Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Introduction & Market Context

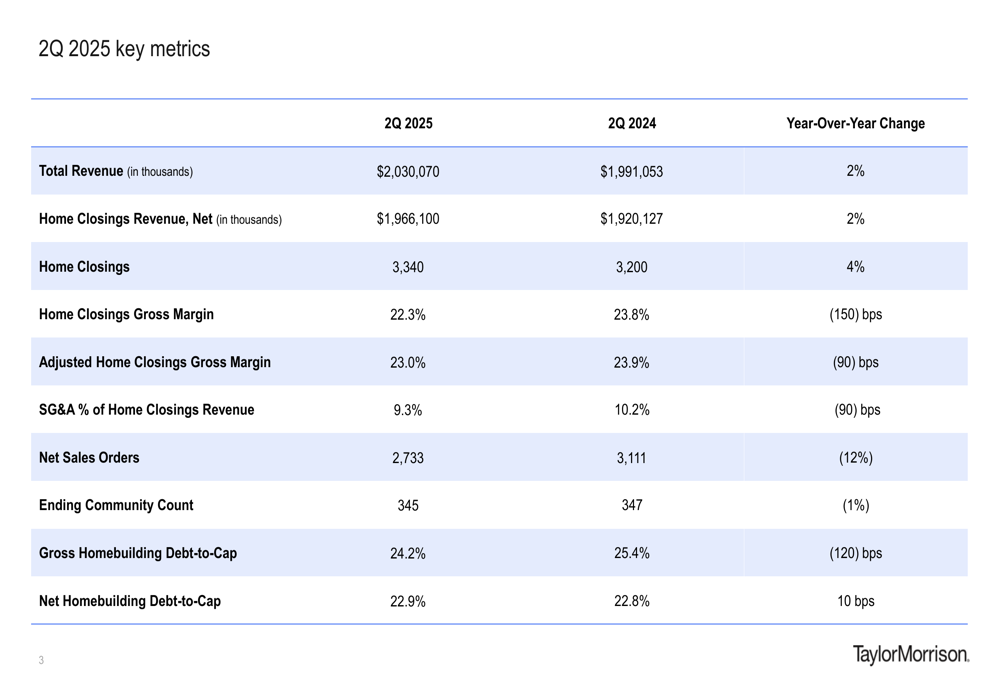

Taylor Morrison Home Corporation (NYSE:TMHC) released its second quarter 2025 investor presentation on July 23, showing modest revenue growth despite challenging market conditions. The homebuilder reported a 2% year-over-year increase in total revenue to $2.03 billion, with home closings up 4% to 3,340 units. However, net sales orders declined 12% compared to the same period last year, reflecting a softer spring selling season.

The company’s stock closed at $60.60 following the earnings release, representing a 3.69% increase, as investors responded positively to the company’s ability to navigate market headwinds while maintaining strong capital efficiency and liquidity.

Quarterly Performance Highlights

Taylor Morrison’s Q2 2025 results showed mixed performance across key metrics. While home closings volume increased, the company experienced margin pressure compared to the previous year.

As shown in the detailed quarterly comparison, home closings revenue reached $1.97 billion, up 2% from Q2 2024. The company’s home closings gross margin decreased by 150 basis points year-over-year to 22.3%, while adjusted home closings gross margin declined by 90 basis points to 23.0%. SG&A as a percentage of home closings revenue improved to 9.3%, down 90 basis points from the prior year, demonstrating enhanced operational efficiency.

