market Context

Synopsys Inc (NASDAQ:SNPS) presented its corporate overview for investors on September 9, 2025, highlighting the transformative impact of its Ansys acquisition and setting ambitious growth targets for fiscal year 2025. The presentation comes as the company’s stock trades near $609.08, showing a slight decline of 0.77% in regular trading but gaining 0.48% in after-hours activity.

The semiconductor design software leader positioned itself at the center of the $19.9 billion Electronic Design Automation (EDA) and Intellectual Property (IP) market, which serves as the foundation for the broader $677 billion semiconductor industry and $2.5 trillion electronic systems market.

Executive Summary

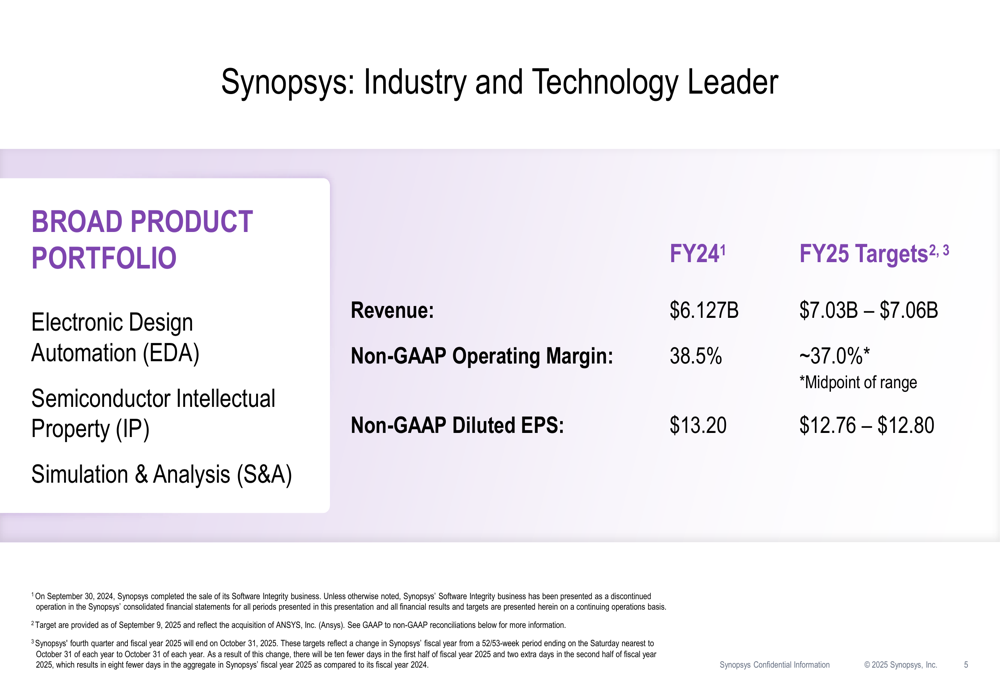

Synopsys reported solid FY24 results with revenue of $6.127 billion and is targeting significant growth in FY25, projecting revenue between $7.03 billion and $7.06 billion – representing approximately 15% year-over-year growth. This expansion is largely driven by the strategic acquisition of Ansys, combining Synopsys’ silicon design leadership with Ansys’ simulation and analysis expertise.

As shown in the following financial highlights slide, the company expects a slight decrease in non-GAAP operating margin from 38.5% in FY24 to approximately 37.0% in FY25, likely reflecting integration costs associated with the Ansys acquisition:

