Street Calls of the Week

Introduction & Market Context

Target Corporation (NYSE:TGT) shared its second quarter 2025 results on August 20, revealing modest improvements from the first quarter despite continuing challenges in overall sales performance. The retail giant’s stock plummeted over 10% in pre-market trading, reflecting investor concerns about the company’s ability to return to growth in a challenging consumer environment.

The presentation comes as Target navigates a complex retail landscape characterized by cautious consumer spending and heightened competition. Despite beating earnings expectations by a slim margin, with EPS of $2.05 versus the forecast of $2.04, the market reaction suggests investors were looking for stronger signals of a turnaround.

Quarterly Performance Highlights

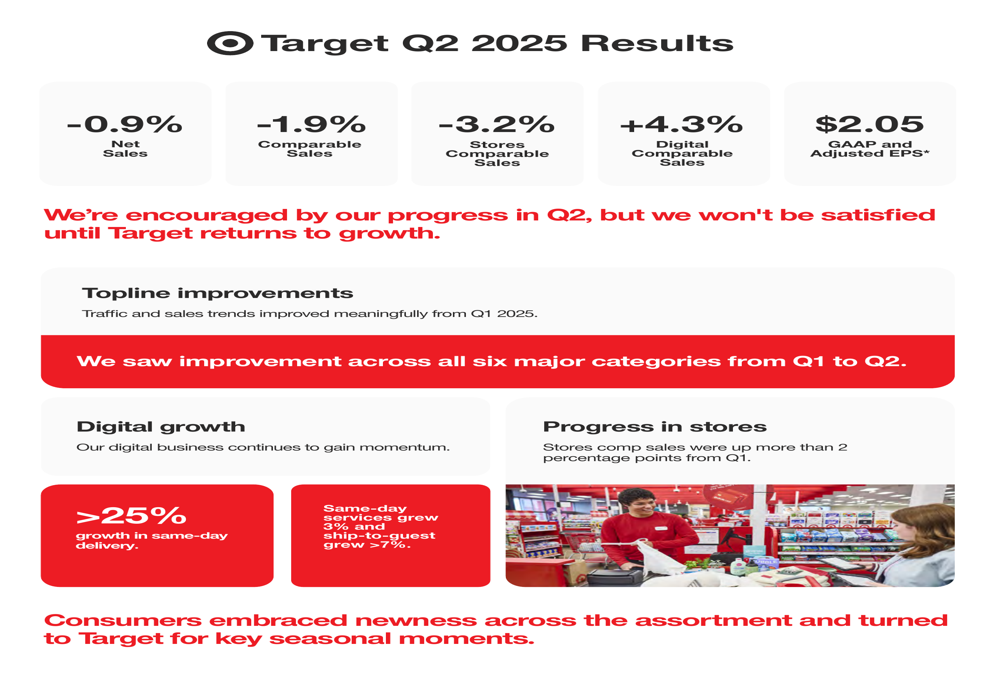

Target’s Q2 2025 results showed a mixed performance with net sales declining 0.9% year-over-year and comparable sales falling 1.9%. However, the company emphasized that these figures represent a meaningful improvement from Q1 2025 performance. Store comparable sales declined 3.2%, while digital comparable sales provided a bright spot with 4.3% growth.

As shown in the company’s quarterly results summary:

The presentation highlighted improved traffic and sales trends from Q1 across all six major merchandise categories. Digital channels continued to show momentum, with same-day delivery growing more than 25%, same-day services up 3%, and ship-to-guest orders increasing more than 7%. In-store comparable sales improved by more than 2 percentage points compared to the first quarter.

Despite these improvements, Target’s leadership acknowledged that they "won’t be satisfied until Target returns to growth," indicating awareness that the current trajectory, while improving, still falls short of the company’s long-term objectives.