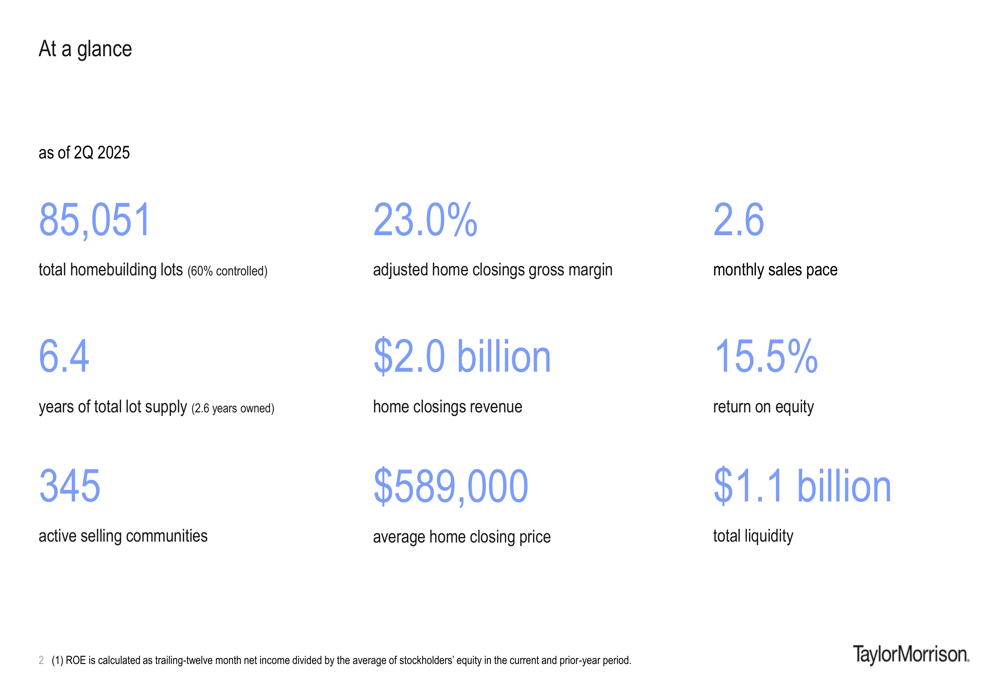

The average home closing price for the quarter was $589,000, with the company maintaining a monthly sales pace of 2.6 homes per community. Taylor Morrison ended the quarter with 345 active communities, a slight decrease from 347 in the same period last year.

The company’s financial position remains solid with total liquidity of $1.1 billion and a return on equity of 15.5%. Taylor Morrison’s land portfolio consists of 85,051 total homebuilding lots, with 60% controlled rather than owned, reflecting the company’s strategic shift toward a more capital-efficient land approach.

Strategic Initiatives

Taylor Morrison continues to execute on its land-lighter investment strategy, increasing the percentage of controlled lots while reducing owned inventory. This approach aims to optimize capital efficiency while maintaining sufficient inventory for future growth.

As illustrated in the land portfolio overview, the company has steadily increased its controlled lot percentage from 53% in Q4 2023 to 60% in Q2 2025, while reducing owned lots from 47% to 40% during the same period. Total homebuilding land investment was $612 million in Q2 2025, with 43% of spending related to development activities. The company maintains 6.4 years of total lot supply, with 2.6 years of owned lots.