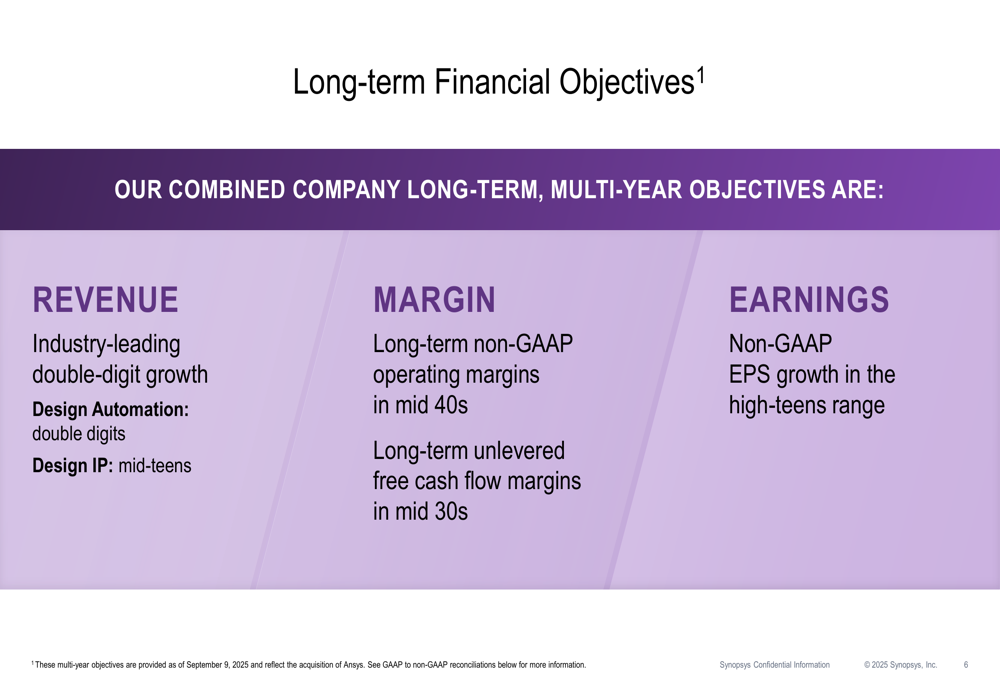

The company’s long-term financial objectives remain ambitious, with projections for industry-leading double-digit revenue growth and high-teens non-GAAP EPS growth over multiple years. Management expressed confidence in eventually achieving non-GAAP operating margins in the mid-40s and unlevered free cash flow margins in the mid-30s.

Strategic Initiatives

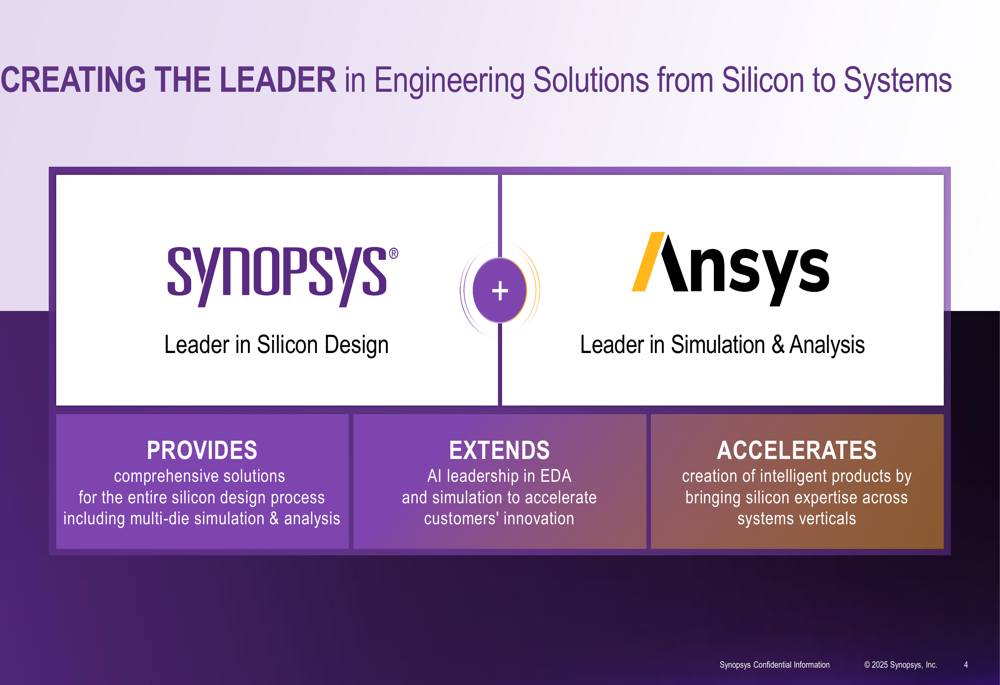

The cornerstone of Synopsys’ strategic vision is the combination with Ansys, creating what the company describes as "the leader in engineering solutions." This merger brings together Synopsys’ expertise in silicon design with Ansys’ capabilities in simulation and analysis, positioning the combined entity to accelerate innovation across the entire product development lifecycle.