Growth Drivers and Success Areas

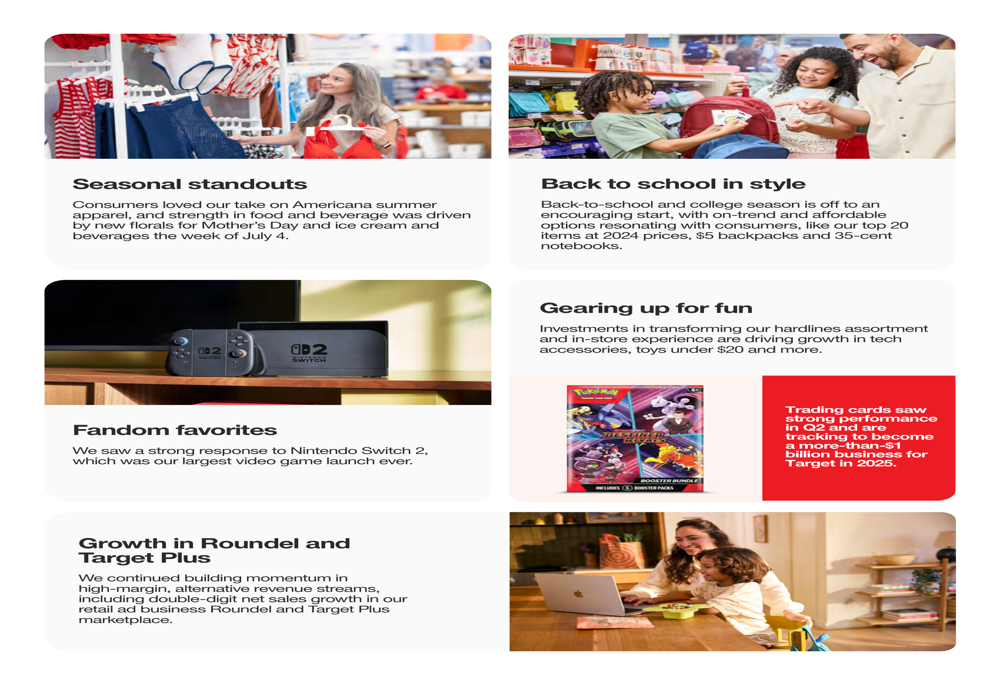

Target identified several key drivers behind its Q2 performance, including strong seasonal merchandise sales and back-to-school initiatives. The company emphasized its focus on affordable offerings, maintaining 2024 prices on top 20 back-to-school items, $5 backpacks, and 35-cent notebooks to attract value-conscious shoppers.

The presentation highlighted several bright spots in the business:

Trading cards emerged as a particularly strong category, with the company noting they are tracking to become a more-than-$1 billion business for Target in 2025. The Nintendo Switch 2 launch also drove significant consumer interest and sales.

Alternative revenue streams showed promising growth, with the retail advertising business Roundel and Target Plus marketplace both delivering double-digit net sales growth. These high-margin businesses represent an increasingly important component of Target’s overall strategy as traditional retail faces headwinds.

Strategic Initiatives and Future Plans

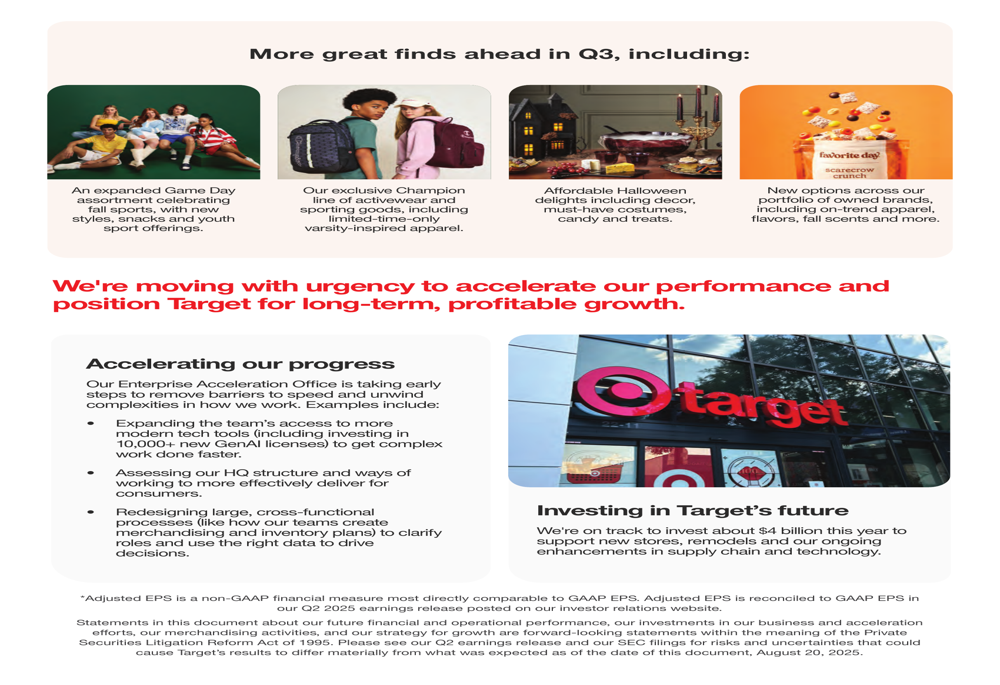

Looking ahead to Q3, Target outlined several initiatives aimed at driving traffic and sales, including an expanded Game Day assortment, an exclusive Champion line of activewear and sporting goods, and affordable Halloween merchandise.

The company is also focusing on operational improvements to accelerate performance and position for long-term, profitable growth. These efforts include removing barriers to speed, unwinding complexities, and expanding access to modern technology tools, including investing in 10,000+ new GenAI licenses.

Target plans to invest approximately $4 billion this year to support new stores, remodels, and enhancements in supply chain and technology infrastructure. This substantial capital expenditure underscores the company’s commitment to long-term growth despite current challenges.

Market Reaction and Analyst Perspectives

Despite the modest earnings beat, Target’s stock dropped sharply in pre-market trading, falling 10.54% to $94.25 from the previous close of $105.36. This reaction suggests investors remain concerned about the company’s overall trajectory and the continued decline in comparable sales, even as management points to sequential improvement.

The stock has been volatile over the past year, trading between a 52-week high of $167.4 and a low of $87.35. According to available data, Target maintains a P/E ratio of 11.52x, which some analysts consider undervalued relative to its historical average and industry peers.

During the earnings call, incoming CEO Michael Fidelke emphasized flexibility in retail, stating, "Retail’s about being flexible. Retail’s about being nimble in response to opportunities." He also highlighted style and design as core elements of Target’s strategy moving forward.

While Target maintained its full-year guidance, anticipating a low single-digit sales decline and GAAP EPS ranging from $8 to $10, the market reaction indicates investors may require more convincing evidence of a sustainable turnaround before regaining confidence in the company’s growth prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.