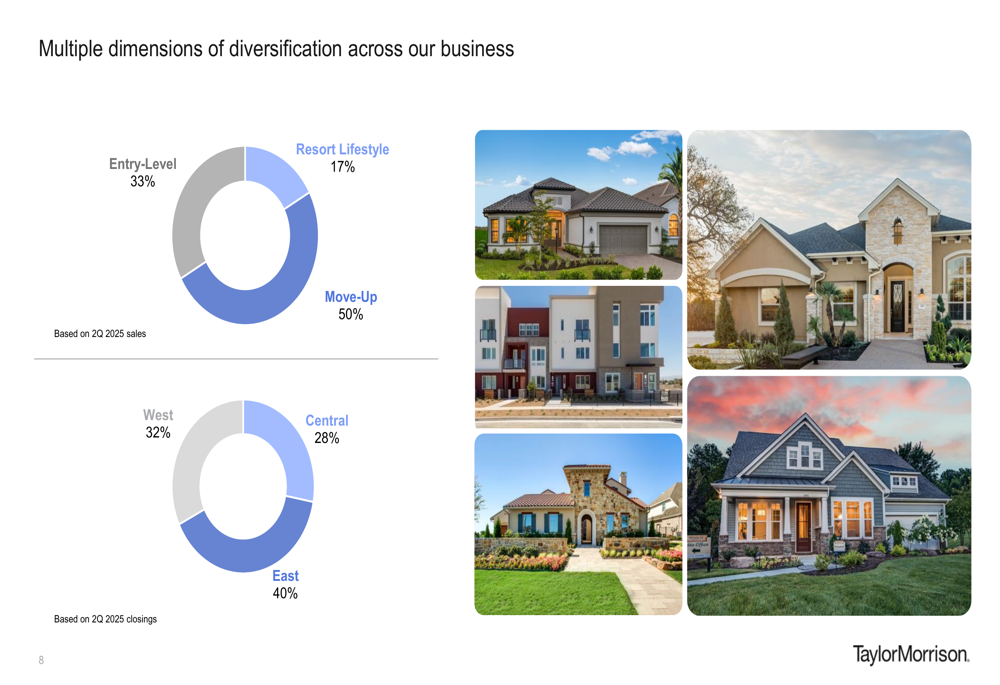

The company’s product diversification strategy continues to provide resilience against market fluctuations. Taylor Morrison maintains a balanced portfolio across consumer segments and geographic regions.

The product mix includes entry-level homes (33% of sales), move-up homes (50%), and resort lifestyle communities (17%). Geographically, home closings are distributed across the East (40%), West (32%), and Central (28%) regions, providing diversification against regional market variations.

Taylor Morrison’s premium Esplanade brand continues to outperform the company average, commanding significant price and margin premiums.

The Esplanade brand achieves an average sales price of $779,000, 35% higher than other Taylor Morrison homes, and delivers an impressive 31% home closings gross margin, 800 basis points above the company average. The brand also generates substantially higher option and lot premiums per home.

Capital Allocation & Financial Position

Taylor Morrison maintains a disciplined approach to capital allocation, with a strong balance sheet and active share repurchase program.

The company’s capital position includes $1.1 billion in total liquidity, comprising $130 million in unrestricted cash and $952 million in revolving credit facility capacity. The net homebuilding debt-to-capital ratio stands at 22.9%, reflecting conservative leverage. Taylor Morrison has repurchased $235 million of common stock in the first half of 2025 and expects to repurchase at least $350 million for the full year, with $675 million remaining under the current authorization.

The company’s senior note maturity schedule is well-structured, with no maturities until 2027, providing financial flexibility in the near term.

Forward-Looking Statements

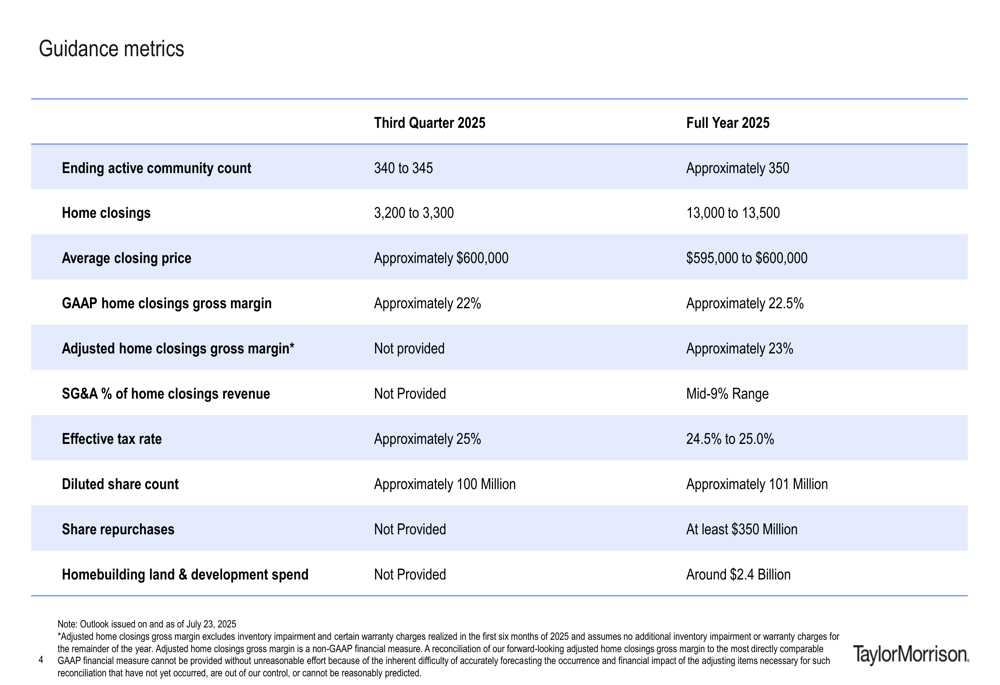

Taylor Morrison provided guidance for both the third quarter and full year 2025, maintaining a cautiously optimistic outlook despite current market challenges.