As illustrated in the following slide, the strategic rationale for the merger centers on extending AI leadership in EDA and simulation while accelerating the creation of intelligent products:

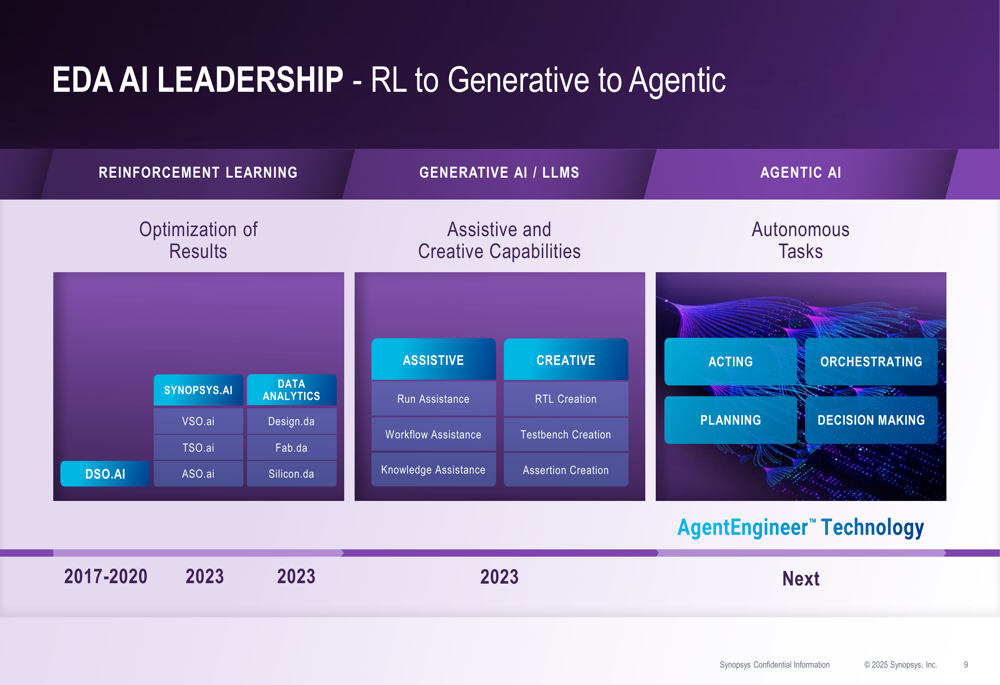

Artificial intelligence represents another key strategic focus, with Synopsys highlighting its evolution from early reinforcement learning applications to current generative AI capabilities and future agentic AI technologies. The company’s AI roadmap spans optimization tools like DSO.ai to assistive capabilities and autonomous engineering tasks through its AgentEngineer™ technology.

The company’s AI leadership progression is detailed in this comprehensive timeline:

Detailed Financial Analysis

Synopsys’ FY24 performance showed strong profitability with a non-GAAP operating margin of 38.5% and non-GAAP diluted EPS of $13.20. The GAAP to non-GAAP reconciliation reveals significant adjustments for stock-based compensation (10.7%) and acquisition-related items (2.3%), which elevated the operating margin from a GAAP figure of 22.1%.

For FY25, the company projects slight EPS compression to $12.76-$12.80, likely reflecting integration costs and increased share count following the Ansys acquisition. However, the absolute revenue growth of approximately $900 million demonstrates the significant scale benefits of the combined entity.

The company’s long-term financial objectives reflect management’s confidence in sustained growth across its portfolio:

These targets align with the company’s Q2 2025 earnings report, which showed a non-GAAP EPS of $3.67 (exceeding forecasts of $3.39) and strong 21% year-over-year growth in the Design IP segment – consistent with the "mid-teens" long-term growth objective for this business unit.

Competitive Industry Position

Synopsys emphasized its market leadership across multiple segments, positioning itself as the #1 player in EDA, Interface IP, Foundation IP, and Simulation & Analysis. The company highlighted its status as the #2 IP provider worldwide, with 26 years of investment in building its portfolio.