For the third quarter of 2025, the company expects an ending active community count of 340-345, home closings of 3,200-3,300, and an average closing price of approximately $600,000. GAAP home closings gross margin is projected at approximately 22%, with an effective tax rate of approximately 25%.

For the full year 2025, Taylor Morrison anticipates approximately 350 active communities, 13,000-13,500 home closings, and an average closing price of $595,000-$600,000. The company expects a GAAP home closings gross margin of approximately 22.5% and an adjusted home closings gross margin of approximately 23%. SG&A as a percentage of home closings revenue is projected in the mid-9% range.

Competitive Industry Position

Taylor Morrison has established several competitive advantages that position the company for long-term success in the homebuilding industry.

Key differentiators include the company’s diversified consumer groups and price points, community-focused land development expertise, prime submarket locations, consumer-centric approach, and scale advantages at national, regional, and local levels. The company also benefits from a well-capitalized balance sheet, wholly-owned financial services, and its recognition as America’s Most Trusted® builder.

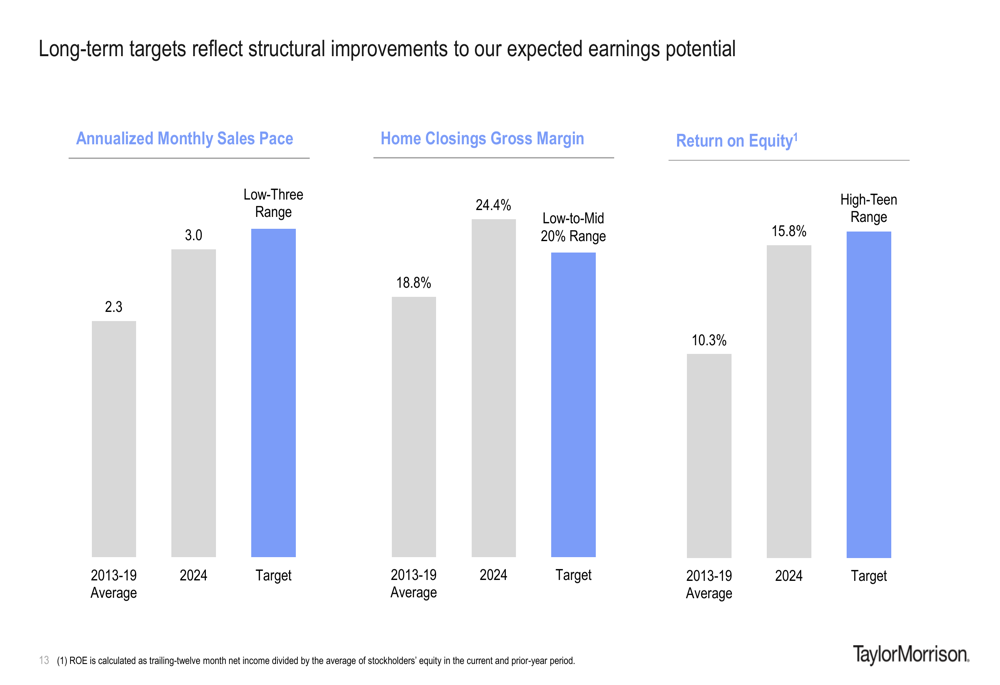

Looking ahead, Taylor Morrison has established ambitious long-term financial targets that build on its historical performance.

The company aims to achieve an annualized monthly sales pace in the low-three range, compared to its 2024 performance of 3.0 and 2013-19 average of 2.3. For home closings gross margin, Taylor Morrison targets the low-to-mid 20% range, building on its 2024 result of 24.4%. The return on equity target is set in the high-teen range, an improvement from the 2024 figure of 15.8%.

These targets reflect Taylor Morrison’s confidence in its strategic positioning and operational capabilities, even as it navigates current market uncertainties and evolving consumer preferences in the homebuilding sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.