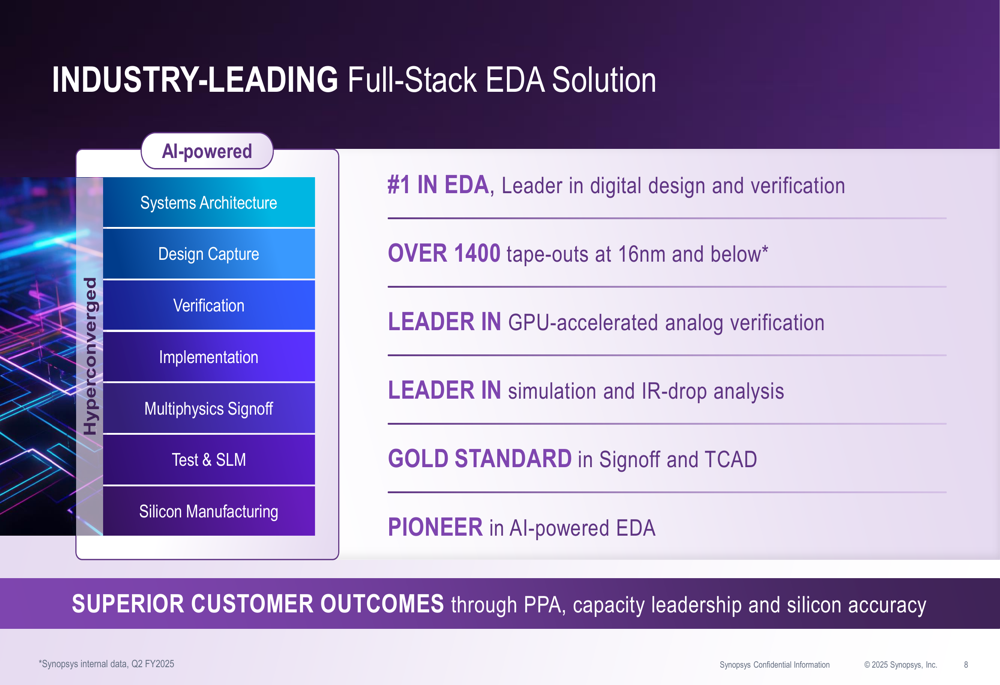

In the EDA space, Synopsys touts leadership in digital design and verification, with over 1,400 tape-outs at 16nm and below. The company also claims leadership in GPU-accelerated analog verification and simulation technologies:

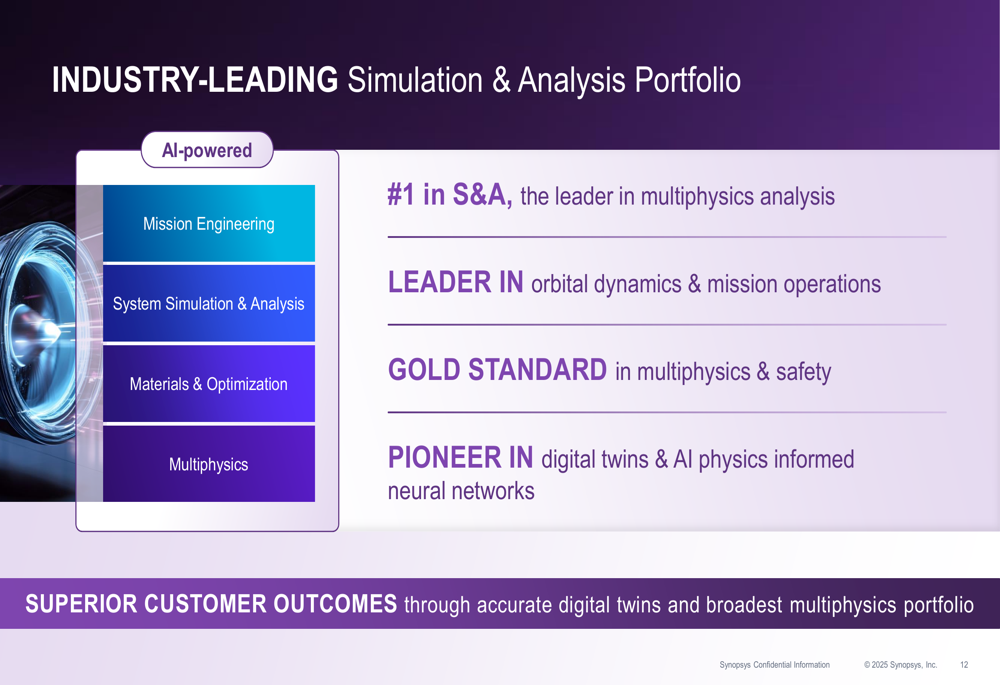

Following the Ansys acquisition, Synopsys has significantly strengthened its simulation and analysis capabilities, becoming the leader in multiphysics analysis and establishing pioneering positions in digital twins and AI physics-informed neural networks:

Forward-Looking Statements

Synopsys’ long-term vision centers on empowering innovation through its expanded technology portfolio. The company’s stated purpose is to "power innovation today that ignites the ingenuity of tomorrow," with a mission to "empower innovators to drive human advancement."

While the company projects confidence in its growth trajectory, investors should note the slight near-term margin pressure as the Ansys integration proceeds. The presentation’s forward-looking statements acknowledge potential risks related to U.S. and foreign trade regulations, government actions, and regulatory changes such as export control restrictions.

The company’s stock performance will likely depend on management’s ability to execute the Ansys integration efficiently while maintaining momentum in its core EDA and IP businesses. With AI-driven innovation accelerating across the semiconductor industry, Synopsys appears well-positioned to capitalize on increasing demand for advanced chip design tools and intellectual property.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.